Wheat Flour Market Size

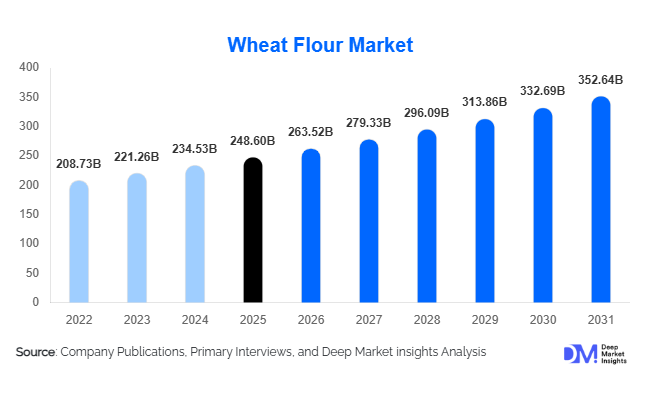

According to Deep Market Insights, the global wheat flour market size was valued at USD 234.8 billion in 2025 and is projected to grow from USD 263.52 billion in 2026 to reach USD 352.64 billion by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The wheat flour market growth is primarily driven by rising global consumption of bakery products, increasing demand for processed and convenience foods, expanding foodservice industries, and the growing adoption of fortified flour across emerging economies.

Wheat flour remains one of the most widely consumed food ingredients globally due to its affordability, versatility, nutritional profile, and compatibility with industrial food processing systems. The market is witnessing significant demand from bakery manufacturers, instant noodle producers, quick-service restaurants, and packaged food companies. Rapid urbanization and changing dietary patterns are accelerating consumption of bread, pizza, noodles, frozen bakery products, and ready-to-cook foods, particularly across Asia-Pacific, the Middle East, and Africa.

The market is also benefiting from advancements in flour milling technologies, including automated roller milling, precision blending, AI-enabled grain quality analysis, and energy-efficient processing systems. Governments across developing economies are increasingly supporting flour fortification initiatives to address micronutrient deficiencies, creating additional growth opportunities for industrial flour producers. Rising demand for organic, whole wheat, and specialty flour products in North America and Europe is further contributing to premiumization within the global wheat flour market.

Key Market Insights

- Refined wheat flour continues to dominate global consumption, supported by large-scale demand from bakery, noodle, and processed food industries.

- Asia-Pacific accounts for the largest regional share, driven by rising packaged food consumption, urbanization, and strong noodle manufacturing industries in China and India.

- Fortified wheat flour adoption is increasing rapidly, supported by government nutrition and food security initiatives across emerging economies.

- Specialty and organic flour categories are witnessing strong growth, particularly in North America and Europe due to rising consumer preference for clean-label and health-focused products.

- Industrial bakery and quick-service restaurant expansion is significantly increasing procurement volumes of standardized commercial flour globally.

- Automation and smart milling technologies, including AI-driven grain monitoring and precision milling systems, are improving operational efficiency and flour consistency.

Wheat Flour Market Trends

Rising Demand for Fortified and Functional Flour

The wheat flour market is increasingly shifting toward fortified and value-added flour products as governments and consumers prioritize nutritional improvement. Flour enriched with iron, folic acid, zinc, vitamins, and protein is gaining widespread adoption across both retail and institutional markets. Countries such as India, Indonesia, Nigeria, and South Africa are implementing mandatory fortification regulations to combat micronutrient deficiencies, significantly increasing industrial demand for fortified flour. Food manufacturers are also launching functional flour variants targeted toward health-conscious consumers seeking higher protein, digestive wellness, and enhanced nutritional benefits. This trend is creating opportunities for flour millers to diversify product portfolios and achieve higher margins through specialty flour offerings.

Growth of Premium and Artisanal Flour Categories

Premium flour products, including organic flour, stone-ground flour, sprouted wheat flour, and high-protein baking flour, are witnessing rising demand globally. Consumers in North America and Europe increasingly prefer minimally processed and clean-label bakery ingredients, driving strong growth in specialty flour segments. Artisan bakeries and premium foodservice operators are introducing differentiated bread and bakery products using customized flour blends, supporting premiumization within the market. E-commerce platforms are further accelerating retail penetration of premium flour brands by enabling direct-to-consumer sales and targeted digital marketing campaigns focused on health and sustainability.

