Co Packing Market Size

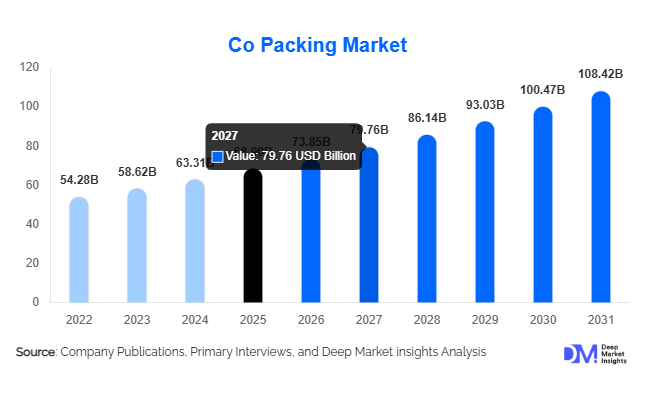

According to Deep Market Insights, the global co packing market size was valued at USD 68.9 billion in 2025 and is projected to grow from USD 73.85 billion in 2026 to reach USD 108.42 billion by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The co packing market growth is driven by increasing outsourcing of manufacturing and packaging operations by food, beverage, personal care, and pharmaceutical companies seeking operational flexibility, cost optimization, and faster product commercialization. Rising demand for contract manufacturing solutions, shorter product life cycles, and growing private-label penetration across retail channels are accelerating adoption of co packing services globally.

Key Market Insights

- Food & beverage brands increasingly outsource packaging operations to reduce capital expenditure and improve speed-to-market.

- Private-label expansion by global retailers is significantly boosting demand for flexible co packing solutions.

- North America leads the global market due to advanced supply chains and strong contract manufacturing ecosystems.

- Asia-Pacific is the fastest-growing region, supported by export-oriented manufacturing hubs in China, India, and Southeast Asia.

- Automation and smart packaging technologies are transforming operational efficiency and traceability across co packing facilities.

- E-commerce fulfillment and customized packaging are emerging as major growth catalysts across industries.

What are the latest trends in the co packing market?

Rise of Flexible and Small-Batch Production

Brands are increasingly launching niche SKUs, seasonal variants, and limited-edition products, creating strong demand for flexible co packing partners capable of small-batch production. Traditional large-scale manufacturing models are being replaced by agile packaging systems supporting rapid changeovers and customization. Co packers are investing in modular production lines that allow quick switching between packaging formats such as pouches, bottles, cartons, and sachets. This trend is especially prominent in functional foods, nutraceuticals, and premium personal care products where innovation cycles are shorter and market testing is essential.

Automation and Digital Integration Across Packaging Lines

Automation adoption is reshaping operational capabilities within co packing facilities. Robotics, AI-driven quality inspection, and IoT-enabled tracking systems are improving throughput while reducing operational errors. Digital twins and predictive maintenance solutions are enabling real-time monitoring of packaging lines, minimizing downtime and enhancing productivity. Technology adoption is also helping co packers meet stringent regulatory compliance requirements, particularly in pharmaceuticals and food safety applications, strengthening long-term client relationships.

What are the key drivers in the co packing market?

Outsourcing to Reduce Capital Investment

Companies increasingly prefer outsourcing packaging and secondary manufacturing processes instead of investing heavily in infrastructure. Co packing enables brands to scale production without committing to expensive equipment or factory expansion. This model is particularly attractive for emerging brands and multinational companies testing new markets, making outsourcing a major growth driver.

Expansion of Private Label and Retail Brands

Retailers worldwide are aggressively expanding private-label portfolios across packaged foods, cosmetics, and household products. These retailers rely heavily on co packers for formulation, packaging, labeling, and distribution readiness. Private-label products now account for significant shelf space globally, creating sustained demand for contract packaging providers capable of large-volume operations.

E-commerce and Direct-to-Consumer Growth

The rapid growth of e-commerce has introduced new packaging requirements such as subscription kits, multi-pack bundles, and protective shipping-ready formats. Co packers increasingly provide fulfillment-integrated services including labeling, kitting, and last-mile preparation, positioning themselves as supply-chain partners rather than just packaging vendors.

