Casual Wear Market Size

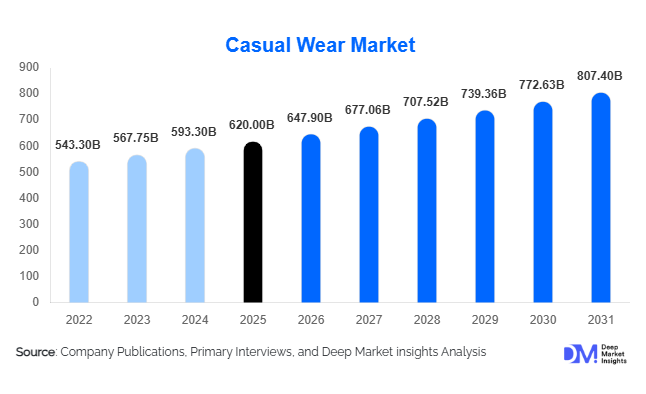

According to Deep Market Insights, the global casual wear market size was valued at USD 620 billion in 2025 and is projected to grow from USD 647.90 billion in 2026 to reach USD 807.40 billion by 2031, expanding at a CAGR of 4.5% during the forecast period (2026–2031). The casual wear market growth is primarily driven by evolving workplace dress codes, increasing consumer preference for comfort-oriented apparel, rapid expansion of e-commerce channels, and growing adoption of athleisure-inspired fashion across both developed and emerging economies. Rising disposable incomes, urbanization, and the influence of social media-driven fashion trends are further supporting market expansion globally.

Key Market Insights

- Comfort-driven fashion continues to reshape global apparel demand, with consumers increasingly favoring versatile clothing suitable for work, travel, and leisure activities.

- Athleisure and hybrid casual apparel are becoming mainstream categories, blurring traditional boundaries between activewear and everyday fashion.

- Asia-Pacific dominates the global casual wear market, supported by strong manufacturing capabilities and rising consumer spending in China, India, and Southeast Asia.

- India represents the fastest-growing major market, driven by urbanization, digital retail penetration, and a rapidly expanding middle-class population.

- Sustainable and recycled apparel is emerging as a major growth segment, particularly across Europe and North America.

- Artificial intelligence, virtual fitting technologies, and direct-to-consumer retail models are transforming customer engagement and supply chain efficiency.

Casual Wear Market Trends

Rise of Sustainable and Circular Fashion

Sustainability has become one of the most influential trends in the global casual wear market. Consumers are increasingly seeking apparel manufactured from organic cotton, recycled polyester, biodegradable fibers, and ethically sourced materials. Major brands are investing heavily in circular economy initiatives such as garment recycling programs, resale platforms, repair services, and low-carbon manufacturing processes. Regulatory developments in Europe are accelerating the adoption of sustainable fashion practices, while growing environmental awareness among younger consumers continues to drive demand for eco-friendly casual wear products. Manufacturers are also implementing water-saving dyeing technologies and traceable supply chains to strengthen brand credibility and improve environmental performance.

Digitalization and AI-Powered Fashion Retail

Technology adoption is rapidly transforming the casual wear industry. Artificial intelligence is increasingly used for inventory optimization, demand forecasting, personalized product recommendations, and trend prediction. Virtual try-on solutions, augmented reality shopping experiences, and AI-driven customer analytics are improving conversion rates and reducing return rates across online channels. Social commerce platforms, influencer marketing, and live-stream shopping events are further strengthening digital sales channels. As brands continue investing in omnichannel retail strategies, technology is expected to become a critical competitive differentiator throughout the forecast period.

Casual Wear Market Drivers

Expansion of Hybrid Work Culture

The widespread adoption of hybrid and flexible work arrangements has significantly accelerated demand for casual and smart-casual apparel. Employees increasingly seek versatile clothing that balances comfort with professional appearance, driving sales of premium basics, casual shirts, chinos, joggers, and athleisure-inspired garments. This shift has permanently altered workplace fashion norms across North America, Europe, and Asia-Pacific, creating sustained demand for casual wear products.

Rapid Growth of E-Commerce and Social Commerce

The expansion of online retail platforms has become a major growth driver for the casual wear market. Consumers benefit from greater product variety, competitive pricing, and enhanced convenience through digital shopping channels. Social media platforms have evolved into important sales channels, with influencer-driven marketing and personalized shopping experiences significantly impacting consumer purchasing behavior. Mobile commerce adoption and direct-to-consumer business models continue to expand global market accessibility.