Wheat Flour Market Drivers

Expansion of Global Bakery and Processed Food Industries

The continuous expansion of bakery and processed food manufacturing remains one of the strongest growth drivers for the wheat flour market. Bread, cakes, pastries, biscuits, pizza bases, frozen bakery products, and instant noodles are experiencing rising global consumption due to urbanization and changing dietary habits. Industrial food manufacturers require standardized flour quality and large-scale procurement volumes, creating stable long-term demand for commercial flour suppliers. Emerging economies across Asia-Pacific, Latin America, and Africa are witnessing especially strong growth in packaged food consumption due to increasing disposable incomes and expanding retail infrastructure.

Growth in Quick-Service Restaurants and Convenience Foods

The rapid expansion of quick-service restaurants and convenience food industries is significantly increasing demand for industrial wheat flour. Global fast-food chains continue to expand aggressively across India, Southeast Asia, the Middle East, and Africa, driving consumption of burger buns, wraps, pizza crusts, tortillas, and coating applications. Consumers are increasingly favoring ready-to-eat and ready-to-cook food products due to busy lifestyles and rising workforce participation, supporting higher flour consumption within industrial food manufacturing. Frozen food production and packaged snack manufacturing are also contributing substantially to flour demand growth.

Wheat Flour Market Restraints

Volatility in Wheat Prices and Agricultural Supply

The wheat flour market remains highly vulnerable to fluctuations in global wheat prices caused by adverse weather conditions, geopolitical tensions, export restrictions, fertilizer cost inflation, and supply chain disruptions. Climate-related production risks, including droughts and floods in major wheat-producing regions, can significantly impact raw material availability and profitability for flour millers. Sudden spikes in wheat prices often compress operating margins for manufacturers and increase pricing pressure across downstream food industries.

Increasing Preference for Alternative and Gluten-Free Diets

The growing popularity of gluten-free and low-carbohydrate diets in developed economies presents a challenge for traditional wheat flour consumption. Consumers increasingly seeking alternative grains such as oats, rice, almond, millet, and chickpea flour are contributing to gradual diversification away from conventional wheat-based products. Rising awareness regarding gluten intolerance and celiac disease is also encouraging some consumers to reduce wheat intake, particularly in premium urban markets across North America and Europe.

Wheat Flour Market Opportunities

Export-Oriented Flour Production Expansion

Export-oriented flour manufacturing presents a major opportunity for global wheat flour producers. Countries such as Türkiye, Kazakhstan, Russia, Canada, and Australia are increasingly investing in value-added flour processing infrastructure to strengthen exports of processed wheat products rather than only exporting raw grain. Rising flour demand from Africa, the Middle East, and Southeast Asia is encouraging commercial millers to expand production capacities and develop international supply agreements. Export-focused milling operations are benefiting from improved profitability, long-term trade contracts, and higher industrial utilization rates.

Growth of Smart Milling and Automation Technologies

Technological modernization within flour milling operations is creating substantial operational and profitability opportunities. Automated roller mills, AI-based grain inspection systems, predictive maintenance technologies, and precision blending systems are helping companies improve flour consistency, reduce wastage, and optimize extraction efficiency. Smart milling technologies also support energy savings and improved quality control, enabling manufacturers to meet stringent food safety and export standards. Companies investing in automation are expected to strengthen competitiveness while improving long-term operating margins.

Product Type Insights

Refined wheat flour dominates the global market, accounting for the largest share of industrial and retail consumption due to its widespread use in bakery products, noodles, processed foods, and foodservice applications. All-purpose flour and bread flour remain the most commercially significant categories because of their versatility and large-scale utilization in commercial baking operations. Whole wheat flour is witnessing strong growth due to rising consumer awareness regarding dietary fiber and healthier eating habits. Specialty flour categories, including organic flour, stone-ground flour, and protein-enriched flour, are gaining popularity among premium bakery manufacturers and health-conscious consumers. Fortified flour is also emerging as a rapidly expanding category as governments and food manufacturers increasingly prioritize nutritional enhancement and food security programs globally.

Application Insights

Bakery products remain the largest application segment within the wheat flour market, supported by rising global demand for bread, cakes, pastries, biscuits, pizza bases, and frozen bakery products. Industrial bakery manufacturers continue expanding production capacities to meet increasing urban food consumption. Noodles and pasta applications also represent a significant share of flour utilization, particularly across Asia-Pacific where instant noodle consumption continues to rise rapidly. Processed food applications, including snacks, ready-to-eat meals, and frozen foods, are witnessing accelerated growth due to increasing consumer preference for convenience foods. Wheat flour is additionally used in batter and coating systems, sauces, thickening applications, and foodservice operations, further diversifying market demand across multiple industries.

