Whipped Topping Market Size

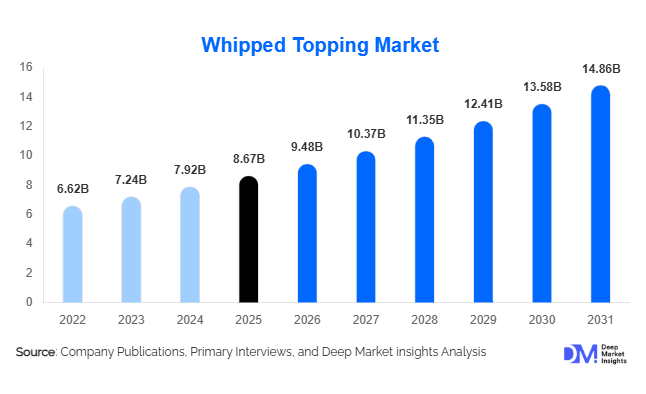

According to Deep Market Insights, the global whipped topping market size was valued at USD 8.67 billion in 2025 and is projected to grow from USD 9.48 billion in 2026 to reach USD 14.86 billion by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The whipped topping market growth is primarily driven by rising demand for premium bakery and dessert products, increasing consumption of specialty beverages, and the rapid expansion of non-dairy and plant-based whipped topping solutions across retail and foodservice sectors globally.

Key Market Insights

- Non-dairy whipped toppings dominate the market, supported by growing vegan preferences, lactose intolerance awareness, and cost-efficiency advantages for foodservice operators.

- Bakery and confectionery applications remain the largest revenue contributors, fueled by rising consumption of cakes, pastries, frozen desserts, and premium ready-to-eat desserts globally.

- North America leads the global whipped topping market, driven by strong café culture, high dessert consumption, and extensive adoption of aerosol whipped topping products.

- Asia-Pacific is the fastest-growing regional market, supported by urbanization, westernized eating habits, and rapid growth of bakery chains and quick-service restaurants.

- Plant-based whipped toppings are witnessing accelerated innovation, with manufacturers launching coconut-based, oat-based, and almond-based formulations targeting health-conscious consumers.

- Technological advancements in emulsification, aerosol packaging, and frozen stabilization are improving product shelf life, texture consistency, and distribution efficiency.

Whipped Topping Market Trends

Rapid Expansion of Plant-Based and Clean-Label Products

The whipped topping market is increasingly shifting toward plant-based and clean-label formulations as consumers seek healthier and allergen-friendly alternatives. Manufacturers are launching whipped toppings made from coconut, oat, soy, and almond ingredients to cater to vegan and lactose-intolerant consumers. Demand for products free from artificial preservatives, synthetic stabilizers, and hydrogenated fats is growing rapidly, particularly across North America and Europe. Clean-label innovation is becoming a major differentiator, with companies investing heavily in natural emulsifiers, organic certifications, and reduced-sugar formulations. Foodservice operators are also adopting premium plant-based whipped toppings to align with changing consumer dietary preferences and sustainability expectations.

Growing Integration in Specialty Beverages and Café Culture

Whipped toppings are increasingly being utilized in premium beverages including cold coffees, frappes, flavored lattes, milkshakes, bubble tea, and frozen beverages. The expansion of global café chains and artisanal beverage outlets is significantly boosting institutional demand for whipped toppings with stable texture and long shelf life. Social media-driven food presentation trends are further accelerating demand for visually appealing beverage toppings. Manufacturers are developing customized flavor variants such as caramel, mocha, hazelnut, and seasonal formulations to support café menu innovation. The growing influence of coffeehouse culture in Asia-Pacific and the Middle East is creating substantial opportunities for whipped topping suppliers serving commercial beverage applications.