Casual Wear Market Restraints

Raw Material Price Volatility

The casual wear industry remains highly exposed to fluctuations in cotton, polyester, synthetic fiber, and energy prices. Rising raw material costs directly impact manufacturing expenses and profit margins, creating pricing challenges for both premium and mass-market brands. Supply chain disruptions and geopolitical uncertainties further contribute to cost volatility across global apparel production networks.

Intense Market Competition

The market is characterized by significant competition among global fashion brands, regional manufacturers, fast-fashion companies, and digital-native apparel businesses. Frequent product launches, aggressive discounting strategies, and rising customer acquisition costs place pressure on profitability. Maintaining brand differentiation while managing operational costs remains a major challenge for market participants.

Casual Wear Market Opportunities

Expansion in Emerging Consumer Markets

Emerging economies including India, Indonesia, Vietnam, Philippines, Brazil, and several African countries represent substantial growth opportunities for casual wear manufacturers. Rising disposable incomes, expanding middle-class populations, increasing urbanization, and improving internet penetration are driving apparel consumption across these markets. International brands are increasingly localizing product offerings and expanding omnichannel retail networks to capture growing demand. These regions are expected to contribute a significant portion of incremental global apparel sales over the next decade.

AI-Enabled Personalization and Direct-to-Consumer Growth

Advancements in artificial intelligence and customer analytics are creating opportunities for personalized fashion retail experiences. Brands leveraging AI-driven recommendations, predictive purchasing behavior, virtual fitting tools, and customized marketing campaigns are achieving stronger customer engagement and higher conversion rates. Direct-to-consumer platforms also provide greater control over pricing, inventory, and customer relationships, allowing companies to improve margins while building stronger brand loyalty. The integration of personalization technologies is expected to create significant competitive advantages across the casual wear market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 620 Billion |

| Market Size in 2026 | USD 647.90 Billion |

| Market Size in 2031 | USD 807.40 Billion |

| CAGR | 4.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Top wear emerged as the leading product segment, accounting for approximately 34% of the global casual wear market in 2025. The segment's dominance is primarily attributed to its high purchase frequency, lower average replacement cycle compared to bottom wear, and broad applicability across multiple consumer demographics. Products such as T-shirts, casual shirts, polo shirts, hoodies, sweatshirts, and lightweight jackets have become essential wardrobe staples due to their versatility across workplace, leisure, travel, and social settings. The increasing adoption of hybrid work environments has further strengthened demand for smart-casual tops that combine comfort with professional aesthetics.

The growth of social media-driven fashion trends and fast-fashion retailing has also accelerated product turnover within this category, encouraging consumers to purchase multiple styles and seasonal collections throughout the year. In addition, collaborations between fashion brands, celebrities, and influencers continue to stimulate demand for premium and limited-edition top wear products. The category is expected to maintain its market leadership during the forecast period due to rising consumer preference for versatile apparel, increasing athleisure adoption, and growing demand for sustainable cotton and recycled-fiber garments.

Bottom wear represents the second-largest product category, benefiting from growing workplace casualization, increased acceptance of denim and chinos in professional environments, and the rising popularity of joggers and stretch-based apparel. Athleisure-inspired casual wear remains the fastest-growing product segment as consumers increasingly seek multifunctional apparel that supports active lifestyles while maintaining everyday fashion appeal. Seasonal casual wear collections continue to generate significant revenue opportunities, particularly across North America and Europe where weather-driven purchasing behavior influences apparel consumption patterns.

Consumer Group Insights

Women accounted for approximately 42% of total global casual wear revenue in 2025, making them the largest consumer group. The segment benefits from broader product assortments, faster fashion cycles, higher purchasing frequency, and greater engagement with fashion trends compared to other consumer categories. Women's casual wear manufacturers continually introduce new styles, colors, and seasonal collections, creating repeat purchasing behavior and supporting premium pricing opportunities. Social media influence, celebrity endorsements, and growing fashion consciousness among millennials and Gen Z consumers continue to drive category expansion globally.

Men's casual wear represents the fastest-evolving consumer segment, supported by increasing fashion awareness, growing demand for premium basics, and widespread adoption of athleisure apparel. The shift toward casual workplace dressing and increasing spending on personal grooming and fashion are further contributing to market growth. Children's casual wear remains a stable revenue contributor, driven by population growth in emerging markets, rising disposable incomes, and increasing penetration of branded apparel among middle-income households.

