Whey Protein Muscle Gainer Market Size

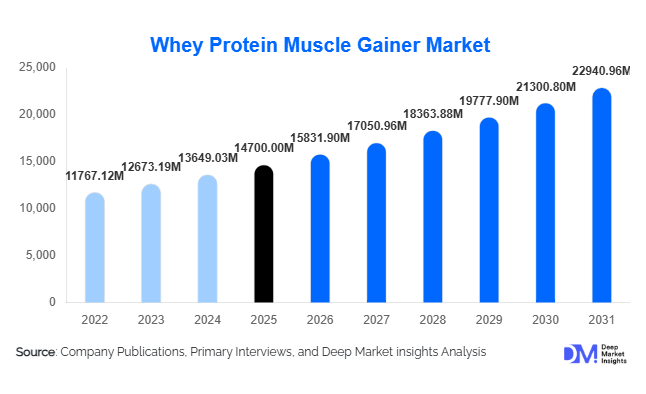

According to Deep Market Insights,the global whey protein muscle gainer market size was valued at USD 14,700 million in 2025 and is projected to grow from USD 15,831.90 million in 2026 to reach USD 22,940.96 million by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The market growth is primarily driven by rising global fitness participation, increasing demand for high-protein nutritional supplements, expanding gym memberships, and growing awareness regarding muscle recovery and weight management. The transition of muscle gainers from niche bodybuilding supplements to mainstream fitness nutrition products has significantly broadened the consumer base across both developed and emerging economies.

Key Market Insights

- Standard whey-based muscle gainers dominate the market, accounting for nearly 46% of the 2025 global revenue share due to affordability and broad consumer adoption.

- Recreational fitness consumers represent the largest end-user segment, contributing approximately 52% of total demand in 2025.

- North America leads the global market, holding around 34% share in 2025, supported by high supplement penetration and strong sports culture.

- Asia-Pacific is the fastest-growing region, projected to expand at over 9% CAGR, led by China and India.

- Offline specialty retail remains dominant, accounting for approximately 54% of 2025 sales, although online channels are expanding rapidly.

- Premium isolate and hydrolyzed whey formulations are gaining traction due to clean-label and high-absorption preferences.

What are the latest trends in the whey protein muscle gainer market?

Premiumization and Clean-Label Formulations

Consumers are increasingly shifting toward premium whey isolate and hydrolyzed formulations that offer higher protein concentration, lower lactose content, and minimal added sugars. Clean-label products free from artificial sweeteners and fillers are gaining prominence, particularly in North America and Europe. Manufacturers are investing in microfiltration and enzymatic hydrolysis technologies to improve bioavailability and taste profiles. Functional fortification with digestive enzymes, creatine monohydrate, BCAAs, and micronutrients is becoming mainstream, allowing brands to command higher price points and margins in competitive markets.

Digital-First Distribution and Subscription Models

E-commerce platforms and direct-to-consumer channels are reshaping distribution dynamics. Brands are increasingly adopting subscription-based delivery models, offering personalized dosage plans integrated with fitness tracking apps. Online platforms provide competitive pricing transparency and influencer-driven marketing, accelerating adoption among younger consumers. Social media engagement and athlete endorsements are playing a critical role in brand differentiation, particularly in emerging markets where digital penetration is rapidly expanding.

What are the key drivers in the whey protein muscle gainer market?

Expanding Global Fitness Industry

The rapid expansion of gyms, health clubs, and organized sports programs is a primary driver of whey protein muscle gainer demand. The global fitness industry is growing at over 8% annually, directly influencing protein supplement consumption. Increased participation in strength training, bodybuilding, and athletic conditioning is reinforcing sustained product demand across age groups.

Rising Disposable Income in Emerging Markets

Urbanization and growing middle-class incomes in countries such as China, India, Brazil, and Indonesia are expanding the consumer base for sports nutrition products. Consumers are increasingly allocating discretionary spending toward health and wellness, including premium protein supplementation. Localization of flavors and affordable packaging formats are enabling broader penetration in Tier-2 and Tier-3 cities.

What are the restraints for the global market?

