Children Clothing Market Size

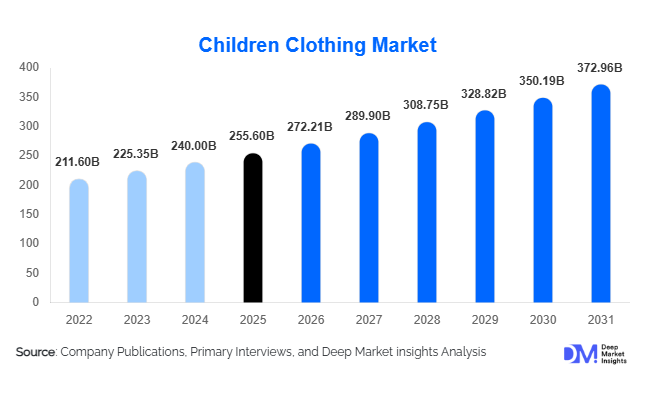

According to Deep Market Insights, the global children clothing market size was valued at USD 255.6 billion in 2025 and is projected to grow from USD 272.21 billion in 2026 to reach USD 372.96 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The market growth is primarily driven by rising disposable incomes, increasing fashion consciousness among parents, growing penetration of organized retail channels, and rapid expansion of e-commerce platforms worldwide. The children's apparel industry benefits from recurring demand as children frequently outgrow clothing, creating a stable replacement cycle that remains relatively resilient even during economic fluctuations. Furthermore, growing awareness regarding sustainable fabrics, organic cotton products, and premium-quality apparel is encouraging manufacturers to innovate and diversify product portfolios. Emerging economies across Asia-Pacific, Latin America, and Africa are generating substantial new demand as urbanization and middle-class spending continue to rise. Digital marketing, social media influence, character licensing partnerships, and direct-to-consumer business models are further transforming purchasing behavior, making children's apparel one of the most dynamic categories within the global fashion industry.

Key Market Insights

- Bottom wear remains the largest product category, accounting for approximately 22.4% of global revenue due to its high replacement frequency and year-round demand.

- School-age children represent the largest consumer group, contributing nearly 31.8% of global market demand through school uniforms, casual wear, and sports apparel purchases.

- Asia-Pacific dominates the global market, accounting for approximately 36.5% of total revenue, supported by large child populations and expanding middle-class consumption.

- India is emerging as the fastest-growing national market, driven by demographic advantages, rising disposable incomes, and rapid organized retail expansion.

- E-commerce is the fastest-growing distribution channel, accounting for nearly 28.9% of market revenue while continuing to gain share from traditional retail formats.

- Sustainable and organic children's apparel is gaining momentum, supported by growing parental awareness regarding environmental sustainability and child health.

Children Clothing Market Trends

Sustainable and Organic Apparel Adoption Accelerating

Sustainability has become one of the most influential trends shaping the global children clothing market. Parents are increasingly seeking products manufactured using organic cotton, recycled polyester, and environmentally friendly production processes. Concerns regarding skin sensitivity, chemical exposure, and environmental impact are encouraging purchases of certified sustainable apparel. Major brands are introducing eco-friendly collections and implementing circular fashion initiatives that incorporate recyclable materials and take-back programs. Regulatory pressure across Europe and North America is further accelerating adoption of sustainable manufacturing standards. As sustainability becomes a purchasing priority rather than a niche preference, manufacturers are investing heavily in green supply chains, renewable energy utilization, and environmentally responsible sourcing strategies.

Digital Commerce and Personalization Reshaping Consumer Purchasing Behavior

The rapid growth of e-commerce and direct-to-consumer business models is fundamentally transforming children's apparel retail. Parents increasingly prefer online platforms due to convenience, broader product selection, competitive pricing, and simplified returns. Brands are utilizing artificial intelligence, data analytics, and personalized recommendation engines to improve customer engagement and conversion rates. Virtual fitting tools, size prediction algorithms, and social commerce integrations are enhancing the online shopping experience. Mobile-first purchasing behavior across emerging economies is creating additional growth opportunities, while social media influencers and digital content creators continue to shape apparel trends among younger consumers and parents.

Children Clothing Market Drivers

Growing Fashion Awareness Among Parents

Parents are increasingly viewing children's clothing as an extension of personal lifestyle and family identity. Social media platforms, celebrity endorsements, and influencer-driven trends have elevated the importance of fashionable apparel for children. Premium brands, designer collections, and occasion-specific clothing are witnessing strong demand across developed and emerging economies alike. This trend is particularly prominent among urban middle-class households, where spending on children's apparel continues to increase despite broader economic uncertainties.