The unisex casual wear segment is witnessing above-average growth as fashion brands increasingly launch gender-neutral collections that align with evolving consumer preferences for inclusivity and self-expression. The segment is particularly popular among younger consumers who prioritize comfort, sustainability, and minimalist design aesthetics.

Distribution Channel Insights

Offline retail channels maintained their leadership position with approximately 58% of global casual wear sales in 2025. Physical stores continue to play a critical role in consumer purchasing decisions, particularly for apparel products where fitting, fabric evaluation, and immediate product availability remain important considerations. Brand-owned stores, department stores, specialty apparel retailers, and multi-brand outlets benefit from experiential shopping environments that strengthen customer engagement and brand loyalty. The continued expansion of premium retail formats and experiential flagship stores has enabled leading apparel brands to maintain strong footfall despite increasing digital competition. In developing markets, physical retail networks remain particularly important due to lower online penetration rates and consumer preference for in-store purchases.

However, online retail remains the fastest-growing distribution channel, supported by rising smartphone penetration, expanding internet access, improved logistics infrastructure, and increasing consumer trust in digital transactions. E-commerce marketplaces, brand-owned websites, mobile shopping applications, and social commerce platforms are increasingly influencing apparel purchasing behavior. Artificial intelligence-powered product recommendations, virtual fitting technologies, and omnichannel fulfillment strategies are expected to further accelerate online casual wear sales throughout the forecast period.

Material Type Insights

Cotton remained the dominant material segment, accounting for approximately 31% of global casual wear demand in 2025. The material's leadership position is driven by its superior comfort, breathability, softness, durability, and adaptability across diverse climatic conditions. Cotton-based garments continue to be preferred by consumers across both developed and emerging markets, particularly for everyday wear categories such as T-shirts, casual shirts, and loungewear.

The increasing consumer preference for natural fibers, coupled with rising demand for organic and sustainably sourced cotton, continues to strengthen the segment's market position. Leading apparel brands are investing heavily in certified sustainable cotton procurement programs to address growing environmental concerns and comply with evolving sustainability regulations.

Denim remains a critical material category due to the enduring popularity of jeans and casual outerwear products. Polyester and blended fabrics continue to gain traction because of their cost-effectiveness, wrinkle resistance, moisture-wicking capabilities, and suitability for athleisure apparel. Meanwhile, sustainable materials including recycled polyester, regenerated fibers, and organic textiles represent the fastest-growing material segment, driven by increasing consumer awareness regarding environmental sustainability and circular fashion initiatives.

End-Use Insights

Individual consumers accounted for nearly 88% of total casual wear demand in 2025, making personal apparel consumption the dominant end-use segment. Rising disposable incomes, increasing urbanization, expanding middle-class populations, and growing fashion consciousness continue to drive consumer spending on casual apparel globally. The growing influence of social media, celebrity endorsements, and digital marketing campaigns has further accelerated purchasing frequency across multiple demographic groups.

Corporate casual uniform programs are emerging as an important secondary demand segment as organizations increasingly adopt business-casual workplace policies. Companies across technology, retail, hospitality, and service sectors are replacing traditional formal attire with branded casual apparel, creating recurring procurement opportunities for manufacturers.

The hospitality sector continues to generate steady demand through branded employee uniforms, while educational institutions with relaxed dress codes contribute to growing consumption among younger demographics. Entertainment, media, influencer marketing, and content creation industries are also becoming increasingly important consumers of fashion-forward casual apparel. Furthermore, export-oriented apparel manufacturing hubs including China, Bangladesh, Vietnam, and India continue to support large-scale production volumes, reinforcing global supply chain growth and market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Casual Wear Market Segmentations

By Product Type

- Top Wear

- Bottom Wear

- Dresses & One-Piece Apparel

- Athleisure Casual Wear

- Seasonal Casual Wear

By Consumer Group

- Men

- Women

- Children

- Unisex

By Price Category

- Economy/Mass Market

- Mid-Premium

- Premium

- Luxury Casual Wear

By Material Type

- Cotton

- Denim

- Polyester/Synthetic Fibers

- Wool

- Linen

- Blended Fabrics

- Sustainable/Recycled Materials

By Distribution Channel

- Offline Retail

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 41.5% of the global casual wear market in 2025, making it the largest regional market worldwide. The region benefits from a unique combination of large consumer populations, rising disposable incomes, strong manufacturing capabilities, and rapidly expanding e-commerce ecosystems. China remains both the largest apparel manufacturing hub and one of the largest consumption markets globally, supported by vertically integrated textile supply chains, advanced production infrastructure, and a growing middle-class population.

