Women’s Sports Nutrition Market Size

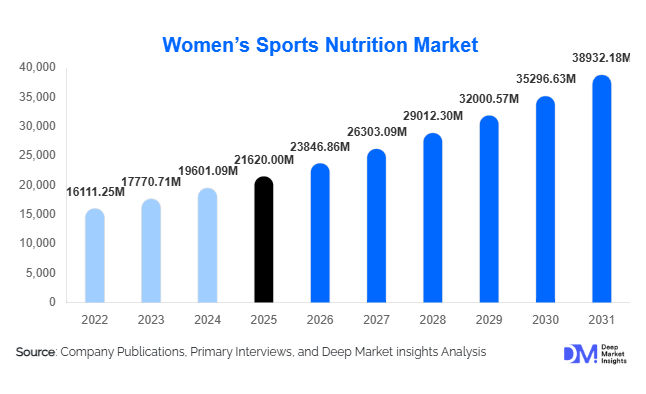

According to Deep Market Insights,the global women’s sports nutrition market size was valued at USD 21,620 million in 2025 and is projected to grow from USD 23,846.86 million in 2026 to reach USD 38,932.18 million by 2031, expanding at a CAGR of 10.3% during the forecast period (2026–2031). The market growth is primarily driven by rising female participation in fitness and competitive sports, increasing awareness of gender-specific nutritional requirements, and the growing demand for clean-label, plant-based, and functional performance supplements tailored to women’s health needs. The convergence of sports nutrition with beauty, preventive healthcare, and weight management categories is further accelerating innovation and product premiumization across global markets.

Key Market Insights

- Protein supplements dominate the market, accounting for nearly 42% of total revenue in 2025, driven by strong adoption for lean muscle development and weight management.

- Online retail channels lead distribution, contributing approximately 34% of global sales due to D2C expansion and influencer-led marketing.

- North America holds the largest regional share, representing about 38% of global demand in 2025.

- Asia-Pacific is the fastest-growing region, projected to expand at over 12% CAGR through 2031.

- Plant-based and clean-label formulations are among the fastest-growing subsegments globally.

- Women aged 25–34 years represent the largest consumer group, contributing nearly 36% of total market demand.

What are the latest trends in the women’s sports nutrition market?

Rise of Plant-Based and Clean-Label Formulations

Consumers are increasingly shifting toward plant-based protein blends derived from pea, rice, soy, and hemp. Lactose intolerance awareness, vegan lifestyle adoption, and sustainability concerns are driving this trend. Brands are investing in transparent sourcing, non-GMO certifications, and hormone-free formulations to build trust among female consumers. Clean-label positioning with minimal additives and natural sweeteners is reshaping purchasing behavior, particularly in North America and Europe.

Personalized and Hormone-Specific Nutrition

Companies are developing stage-specific formulations targeting menstrual health, pregnancy recovery, menopause support, and metabolic balance. Subscription-based supplement packs and AI-driven personalized nutrition recommendations are gaining traction. This trend reflects a shift from generic sports supplements toward clinically backed, hormone-responsive performance products tailored to women’s physiology.

What are the key drivers in the women’s sports nutrition market?

Increasing Female Fitness Participation

Women now account for nearly 45% of global gym memberships, significantly increasing demand for protein powders, pre-workout supplements, and recovery products. Strength training and endurance sports participation among women have risen steadily over the past five years, expanding the addressable market.

Preventive Healthcare and Weight Management Awareness

Growing concerns around obesity, metabolic disorders, and bone health are encouraging women to incorporate functional nutrition into daily routines. Sports nutrition products are increasingly perceived as preventive health supplements rather than athlete-exclusive products, widening consumer reach.

What are the restraints for the global market?

Regulatory Compliance and Labeling Constraints

Stringent regulations governing supplement claims across regions such as North America, Europe, and Asia increase compliance costs and slow product approvals. Variations in ingredient approvals and health claim standards create complexity for multinational brands.

Price Sensitivity in Emerging Economies

Premium sports nutrition products often carry higher price points, limiting penetration in price-sensitive markets. Imported formulations face additional cost burdens due to duties and logistics expenses, affecting affordability.

What are the key opportunities in the women’s sports nutrition industry?