Expansion of E-Commerce Infrastructure

The proliferation of online retail platforms has significantly improved product accessibility and purchasing convenience. Consumers can now compare brands, access wider product assortments, and benefit from promotional pricing through digital channels. E-commerce has enabled both global brands and regional manufacturers to expand their customer reach without substantial investments in physical retail infrastructure. Enhanced logistics networks and same-day delivery services are further supporting market expansion.

Children Clothing Market Restraints

Volatility in Raw Material Costs

Fluctuating prices of cotton, polyester, dyes, and textile inputs continue to impact manufacturing costs across the apparel value chain. Rising labor expenses and logistics costs have further increased production expenditures, creating pricing pressures for manufacturers and retailers. Smaller market participants often face greater challenges in managing these cost fluctuations due to limited purchasing scale and supply chain leverage.

Intense Competitive Environment

The global children clothing industry remains highly fragmented, with competition arising from international brands, regional manufacturers, fast-fashion retailers, and private-label products. This competitive intensity limits pricing flexibility and places pressure on profit margins. Companies must continuously invest in product innovation, marketing initiatives, and digital capabilities to maintain market share and customer loyalty.

Children Clothing Market Opportunities

Expansion of Sustainable and Premium Product Lines

Demand for premium-quality, organic, and sustainable children's apparel presents a significant growth opportunity for market participants. Parents are increasingly willing to pay premium prices for products offering superior comfort, safety, durability, and environmental sustainability. Companies capable of establishing strong sustainability credentials are likely to benefit from higher customer retention and enhanced brand differentiation. Sustainable apparel categories are expected to outperform overall market growth rates throughout the forecast period.

Emerging Market Penetration and Digital-First Strategies

Rapid urbanization and rising disposable incomes across India, Indonesia, Vietnam, Nigeria, Mexico, and other emerging economies are creating substantial opportunities for industry participants. Digital-first retail models enable companies to enter these markets with relatively low infrastructure investment. Direct-to-consumer channels, mobile commerce platforms, and localized marketing campaigns provide efficient pathways for customer acquisition and long-term market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 255.6 Billion |

| Market Size in 2026 | USD 272.21 Billion |

| Market Size in 2031 | USD 372.96 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bottom wear accounted for the largest share of the global children clothing market, representing approximately 22.4% of total revenue in 2025. The segment's leadership is primarily driven by its high replacement frequency and universal adoption across all age groups. Products such as jeans, trousers, shorts, skirts, and leggings experience consistent demand as children rapidly outgrow clothing sizes and require frequent wardrobe updates throughout the year. In addition, the increasing popularity of casual dressing trends among children, coupled with the growing influence of athleisure-inspired fashion, has expanded demand for comfortable and versatile bottom wear products. The segment also benefits from strong school-related purchases, particularly in regions where uniform programs require multiple sets of trousers, skirts, or shorts. Manufacturers continue to introduce stretch fabrics, stain-resistant materials, and durable designs that improve product longevity while maintaining comfort, further supporting category growth.

Tops and T-shirts remain a major revenue contributor due to their everyday utility and year-round purchasing cycle. Dresses and occasion wear continue to witness strong demand in the girls' apparel segment, particularly across North America, Europe, and affluent Asia-Pacific markets where spending on premium fashion products is increasing. Meanwhile, sportswear and activewear represent one of the fastest-growing categories, supported by rising participation in school sports, fitness activities, and outdoor recreation. School uniforms continue to generate stable demand across Asia-Pacific, the Middle East, and Africa, where institutional dress requirements create recurring purchasing cycles that are less susceptible to economic fluctuations.

Age Group Insights

School-age children (6–12 years) dominated the global children clothing market, accounting for approximately 31.8% of total revenue in 2025. The segment benefits from a combination of educational, recreational, and lifestyle-related clothing requirements. Children within this age group typically require multiple apparel categories, including school uniforms, casual wear, sportswear, seasonal clothing, and occasion-specific outfits, resulting in higher annual spending per child compared to other age groups. The growing participation of children in extracurricular activities, organized sports programs, and social events further strengthens apparel demand within this segment.