What are the restraints for the global market?

Operational Complexity and Margin Pressure

Managing multiple clients, varied packaging formats, and fluctuating order volumes increases operational complexity. Co packers must balance efficiency with customization, which can compress margins, especially when raw material costs fluctuate or demand forecasting is inaccurate.

Regulatory Compliance Challenges

Strict food safety, pharmaceutical validation, and labeling regulations across regions increase compliance costs. Smaller co packers often struggle to maintain certifications such as GMP, HACCP, and ISO standards, limiting scalability and market participation.

What are the key opportunities in the co packing industry?

Automation and Smart Factory Adoption

Investments in robotics and AI-driven packaging operations present major opportunities for co packers to increase throughput while reducing labor dependency. Smart factories enable predictive analytics, traceability, and improved inventory management, helping companies attract multinational clients seeking technologically advanced partners.

Emerging Market Manufacturing Expansion

Rapid industrialization across Southeast Asia, India, and Latin America creates strong opportunities for regional co packers. Multinational brands increasingly establish localized supply chains to reduce logistics costs and mitigate geopolitical risks, driving demand for regional contract packaging providers.

Sustainable Packaging Solutions

Growing environmental regulations and consumer demand for eco-friendly packaging are encouraging co packers to adopt recyclable materials, lightweight packaging, and biodegradable formats. Providers specializing in sustainable solutions are gaining competitive advantage and securing long-term contracts with global brands.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.9 Billion |

| Market Size in 2026 | USD 73.85 Billion |

| Market Size in 2031 | USD 108.42 Billion |

| CAGR | 8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

The global co packing services market demonstrates strong structural growth as brand owners increasingly prioritize operational flexibility, speed-to-market, and cost optimization through outsourced packaging solutions. Among service categories, primary packaging services continue to dominate the industry, accounting for approximately 34% of the global market share in 2025. This leadership position is primarily driven by the essential nature of primary packaging operations, including filling, sealing, labeling, dosing, and product protection functions that directly impact product quality, shelf life, and regulatory compliance. Food and beverage manufacturers, pharmaceutical companies, and personal care brands increasingly rely on specialized co packers equipped with automated production lines capable of maintaining consistency across high-volume production cycles.The leading driver behind primary packaging dominance is the rapid expansion of fast-moving consumer goods (FMCG) categories requiring scalable production without heavy capital investment from brand owners. Contract manufacturing integrated with packaging services represents one of the fastest-growing service segments, reflecting a broader outsourcing transformation across consumer industries. Brands increasingly seek end-to-end partners capable of managing formulation support, production, packaging, labeling, and distribution preparation under a single operational framework. This integrated model reduces logistical complexity, enhances quality control, and shortens commercialization timelines. The rising number of startup brands and digitally native consumer companies further strengthens this trend, as smaller firms lack in-house manufacturing infrastructure and depend heavily on turnkey co packing providers.

Packaging Format Insights

Packaging format evolution remains a central factor shaping demand dynamics across the global co packing industry. Flexible packaging leads the market with nearly 38% share in 2025, supported by its cost efficiency, lightweight structure, and adaptability across diverse product categories. Flexible solutions such as pouches, sachets, stick packs, and flow wraps have gained widespread adoption due to reduced material consumption, improved transportation efficiency, and compatibility with automated high-speed packaging lines.The primary growth driver for flexible packaging is the rapid expansion of e-commerce distribution channels, where durability, lightweight shipping, and space efficiency significantly reduce logistics costs. Brands shipping directly to consumers increasingly favor flexible formats that minimize damage risk while optimizing storage and fulfillment operations. In emerging economies, single-use sachets and small-format packaging continue to dominate due to affordability and accessibility, enabling brands to reach price-sensitive consumer segments.Multi-pack and display-ready packaging formats are gaining traction across organized retail environments. Retail chains increasingly prioritize packaging solutions that reduce in-store handling time while improving merchandising visibility. Co packers capable of delivering customized display packaging solutions benefit from rising demand linked to promotional campaigns, subscription boxes, and seasonal product bundles. The growing intersection between packaging design and marketing strategy further elevates the role of packaging partners in brand storytelling and consumer engagement.

