Yeast Beta Glucan Market Size

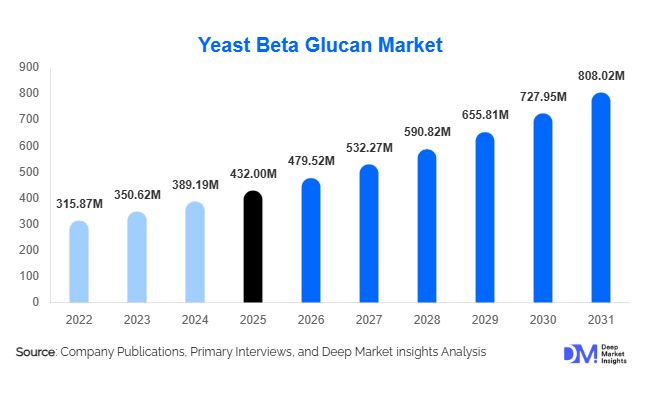

According to Deep Market Insights,the global yeast beta glucan market size was valued at USD 432 million in 2025 and is projected to grow from USD 479.52 million in 2026 to reach USD 808.02 million by 2031, expanding at a CAGR of 11.0% during the forecast period (2026–2031). Market growth is primarily driven by increasing global demand for immune-support ingredients, rising adoption of preventive healthcare solutions, and expanding applications of yeast-derived beta glucan across nutraceuticals, functional foods, pharmaceuticals, and animal nutrition industries. The growing preference for natural, clean-label bioactive ingredients and regulatory support for immune-health formulations are further strengthening market expansion globally.

Key Market Insights

- Immune health supplementation remains the primary growth driver, with yeast beta glucan increasingly integrated into daily wellness formulations rather than seasonal products.

- High-purity beta-1,3/1,6 glucan extracts dominate premium applications, particularly in pharmaceutical and clinical nutrition segments.

- North America leads global demand due to strong nutraceutical consumption and advanced supplement distribution networks.

- Asia-Pacific is the fastest-growing region, supported by expanding middle-class health awareness and fermentation manufacturing capacity.

- Animal feed producers are adopting beta glucan as an antibiotic alternative, accelerating demand across poultry and aquaculture industries.

- Technological advancements in extraction and microencapsulation are enabling wider use in beverages and functional foods.

What are the latest trends in the yeast beta glucan market?

Shift Toward Clinically Validated Functional Ingredients

The yeast beta glucan market is increasingly transitioning toward science-backed formulations supported by clinical trials and standardized bioactivity claims. Manufacturers are investing heavily in research demonstrating immune modulation, inflammation control, and metabolic health benefits. Pharmaceutical-grade beta glucan products with higher purity levels are gaining traction among medical nutrition providers and premium supplement brands. Regulatory approvals for functional claims in developed markets are further accelerating adoption. Companies are also emphasizing traceability and standardized molecular structures to meet pharmaceutical and clinical application requirements, transforming beta glucan from a commodity ingredient into a high-value bioactive compound.

Expansion into Functional Food and Beverage Applications

Food and beverage manufacturers are incorporating yeast beta glucan into fortified drinks, dairy alternatives, nutrition bars, and protein products. Advances in formulation technologies have improved taste neutrality and solubility, overcoming earlier application challenges. Consumers increasingly seek everyday foods that provide health benefits beyond basic nutrition, driving demand for immune-support ingredients integrated into routine consumption. Microencapsulation technologies allow improved stability during processing, enabling large-scale commercialization in ready-to-drink beverages and functional snacks. This shift is expanding the addressable market beyond supplements into mainstream consumer products.

What are the key drivers in the yeast beta glucan market?

Growing Preventive Healthcare Awareness

Consumers worldwide are prioritizing preventive health and immune resilience, significantly boosting demand for nutraceutical ingredients. Yeast beta glucan’s ability to activate immune responses has positioned it as a key component in daily wellness supplements. Aging populations and rising chronic disease prevalence are reinforcing consistent supplement consumption, supporting long-term demand stability. Healthcare professionals increasingly recommend immune-support products, further strengthening adoption across developed and emerging markets.

Antibiotic-Free Animal Nutrition Transition

Global regulations limiting antibiotic growth promoters in livestock production are driving adoption of immune-enhancing feed additives. Yeast beta glucan improves disease resistance, feed efficiency, and survival rates in poultry, swine, and aquaculture. Producers are incorporating functional feed solutions to maintain productivity while complying with regulatory standards. Rapid aquaculture expansion in Asia and Latin America is particularly contributing to strong growth in feed-grade beta glucan demand.

What are the restraints for the global market?

High Production and Purification Costs

The extraction and purification of yeast beta glucan require advanced fermentation and processing technologies, increasing production costs compared with plant-based alternatives. High purification standards necessary for pharmaceutical-grade products further elevate manufacturing expenses, limiting penetration in price-sensitive markets.

