Bridal Gowns Market Size

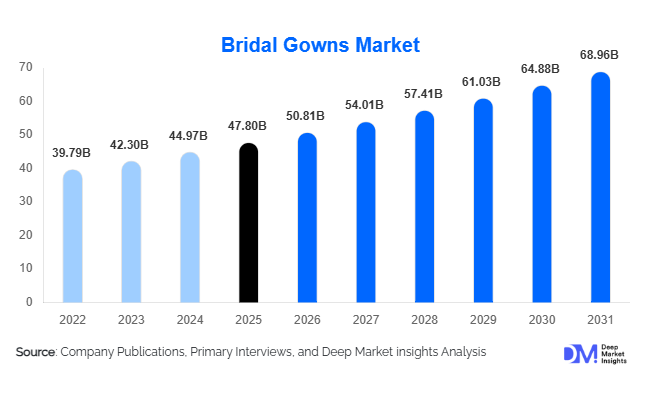

According to Deep Market Insights, the global bridal gowns market size was valued at USD 47.8 billion in 2025 and is projected to grow from USD 50.81 billion in 2026 to reach USD 68.96 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The bridal gowns market growth is primarily driven by rising wedding expenditures, increasing demand for personalized bridal fashion, growing destination wedding trends, and the expansion of premium and luxury bridal wear across both developed and emerging economies. Social media influence, celebrity-inspired wedding fashion, and the growing adoption of digital bridal shopping platforms are further contributing to market expansion globally.

Key Market Insights

- Customized and made-to-measure bridal gowns are witnessing strong demand, as brides increasingly seek unique designs tailored to individual preferences and wedding themes.

- Asia-Pacific dominates the global bridal gowns market, supported by high annual marriage volumes in China and India and rising wedding spending among middle-class consumers.

- Sustainable bridal fashion is gaining momentum, with increasing demand for eco-friendly fabrics, ethical production methods, rental gowns, and resale bridal platforms.

- Luxury bridal wear continues to outperform the broader market, driven by destination weddings, celebrity influence, and premium consumer spending.

- Online bridal retail channels are expanding rapidly, enabling virtual consultations, digital fittings, and direct-to-consumer sales models.

- Rental and circular bridal fashion models are emerging as high-growth segments, particularly among younger consumers seeking affordability and sustainability.

Bridal Gowns Market Trends

Rise of Personalized and Bespoke Bridal Fashion

Personalization has become one of the defining trends in the bridal gowns market. Brides increasingly seek custom-made gowns that reflect their individual style, cultural heritage, and wedding themes. Bridal designers are responding by offering made-to-measure services, customization options, and exclusive couture collections. Technologies such as 3D body scanning, virtual fitting platforms, and AI-driven design recommendations are helping manufacturers improve customer engagement while reducing fitting errors. Premium bridal brands are increasingly positioning bespoke craftsmanship as a key differentiator, allowing them to command higher margins and strengthen brand loyalty.

Sustainable and Circular Bridal Wear Adoption

Sustainability is transforming bridal purchasing behavior across major markets. Consumers are becoming more conscious of environmental impacts associated with single-use wedding apparel. This has led to growing demand for sustainable fabrics, ethically sourced materials, rental bridal gowns, and resale marketplaces. Brands are introducing recycled lace, organic silk, and low-impact manufacturing processes to appeal to environmentally conscious consumers. Bridal gown rental platforms and second-hand marketplaces are also expanding globally, creating new revenue streams while supporting circular fashion initiatives. These trends are particularly prominent among Millennials and Gen Z consumers who prioritize both sustainability and affordability.

Bridal Gowns Market Drivers

Increasing Global Wedding Expenditure

Wedding spending continues to rise globally as consumers prioritize experiential and memorable celebrations. Bridal gowns remain one of the largest expenditure categories within wedding budgets. Higher disposable incomes, urbanization, and evolving wedding traditions are encouraging brides to invest in premium and luxury wedding attire. Markets such as the United States, China, India, and the Middle East continue to witness increasing bridal fashion spending, supporting steady market growth.