India represents the fastest-growing major market globally, driven by urbanization, favorable demographics, increasing workforce participation, rising fashion awareness, and rapid digital commerce expansion. Japan and South Korea continue to lead premium casual wear consumption due to high purchasing power, strong fashion consciousness, and demand for innovative apparel products. Southeast Asian markets including Indonesia, Vietnam, Thailand, and the Philippines are witnessing strong growth supported by expanding middle-income populations and increasing penetration of international fashion brands.

Key regional growth drivers include rising disposable incomes, urban migration, growing youth populations, increasing smartphone penetration, strong apparel manufacturing investments, and expanding direct-to-consumer retail channels.

North America

North America accounted for approximately 28% of global market revenue in 2025, making it the second-largest regional market. The United States alone contributes nearly 24% of worldwide casual wear demand due to high consumer spending power, strong fashion adoption rates, and widespread acceptance of casual workplace attire. Athleisure remains a particularly influential category within the region, supported by increasing health consciousness and active lifestyle trends.

Canada continues to experience strong demand for premium and sustainable apparel products, while Mexico benefits from growing retail modernization and increasing participation in North American apparel supply chains. The region also exhibits one of the highest levels of digital retail penetration globally. Key regional growth drivers include athleisure adoption, hybrid work culture, premiumization trends, high e-commerce penetration, increasing demand for sustainable fashion, and continuous innovation in retail technology.

Europe

Europe accounted for approximately 21% of global casual wear demand in 2025. Germany, the United Kingdom, France, Italy, and Spain represent the region's largest markets and collectively account for the majority of apparel consumption. European consumers exhibit strong preferences for premium-quality apparel, sustainable manufacturing practices, and ethically sourced materials.

The region has become a global leader in circular fashion initiatives, with apparel brands increasingly investing in recycling programs, resale platforms, and environmentally responsible production methods. Fashion-forward consumer behavior and high discretionary spending continue to support demand for premium casual wear products. Key growth drivers include stringent sustainability regulations, increasing adoption of circular fashion, strong consumer spending on premium apparel, advanced retail infrastructure, and growing demand for eco-friendly and ethically produced garments.

Latin America

Latin America accounted for approximately 5% of the global casual wear market in 2025, with Brazil and Mexico serving as the region's primary demand centers. The casual wear sector continues to benefit from expanding urban populations, improving economic conditions, and increasing fashion awareness among younger consumers. International apparel brands are actively expanding their retail presence across major metropolitan areas to capitalize on rising consumer demand.

Brazil remains the largest apparel market in the region due to its sizeable population and established domestic textile industry, while Mexico benefits from strong retail growth and increasing integration with North American supply chains. Key regional growth drivers include urbanization, increasing middle-class purchasing power, retail modernization, expanding shopping mall infrastructure, rising digital commerce adoption, and growing influence of global fashion trends.

Middle East & Africa

The Middle East & Africa region accounted for approximately 4.5% of global market revenue in 2025. The UAE and Saudi Arabia represent the largest premium apparel markets due to high disposable incomes, luxury-oriented consumer preferences, and well-developed retail ecosystems. Demand for international casual wear brands continues to increase across the Gulf Cooperation Council countries as consumers seek premium fashion products aligned with global trends.

South Africa remains the largest apparel market within Sub-Saharan Africa, while countries such as Nigeria, Kenya, and Egypt are emerging as attractive growth markets due to expanding urban populations and increasing consumer spending. The region's youthful demographic profile provides substantial long-term growth potential. Key growth drivers include rapid urbanization, population growth, expanding retail infrastructure, rising disposable incomes, increasing international brand penetration, tourism-driven retail demand, and growing adoption of e-commerce platforms.

Key Players in the Casual Wear Market

- Nike Inc.

- Adidas AG

- Inditex SA

- H&M Group

- Uniqlo (Fast Retailing Co., Ltd.)

- Levi Strauss & Co.

- Puma SE

- Gap Inc.

- VF Corporation

- LVMH

- Ralph Lauren Corporation

- PVH Corp.

- American Eagle Outfitters

- Abercrombie & Fitch Co.

- Next plc