Yoghurt Market Size

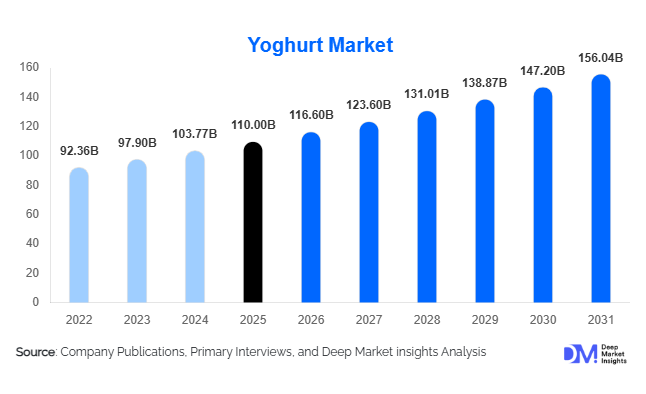

According to Deep Market Insights, the global yoghurt market size was valued at USD 110.0 billion in 2026 and is projected to grow from USD 116.6 billion in 2027 to reach USD 156.04 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The yoghurt market growth is primarily driven by rising consumer awareness of gut health and probiotics, increasing demand for high-protein functional foods, and the rapid expansion of plant-based and lactose-free dairy alternatives across global markets.

Key Market Insights

- Functional and probiotic yoghurt demand is rising globally, driven by growing awareness of digestive health and immunity benefits.

- Greek yoghurt continues to dominate premium dairy segments, supported by high protein content and fitness-oriented consumption patterns.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising disposable incomes, and expanding cold-chain infrastructure.

- Plant-based yoghurt alternatives are gaining strong traction, especially among lactose-intolerant and vegan consumers in urban economies.

- Supermarkets and hypermarkets remain the dominant distribution channel, while online grocery platforms are expanding rapidly.

- Health-conscious and low-fat variants are increasingly preferred, particularly among millennial and Gen Z consumers.

What are the latest trends in the global yoghurt market?

Growth of Plant-Based and Dairy-Free Yoghurt

One of the most significant trends in the yoghurt market is the rapid expansion of plant-based alternatives made from almond, oat, coconut, and soy. These products are gaining popularity among vegan consumers and individuals with lactose intolerance. Manufacturers are investing heavily in improving taste, texture, and nutritional parity with dairy yoghurt. This segment is particularly strong in North America and Europe, where clean-label and sustainable food choices are becoming mainstream. Continuous innovation in fermentation technology is further enhancing product quality and market acceptance.

Rise of Functional and High-Protein Yoghurt

Consumers are increasingly demanding yoghurt products enriched with functional ingredients such as probiotics, prebiotics, vitamins, collagen, and protein isolates. Greek yoghurt and skyr variants are leading this trend due to their high protein content and low sugar formulation. Fitness-oriented consumers and athletes are driving strong demand for protein-fortified snacks, making yoghurt a core component of sports nutrition diets. This trend is further supported by rising gym memberships and growing interest in preventive healthcare globally.

What are the key drivers in the yoghurt market?

Rising Health and Wellness Awareness

The growing global focus on health and wellness is a major driver of yoghurt consumption. Consumers are actively seeking foods that support digestion, immunity, and weight management. Yoghurt, being a natural probiotic-rich product, fits well into this trend. Increasing awareness of gut microbiome health has significantly boosted daily consumption of yoghurt across all age groups, especially in urban populations.

Expansion of Organized Retail and Cold Chain Infrastructure

The rapid growth of supermarkets, hypermarkets, and convenience stores, particularly in emerging economies, has significantly improved yoghurt accessibility. Investments in cold chain logistics and refrigeration infrastructure have enabled longer shelf life and wider distribution. This has allowed manufacturers to expand into rural and semi-urban markets, increasing overall consumption volumes globally.

Increasing Demand for Convenient Snacking

Changing lifestyles and busy work schedules have increased demand for ready-to-eat and portable nutrition products. Single-serve yoghurt cups and drinkable yoghurt formats are gaining popularity as convenient snack alternatives. This shift is particularly strong among working professionals and students, further boosting market penetration.

What are the restraints for the global yoghurt market?

Raw Material Price Volatility

Fluctuations in raw milk prices and dairy feed costs significantly impact production expenses in the yoghurt industry. Seasonal variations, climate change, and supply chain disruptions contribute to unstable pricing. This creates pressure on manufacturers to maintain profitability while keeping retail prices competitive.

Rising Competition from Alternative Healthy Snacks

The yoghurt market faces increasing competition from protein bars, plant-based desserts, and fortified beverages. These alternatives often target the same health-conscious consumer base, limiting yoghurt’s share in the broader functional food category. This competitive pressure is particularly strong in developed markets where product substitution is high.

