Black and White Pepper Market Size

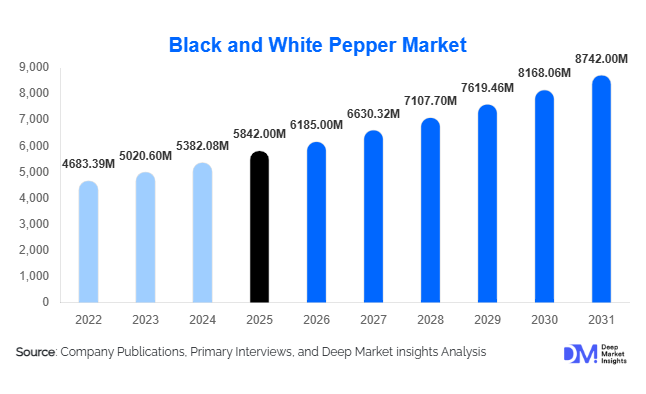

According to Deep Market Insights, the global black and white pepper market size was valued at USD 5,842 million in 2025 and is projected to grow from USD 6,185 million in 2026 to reach USD 8,742 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing global consumption of spices across processed food industries, rising demand for natural flavor enhancers, expanding international culinary exposure, and growing adoption of clean-label ingredients within food manufacturing.

Key Market Insights

- Food processing industries remain the largest consumers, accounting for a significant share of global pepper demand across seasoning blends, ready meals, and sauces.

- Asia-Pacific dominates production and consumption, supported by large cultivation bases in Vietnam and India and strong domestic culinary usage.

- Premium white pepper demand is rising due to growth in European and Asian gourmet cuisine applications.

- Export-driven trade structures continue shaping pricing trends, with Vietnam remaining the largest global exporter.

- Clean-label and organic spice demand is accelerating adoption among packaged food manufacturers.

- Automation and traceability technologies are improving quality control and supply chain transparency.

What are the latest trends in the black and white pepper market?

Shift Toward Natural Flavor Enhancers

Food manufacturers worldwide are replacing synthetic flavoring agents with natural spices, positioning pepper as a core ingredient in reformulated products. Black pepper, known for its pungency and universal culinary compatibility, is increasingly used in plant-based foods, meat alternatives, and ready-to-eat meals. This shift aligns with clean-label trends, where consumers actively seek recognizable ingredients with functional health benefits. Pepper’s antioxidant and digestive properties further enhance its positioning within functional food categories.

Premiumization and Origin-Based Branding

Single-origin pepper varieties such as Malabar, Tellicherry, and Lampong are gaining commercial importance. Buyers increasingly value traceability, terroir-based flavor differentiation, and sustainability certifications. Specialty retailers and gourmet food manufacturers are introducing premium pepper variants targeting high-income consumers and professional chefs. Packaging innovation, including grinder-ready formats and nitrogen-flushed packs, is extending shelf life while preserving aroma quality.

What are the key drivers in the black and white pepper market?

Expansion of Global Processed Food Industry

The rapid expansion of processed food production globally has significantly increased demand for standardized spice inputs. Pepper is among the most widely used seasoning ingredients across frozen foods, snacks, sauces, and instant meals. As urbanization accelerates and dual-income households grow, consumption of convenience foods continues to rise, directly strengthening pepper demand volumes worldwide.

Growth of International Cuisine Consumption

Globalization of culinary preferences has expanded pepper usage beyond traditional markets. Asian, Mediterranean, and fusion cuisines increasingly rely on pepper as a foundational spice. Restaurant chains and foodservice operators are expanding globally, driving consistent bulk procurement contracts with spice suppliers.

Health and Functional Ingredient Adoption

Piperine, the active compound in pepper, is associated with improved nutrient absorption and digestive health. Nutraceutical companies are incorporating pepper extracts into dietary supplements and functional beverages. This diversification beyond culinary applications has strengthened demand resilience.

What are the restraints for the global market?

Price Volatility Due to Climate Dependency

Pepper cultivation remains highly sensitive to weather conditions such as excessive rainfall, droughts, and pest outbreaks. Production fluctuations in major producing countries can cause sharp price volatility, affecting procurement planning for food manufacturers.

Supply Chain Fragmentation

The industry relies heavily on smallholder farmers, leading to inconsistent quality and traceability challenges. Lack of standardized post-harvest processing infrastructure in some producing regions increases contamination risks and export compliance complexities.

What are the key opportunities in the black and white pepper industry?

Organic and Sustainable Pepper Production

Rising consumer preference for organic food products presents a significant opportunity. Certified organic pepper commands premium pricing, particularly in Europe and North America. Investments in sustainable farming practices, fair-trade certification, and regenerative agriculture are enabling exporters to access high-margin markets.