Lack of Standardized Quality Benchmarks

Variability in extraction methods across suppliers leads to differences in bioactivity and product consistency. The absence of universal global standards can slow regulatory approvals and create purchasing hesitancy among pharmaceutical manufacturers seeking consistent efficacy data.

What are the key opportunities in the yeast beta glucan industry?

Clinical Nutrition and Medical Applications

Growing clinical research supporting beta glucan’s immune and metabolic health benefits is opening opportunities within hospital nutrition, oncology recovery formulations, and medical foods. Pharmaceutical partnerships and prescription-based nutraceutical products are expected to create high-margin growth avenues. Increasing healthcare expenditure and demand for recovery-support nutrition further strengthen this opportunity.

Functional Feed and Aquaculture Expansion

The global push toward sustainable livestock production presents significant opportunities for yeast beta glucan suppliers. Aquaculture producers are adopting immune-support additives to reduce disease outbreaks and improve yield efficiency. As seafood consumption rises globally, feed manufacturers are scaling beta glucan inclusion rates, creating strong volume-driven demand growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 432 Million |

| Market Size in 2026 | USD 479.52 Million |

| Market Size in 2031 | USD 808.02 Million |

| CAGR | 11% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global yeast beta glucan market is strongly led by highly purified beta-1,3/1,6 glucan extracts, which account for nearly 41% of total demand. Their dominance is primarily driven by superior immunomodulatory bioactivity, higher purity standards, and strong clinical acceptance across pharmaceutical and premium nutraceutical formulations. Increasing scientific validation supporting immune enhancement, inflammation management, and metabolic health benefits has encouraged manufacturers to prioritize high-purity extracts for value-added applications. Insoluble beta glucan products continue to maintain substantial demand within animal nutrition, where cost efficiency combined with proven gut health and immune performance benefits supports widespread usage in livestock and aquaculture feed formulations. Meanwhile, soluble beta glucan variants are gaining rapid adoption in functional foods and beverage applications due to improved dispersibility, texture compatibility, and formulation flexibility, enabling incorporation into ready-to-drink beverages, dairy alternatives, and fortified snacks. Modified and encapsulated beta glucan formats are emerging as advanced product categories, driven by technological advancements aimed at improving bioavailability, stability during processing, and targeted nutrient delivery, particularly within next-generation dietary supplements and clinical nutrition products.

Application Insights

Dietary supplements and nutraceuticals represent the leading application segment, contributing approximately 44% of global demand, primarily driven by rising consumer focus on preventive healthcare, immune resilience, and daily wellness supplementation. Increasing aging populations, post-pandemic health awareness, and growing acceptance of scientifically supported functional ingredients continue to accelerate supplement adoption worldwide. Functional foods and beverages are experiencing strong expansion as food manufacturers integrate immune-support ingredients into everyday consumption formats, supported by clean-label trends and consumer preference for health benefits embedded within routine diets. Animal nutrition applications are expanding rapidly as producers increasingly adopt beta glucan as a natural alternative to antibiotic growth promoters, improving disease resistance and feed efficiency while aligning with evolving regulatory standards. Pharmaceutical and clinical nutrition applications are growing steadily as ongoing clinical research validates therapeutic benefits in immune recovery, oncology support, and metabolic health management. Personal care and cosmetic applications are emerging as a niche yet promising segment, leveraging beta glucan’s skin-repair, hydration enhancement, and anti-inflammatory properties in premium dermatological and cosmeceutical formulations.

Distribution Channel Insights

Direct manufacturer supply contracts dominate global distribution, accounting for over half of total sales as large nutraceutical, pharmaceutical, and feed manufacturers increasingly prioritize long-term sourcing agreements to ensure ingredient traceability, standardized quality, and price stability amid fluctuating raw material costs. Ingredient distributors continue to play a vital role in market accessibility by serving small and mid-scale manufacturers that lack direct procurement capabilities or large purchasing volumes. Contract manufacturing organizations are expanding their influence as supplement brands increasingly outsource formulation development, encapsulation, and large-scale production to reduce operational complexity and accelerate product commercialization timelines. Additionally, digital B2B ingredient procurement platforms are emerging as transformative distribution channels, improving transparency, shortening procurement cycles, and enabling regional manufacturers to access global suppliers more efficiently, thereby supporting market penetration across developing economies.