Emerging Market Expansion

Rapid urbanization and rising female workforce participation in countries such as India, China, Brazil, and Indonesia are unlocking new demand pools. Localization strategies, smaller pack sizes, and omnichannel retail expansion can help brands penetrate these high-growth regions.

Integration of Beauty and Performance Nutrition

The growing popularity of collagen-based supplements that support skin, hair, and joint health alongside athletic recovery presents cross-category expansion opportunities. The convergence of beauty and sports nutrition is creating premium positioning potential and higher margin segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21620 Million |

| Market Size in 2026 | USD 23846.86 Million |

| Market Size in 2031 | USD 38932.18 Million |

| CAGR | 10.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Protein supplements continue to dominate the global women’s sports nutrition market, accounting for approximately 42% of total revenue in 2025. The leadership of this segment is primarily driven by rising female participation in resistance training, increasing awareness of daily protein requirements for muscle recovery and toning, and growing preference for clean-label and plant-based formulations. Within this category, plant-based protein powders and ready-to-drink shakes are witnessing double-digit growth as consumers seek lactose-free, vegan, and allergen-friendly alternatives. The shift toward holistic wellness has further accelerated demand for multi-functional protein blends fortified with vitamins, minerals, and adaptogens.

Weight management and fat-burning supplements contribute nearly 18% of the market, reflecting strong demand linked to lifestyle-related health concerns, including obesity, metabolic disorders, and sedentary work patterns. The segment benefits from increased digital fitness coaching, personalized nutrition apps, and social media–driven body transformation trends. Collagen and beauty-linked performance supplements are emerging rapidly, particularly in premium urban markets, as women increasingly seek products that combine athletic performance with skin health, hair strength, and anti-aging benefits. This convergence of beauty and sports nutrition is creating high-margin innovation opportunities across global markets.

Form Insights

Powder-based products dominate the market with nearly 38% share in 2025, supported by their cost efficiency, customizable dosage flexibility, and extended shelf life. The leading driver for this segment is consumer preference for personalized nutrition, allowing users to adjust serving sizes, blend with smoothies, and integrate supplements into daily meal routines. Bulk packaging and subscription-based online sales models further strengthen powder format penetration, especially among regular gym-goers.

Ready-to-drink (RTD) formulations represent the fastest-growing form, driven by convenience, portability, and increasing on-the-go consumption among working women and fitness enthusiasts. The growth of urban lifestyles, rising office-based employment, and expanding retail refrigeration infrastructure support this trend. Additionally, improved flavor innovation and low-sugar formulations are enhancing repeat purchase rates in developed and emerging markets alike.

Distribution Channel Insights

Online retail leads the global market with approximately 34% share in 2025, primarily driven by expanding e-commerce penetration, influencer marketing, and subscription-based direct-to-consumer strategies. The leading growth driver in this segment is the ability of digital platforms to offer personalized product recommendations, bundle discounts, and transparent ingredient comparisons. Direct-to-consumer platforms and major e-commerce marketplaces allow niche and women-focused brands to scale rapidly while maintaining higher margins.

Specialty nutrition stores and pharmacies remain strong offline channels, particularly for premium, clinically positioned, and medically endorsed supplements. These channels benefit from in-store consultation services, pharmacist recommendations, and higher consumer trust in regulated environments. Supermarkets and hypermarkets continue to expand shelf space for women-centric sports nutrition products as mainstream adoption increases.

Age Group Insights

Women aged 25–34 years represent the largest consumer segment, contributing nearly 36% of total market revenue in 2025. The primary driver of dominance in this demographic is the combination of high disposable income, strong social media influence, career-stage financial independence, and active lifestyle adoption. This age group shows strong engagement in gym memberships, boutique fitness studios, marathon participation, and digital wellness programs.

The 35–44 age segment is expanding steadily due to increasing awareness around hormonal balance, metabolic health, bone density maintenance, and preventive healthcare. Demand within this group is particularly strong for collagen supplements, plant-based proteins, and products targeting energy support and lean muscle preservation. Older demographics are gradually entering the category as healthy aging trends gain momentum globally.

Fitness Goal Insights

Weight management leads the market with approximately 31% share in 2025, supported by rising urbanization, sedentary lifestyles, and growing concerns regarding obesity and metabolic health. The leading driver of this segment is the integration of nutrition supplementation with structured diet programs, wearable fitness devices, and calorie-tracking applications that encourage measurable progress.