Whipped Topping Market Drivers

Rising Consumption of Bakery and Dessert Products

The growing global bakery industry is one of the strongest drivers for whipped topping demand. Cakes, pastries, waffles, pancakes, cupcakes, mousse desserts, and frozen confectionery products extensively utilize whipped toppings for decoration, texture enhancement, and flavor enrichment. Increasing urbanization, rising disposable income, and changing consumer lifestyles are driving higher consumption of premium bakery items globally. Celebration-oriented food culture and increasing demand for aesthetically appealing desserts are also contributing significantly to market expansion. Industrial bakeries and packaged dessert manufacturers continue to increase procurement of whipped toppings due to operational convenience and product consistency.

Expansion of Foodservice and Café Chains

The rapid expansion of café chains, quick-service restaurants, and dessert-focused foodservice outlets is accelerating global whipped topping consumption. International coffee chains are increasingly incorporating whipped toppings into beverages and desserts to improve product differentiation and customer experience. Emerging markets such as India, China, Indonesia, Saudi Arabia, and Brazil are witnessing rapid growth in café density and western-style dessert consumption. Foodservice operators prefer whipped toppings with longer shelf life, better temperature stability, and ease of application, encouraging strong demand for frozen and aerosol-based products. This trend is expected to remain a major long-term growth driver for the market.

Whipped Topping Market Restraints

Volatility in Dairy and Vegetable Oil Prices

The whipped topping market remains vulnerable to fluctuations in dairy cream, palm oil, coconut oil, and emulsifier prices. Climatic disruptions, geopolitical instability, and agricultural supply constraints can significantly affect raw material availability and pricing structures. Rising input costs directly impact manufacturing margins and increase pricing pressure on suppliers operating in highly competitive retail and foodservice markets. This volatility creates procurement challenges for manufacturers dependent on stable ingredient sourcing.

Stringent Food Labeling and Regulatory Compliance

Governments across Europe and North America are implementing stricter regulations regarding trans fats, artificial additives, allergen declarations, and clean-label compliance. Manufacturers using synthetic stabilizers or partially hydrogenated oils are increasingly required to reformulate products to meet evolving food safety standards. Compliance with international labeling requirements and sustainability regulations also raises operational complexity and production costs. Smaller manufacturers often face difficulties in managing reformulation investments and regulatory adaptation.

Whipped Topping Market Opportunities

Premium Plant-Based Product Innovation

The rapid expansion of vegan and dairy-free food categories presents substantial opportunities for whipped topping manufacturers. Premium plant-based whipped toppings made from oat, almond, and coconut ingredients are gaining strong traction among health-conscious consumers. Manufacturers introducing organic, low-sugar, and clean-label products can capture higher-margin market segments and differentiate themselves through innovation. Foodservice chains are increasingly integrating plant-based toppings into beverages and desserts to align with consumer demand for sustainable and allergen-friendly offerings. This shift is expected to create significant growth opportunities across both developed and emerging economies.

Expansion of Emerging Market Foodservice Infrastructure

Developing economies across Asia-Pacific, Latin America, and the Middle East are witnessing rapid expansion of bakery chains, café brands, hotels, and quick-service restaurants. Rising disposable income and westernization of eating habits are increasing demand for premium desserts and specialty beverages that utilize whipped toppings extensively. Manufacturers establishing regional production facilities and cold-chain networks in these high-growth markets can significantly improve market penetration and reduce logistics costs. Institutional demand from hotels, catering companies, and industrial bakeries is expected to create strong long-term growth opportunities for whipped topping suppliers globally.