The segment is also supported by increasing parental spending on branded and premium apparel products as families place greater emphasis on quality, durability, and fashion-conscious designs. Teenagers represent the fastest-evolving consumer category due to strong exposure to social media, celebrity influences, and digital fashion trends. Their preference for branded products, streetwear-inspired designs, and frequent wardrobe updates is creating substantial opportunities for apparel manufacturers. Toddlers and preschool-aged children continue to contribute significantly to market growth due to rapid physical development that necessitates frequent clothing replacement. Infant apparel remains a stable segment, supported by consistent birth rates and increasing demand for comfort-focused, organic, and hypoallergenic clothing products.

Material Type Insights

Cotton remains the dominant material segment, accounting for approximately 48.5% of global children clothing market revenue in 2025. The segment's leadership is primarily attributed to cotton's superior softness, breathability, moisture absorption capabilities, and suitability for children's sensitive skin. Parents consistently prioritize comfort and safety when selecting apparel products, making cotton the preferred material for everyday wear, sleepwear, infant clothing, and school uniforms. The widespread availability of cotton across major apparel manufacturing hubs also supports its cost competitiveness and broad adoption.

Furthermore, growing awareness regarding skin allergies and chemical sensitivities has reinforced consumer preference for natural fibers over synthetic alternatives. Blended fabrics and polyester-based materials continue gaining market share due to their durability, wrinkle resistance, color retention, and affordability. However, one of the most significant developments within the material segment is the rapid growth of organic cotton and sustainable textiles. Environmental concerns, sustainability regulations, and increasing consumer awareness are encouraging manufacturers to expand eco-friendly product offerings. Recycled polyester, organic cotton, and innovative bio-based fabrics are expected to record above-market growth rates as brands increasingly align product portfolios with sustainability objectives.

Distribution Channel Insights

E-commerce emerged as the fastest-growing distribution channel and accounted for approximately 28.9% of global children clothing market revenue in 2025. The channel's rapid expansion is driven by increasing internet penetration, smartphone adoption, digital payment infrastructure, and growing consumer preference for convenient shopping experiences. Parents increasingly favor online platforms due to their ability to compare products, access a broader assortment of brands, review customer feedback, and benefit from competitive pricing and promotional discounts.

The segment has further benefited from advancements in artificial intelligence, personalized recommendation engines, virtual sizing tools, and flexible return policies that improve the online shopping experience. Direct-to-consumer channels are also gaining traction as brands seek to strengthen customer relationships while improving profit margins. Despite the rapid growth of digital channels, traditional retail formats continue to account for the majority of market sales due to the importance of physical product evaluation, particularly for younger children's apparel. Specialty children's apparel stores remain highly relevant in premium and branded categories, while hypermarkets, supermarkets, and department stores continue to serve mass-market consumers through extensive geographic coverage and established customer trust.

Price Category Insights

The mid-range segment dominated the global children clothing market with approximately 46.3% revenue share in 2025. The segment's leadership is supported by consumers' increasing preference for products that offer an optimal balance between affordability, quality, comfort, and durability. Parents are becoming more selective in their purchasing decisions, seeking apparel products that can withstand frequent washing and everyday wear while remaining cost-effective given children's rapid growth cycles.

Rising middle-class populations across Asia-Pacific, Latin America, and parts of the Middle East have significantly contributed to the expansion of mid-priced apparel offerings. At the same time, premium and luxury children's clothing segments are experiencing accelerated growth in developed economies and affluent urban centers. Increasing household incomes, growing brand consciousness, and heightened awareness of sustainable and organic products are encouraging consumers to invest in higher-value apparel. Economy-priced products continue to maintain strong demand in emerging markets where affordability remains a key purchasing criterion, particularly among large family households and price-sensitive consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Children Clothing Market Segmentations

By Product Type

- Tops & T-Shirts

- Shirts & Blouses

- Bottom Wear

- Dresses & Frocks

- Outerwear

- Sleepwear & Nightwear

- Innerwear & Undergarments

- School Uniforms

- Sportswear & Activewear

- Ethnic & Traditional Wear

- Swimwear

- Infant Essentials

By Age Group

- Infants (0–12 Months)

- Toddlers (1–3 Years)

- Preschool Children (3–5 Years)

- School-Age Children (6–12 Years)

- Teenagers (13–16 Years)

By Gender

- Boys

- Girls

- Unisex

By Material Type

- Cotton

- Polyester

- Blended Fabrics

- Organic Cotton

- Wool

- Denim

- Sustainable/Recycled Fabrics

By Distribution Channel

- Hypermarkets & Supermarkets

- Department Stores

- Specialty Kidswear Stores

- Brand-Owned Stores

- Factory Outlets

- E-Commerce Platforms

- Direct-to-Consumer (DTC) Websites

- Social Commerce

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 36.5% of global children clothing market revenue in 2025, making it the largest regional market. The region's dominance is driven by its large child population, expanding middle-class consumer base, rising disposable incomes, and rapid urbanization. China remains the largest national market due to strong domestic consumption, extensive manufacturing capabilities, and the growing popularity of premium children's apparel brands. India represents the fastest-growing major market, supported by favorable demographic trends, increasing household incomes, rising female workforce participation, and the rapid expansion of organized retail and e-commerce platforms.