Muscle building and strength training follow closely as more women adopt resistance training programs, CrossFit, and high-intensity interval training routines. Increased visibility of female athletes, fitness influencers, and body-positive movements is reshaping traditional perceptions around strength training, significantly expanding demand for protein-rich and performance-enhancing formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Women’s Sports Nutrition Market Segmentations

By Product Type

- Protein Supplements

- Functional Foods

- Sports Drinks

- Amino Acids & BCAAs

- Pre-Workout & Post-Workout Formulations

- Weight Management & Fat Burners

- Collagen & Beauty-Linked Performance Supplements

- Plant-Based Sports Nutrition Products

By Form

- Powder

- Ready-to-Drink (RTD)

- Capsules & Tablets

- Bars

- Gummies & Soft Chews

By Distribution Channel

- Online Retail (D2C & E-commerce Platforms)

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Pharmacies & Drug Stores

- Fitness Centers & Health Clubs

By Age Group

- 15–24 Years

- 25–34 Years

- 35–44 Years

- 45 Years & Above

By Fitness Goal

- Muscle Building & Strength Training

- Weight Management

- Endurance & Athletic Performance

- General Wellness & Active Lifestyle

Regional Insights

North America

North America accounts for approximately 38% of the global women’s sports nutrition market in 2025, with the United States contributing nearly 75% of regional demand. Regional growth is driven by high gym penetration rates, strong presence of direct-to-consumer supplement brands, advanced product innovation pipelines, and widespread acceptance of premium and functional nutrition products. The mature e-commerce ecosystem and subscription-based wellness models further accelerate adoption. In Canada, growth is supported by rising clean-label awareness, strong demand for plant-based proteins, and regulatory emphasis on product safety and ingredient transparency.

Europe

Europe represents around 27% of global market share in 2025, led by Germany, the United Kingdom, and France. Regional expansion is driven by increasing female participation in organized sports, sustainability-focused purchasing behavior, and stringent regulatory standards that enhance consumer confidence. Demand is strongly shaped by clean-label positioning, organic certifications, and environmentally responsible packaging. Western Europe shows particularly strong adoption of plant-based proteins and vegan sports nutrition products, while Eastern Europe is witnessing rising demand due to expanding fitness infrastructure and growing middle-class populations.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 12% CAGR through 2031. Growth is primarily fueled by rapid urbanization, rising disposable incomes, increasing digital fitness engagement, and expanding awareness of preventive health among women. China and India serve as major growth engines due to expanding middle-class populations, higher female workforce participation, and rapid e-commerce penetration. Japan and Australia maintain stable demand supported by mature supplement markets, high product quality standards, and strong health-conscious consumer bases. Regional brands are increasingly launching localized flavors and culturally adapted formulations to capture diverse consumer preferences.

Latin America

Brazil and Mexico lead regional demand, supported by rising sports participation, expanding urban middle-class populations, and growing social media–driven fitness culture. Regional growth is further driven by improving retail distribution networks and increasing domestic manufacturing capabilities, which enhance affordability and product accessibility. Government-led public health initiatives targeting obesity reduction also contribute to higher awareness and supplement adoption among women.

Middle East & Africa

The United Arab Emirates and Saudi Arabia are emerging as high-value markets supported by government-backed fitness initiatives, increasing female workforce participation, and rapid expansion of premium fitness centers. Rising health awareness campaigns and lifestyle diversification under economic transformation programs are accelerating demand. In sub-Saharan Africa, South Africa leads regional consumption due to comparatively developed retail infrastructure and a growing urban fitness community. Overall regional growth is supported by expanding modern trade channels and increasing availability of imported premium sports nutrition brands.

Key Players in the Women’s Sports Nutrition Market

- Glanbia plc

- Herbalife Ltd.

- Nestlé Health Science

- Abbott Laboratories

- PepsiCo Inc.

- The Hut Group

- Orgain Inc.

- Garden of Life LLC

- Transparent Labs

- MusclePharm Corporation

- GNC Holdings LLC

- Optimum Nutrition

- Myprotein

- Isopure Company

- Vega (Danone)