What are the key opportunities in the yoghurt industry?

Expansion of Plant-Based Innovation

The growing vegan population and rising environmental concerns present a major opportunity for plant-based yoghurt manufacturers. Companies investing in high-quality dairy-free formulations with improved taste and protein content are expected to capture significant market share. This segment is also benefiting from sustainability-driven consumer preferences.

Growth in Personalized Nutrition Products

The rise of personalized nutrition is opening new opportunities for yoghurt products tailored to specific health needs such as weight management, immunity support, and digestive health. Fortified yoghurt with customized nutrient profiles is gaining traction in premium urban markets, creating strong potential for innovation-led growth.

Digital Retail and Subscription-Based Dairy Models

The expansion of online grocery platforms and direct-to-consumer dairy delivery services is transforming distribution channels. Subscription-based yoghurt delivery models are gaining popularity in urban regions, offering convenience, freshness, and customization. This trend is expected to significantly enhance market penetration in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 110 Billion |

| Market Size in 2026 | USD 116.6 Billion |

| Market Size in 2031 | USD 156.04 Billion |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global yoghurt market demonstrates a highly diversified product landscape, with distinct product types catering to evolving consumer preferences, nutritional requirements, and lifestyle patterns. Among these, Greek yoghurt continues to dominate the market and represents the leading segment in terms of value share. The primary driver behind the leadership of Greek yoghurt is its superior nutritional profile, particularly its high protein content, low sugar levels, and thick, creamy texture, which aligns strongly with the rising global demand for functional and protein-rich foods. Consumers increasingly associate Greek yoghurt with weight management, muscle recovery, and overall fitness, making it a staple in health-conscious diets. Additionally, aggressive marketing by leading dairy brands, coupled with widespread availability across developed and emerging markets, has further strengthened its position.Organic yoghurt is also gaining increasing traction, particularly in premium and urban retail channels. The demand for organic variants is driven by the clean-label movement, which emphasizes natural ingredients, minimal processing, and the absence of synthetic additives or pesticides. Consumers are willing to pay a premium for products perceived as healthier and environmentally responsible. This trend is particularly pronounced in developed markets, where regulatory frameworks and certification standards further reinforce consumer trust in organic products.Overall, the product type segment is characterized by a strong shift toward health-oriented, functional, and premium offerings. While traditional products continue to ensure volume stability, innovative and value-added segments are driving revenue growth and shaping the future trajectory of the global yoghurt market.

Application Insights

From an application perspective, the yoghurt market is primarily driven by retail consumption, which remains the largest and most dominant segment globally. The leading driver for this segment is the sustained and growing household demand for convenient, nutritious, and ready-to-eat food products. Yoghurt’s versatility as a breakfast item, snack, dessert, and even meal replacement contributes significantly to its widespread adoption across different age groups and demographics. The increasing penetration of packaged dairy products, particularly in emerging economies, has further accelerated retail consumption. Moreover, rising health awareness has encouraged consumers to incorporate yoghurt into daily diets due to its probiotic benefits, digestive health support, and nutrient density.The health and fitness nutrition segment is emerging as a high-growth application area, driven by the global surge in demand for protein-rich, functional, and performance-enhancing foods. Yoghurt, particularly high-protein variants such as Greek yoghurt and fortified products, is increasingly being consumed by athletes, fitness enthusiasts, and health-conscious individuals. The segment is further supported by the rising popularity of sports nutrition, dietary supplements, and wellness-focused lifestyles. Manufacturers are actively developing specialized yoghurt products with added nutrients, probiotics, and functional ingredients to cater to this niche yet rapidly expanding consumer base.Overall, the application landscape of the yoghurt market reflects a strong alignment with changing dietary habits, lifestyle trends, and the increasing integration of health and wellness into everyday consumption patterns. While retail remains the backbone of market demand, emerging applications in foodservice, industrial processing, and fitness nutrition are unlocking new growth opportunities.

Distribution Channel Insights

The distribution channel landscape of the global yoghurt market is evolving rapidly, driven by changing consumer shopping behaviors, technological advancements, and the expansion of retail infrastructure. Supermarkets and hypermarkets continue to dominate yoghurt sales, supported by their extensive product assortments, strong brand visibility, and the ability to offer competitive pricing through economies of scale. These retail formats provide consumers with a wide variety of options, including different flavors, packaging sizes, and product types, making them the preferred choice for bulk and routine purchases. The leading driver for this segment is the convenience of one-stop shopping combined with promotional activities and in-store visibility that influence purchasing decisions.Online retail is the fastest-growing distribution channel, reflecting the broader shift toward e-commerce and digital consumption. The primary driver of growth in this segment is the increasing consumer preference for convenience, home delivery, and time-saving shopping experiences. The rise of subscription models, digital payment systems, and targeted online promotions has further accelerated the adoption of online platforms for purchasing dairy products, including yoghurt. Additionally, improvements in cold chain logistics and last-mile delivery have addressed previous challenges associated with transporting perishable goods, enabling online channels to gain significant traction.