Expansion of Destination Weddings

The rapid growth of destination weddings has significantly increased demand for bridal apparel. Brides participating in destination ceremonies often purchase multiple outfits for pre-wedding events, ceremonies, receptions, and post-wedding celebrations. This trend is driving higher average transaction values across both luxury and premium bridal segments. Popular destination wedding locations across Europe, Southeast Asia, and the Caribbean are contributing to increased demand for lightweight, travel-friendly, and customized bridal designs.

Bridal Gowns Market Restraints

High Product Costs and Price Sensitivity

Despite strong premiumization trends, bridal gown purchases remain highly discretionary. Luxury and couture gowns can represent a significant financial commitment for consumers, making the market sensitive to economic uncertainty and inflationary pressures. Cost-conscious consumers are increasingly considering rental, resale, or lower-cost alternatives, creating challenges for traditional bridal retailers.

Seasonal Demand and Marriage Rate Fluctuations

The bridal gowns industry remains dependent on marriage rates and seasonal wedding patterns. Economic downturns, changing social attitudes toward marriage, and declining marriage rates in certain developed countries can impact demand. In addition, wedding seasonality often creates inventory management challenges and uneven revenue generation for manufacturers and retailers.

Bridal Gowns Market Opportunities

Growth of Sustainable Bridal Fashion

The increasing focus on sustainability presents a significant opportunity for bridal fashion brands. Eco-conscious consumers are driving demand for sustainable materials, ethical manufacturing, and circular fashion models. Companies investing in environmentally friendly collections, rental programs, and resale platforms are expected to capture a growing segment of the bridal apparel market. Sustainability certifications and transparent sourcing practices are also becoming important purchasing criteria.

Emerging Market Expansion

Rapid economic growth and increasing disposable incomes across emerging markets such as India, Indonesia, Vietnam, Saudi Arabia, and the UAE are creating substantial growth opportunities. Rising urbanization, expanding middle-class populations, and increasing wedding expenditures are driving demand for both premium and affordable bridal gowns. International brands are actively expanding retail footprints and establishing localized collections to address these high-growth markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 47.8 Billion |

| Market Size in 2026 | USD 50.81 Billion |

| Market Size in 2031 | USD 68.96 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Style Insights

A-Line bridal gowns dominated the global bridal gowns market, accounting for approximately 28% of total revenue in 2025. The segment's leadership is primarily attributed to its universal silhouette, which complements a wide range of body types while balancing elegance, comfort, and practicality. Unlike highly structured designs such as mermaid or trumpet gowns, A-Line dresses appeal to both traditional and contemporary brides, making them suitable across diverse cultural and regional wedding formats. Their versatility allows designers to incorporate various fabrics, embellishments, sleeve styles, and necklines, expanding consumer appeal across multiple price points.

The growing trend toward destination weddings and outdoor ceremonies has further strengthened demand for A-Line gowns due to their lightweight construction and ease of movement. Additionally, bridal boutiques frequently recommend A-Line designs as the safest option for first-time bridal shoppers, contributing to higher conversion rates. Ball gowns continue to maintain strong demand within luxury bridal segments, particularly across North America and the Middle East where grand wedding celebrations and premium wedding budgets support demand for voluminous and highly embellished designs. Meanwhile, mermaid and trumpet gowns are experiencing accelerated growth among younger consumers influenced by celebrity weddings, social media platforms, and fashion-forward bridal trends. Sheath, slip, and minimalist bridal gowns are also gaining popularity as modern brides increasingly seek comfort, travel convenience, and understated elegance for destination and intimate wedding ceremonies.

Price Category Insights

Mid-range bridal gowns represented the largest price category, accounting for approximately 42% of global market revenue in 2025. The segment benefits from its ability to deliver premium aesthetics, quality craftsmanship, and designer-inspired styling while remaining accessible to the broad middle-income consumer base. The majority of wedding consumers globally operate within defined wedding budgets, making the mid-range category the optimal balance between affordability and exclusivity.

Rising disposable incomes across emerging economies, particularly in Asia-Pacific and Latin America, continue to support growth within this segment. Brides increasingly prioritize gown quality, customization options, and brand reputation without necessarily moving into luxury price ranges. The premium and luxury bridal categories are witnessing above-average growth rates due to increasing wedding expenditures, destination weddings, and growing demand for bespoke bridal experiences. In contrast, economy bridal gowns continue to play a critical role in high-volume emerging markets where affordability remains a key purchase determinant. The expansion of online bridal retail platforms is also improving access to mid-range products globally, further strengthening segment dominance.