Value-Added Processing and Pepper Extracts

Manufacturers are expanding into pepper oils, oleoresins, and extracts used in pharmaceuticals, cosmetics, and nutraceutical formulations. These high-value derivatives provide higher profit margins compared to raw pepper trading and reduce exposure to commodity price swings.

Emerging Market Consumption Growth

Rapid urbanization in Africa, Southeast Asia, and Latin America is increasing packaged food consumption. As modern retail expands, spice consumption patterns are shifting from loose formats to branded packaged pepper products, creating opportunities for multinational spice brands and private-label manufacturers.

Product Type Insights

The global black and white pepper market demonstrates strong product concentration patterns, with black pepper continuing to dominate overall consumption due to its versatility, affordability, and deep integration into global culinary systems. In 2025, black pepper accounts for nearly 72% of the global market share, reflecting its universal application across household cooking, industrial food processing, seasoning blends, and restaurant usage. The dominance of black pepper is largely attributed to minimal processing requirements compared to white pepper, resulting in lower production costs and higher supply availability. Additionally, black pepper retains a stronger pungency and aromatic profile due to the presence of outer fruit layers, making it the preferred choice for mass-market food formulations and spice blends.The leading segment driver for black pepper remains its extensive adoption in processed foods and convenience meals. As global urbanization accelerates and consumers increasingly rely on ready-to-eat and ready-to-cook products, manufacturers prioritize ingredients that deliver consistent flavor intensity while maintaining cost efficiency. Black pepper fulfills this requirement effectively, enabling standardized taste profiles across large-scale production environments. Furthermore, expanding quick-service restaurant chains worldwide rely heavily on black pepper seasoning to maintain flavor consistency across menus, reinforcing demand stability.White pepper holds approximately 28% market share, supported primarily by specialized culinary applications where appearance, texture, and milder flavor characteristics are critical. White pepper undergoes additional processing through soaking and removal of the outer skin, resulting in a smoother taste and lighter color. This makes it particularly desirable in European sauces, Asian soups, seafood dishes, and premium food preparations where visual aesthetics influence consumer perception.The growth driver for the white pepper segment stems from premiumization trends within global food markets. As consumers increasingly seek refined culinary experiences and restaurant-quality meals at home, food manufacturers and chefs adopt white pepper to enhance flavor without altering product appearance. Additionally, rising demand for premium packaged foods and gourmet cooking ingredients across developed economies is strengthening white pepper’s market expansion. Growth is also supported by higher price realization compared to black pepper, encouraging exporters to diversify product offerings toward value-added variants.Over the forecast period, product diversification strategies-including blended peppers, specialty grades, and origin-certified varieties-are expected to further reshape product segmentation dynamics. However, black pepper will remain the backbone of the global industry due to its scalability, widespread consumer familiarity, and compatibility with both traditional and modern food applications.

Form Insights

Market performance across pepper forms highlights the importance of supply chain efficiency, storage stability, and end-user convenience. Whole peppercorns lead the global market with approximately 41% market share, driven primarily by their extended shelf life and flexibility across multiple downstream applications. Whole peppercorns preserve volatile oils more effectively than processed forms, ensuring longer flavor retention during storage and transportation. This characteristic makes them particularly suitable for international bulk trade and industrial grinding operations.The leading segment driver for whole peppercorns is their strategic importance within global spice trading systems. Food manufacturers and spice processors prefer importing whole peppercorns because they allow customized grinding sizes, improved freshness control, and reduced contamination risks. Additionally, exporters favor whole pepper shipments due to lower spoilage rates and better logistics efficiency, strengthening this segment’s dominance.Ground pepper accounts for roughly 36% of market share, supported by rising retail convenience demand and increasing household adoption. Consumers increasingly prioritize ready-to-use cooking ingredients that reduce preparation time, particularly in urban markets where cooking habits are evolving toward efficiency. Ground pepper satisfies this requirement by offering immediate usability without grinders or additional preparation.The primary driver supporting ground pepper growth is retail modernization and private-label expansion. Supermarkets and branded spice companies continue launching packaged ground pepper products in varying pack sizes tailored to household consumption patterns. Growth in e-commerce grocery platforms further enhances accessibility, allowing consumers to purchase standardized spice products conveniently.Crushed pepper and specialty forms collectively represent around 23% market share, driven by evolving seasoning preferences and culinary experimentation. These formats are widely used in snack coatings, marinades, spice rubs, and gourmet seasoning blends. Foodservice operators increasingly incorporate crushed pepper for visual texture enhancement and flavor layering, contributing to steady demand expansion.Innovation in packaging technologies, including grinder bottles, resealable pouches, and moisture-resistant containers, is expected to further influence form-based demand distribution, enabling manufacturers to cater to both premium and mass-market consumers simultaneously.