Product Type Insights

Homofermentative inoculants continue to dominate the global silage inoculants market, accounting for nearly 38% of total market revenue in 2025. The leadership of this segment is primarily driven by the growing requirement for rapid fermentation efficiency, improved nutrient retention, and minimized dry matter loss during forage preservation. These inoculants are highly effective in accelerating lactic acid production, which rapidly lowers silage pH and prevents the growth of undesirable microorganisms. Their widespread adoption across corn silage and grass silage applications is particularly strong in large-scale dairy operations where feed consistency and animal productivity are critical economic factors. The increasing commercialization of dairy farming across developed and emerging economies has further strengthened demand for homofermentative solutions, especially among producers seeking improved milk yield and optimized feed conversion efficiency.Combination inoculants integrating both homofermentative and heterofermentative bacterial strains are emerging as one of the fastest-growing product categories. Large dairy farms and integrated livestock operations are increasingly investing in multifunctional inoculant solutions capable of simultaneously improving fermentation quality, aerobic stability, and nutrient preservation. The segment is benefiting from continuous advancements in microbial engineering and customized bacterial strain development tailored to specific forage types and climatic conditions. Enzyme-based inoculants are also gaining momentum as premium feed preservation products due to their ability to improve fiber degradation, starch availability, and nutrient digestibility. High-performance livestock operations focused on maximizing animal productivity are increasingly utilizing enzyme-enhanced inoculants to improve feed efficiency and overall herd performance.

Crop Type Insights

Corn silage remains the dominant crop segment within the global silage inoculants market, accounting for approximately 42% of overall market demand in 2025. The segment’s leadership is strongly supported by the extensive cultivation of corn across North America, Europe, and China, combined with its superior energy density and highly favorable fermentation characteristics. Corn silage provides high digestible energy content required for commercial dairy and beef cattle operations, making it one of the most widely preserved forage crops globally. Increasing demand for high-quality animal nutrition and rising milk production targets continue to strengthen inoculant adoption within corn silage applications. Mechanized harvesting systems and precision silage management technologies have further accelerated inoculant penetration in commercial corn forage production.Sorghum and cereal crop silage segments are witnessing accelerating growth, especially across drought-prone and water-scarce agricultural regions. Climate variability, rising water conservation concerns, and increasing pressure on irrigation resources are encouraging livestock producers to shift toward resilient forage crops such as sorghum. These crops require lower water input while still supporting acceptable nutritional performance, thereby increasing the importance of inoculants in maintaining silage quality. Mixed forage silage applications are also expanding rapidly as integrated livestock operators seek balanced nutritional profiles, feed diversity, and improved herd health outcomes. The trend toward customized forage blends is creating new growth opportunities for specialized inoculant formulations designed for multiple crop combinations.

Form Insights

Dry silage inoculants dominate the market with nearly 61% share due to their superior shelf stability, ease of transportation, reduced storage costs, and operational convenience. Powder and granular inoculants are extensively utilized across commercial dairy farms and beef feedlots because they are highly compatible with mechanized forage harvesting equipment and automated silage application systems. The dominance of dry formulations is also supported by their longer product lifespan and reduced risk of microbial degradation during storage and distribution. Livestock operators increasingly prefer dry inoculants because they simplify logistics management and reduce handling complexity during large-scale silage preparation.Liquid silage inoculants are also experiencing growing adoption due to the increasing use of precision application technologies within advanced livestock farming systems. Liquid formulations provide highly accurate dosing capabilities and uniform bacterial coverage, making them particularly suitable for high-moisture silage and precision forage preservation applications. The segment is benefiting from advancements in liquid formulation stability, enhanced microbial survivability, and automated spraying technologies integrated within modern harvesting equipment. Increasing digitalization of livestock farming and precision feed management practices are expected to support future expansion of the liquid inoculants segment over the forecast period.

Livestock Application Insights

Dairy cattle feed remains the largest livestock application segment, contributing nearly 47% of global market revenue in 2025. The segment’s dominance is primarily driven by continuously rising global milk demand, expanding commercial dairy herd sizes, and increasing emphasis on feed efficiency optimization. Silage inoculants play a critical role in preserving forage nutritional quality, minimizing feed losses, and improving rumen digestibility, all of which directly influence milk productivity and farm profitability. Commercial dairy operators increasingly invest in high-quality inoculants to maintain consistent forage availability throughout the year and reduce dependence on fluctuating feed markets.Beef cattle feedlots represent another major application segment, particularly across North America, Brazil, and Argentina where industrial beef production systems rely heavily on large-scale forage preservation. Increasing global beef consumption and export-oriented livestock production are encouraging feedlot operators to improve silage quality and reduce feed wastage. Sheep, goat, swine, and equine feed applications are also witnessing gradual expansion due to rising awareness regarding nutritional optimization and improved feed management practices. Small and medium livestock producers are increasingly recognizing the economic benefits associated with reduced spoilage and improved forage digestibility.