End-Use Industry Insights

The food and beverage industry represents the largest end-use segment within the co packing services market, contributing approximately 46% of total global demand in 2025. The segment’s dominance is primarily driven by changing consumer lifestyles characterized by urbanization, increased workforce participation, and rising preference for convenient meal solutions. Ready-to-eat foods, frozen meals, functional beverages, and snack innovations require scalable, compliant, and high-speed packaging operations, making outsourcing a strategic necessity for manufacturers.The leading driver supporting food and beverage segment growth is continuous product innovation combined with shorter product life cycles. Brands frequently introduce new flavors, packaging sizes, and health-focused variants, creating operational complexity that co packers are uniquely positioned to manage. Additionally, stringent food safety regulations encourage partnerships with specialized providers possessing certified facilities and traceability systems.Pharmaceutical and healthcare applications are also expanding steadily as regulatory complexity increases globally. Drug manufacturers increasingly outsource packaging functions such as serialization, tamper-evident sealing, and compliance labeling to specialized co packers equipped with advanced quality assurance systems. Growth in nutraceuticals, dietary supplements, and wellness products further contributes to demand, particularly as consumers prioritize preventive healthcare solutions.

Distribution Channel Insights

Distribution dynamics within the co packing services market are shaped by long-term partnerships between brand owners and outsourcing providers. Direct brand contracts dominate the market, accounting for approximately 57% market share, as multinational corporations establish strategic relationships with co packers to ensure production continuity and cost predictability. These partnerships often involve multi-year agreements supported by shared forecasting systems and integrated supply chain planning.The primary driver behind direct contracting dominance is the need for operational reliability and consistent quality across global product portfolios. Large brands increasingly rely on dedicated co packing facilities aligned with their production standards, enabling faster scaling during demand fluctuations while reducing capital expenditure requirements.E-commerce fulfillment partnerships represent a rapidly emerging distribution channel. Subscription-based consumption models and direct-to-consumer brands require specialized packaging workflows tailored for parcel shipping, personalization, and rapid order fulfillment. Co packers increasingly integrate packaging operations with logistics providers to support omnichannel retail ecosystems, enabling brands to serve both online and offline markets efficiently.

End-Use Analysis

Demand for co packing services is closely aligned with macro-level expansion across downstream consumer industries. The global packaged food industry, valued at more than USD 3 trillion, continues to expand as urban populations grow and convenience consumption becomes mainstream. This structural shift significantly increases outsourcing requirements, as manufacturers seek scalable production solutions capable of handling fluctuating demand patterns without large infrastructure investments.The cosmetics and personal care industry is growing at an annual rate exceeding 6%, supported by premiumization trends, digital marketing influence, and increasing consumer willingness to experiment with niche brands. Independent beauty companies often operate asset-light business models, outsourcing manufacturing and packaging to specialized partners. This trend reinforces long-term growth opportunities for co packers offering flexible production capabilities and innovative packaging solutions.Export-driven demand plays a particularly important role in market expansion. Manufacturers exporting products internationally depend on co packers to ensure multilingual labeling, regulatory compliance, and region-specific packaging adaptations. Asia-Pacific exporters especially leverage co packing services to meet stringent standards in North American and European markets. Emerging applications such as nutraceutical kits, meal subscription packaging, and customized promotional bundles further diversify market opportunities and enhance service value.

Explore more data points, trends and opportunities Download Free Sample Report

Co Packing Market Segmentations

By Service Type

- Primary Packaging Services

- Secondary Packaging Services

- Contract Manufacturing & Filling

- Assembly & Kitting Services

- Labeling & Compliance Packaging

- Warehousing & Logistics Integration

By Packaging Format

- Flexible Packaging

- Rigid Packaging

- Bottles & Containers

- Cartons & Corrugated Packaging

- Pouches & Sachets

- Multipacks & Promotional Bundles

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Pharmaceuticals & Healthcare