Distribution Channel Insights

Bridal boutiques remained the leading distribution channel, accounting for nearly 46% of global bridal gown sales in 2025. The segment continues to outperform alternative channels due to the highly personalized nature of bridal gown purchasing. Unlike conventional fashion purchases, bridal gowns require multiple fittings, customization consultations, fabric selection discussions, and alteration services, all of which are best facilitated through specialized boutique environments.

Consumers continue to value the experiential aspect of bridal shopping, including one-on-one styling appointments, family participation, personalized recommendations, and professional fitting services. Bridal boutiques also benefit from exclusive designer partnerships and premium customer service capabilities that are difficult to replicate online. However, digital channels are rapidly expanding as manufacturers invest in virtual consultations, AI-driven sizing tools, augmented reality fitting technologies, and direct-to-consumer business models. Online bridal sales are expected to record the fastest growth during the forecast period as younger consumers increasingly embrace digital shopping experiences. Multi-brand wedding retailers continue to maintain strong market positions due to extensive product portfolios and localized customer relationships.

Customization Insights

Ready-to-wear bridal gowns accounted for approximately 58% of global market revenue in 2025, making them the largest customization segment. Their leadership is primarily driven by affordability, shorter lead times, and immediate product availability. Many brides prefer ready-to-wear options due to budget considerations and compressed wedding planning timelines, particularly in developing markets where elaborate customization remains less common.

Despite current dominance, made-to-measure and fully customized bridal gowns are experiencing significantly faster growth. Rising consumer demand for personalization, exclusivity, and unique bridal aesthetics is encouraging greater adoption of custom bridal solutions. Technological innovations such as 3D body scanning, digital measurement tools, virtual fittings, and AI-assisted design platforms are reducing production complexity and enabling brands to scale customization services more efficiently. As wedding spending increases globally, the customized bridal gown segment is expected to capture a larger share of premium and luxury bridal expenditures.

Consumer Age Group Insights

Brides aged 25–34 years represented approximately 61% of global bridal gown demand in 2025, making this the largest consumer segment. The segment corresponds closely with peak marriage age demographics across major global markets and possesses the strongest combination of purchasing power, career stability, and wedding expenditure capacity.

Consumers within this age group are highly engaged with bridal fashion trends, social media influences, designer brands, and customization options. They also demonstrate greater willingness to invest in premium wedding experiences, supporting demand across mid-range and luxury bridal categories. Brides under the age of 25 primarily contribute to entry-level and affordable bridal segments, while consumers aged 35–44 years increasingly drive premium and bespoke bridal purchases, particularly among professionals and second-marriage consumers. Growing acceptance of later marriages across developed economies is also contributing to increased demand among older age groups seeking contemporary, minimalist, and highly personalized bridal fashion solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Bridal Gowns Market Segmentations

By Style Type

- A-Line Bridal Gowns

- Ball Gowns

- Mermaid Bridal Gowns

- Trumpet Bridal Gowns

- Sheath / Column Gowns

- Slip & Minimalist Gowns

- Tea-Length Bridal Gowns

- Fit-and-Flare Gowns

- Couture / Designer Bridal Gowns

By Price Category

- Economy Bridal Gowns (Below USD 500)

- Mid-Range Bridal Gowns (USD 500–1,500)

- Premium Bridal Gowns (USD 1,500–5,000)

- Luxury & Couture Bridal Gowns (Above USD 5,000)

By Distribution Channel

- Bridal Boutiques

- Brand-Owned Stores

- Multi-Brand Wedding Retailers

- Online Direct-to-Consumer Platforms

- Department Stores

By Customization Type

- Ready-to-Wear Bridal Gowns

- Made-to-Measure Bridal Gowns

- Fully Customized / Couture Bridal Gowns

By Fabric Type

- Satin Bridal Gowns

- Lace Bridal Gowns

- Tulle Bridal Gowns

- Silk Bridal Gowns

- Chiffon Bridal Gowns

- Organza Bridal Gowns

- Mixed Fabric Bridal Gowns

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 38% of global bridal gown revenue in 2025, making it the largest regional market. The region's dominance is supported by its exceptionally high annual marriage volumes, expanding middle-class population, rising disposable incomes, and strong cultural emphasis on elaborate wedding celebrations. China and India collectively account for a substantial share of global weddings annually, creating a significant addressable market for bridal apparel manufacturers.