Distribution Channel Insights

Direct sales channels continue to dominate the global silage inoculants market, accounting for approximately 40% of total market revenue. Large commercial dairy farms, feedlots, and integrated livestock producers increasingly prefer direct procurement agreements with manufacturers due to access to customized microbial recommendations, technical consultation services, and after-sales support. The growing complexity of forage preservation requirements has strengthened the importance of direct manufacturer relationships, particularly among large-scale livestock operations seeking tailored inoculant solutions based on crop type, moisture level, and climatic conditions.Manufacturers are increasingly expanding their field support teams and technical advisory services to strengthen long-term customer retention and improve product performance outcomes. The rising adoption of precision livestock farming technologies is also supporting direct sales growth as producers seek data-driven forage preservation strategies and performance monitoring solutions.Agricultural cooperatives and specialty feed additive distributors remain highly important channels across Europe, Latin America, and emerging agricultural economies where regional distribution networks play a critical role in reaching smaller livestock operators. These channels provide localized technical guidance and improve product accessibility in rural farming regions. Meanwhile, online agricultural platforms are gradually expanding due to increasing digital agriculture adoption and growing smartphone penetration within farming communities. E-commerce channels are improving accessibility for small and medium-scale livestock operators seeking efficient product comparison and procurement capabilities.

End-Use Insights

Commercial dairy farms remain the leading end-use segment within the silage inoculants market due to their significant forage consumption requirements and continuous focus on maximizing milk productivity. Large dairy operators increasingly prioritize silage quality management to reduce nutritional losses and maintain stable feed supply throughout seasonal fluctuations. The growing industrialization of dairy production across both developed and developing economies continues to strengthen inoculant demand within this segment.Beef feedlots are also rapidly increasing adoption rates as industrial livestock systems emphasize feed consistency, nutrient preservation, and operational efficiency. High-volume forage storage requirements within commercial beef operations make silage inoculants essential for minimizing spoilage and improving feed conversion ratios. Increasing pressure to improve meat production efficiency and profitability is encouraging broader inoculant utilization within beef cattle systems.Feed manufacturers and vertically integrated livestock producers are becoming increasingly important consumers of silage inoculants as compound feed production expands globally. These organizations prioritize stable raw material quality and long-term feed cost optimization, thereby supporting advanced forage preservation practices. Contract silage producers are emerging as a rapidly expanding customer segment in developed agricultural markets where outsourced forage harvesting and preservation services are becoming increasingly common. The growing professionalization of forage management services is expected to further support market expansion over the coming years.

| By Product Type | By Form | By Flavor | By Nature | By Application |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of the global silage inoculants market in 2025, making it the leading regional market. The region’s dominance is strongly supported by advanced dairy farming systems, widespread mechanization of forage harvesting, and extensive corn silage production across the United States and Canada. The United States remains the largest contributor to regional demand due to high adoption of precision livestock farming technologies and increasing emphasis on feed efficiency optimization. Commercial dairy farms and beef feedlots across the country continue investing heavily in advanced forage preservation strategies to minimize feed losses and maximize animal productivity.Another major regional growth driver is the strong presence of technologically advanced feed additive manufacturers and agricultural biotechnology companies continuously investing in microbial innovation. Increasing focus on reducing operational costs and improving sustainability within livestock farming is encouraging producers to adopt biological inoculant solutions over conventional preservation methods. Canada also contributes significantly to market growth due to strict forage quality standards, rising dairy productivity investments, and increasing awareness regarding nutrient preservation. Favorable government support for sustainable livestock farming practices and precision agriculture technologies further strengthens regional market expansion.