- Household & Homecare Products

- Nutraceuticals & Dietary Supplements

- Consumer Electronics & Industrial Goods

By Distribution Model

- Brand-Owner Outsourcing Contracts

- Retail Private Label Packaging

- E-Commerce Fulfillment Packaging

- Promotional & Seasonal Packaging Programs

Regional Insights

North America

North America accounted for approximately 32% of the global co packing services market in 2025, led primarily by the United States. The region’s leadership is supported by high outsourcing adoption rates, advanced manufacturing infrastructure, and mature retail ecosystems. One of the key drivers of regional growth is strong private-label penetration across supermarkets and warehouse retail chains, which rely heavily on contract packaging partners to maintain cost competitiveness and product variety.Automation adoption represents another major growth driver. North American co packers increasingly invest in robotics, digital quality monitoring, and smart packaging technologies to improve efficiency and reduce labor dependency. The expanding pharmaceutical sector also contributes significantly, as stringent regulatory standards encourage outsourcing to specialized providers capable of maintaining compliance. In Canada, growth is supported by rising food exports, increasing demand for clean-label products, and government initiatives promoting domestic food processing industries.

Europe

Europe holds nearly 27% of global market share, with Germany, the United Kingdom, France, and Italy serving as key demand centers. Regional growth is strongly influenced by sustainability regulations that encourage brands to partner with certified co packers capable of delivering recyclable, biodegradable, and reduced-material packaging solutions. Environmental compliance requirements increase operational complexity, making outsourcing more attractive for manufacturers lacking specialized expertise.The region’s well-established premium food and beverage export sector acts as a major driver, requiring high-quality packaging aligned with international standards. Europe’s strong cosmetic manufacturing clusters, particularly in France and Italy, also stimulate demand for specialized packaging services supporting luxury branding and small-batch production. Additionally, rising demand for convenience foods among aging populations contributes to sustained packaging outsourcing growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 9%. China and India serve as major manufacturing hubs due to large-scale production capabilities, expanding domestic consumption, and export-oriented industrial strategies. A primary driver of regional growth is rapid urbanization combined with rising middle-class income levels, which significantly increase demand for packaged foods, personal care products, and healthcare goods.Competitive labor costs and expanding FMCG production attract multinational brands seeking cost-efficient outsourcing solutions. Southeast Asian countries such as Vietnam and Thailand are emerging as preferred contract packaging destinations, supported by favorable trade policies and increasing foreign investment. The rapid growth of e-commerce platforms across the region further accelerates demand for flexible packaging formats and fulfillment-oriented co packing services.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth driven by economic diversification initiatives and expanding food processing industries. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in domestic manufacturing capabilities to reduce reliance on imports. A key growth driver is increasing demand for localized packaging solutions that comply with regional labeling regulations and cultural preferences.Rising packaged food consumption, supported by urban population growth and modern retail expansion, strengthens outsourcing demand. In Africa, improving logistics infrastructure and growing consumer markets encourage investment in regional co packing facilities. South Africa serves as a major hub supporting food exports and regional distribution networks, further enhancing market development.

Latin America

Latin America’s co packing services market is primarily driven by Brazil and Mexico, where retail modernization and private-label expansion continue transforming consumer markets. A major regional growth driver is the expansion of organized retail chains and discount supermarkets, which increasingly depend on outsourced packaging to manage diverse product portfolios efficiently.Export-oriented food processing industries also contribute significantly to market growth, particularly in agricultural and processed food categories. Currency fluctuations and cost pressures encourage manufacturers to adopt asset-light operating models, increasing reliance on co packing partners. Additionally, rising urbanization and growing middle-class populations stimulate demand for packaged consumer goods, reinforcing long-term outsourcing opportunities across the region.

Key Players in the Co Packing Market

- AmeriPac Inc.

- Sharp Packaging Services

- Jones Packaging Group

- Assemblies Unlimited

- Deufol SE

- FedEx Supply Chain

- DHL Supply Chain

- Unicep Packaging

- Co-Pak Packaging Corporation

- Stamar Packaging

- Multipack Solutions

- Verst Logistics

- Green Packaging Asia

- Summit Packaging Solutions

- ActionPak Inc.