Raw Material Price Volatility

Whey protein is derived from dairy processing, making the market sensitive to fluctuations in milk production, feed costs, and global dairy trade policies. Volatility in whey concentrate and isolate prices directly impacts manufacturing costs and retail pricing strategies, creating margin pressures for brands operating in price-sensitive markets.

Regulatory and Labeling Compliance

Stringent regulatory requirements regarding health claims, protein content verification, and labeling standards in North America and Europe increase compliance costs. Variations in supplement regulations across countries also complicate cross-border trade, particularly for exporters targeting multiple regions.

What are the key opportunities in the whey protein muscle gainer industry?

Emerging Market Penetration

Rapidly expanding fitness infrastructure in Asia-Pacific and Latin America presents strong growth opportunities. Government-backed sports initiatives and increasing youth participation in athletics are accelerating demand. Companies that optimize price points and introduce region-specific formulations can significantly expand market share in these high-growth economies.

Institutional and Sports Academy Procurement

Bulk supply contracts with sports academies, universities, and professional training centers offer stable, high-volume revenue streams. As governments increase investments in grassroots sports development, institutional procurement of protein supplements is expected to rise, particularly in North America, Europe, and China.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14700 Million |

| Market Size in 2026 | USD 15831.90 Million |

| Market Size in 2031 | USD 22940.96 Million |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard whey protein muscle gainers dominate the global market, accounting for approximately 46% of total revenue share in 2025. The leadership of this segment is primarily driven by its affordability, balanced macronutrient composition, and suitability for beginner and intermediate fitness consumers seeking steady muscle mass development. These formulations typically combine whey protein concentrate with optimized carbohydrate blends to support caloric surplus and post-workout recovery, making them widely accessible across retail channels. The segment benefits from strong brand visibility, mass-market pricing strategies, and high repeat purchase rates among gym-goers focused on progressive weight gain.

Premium whey isolate-based muscle gainers represent one of the fastest-growing segments, supported by increasing demand for higher protein purity, reduced lactose content, and lower fat formulations. Consumers with advanced fitness goals and those with mild lactose intolerance are increasingly opting for isolate-based products due to their superior digestibility and cleaner nutritional profile. Hydrolyzed whey-based products, known for rapid absorption and enhanced bioavailability, cater primarily to professional athletes and competitive bodybuilders seeking faster muscle recovery and reduced post-exercise muscle breakdown. Meanwhile, advanced blended formulations fortified with creatine, branched-chain amino acids (BCAAs), digestive enzymes, and essential micronutrients are gaining traction in premium retail and specialty nutrition channels, driven by the growing preference for all-in-one performance supplements.

Distribution Channel Insights

Offline retail channels account for nearly 54% of global sales in 2025, maintaining leadership due to strong consumer trust and personalized buying experiences. Specialty nutrition stores, gym-based retail counters, supermarkets, and pharmacy chains play a critical role in influencing purchasing decisions through expert recommendations, product sampling, and immediate product availability. The dominance of offline channels is further supported by impulse purchases and strong brand merchandising strategies within organized retail environments.

Online retail, however, represents the fastest-growing distribution channel, fueled by expanding e-commerce penetration, competitive pricing, subscription-based replenishment models, and influencer-driven digital marketing campaigns. Consumers increasingly prefer online platforms for product comparison, access to customer reviews, and broader product variety. Direct-to-consumer (DTC) websites are enhancing brand profitability by minimizing intermediary margins and enabling personalized product bundles, targeted promotions, and loyalty programs. The integration of digital payment infrastructure and improved last-mile delivery services is further accelerating online channel expansion globally.

End-User Insights

Recreational fitness consumers constitute the largest end-user segment, contributing approximately 52% of global demand in 2025. The segment’s leadership is driven by the rapid expansion of commercial gyms, growing participation in strength training programs, and increasing social media influence promoting muscle-building aesthetics. These consumers primarily seek cost-effective, easy-to-consume formulations that support consistent muscle gain and workout recovery.