End-Use Industry Insights

Human nutrition and wellness remains the dominant end-use industry, contributing nearly 49% of global demand, driven by rising global supplement consumption, increasing health consciousness, and expanding preventive healthcare adoption across both developed and emerging economies. Growth in personalized nutrition trends and functional ingredient innovation further strengthens demand within this segment. Animal health and aquaculture represent the fastest-growing end-use category, supported by global regulatory pressure to reduce antibiotic usage, rising protein consumption, and increasing investments in sustainable livestock productivity solutions. Pharmaceutical and clinical nutrition sectors are gaining momentum as beta glucan becomes increasingly integrated into immune-support therapies, recovery nutrition products, and medically supervised dietary interventions supported by expanding clinical evidence. Cosmetic and dermatology applications are developing gradually but consistently, particularly within premium skincare segments focused on inflammation reduction, skin barrier repair, and microbiome-friendly formulations, reflecting the broader convergence between nutrition science and dermatological innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Yeast Beta Glucan Market Segmentations

By Product Type

- Beta-1,3/1,6 Yeast Beta Glucan (High Purity)

- Insoluble Yeast Beta Glucan

- Soluble Yeast Beta Glucan

- Modified & Microencapsulated Beta Glucan

By Application

- Dietary Supplements & Nutraceuticals

- Functional Foods & Beverages

- Animal Nutrition & Feed Additives

- Pharmaceuticals & Clinical Nutrition

- Personal Care & Cosmetics

By Distribution Channel

- Direct Manufacturer Sales (B2B Contracts)

- Ingredient Distributors

- Contract Manufacturing Organizations (CMOs)

- Online B2B Ingredient Platforms

By End-Use Industry

- Human Nutrition & Wellness Industry

- Animal Health & Aquaculture Industry

- Pharmaceutical & Clinical Nutrition Industry

- Cosmetics & Dermatology Industry

Regional Insights

North America

North America accounted for approximately 34% of the global yeast beta glucan market in 2025, led by the United States, where strong consumer awareness regarding immune health and preventive wellness continues to drive sustained product adoption. Regional growth is supported by high dietary supplement penetration, advanced nutraceutical research infrastructure, and continuous innovation from established ingredient manufacturers. Favorable regulatory clarity, widespread clinical research activity, and strong demand for premium, science-backed ingredients further enhance market expansion. Additionally, rising demand for clean-label functional foods and increasing pet and animal nutrition spending are reinforcing multi-industry consumption across the region.

Europe

Europe held nearly 28% market share, with Germany, France, and the United Kingdom representing key consumption hubs. Regional growth is strongly driven by stringent livestock antibiotic reduction policies, which have accelerated adoption of immune-enhancing feed additives such as yeast beta glucan. The region’s mature functional food sector, combined with high consumer preference for natural and clean-label ingredients, continues to stimulate innovation across bakery, dairy, and fortified food categories. Strong regulatory oversight promoting ingredient safety and sustainability, along with growing demand for plant-based and wellness-focused nutrition solutions, further supports long-term market expansion across Western and Northern Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by expanding healthcare awareness, rising disposable incomes, and rapidly growing nutraceutical manufacturing capabilities across China, Japan, South Korea, and India. China dominates global production capacity due to advanced fermentation expertise and large-scale manufacturing infrastructure, enabling competitive supply dynamics. Japan leads high-value nutraceutical consumption supported by an aging population and strong functional food culture, while India’s expanding supplement manufacturing ecosystem and increasing preventive healthcare awareness are significantly boosting domestic demand. Urbanization, e-commerce expansion, and government initiatives promoting health and nutrition further accelerate regional adoption across multiple end-use industries.

Latin America

Latin America is emerging as a high-potential growth region, led by Brazil and Mexico, where strong livestock and poultry industries are driving demand for immune-support feed additives. Regional growth is supported by expanding export-oriented meat production, increasing focus on animal health optimization, and gradual adoption of antibiotic-free farming practices aligned with international trade standards. Rising middle-class populations and improving awareness of dietary supplements are also contributing to expanding human nutrition applications, particularly in urban markets.

Middle East & Africa

The Middle East and Africa region is witnessing gradual but consistent market expansion supported by improving healthcare infrastructure and rising awareness of lifestyle-related health conditions. Countries such as the UAE and Saudi Arabia are experiencing increasing imports of premium nutraceutical products driven by higher disposable incomes and growing preventive healthcare adoption. Government healthcare investments and expanding retail supplement distribution channels are strengthening regional demand. Across Africa, early-stage adoption is primarily linked to livestock productivity improvement initiatives and increasing focus on animal disease prevention, creating long-term growth opportunities as agricultural modernization progresses.

Key Players in the Yeast Beta Glucan Market

- Kerry Group plc

- Lesaffre Group

- Lallemand Inc.

- Angel Yeast Co., Ltd.

- DSM-Firmenich

- Tate & Lyle PLC

- Kemin Industries

- Alltech Inc.

- AB Mauri

- Ohly GmbH

- Leiber GmbH

- Biotec Pharmacon ASA

- Garuda International Inc.

- Specialty Biotech Co., Ltd.

- Synergy Flavors Inc.