Europe

Europe held nearly 28% of global market share in 2025, supported by highly developed dairy industries across Germany, France, the Netherlands, and the United Kingdom. Regional growth is primarily driven by strong demand for sustainable and biologically derived feed additives as European livestock producers increasingly move away from chemical preservatives. Strict environmental regulations and growing consumer preference for natural livestock production practices are accelerating inoculant adoption throughout the region.The region also benefits from advanced forage harvesting infrastructure, widespread scientific silage management practices, and strong research support for microbial feed technologies. Western European countries are witnessing rising demand for organic-certified inoculants and clean-label livestock production systems, encouraging manufacturers to develop environmentally sustainable microbial formulations. Germany continues to serve as a major agricultural technology hub, while France and the Netherlands maintain strong dairy export industries that rely heavily on consistent forage quality. Increasing pressure to reduce greenhouse gas emissions and improve feed efficiency within European livestock systems is expected to continue driving market growth.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market, expanding at a CAGR exceeding 10% during the forecast period. Rapid livestock industrialization, increasing dairy modernization, and rising animal protein consumption are major drivers supporting regional expansion. China dominates regional demand due to large-scale dairy farm expansion, increasing adoption of commercial feed systems, and strong government support for agricultural productivity enhancement. The country’s growing focus on feed quality management and import substitution in dairy production continues to strengthen inoculant demand.Rapid urbanization, rising disposable income, and increasing demand for high-quality dairy and meat products across Southeast Asia are also contributing significantly to market growth. The expansion of commercial livestock farms, improved cold-chain infrastructure, and rising mechanization of forage harvesting operations are expected to further strengthen long-term regional demand.

Latin America

Latin America accounted for nearly 14% of global market demand in 2025, led primarily by Brazil and Argentina. The region’s strong beef and dairy export industries continue supporting large-scale forage preservation practices and increasing inoculant utilization. Brazil represents the largest regional market due to its rapidly expanding commercial livestock sector and growing focus on improving feed conversion efficiency and export competitiveness.Government support for agricultural modernization and livestock productivity enhancement remains a major regional growth driver. Increasing investments in mechanized forage harvesting systems, silage storage infrastructure, and feed management technologies are supporting broader inoculant adoption among commercial producers. Argentina also maintains substantial demand due to its highly developed beef production industry and increasing emphasis on year-round forage availability. Rising climate variability and the need for improved drought resilience are encouraging producers across the region to adopt advanced silage preservation technologies capable of reducing feed losses and improving livestock productivity.

Middle East & Africa

The Middle East & Africa region is witnessing steady market growth due to rising investments in food security, livestock industrialization, and climate-resilient agricultural systems. Harsh climatic conditions and limited natural grazing availability are encouraging livestock producers to increasingly depend on preserved forage solutions. Saudi Arabia and the United Arab Emirates remain major regional markets because of expanding industrial dairy operations, rising demand for premium dairy products, and substantial investments in technologically advanced livestock farming infrastructure.South Africa continues to represent a key African market due to its relatively developed commercial livestock sector and growing adoption of modern forage preservation practices. Regional governments are increasingly supporting agricultural diversification and livestock productivity improvement initiatives aimed at reducing dependence on food imports. Rising awareness regarding feed efficiency, nutrient preservation, and year-round forage availability is expected to continue supporting inoculant adoption across both dairy and beef production systems. Increasing investments in irrigation efficiency, forage crop cultivation, and modern feed management technologies are likely to create additional long-term growth opportunities throughout the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Whipped Topping Market

- Rich Products Corporation

- Conagra Brands, Inc.

- FrieslandCampina

- Fonterra Co-operative Group

- Puratos Group

- Dawn Foods

- Lactalis Group

- Ornua Co-operative Limited

- CSM Ingredients

- Müller Group

- Gay Lea Foods

- Fuji Oil Holdings

- Kerry Group

- Nestlé S.A.

- Dr. Oetker