Bodybuilders and professional athletes represent a significant share of premium and specialized formulations, driven by performance optimization requirements, structured training regimens, and higher supplement spending capacity. Sports institutions, fitness academies, and rehabilitation centers are emerging as important demand generators, particularly for structured nutrition programs supporting athletic development and injury recovery. Additionally, clinical nutrition applications are gradually expanding, particularly for muscle preservation therapy, post-surgical recovery, and elderly weight management programs in hospital and long-term care settings, reflecting the widening functional scope of whey-based muscle gainers.

Explore more data points, trends and opportunities Download Free Sample Report

Whey Protein Muscle Gainer Market Segmentations

By Product Type

- Standard Whey Protein Muscle Gainers

- Whey Isolate-Based Muscle Gainers

- Hydrolyzed Whey Protein Muscle Gainers

- Advanced Blended & Fortified Mass Gainers

By Distribution Channel

- Offline Retail

- Online Retail

- Direct-to-Consumer

By Packaging Format

- Bulk Packs

- Standard Packs

- Single-Serve Sachets & Ready-to-Mix Pouches

By End-User

- Bodybuilders & Professional Athletes

- Recreational Fitness Consumers

- Sports Teams & Institutional Buyers

- Clinical & Nutritional Rehabilitation Users

Regional Insights

North America

North America leads the global whey protein muscle gainer market, holding approximately 34% of total market share in 2025. The United States accounts for nearly 78% of regional demand, supported by high dietary supplement penetration, strong consumer awareness regarding protein intake, and well-established sports nutrition brands. Growth in the region is driven by a mature fitness culture, widespread gym memberships, collegiate sports programs, and high disposable income levels. The presence of advanced manufacturing infrastructure, stringent quality standards, and aggressive marketing by established players further strengthens market expansion. Canada contributes steady growth due to rising health consciousness and increasing adoption of strength training among younger demographics.

Europe

Europe holds approximately 27% of global market share in 2025, led by Germany, the United Kingdom, and France. Germany contributes nearly 22% of regional demand, driven by strong sports nutrition awareness, organized fitness communities, and increasing participation in amateur bodybuilding competitions. Regional growth is supported by expanding e-commerce channels, clean-label product innovation, and regulatory frameworks that encourage high-quality supplement manufacturing. Rising demand for premium, lactose-reduced, and fortified formulations is further accelerating adoption across Western Europe, while Eastern Europe presents emerging growth opportunities due to improving disposable incomes and expanding gym infrastructure.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at a CAGR exceeding 9% through 2031. China accounts for nearly 30% of regional demand, supported by rapid urbanization, increasing disposable income, and expanding domestic supplement manufacturing. The proliferation of fitness centers and digital health influencers is significantly shaping consumer purchasing behavior. India is emerging as one of the fastest-growing national markets, driven by the rapid expansion of organized gym chains, growing youth population, and rising awareness regarding protein deficiency and muscle-building nutrition. Additionally, Southeast Asian markets are witnessing increased product availability through cross-border e-commerce and regional brand expansions, strengthening overall market growth.

Latin America

Latin America represents approximately 6–7% of global demand, led by Brazil and Mexico. Regional growth is driven by increasing urban fitness participation, expanding middle-class income levels, and growing influence of bodybuilding culture. Brazil remains the largest contributor due to strong sports culture and rising gym memberships. Improving retail penetration and increasing availability of affordable whey-based products are supporting gradual adoption, while local manufacturing capabilities are helping stabilize pricing structures.

Middle East & Africa

The Middle East & Africa accounts for roughly 5–6% of global market share, with the UAE and Saudi Arabia serving as primary demand centers. Growth in the region is supported by expanding sports infrastructure, rising health awareness, and increasing government initiatives promoting active lifestyles. Premium supplement demand is particularly strong in the Gulf Cooperation Council (GCC) countries due to higher disposable income and strong brand affinity for imported nutrition products. In Africa, improving urbanization rates and gradual expansion of modern retail formats are expected to contribute to long-term market development.

Key Players in the Whey Protein Muscle Gainer Market

- Glanbia plc

- Optimum Nutrition

- MuscleTech

- Abbott Laboratories

- Herbalife Nutrition

- Dymatize

- BSN

- Myprotein

- Universal Nutrition

- GNC Holdings

- Nutrabolt

- BPI Sports

- Rule One Proteins

- Labrada Nutrition

- Ultimate Nutrition