Demand growth is being driven by increasing urbanization, rising female workforce participation, premiumization of wedding spending, and growing adoption of Western-style wedding ceremonies. In China, demand for designer bridal gowns is expanding due to growing luxury consumption and social media influence. India continues to witness rising adoption of white wedding gowns alongside traditional bridal attire, particularly among urban consumers. Japan and South Korea contribute significantly to premium bridal fashion demand through high per-wedding spending and strong demand for customized bridal services. The region is expected to remain the fastest-growing market globally, supported by expanding wedding industry ecosystems and increasing consumer spending on experiential weddings.

North America

North America represented approximately 29% of global market revenue in 2025 and remains one of the most valuable bridal fashion markets globally. The United States accounts for the majority of regional demand, supported by among the highest per-wedding expenditures worldwide. Bridal gowns often represent a significant portion of overall wedding budgets, creating strong demand for premium and designer collections.

Regional growth is being driven by increasing consumer preference for customized bridal gowns, destination weddings, luxury wedding experiences, and sustainable bridal fashion. Growing demand for inclusive sizing, body-positive designs, and personalized styling services is also reshaping product development strategies. Canada continues to demonstrate steady growth through increasing demand for sustainable bridal collections and premium bridal retail experiences. Strong e-commerce adoption and high consumer awareness of international designer brands further support market expansion.

Europe

Europe remains a leading premium bridal fashion market, supported by its established luxury fashion heritage and strong designer ecosystem. Italy, France, Spain, Germany, and the United Kingdom collectively account for the majority of regional bridal gown demand. The presence of globally recognized bridal designers and couture houses continues to position Europe as a center for premium bridal innovation.

Growth drivers include increasing demand for sustainable bridal fashion, growing popularity of rental and resale bridal models, and rising adoption of made-to-order collections. Southern European countries are benefiting from strong destination wedding activity, attracting international brides seeking luxury wedding experiences. Additionally, European consumers exhibit high environmental awareness, encouraging adoption of eco-friendly fabrics, ethical production practices, and circular fashion initiatives. Rising demand for minimalist and contemporary bridal aesthetics is further supporting product innovation across the region.

Latin America

Latin America represents an emerging growth market for bridal gowns, led primarily by Brazil and Mexico. The region benefits from a large young population, improving economic conditions, increasing urbanization, and growing adoption of premium wedding celebrations. Wedding ceremonies remain culturally significant across most Latin American countries, supporting consistent demand for bridal apparel.

Market growth is being driven by rising disposable incomes, expanding access to international bridal brands, and increasing influence of social media and celebrity wedding trends. Premium bridal fashion is gaining traction among affluent consumers, while mid-range products continue to dominate due to affordability considerations. Improvements in retail infrastructure and cross-border e-commerce accessibility are also enhancing product availability throughout the region.

Middle East & Africa

The Middle East and Africa region represents one of the highest-value bridal markets in terms of average selling prices. Countries such as the United Arab Emirates and Saudi Arabia continue to generate strong demand for couture bridal gowns, luxury designer labels, and highly customized wedding apparel. Large wedding budgets, lavish celebration traditions, and high disposable incomes among affluent consumers continue to support premium segment growth.

Regional growth is being driven by increasing luxury consumption, rising destination wedding activity, and growing investment in luxury hospitality infrastructure. The UAE has emerged as a key regional bridal fashion hub, attracting international designers and affluent bridal consumers from across the Gulf Cooperation Council countries. In Africa, South Africa remains the largest bridal apparel market due to increasing urbanization, expanding middle-class populations, and growing wedding expenditures. The emergence of modern bridal retail concepts and increasing exposure to international bridal fashion trends are expected to further accelerate regional demand growth throughout the forecast period.

Key Players in the Bridal Gowns Market

- Pronovias

- David's Bridal

- Maggie Sottero

- Essence of Australia

- Morilee

- Vera Wang Bride

- Rosa Clará

- Justin Alexander

- Monique Lhuillier

- Yumi Katsura

- Elie Saab Bridal

- Galia Lahav

- Amsale

- Oscar de la Renta Bridal

- WONA Concept