Additional growth drivers include government support for domestic textile manufacturing, increasing penetration of international apparel brands, and growing awareness of children's fashion trends among urban consumers. Southeast Asian countries such as Indonesia and Vietnam are witnessing rising apparel demand due to improving living standards and growing retail infrastructure, while Japan and South Korea continue to drive demand for premium, branded, and high-quality children's apparel products.

North America

North America accounted for approximately 25.4% of global market revenue in 2025. The United States remains the largest contributor, representing nearly 20.3% of worldwide demand. Regional growth is primarily driven by high consumer spending power, strong adoption of premium apparel products, and well-established retail and e-commerce ecosystems. Parents in North America increasingly prioritize product quality, comfort, sustainability, and brand reputation when purchasing children's apparel.

The growing popularity of organic clothing, sustainable fabrics, and ethically produced apparel continues to shape purchasing behavior across the region. Furthermore, strong digital commerce penetration, widespread adoption of direct-to-consumer business models, and increasing demand for licensed character apparel are supporting market expansion. Canada contributes significantly through rising demand for environmentally responsible apparel and premium winter clothing products designed for harsh climatic conditions.

Europe

Europe represented approximately 24.1% of global children clothing market demand in 2025. Germany, the United Kingdom, France, Italy, and Spain remain the largest regional markets due to their strong purchasing power and mature retail sectors. One of the primary growth drivers across Europe is the increasing emphasis on sustainability and ethical consumption. Consumers are demonstrating strong preferences for organic cotton, recycled materials, and environmentally certified apparel products.

Stringent environmental regulations and sustainability-focused government initiatives are encouraging manufacturers and retailers to adopt responsible sourcing and production practices. The region also benefits from strong demand for premium and designer children's apparel, particularly in Western Europe. In addition, rising e-commerce penetration, growing adoption of circular fashion models, and increasing consumer awareness regarding textile sustainability continue to support long-term market growth.

Latin America

Latin America accounted for approximately 7.4% of global market revenue in 2025, led by Brazil and Mexico. Market growth is being driven by increasing urbanization, rising middle-class populations, and improving retail infrastructure across major economies. Expanding access to international brands and the rapid growth of digital commerce platforms have significantly improved product availability and consumer choice throughout the region.

Brazil remains the largest market due to its sizeable population and growing domestic apparel industry, while Mexico benefits from strong economic integration with North American supply chains and increasing organized retail penetration. Growing youth populations, improving employment levels, and rising consumer spending on children's products continue to create favorable growth conditions across the region. The increasing popularity of affordable branded apparel is further supporting market expansion.

Middle East & Africa

The Middle East & Africa accounted for approximately 6.6% of global market demand in 2025. The region is characterized by strong population growth, high birth rates in several countries, and increasing urbanization levels that continue to expand the consumer base for children's apparel. Saudi Arabia and the United Arab Emirates represent the largest markets in the Gulf region, supported by high disposable incomes, premium consumption patterns, and strong demand for international apparel brands.

Across Africa, countries such as South Africa, Nigeria, and Egypt are witnessing increasing apparel consumption due to expanding middle-class populations, improving retail infrastructure, and growing access to affordable clothing products. Government initiatives aimed at strengthening domestic textile industries, combined with rising internet penetration and e-commerce adoption, are creating new opportunities for apparel manufacturers. Premium children's clothing remains particularly strong in affluent Gulf Cooperation Council countries, while value-oriented apparel continues to dominate demand across much of the African continent.

Key Players in the Children Clothing Market

- Nike Inc.

- Inditex SA (Zara Kids)

- H&M Group

- Carter's Inc.

- Adidas AG

- Gap Inc.

- Fast Retailing Co. Ltd. (Uniqlo)

- The Children's Place Inc.

- PVH Corp.

- Next plc

- Mothercare plc

- Cotton On Group

- Balabala

- Primark

- Benetton Group