Fermented Ingredients Market Size

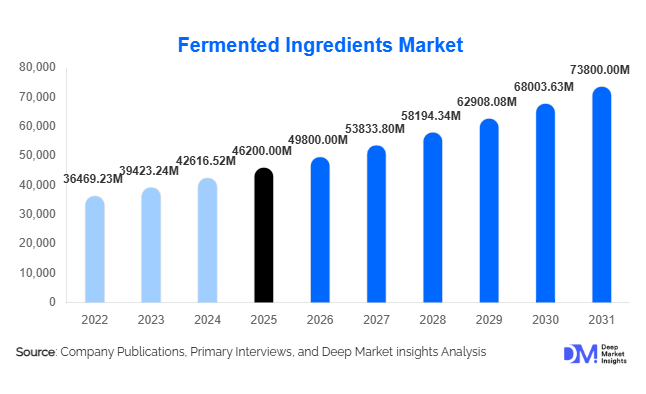

According to Deep Market Insights, the global fermented ingredients market size was valued at USD 46,200 million in 2025 and is projected to grow from USD 49,800 million in 2026 to reach USD 73,800 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The fermented ingredients market growth is primarily driven by rising demand for natural and clean-label ingredients, increasing adoption of bio-based manufacturing processes, and the expanding use of fermented components across food & beverages, animal nutrition, pharmaceuticals, and industrial biotechnology applications.

Key Market Insights

- Fermented organic acids and amino acids dominate global demand, supported by their widespread use in food preservation, feed efficiency enhancement, and industrial processing.

- Asia-Pacific leads the global market, accounting for the largest share due to large-scale fermentation capacity in China, Japan, and India.

- Fed-batch fermentation technology remains the most widely adopted, driven by superior yield control and cost efficiency.

- Food & beverage applications represent the largest consumption segment, fueled by clean-label trends and growth in processed foods.

- Animal nutrition is the fastest-growing application, supported by rising global meat consumption and feed optimization requirements.

- Precision fermentation and strain engineering are emerging as key technological differentiators among leading manufacturers.

What are the latest trends in the fermented ingredients market?

Expansion of Precision Fermentation Technologies

Precision fermentation is reshaping the fermented ingredients market by enabling the production of high-purity amino acids, enzymes, vitamins, and bioactive compounds with improved efficiency. Companies are increasingly investing in genetically optimized microbial strains and AI-driven fermentation controls to increase yields, shorten production cycles, and reduce energy consumption. This trend is particularly prominent in enzyme and specialty ingredient manufacturing, where consistency and scalability are critical. Precision fermentation is also supporting the development of novel ingredients for functional foods, nutraceuticals, and pharmaceutical applications.

Rising Adoption of Clean-Label and Natural Ingredients

Global consumer preference for clean-label products is accelerating the shift from chemically synthesized additives to naturally fermented alternatives. Food and beverage manufacturers are increasingly reformulating products to include fermented organic acids, natural preservatives, and fermentation-derived flavor enhancers. This trend is reinforced by stricter regulatory frameworks in North America and Europe, which favor bio-based and non-synthetic ingredients. As a result, fermented ingredients are becoming central to clean-label product innovation across multiple end-use industries.

What are the key drivers in the fermented ingredients market?

Growing Demand from the Food & Beverage Industry

The food processing industry is the largest driver of fermented ingredient demand, accounting for nearly 40% of total market consumption in 2025. Fermented acids, enzymes, and microbial cultures are widely used in bakery, dairy, beverages, and processed foods to improve shelf life, flavor, texture, and nutritional value. Rapid urbanization, rising consumption of convenience foods, and increasing focus on functional nutrition are further strengthening demand.

Expansion of the Global Animal Nutrition Sector

The animal feed industry is one of the fastest-growing demand centers for fermented ingredients. Amino acids, enzymes, and probiotics derived through fermentation improve feed efficiency, animal health, and growth performance. Rising global meat and dairy consumption, particularly in Asia-Pacific and Latin America, is driving sustained growth in this segment. Regulatory restrictions on antibiotic growth promoters are also accelerating the adoption of fermentation-based feed additives.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fermented ingredient production relies heavily on carbohydrate-rich feedstocks such as corn, sugar, and molasses. Price volatility in these raw materials directly impacts production costs and profit margins, posing a significant challenge for manufacturers. Fluctuations in agricultural output, trade policies, and energy prices further intensify cost pressures.

High Capital and Technical Barriers

Establishing large-scale fermentation facilities requires substantial capital investment, advanced process control systems, and specialized technical expertise. These barriers limit entry for smaller players and can slow capacity expansion, particularly in regions with limited biotechnology infrastructure.

What are the key opportunities in the fermented ingredients industry?

Precision Nutrition and Functional Ingredients

The growing focus on personalized nutrition and functional health solutions presents significant opportunities for fermented ingredient manufacturers. Fermented probiotics, amino acids, and bioactive compounds are increasingly incorporated into products targeting gut health, immunity, metabolic wellness, and cognitive performance. This trend enables manufacturers to access premium, high-margin segments.

Emerging Market Expansion

Rapid industrialization and food processing expansion in emerging economies such as India, Vietnam, Brazil, and Indonesia offer strong growth opportunities. Government incentives, rising domestic consumption, and increasing foreign direct investment are supporting the development of local fermentation infrastructure, reducing dependence on imports and improving supply chain efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46200 Million |

| Market Size in 2026 | USD 49800 Million |

| Market Size in 2031 | USD 73800 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

Organic acids represent the largest ingredient type segment, accounting for approximately 32% of the global fermented ingredients market in 2025. Their dominance is driven by extensive use in food preservation, animal feed, and industrial applications. Amino acids follow closely, supported by strong demand from the feed and pharmaceutical industries. Enzymes and vitamins represent high-value segments, benefiting from growth in biotechnology, pharmaceuticals, and specialty food applications. Microbial biomass, including probiotics and yeast, is gaining traction due to increasing focus on gut health and functional foods.