Nature Insights

Based on nature classification, conventional pepper dominates the global market with approximately 85% market share, reflecting large-scale agricultural production and competitive pricing structures. Conventional farming practices benefit from established cultivation methods, higher yield outputs, and broader farmer participation across major producing countries such as Vietnam, India, Indonesia, and Brazil. These advantages enable consistent supply availability, making conventional pepper the preferred option for industrial buyers and price-sensitive markets.The leading driver for the conventional segment lies in large-volume procurement by food processing companies. Industrial manufacturers prioritize supply reliability and cost optimization, both of which are supported by conventional farming systems capable of meeting global demand volumes. Additionally, developing economies continue to rely heavily on conventional pepper due to affordability considerations among consumers.Despite its smaller share, organic pepper represents the fastest-growing segment, supported by rising consumer awareness surrounding food safety, sustainability, and clean-label consumption. Organic cultivation avoids synthetic pesticides and fertilizers, aligning with regulatory requirements and premium positioning strategies in North America and Europe. Organic pepper commands higher pricing, providing farmers with improved income potential and encouraging gradual acreage conversion.The growth driver for organic pepper stems from increasing demand for transparency and traceability across global food supply chains. Retailers and multinational food brands increasingly require certified ingredients to meet sustainability commitments and consumer expectations. As certification infrastructure improves in producing countries, organic pepper production is expected to expand steadily, narrowing the gap with conventional varieties over the long term.

Application Insights

Application-based segmentation highlights the central role of industrial food production in shaping global pepper demand. Food processing applications lead globally, contributing nearly 54% of total demand in 2025. Pepper serves as a foundational seasoning ingredient across processed meats, sauces, snacks, frozen foods, and ready meals, ensuring stable consumption regardless of economic cycles.The leading segment driver for food processing applications is the rapid expansion of convenience food consumption worldwide. Urban lifestyles, dual-income households, and evolving dietary habits have significantly increased reliance on packaged foods requiring standardized flavoring solutions. Pepper’s compatibility with diverse cuisines and preservation-enhancing properties make it indispensable within industrial formulations.Household retail consumption accounts for approximately 26% of demand, supported by growing home cooking trends and increased availability of branded spice products. Rising culinary experimentation influenced by social media and global cuisine exposure encourages consumers to incorporate spices more frequently into daily cooking.Foodservice applications represent around 15% share, driven by restaurant expansion, hospitality growth, and quick-service restaurant penetration across emerging markets. Pepper remains a universal seasoning ingredient used across cuisines, enabling consistent demand growth alongside global dining industry expansion.Pharmaceutical and nutraceutical applications, although smaller at roughly 5%, represent the fastest-growing application segment. Piperine, the bioactive compound in pepper, enhances nutrient absorption and is increasingly incorporated into dietary supplements and functional health formulations. The leading driver here is rising consumer focus on preventive healthcare and natural functional ingredients.

Distribution Channel Insights

Distribution dynamics demonstrate strong dominance of industrial procurement channels. B2B industrial supply accounts for nearly 63% share, reflecting bulk purchasing by food manufacturers, seasoning companies, and spice processors. Long-term supplier agreements and global commodity trading networks reinforce this channel’s leadership position.The leading driver for B2B dominance is large-scale food manufacturing expansion, which requires continuous supply of standardized raw materials. Pepper’s role as a high-volume seasoning ingredient ensures recurring procurement cycles, stabilizing demand within industrial channels.Retail supermarkets and hypermarkets contribute approximately 24% of total distribution, benefiting from organized retail growth and increased consumer preference for packaged, branded spices. Retailers continue expanding private-label spice portfolios to capture value-conscious consumers while maintaining product quality assurance.Online channels represent about 13% share but are expanding rapidly due to digital grocery adoption. E-commerce platforms enable access to premium, organic, and specialty pepper varieties previously unavailable in traditional retail environments. Subscription-based grocery models and direct-to-consumer spice brands further support online channel growth.

End-Use Analysis

The processed food industry remains the largest end-use sector, with global pepper consumption valued at over USD 3.2 billion. Pepper enhances flavor complexity, improves sensory appeal, and contributes mild antimicrobial properties that support product shelf stability. Growth in snack foods, frozen meals, and ready-to-eat categories continues to strengthen industrial consumption patterns.Meat processing represents another critical end-use area, as pepper is widely used in marinades, cured meats, sausages, and seasoning blends. The leading driver within this segment is increasing global protein consumption combined with rising demand for value-added meat products requiring standardized seasoning profiles.The nutraceutical industry is emerging as a high-growth end-use segment, expanding at over 9% annually. Piperine extracts are increasingly utilized to enhance bioavailability of vitamins and herbal compounds. Growing consumer interest in natural wellness solutions is accelerating adoption across dietary supplements and functional health products.Export-driven demand continues shaping industry dynamics, particularly with Vietnam and India serving as major suppliers to North America and Europe. Rising quick-service restaurant expansion across Asia and Africa further contributes to incremental pepper consumption growth, reinforcing long-term demand resilience.