Distribution Channel Insights

Direct business-to-business sales dominate the wheat flour market as commercial millers primarily supply industrial bakeries, food manufacturers, quick-service restaurant chains, and institutional buyers through long-term procurement contracts. Wholesale distribution channels remain highly important across emerging economies where traditional retail and foodservice networks continue to expand. Modern trade and supermarket channels are increasing retail flour sales globally due to growing packaged food consumption and urban retail penetration. Online grocery platforms and e-commerce channels are witnessing rapid growth, particularly for premium and specialty flour products targeted toward health-conscious consumers. Manufacturers are increasingly leveraging digital marketing and direct-to-consumer strategies to strengthen brand visibility within retail segments.

End-Use Industry Insights

The bakery and confectionery industry represents the largest end-use segment for wheat flour globally due to the continuous expansion of bread, pastry, biscuit, and cake manufacturing. Food processing industries also account for substantial demand, particularly within instant noodles, frozen foods, snacks, and packaged convenience meals. Quick-service restaurants are among the fastest-growing end-use industries as global fast-food chains continue expanding across developing economies. Household retail consumption remains significant, especially in Asia-Pacific, the Middle East, and Africa where home cooking continues to contribute heavily to flour demand. Institutional buyers, including schools, public welfare programs, and government food distribution systems, are increasingly procuring fortified flour products under national nutrition initiatives.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry | By Nature |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for a significant share of the global wheat flour market, led by the United States and Canada. The region benefits from highly developed bakery and processed food industries, strong commercial wheat production, and advanced flour milling infrastructure. The United States remains one of the world’s largest producers and exporters of high-protein wheat flour used in industrial baking applications. Demand for specialty flour, organic flour, and fortified flour is increasing steadily due to rising health consciousness among consumers. Frozen bakery products, snack manufacturing, and foodservice applications continue driving commercial flour procurement across the region.

Europe

Europe represents a mature yet highly premiumized wheat flour market, driven by strong demand for artisanal bakery products and clean-label food ingredients. Germany, France, Italy, Türkiye, and the United Kingdom are major flour-consuming countries within the region. Organic flour, stone-ground flour, and specialty baking blends are witnessing substantial demand growth due to increasing consumer preference for minimally processed foods. Türkiye has also emerged as a major flour-exporting nation supplying Middle Eastern and African markets, strengthening Europe’s position within global flour trade.

Asia-Pacific

Asia-Pacific dominates the global wheat flour market with the largest regional share, supported by high population density, rapid urbanization, and strong demand for noodles, bakery products, and processed foods. China and India are the largest consumers due to expanding food manufacturing industries and rising packaged food consumption. Indonesia, Vietnam, Japan, and Thailand also contribute significantly through strong noodle and convenience food industries. India remains one of the fastest-growing markets due to increasing quick-service restaurant penetration, rising disposable income, and government-supported flour fortification programs. Expanding middle-class populations and changing dietary preferences continue accelerating flour demand across the region.

Latin America

Latin America is witnessing steady growth in wheat flour consumption, led by Brazil, Mexico, and Argentina. Bakery products, tortillas, processed foods, and snack manufacturing remain the primary demand drivers within the region. Mexico’s large tortilla and flatbread industry contributes significantly to industrial flour utilization, while Brazil is experiencing increasing demand for packaged bakery products and convenience foods. Urbanization and retail modernization are further supporting commercial flour consumption across major Latin American economies.

Middle East & Africa

The Middle East & Africa region is emerging as one of the fastest-growing wheat flour markets globally due to rising bread consumption, population growth, and increasing dependence on imported wheat products. Egypt remains one of the world’s largest wheat importers and flour consumers, supported by extensive government bread subsidy programs. Saudi Arabia, UAE, Nigeria, and South Africa are also experiencing rising flour demand due to expanding bakery industries and processed food manufacturing. Increasing investments in flour milling infrastructure and food security initiatives are expected to strengthen long-term regional growth prospects.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Wheat Flour Market

- Archer Daniels Midland Company

- Cargill Incorporated

- Ardent Mills

- Conagra Brands

- General Mills

- Associated British Foods

- Wilmar International

- GrainCorp Limited

- King Arthur Baking Company

- Mitsubishi Corporation

- Nisshin Seifun Group

- GoodMills Group

- Bay State Milling Company

- George Weston Limited

- Allied Pinnacle