Application Insights

Food and beverage applications continue to dominate the global fermented ingredients market, capturing a 38% share in 2025. This dominance is primarily driven by the growing emphasis on clean-label reformulation, natural preservation, and flavor enhancement in processed foods. Manufacturers are increasingly incorporating fermented organic acids, enzymes, and microbial cultures to improve shelf life, texture, and nutritional value while complying with stricter consumer and regulatory demands for bio-based ingredients. The animal nutrition segment represents the fastest-growing application, expanding at a robust 9% CAGR, underpinned by rising global meat and dairy consumption, intensification of livestock farming, and the need for feed additives that enhance conversion efficiency and animal health. Pharmaceutical applications are steadily expanding, particularly for fermentation-derived vitamins, amino acids, and bioactive intermediates used in nutraceuticals and APIs. Additionally, industrial applications such as bio-based chemicals, biodegradable polymers, and specialty enzymes are emerging as long-term growth avenues, driven by sustainability mandates and the transition toward circular economies in chemicals and materials.

End-Use Industry Insights

The food processing industry remains the largest end-use sector for fermented ingredients, bolstered by the dual drivers of increasing consumer demand for functional foods and the need for natural preservatives and flavor enhancers in processed products. The animal feed industry follows closely, fueled by the global expansion of livestock production, stringent regulatory pressure to reduce synthetic growth promoters, and growing adoption of probiotic- and amino acid-enriched feeds. Pharmaceutical and biotechnology industries are high-value end-users, with increasing use of fermentation-derived vitamins, amino acids, and enzyme intermediates to support advanced therapeutics, functional supplements, and high-purity APIs. Industrial biotechnology applications, including bio-based chemicals and sustainable materials, are gradually contributing more to the overall market, reflecting the increasing shift toward environmentally friendly production and low-carbon footprint processes.

Explore more data points, trends and opportunities Download Free Sample Report

Fermented Ingredients Market Segmentations

By Ingredient Type

- Organic Acids

- Amino Acids

- Vitamins

- Industrial Enzymes

- Microbial Biomass

By Fermentation Process

- Batch Fermentation

- Fed-Batch Fermentation

- Continuous Fermentation

By Microorganism Type

- Bacteria-Based Fermentation

- Yeast-Based Fermentation

- Fungi-Based Fermentation

By Application

- Food & Beverage

- Animal Nutrition & Feed Additives

- Pharmaceuticals & Nutraceuticals

- Industrial Biotech & Bio-Based Chemicals

- Personal Care & Cosmetics

By End-Use Industry

- Food Processing Industry

- Animal Feed Industry

- Pharmaceutical & Biotechnology Industry

- Industrial Biotechnology & Sustainable Materials

Regional Insights

Asia-Pacific

Asia-Pacific leads the global fermented ingredients market with approximately 38% market share in 2025. China dominates the region, accounting for nearly 18% of global demand, due to its large-scale production of amino acids, organic acids, and vitamins for both domestic consumption and export. The regional growth is driven by the rapid expansion of food processing industries, government incentives for biotechnology and precision fermentation, and increasing investment in livestock and feed production. India, Japan, and South Korea are also key markets, supported by rising disposable incomes, expanding functional food consumption, and strong government policies promoting innovation and R&D in fermentation-based technologies. The high adoption of advanced fermentation processes and increasing focus on clean-label ingredients further reinforce regional demand.

North America

North America holds around 24% of the global market, led by the United States. Growth in this region is driven by robust demand for functional foods, beverages, and nutraceuticals, coupled with advanced biotechnology infrastructure and high adoption of precision fermentation technologies. The increasing trend toward natural and sustainable food ingredients, along with rising investment in industrial fermentation and enzyme production, supports market expansion. Additionally, the demand for fermented feed additives in the livestock and aquaculture sectors is contributing to steady regional growth.

Europe

Europe accounts for approximately 22% of global demand, with Germany, France, and the Netherlands serving as major contributors. Market growth in the region is fueled by stringent regulatory standards favoring natural and sustainable ingredients, widespread adoption of functional and clean-label foods, and the increasing use of fermentation-derived vitamins, enzymes, and amino acids in pharmaceutical applications. The strong presence of multinational food and biotech companies and government support for R&D in green technologies further reinforces demand across food, feed, and industrial applications.

Latin America

Latin America is an emerging market for fermented ingredients, led by Brazil and Argentina. Regional growth is primarily driven by the expansion of the livestock sector, rising demand for natural feed additives, and increasing food exports. The adoption of fermented amino acids, enzymes, and organic acids in both feed and food processing sectors is accelerating due to rising awareness of their nutritional benefits and cost-efficiency. Government initiatives supporting agribusiness and investment in local fermentation capacities are additional growth enablers.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but consistent growth, supported by food security initiatives, expanding livestock and feed production, and increasing imports of fermentation-derived ingredients for food and pharmaceutical applications. The growth is also influenced by rising awareness of nutritional supplements and functional foods, along with strategic government incentives aimed at strengthening biotechnology infrastructure. Countries such as the UAE, Saudi Arabia, and South Africa are emerging as key consumers, while intra-regional trade and import-led growth are driving adoption across smaller economies.