| By Product Type | By Form | By Application | By Distribution Channel | By End Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global pepper market with approximately 46% market share in 2025, supported by its dual role as both the largest production hub and the fastest-growing consumption region. Vietnam leads global exports due to advanced cultivation techniques, competitive pricing, and strong international trade networks, while India and Indonesia maintain significant production capacities supported by favorable climatic conditions.The primary regional growth driver is the rapid expansion of food processing industries across emerging Asian economies. Increasing urbanization, rising disposable incomes, and changing dietary habits are accelerating demand for packaged and convenience foods requiring consistent spice inputs. Domestic consumption in China and India continues to rise as modern retail penetration and organized food manufacturing expand.India represents the fastest-growing consumption market within the region, driven by packaged food expansion, quick-service restaurant growth, and strong cultural reliance on spices. Government initiatives supporting agricultural exports and improvements in spice processing infrastructure further enhance regional competitiveness. Additionally, rising intra-regional trade agreements are facilitating smoother export flows, strengthening Asia-Pacific’s global dominance.

Europe

Europe accounts for nearly 21% market share, characterized by high product quality standards and strong demand for premium pepper varieties. Major markets including Germany, France, the United Kingdom, and the Netherlands drive regional consumption through well-developed food processing sectors and sophisticated retail systems.The leading regional growth driver is increasing consumer preference for organic and sustainably sourced spices. European regulations emphasizing traceability, pesticide limits, and ethical sourcing practices encourage importers to invest in certified supply chains. This has accelerated demand for organic pepper and origin-certified products.Additionally, Europe’s multicultural culinary landscape continues expanding demand for diverse spice applications, particularly within ethnic cuisines. Growth of plant-based food products and gourmet cooking trends further supports pepper consumption, as manufacturers reformulate recipes to enhance natural flavor profiles without artificial additives.

North America

North America represents a mature yet stable pepper market led primarily by the United States. Strong processed food manufacturing infrastructure and high per capita spice consumption underpin regional demand stability.The main regional growth driver is clean-label product reformulation across the food industry. Manufacturers increasingly replace synthetic flavor enhancers with natural spices such as pepper to meet consumer demand for recognizable ingredients. Rising popularity of international cuisines, including Asian and Latin American dishes, also contributes to higher spice utilization.Growth in health-conscious consumption patterns further supports demand, particularly within nutraceutical applications utilizing piperine extracts. E-commerce grocery expansion and premium spice branding strategies are also reshaping retail distribution dynamics across the region.

Middle East & Africa

The Middle East demonstrates strong import dependency, particularly in countries such as the United Arab Emirates and Saudi Arabia, where domestic agricultural production remains limited. Large hospitality and foodservice sectors drive consistent demand for spices, including pepper, across hotels, restaurants, and catering services.The leading regional growth driver is rapid tourism and foodservice industry expansion. International restaurant chains and hospitality investments increase spice consumption volumes while diversifying culinary offerings. Population growth and rising expatriate communities further amplify demand for global cuisines requiring pepper seasoning.Africa is emerging as a consumption growth hub driven by urbanization, expanding retail infrastructure, and increasing adoption of packaged foods. Improvements in distribution networks and supermarket penetration are gradually transforming traditional spice purchasing patterns, supporting long-term market development.

Latin America

Latin America shows steady market expansion led by Brazil and Mexico, supported by growing food processing industries and rising domestic consumption. Pepper is widely incorporated into regional cuisine, ensuring baseline demand stability.The primary regional growth driver is modernization of retail and food manufacturing sectors. Increasing investment in packaged food production and export-oriented food processing facilities is boosting industrial spice demand. Additionally, growing middle-class populations and rising convenience food consumption contribute to sustained market growth.Regional agricultural diversification efforts and expanding trade partnerships are expected to enhance pepper supply chain efficiency, enabling Latin America to strengthen its role both as a consumer and emerging exporter within the global pepper industry.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Black and White Pepper Market

- McCormick & Company, Inc.

- Olam Group Limited

- Kerry Group plc

- Associated British Foods plc

- Sensient Technologies Corporation

- Everest Spices

- MDH Spices

- DS Group

- Bart Ingredients Company Ltd.

- Ajinomoto Co., Inc.

- SHS Group

- Worlée Group

- Vinh Hiệp Co., Ltd.

- Nedspice Group

- Vietnam Spice Joint Stock Company