Explore more data points, trends and opportunities Download Free Sample Report

Yoghurt Market Segmentations

By Product Type

- Greek Yoghurt

- Set Yoghurt

- Stirred Yoghurt

- Drinkable Yoghurt

- Frozen Yoghurt

By Milk Source

- Cow Milk-Based Yoghurt

- Goat Milk-Based Yoghurt

- Sheep Milk-Based Yoghurt

- Plant-Based Alternatives

By Fat Content

- Full-Fat Yoghurt

- Low-Fat Yoghurt

- Fat-Free Yoghurt

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-Commerce

- Direct-to-Consumer (D2C) Channels

- Specialty Health Stores

- Foodservice

By Packaging Type

- Single-Serve Cups

- Multi-Pack Containers

- Drink Bottles

- Sachets & Pouches

- Tubs & Bulk Packaging

Regional Insights

North America

North America represents a mature yet highly dynamic yoghurt market, characterized by strong consumer awareness, high per capita consumption, and continuous product innovation. The United States is the primary contributor to regional demand, supported by high disposable income levels and a well-established retail infrastructure. One of the key drivers of growth in this region is the strong emphasis on health and wellness, which has led to increased consumption of protein-rich and functional yoghurt products, particularly Greek yoghurt. Consumers are actively seeking products that support digestive health, weight management, and overall well-being, driving demand for probiotic and fortified variants.The presence of major global and regional dairy companies, coupled with strong marketing and branding strategies, further supports market growth. Advanced cold chain logistics and widespread availability across retail channels ensure consistent product accessibility, reinforcing North America’s position as a key market for yoghurt.

Europe

Europe remains one of the largest and most established yoghurt markets globally, with deep-rooted cultural integration of dairy consumption. Countries such as France, Germany, and the United Kingdom exhibit high per capita yoghurt consumption, supported by long-standing dietary habits and a strong tradition of dairy production. One of the primary drivers of regional growth is the increasing demand for organic and natural food products. European consumers place a high value on quality, sustainability, and authenticity, driving the adoption of organic and clean-label yoghurt.Probiotic and functional yoghurt products are also gaining significant traction in Europe, driven by increasing awareness of gut health and preventive healthcare. The region’s strong retail infrastructure, coupled with widespread availability of diverse product offerings, further supports market growth. Overall, Europe’s yoghurt market is characterized by stability, innovation, and a strong emphasis on quality and sustainability.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for yoghurt, driven by a combination of demographic, economic, and lifestyle factors. Rapid urbanization, a growing middle-class population, and increasing disposable incomes are key drivers of demand in this region. Countries such as China, India, Japan, and South Korea are प्रमुख contributors, each exhibiting unique consumption patterns and growth dynamics.Cultural adaptability and product localization also play a crucial role in driving demand. Manufacturers are introducing region-specific flavors and formulations to cater to local tastes and preferences, thereby increasing consumer acceptance. Overall, Asia-Pacific offers significant growth opportunities, driven by its large population base and evolving consumer landscape.

Latin America

Latin America is experiencing steady growth in the yoghurt market, with Brazil and Mexico emerging as key contributors. The region’s growth is primarily driven by increasing health awareness and the gradual shift toward packaged and processed dairy products. Consumers are becoming more conscious of the nutritional benefits of yoghurt, particularly its role in digestive health and overall wellness.Urbanization and changing lifestyles are also contributing to the growth of the yoghurt market in Latin America. As more consumers adopt busy and fast-paced lifestyles, the demand for convenient and ready-to-eat food products is increasing. This trend is expected to drive continued growth in the coming years.

Middle East & Africa

The Middle East & Africa region is witnessing moderate growth in the yoghurt market, supported by a combination of demographic and economic factors. Rising urban populations, increasing disposable incomes, and the influence of Western dietary habits are key drivers of demand. Gulf countries, in particular, are significant importers of yoghurt products, driven by high consumption levels and limited domestic production capacity.Overall, the Middle East & Africa region presents a promising yet evolving market landscape, with growth driven by urbanization, retail development, and shifting consumer preferences toward healthier dietary options.

Key Players in the Global Yoghurt Market

- Danone S.A.

- Nestlé S.A.

- Lactalis Group

- Chobani LLC

- Fonterra Co-operative Group

- General Mills Inc. (Yoplait)

- Arla Foods

- FrieslandCampina

- Meiji Holdings Co., Ltd.

- Yakult Honsha Co., Ltd.

- Müller Group

- Saputo Inc.

- GCMMF (Amul)

- China Mengniu Dairy Company Limited

- Yili Group