Wet Pet Food Market Size

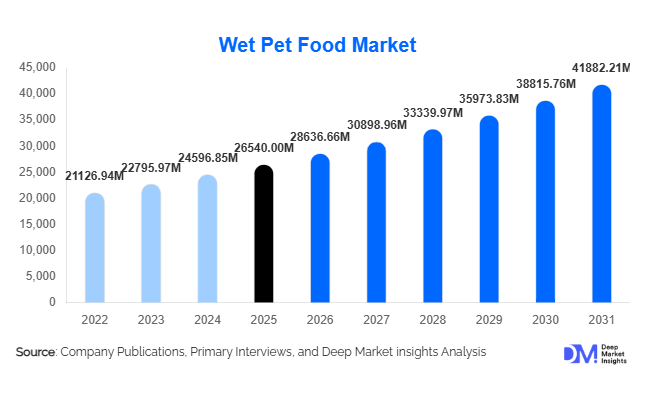

According to Deep Market Insights, the global wet pet food market size was valued at USD 26,540 million in 2025 and is projected to grow from USD 28,636.66 million in 2026 to reach USD 41,882.21 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The wet pet food market growth is primarily driven by increasing pet humanization trends, rising demand for premium and functional pet nutrition, and growing awareness regarding hydration and digestive health benefits associated with wet food diets. Expanding urban pet ownership, rapid e-commerce penetration, and veterinary recommendations supporting wet food feeding are further strengthening global demand.

Key Market Insights

- Premiumization is reshaping purchasing behavior, with consumers increasingly opting for high-protein and functional wet pet food formulations.

- Cat wet food adoption is accelerating globally due to veterinary recommendations emphasizing hydration and urinary health benefits.

- North America dominates the global market, supported by high pet ownership rates and strong premium product penetration.

- Asia-Pacific is the fastest-growing region, driven by rising disposable income and rapid urban pet adoption in China and India.

- E-commerce and subscription feeding models are transforming distribution dynamics and improving customer retention.

- Sustainable packaging and alternative proteins are emerging as major innovation areas across leading manufacturers.

What are the latest trends in the wet pet food market?

Premium and Functional Nutrition Expansion

The wet pet food industry is witnessing strong momentum toward premium and functional nutrition solutions. Pet owners increasingly seek products addressing specific health outcomes such as digestive health, immunity enhancement, weight control, and joint care. Functional wet meals enable better nutrient absorption due to higher moisture content, positioning them as superior alternatives to traditional dry kibble. Manufacturers are introducing veterinary-backed formulations, grain-free recipes, and clean-label ingredient declarations to align with consumer expectations. Limited-ingredient diets and natural protein sources are also gaining traction among health-conscious pet owners seeking transparency and quality assurance.

Rise of Sustainable Packaging and Alternative Proteins

Sustainability considerations are influencing purchasing decisions across developed markets. Companies are investing in recyclable pouches, lightweight trays, and reduced-carbon packaging formats to lower environmental impact. Alternative protein innovation, including insect-based and novel meat sources such as duck and venison, is emerging as a strategic response to volatile meat prices and environmental concerns. These innovations help brands maintain supply stability while appealing to environmentally conscious consumers. Sustainability certifications and ethical sourcing claims increasingly act as brand differentiators in competitive retail environments.

What are the key drivers in the wet pet food market?

Growing Pet Humanization and Premium Spending

Pets are increasingly viewed as family members, encouraging owners to invest in higher-quality nutrition comparable to human food standards. This behavioral shift has significantly increased demand for premium wet food products offering superior taste, texture, and nutritional value. Higher disposable income levels and emotional attachment to pets continue to drive willingness to pay for specialized diets and premium formulations.

Veterinary Recommendations and Health Awareness

Veterinary professionals increasingly recommend wet food diets, particularly for cats and aging pets requiring improved hydration and digestive support. Rising awareness of chronic pet health conditions such as obesity, kidney disease, and allergies has strengthened adoption of therapeutic wet food products. Growth in global pet healthcare spending directly supports expansion of medically formulated wet diets.

What are the restraints for the global market?

High Production and Packaging Costs

Wet pet food manufacturing involves sterilization processes, moisture preservation, and specialized packaging technologies, resulting in higher production costs compared with dry pet food. Metal can prices, energy-intensive processing, and logistics expenses place pressure on manufacturer margins, particularly in emerging markets.

Raw Material Price Volatility

The industry’s dependence on animal-based proteins exposes manufacturers to fluctuations in meat and seafood prices. Supply disruptions and agricultural inflation can increase input costs, forcing pricing adjustments that may limit adoption among price-sensitive consumers.

What are the key opportunities in the wet pet food industry?

Emerging Market Expansion

Rapid urbanization and rising middle-class populations across Asia-Pacific and Latin America present significant opportunities for market expansion. Countries such as China, India, and Brazil are transitioning from homemade feeding toward commercial pet food consumption. Localization strategies, affordable premium offerings, and smaller packaging sizes enable manufacturers to penetrate these high-growth markets effectively.

Direct-to-Consumer and Subscription Models

Digital commerce platforms are creating new growth avenues through subscription-based feeding services and personalized nutrition recommendations. Direct-to-consumer models allow brands to bypass traditional retail margins, strengthen customer relationships, and accelerate innovation cycles. AI-driven feeding recommendations and customized meal plans are expected to further enhance long-term customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26540 Million |

| Market Size in 2026 | USD 28636.66 Million |

| Market Size in 2031 | USD 41882.21 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Pet Type Insights

The global wet pet food market is predominantly led by dog wet food, which accounts for nearly 58% of total market demand. The segment’s leadership is primarily driven by higher food consumption volumes among dogs compared with other companion animals, alongside increasing humanization trends that encourage owners to invest in nutritionally balanced and premium-quality meals. Dog owners are increasingly shifting toward wet formulations due to enhanced palatability, improved digestibility, and perceived health benefits such as better hydration and nutrient absorption. Additionally, the growing adoption of mixed feeding practices, where wet food is combined with dry kibble to enhance taste and nutritional diversity, continues to strengthen demand across developed and emerging economies.Cat wet food represents the fastest-growing pet type segment, supported by strong veterinary recommendations emphasizing moisture-rich diets for feline health management. Wet food helps address hydration deficiencies common among cats and supports urinary tract health, kidney function, and weight management, making it increasingly preferred among health-conscious pet owners. Rising indoor cat populations, particularly in urban environments, further contribute to sustained demand growth as owners prioritize premium and functional nutrition solutions.Wet food products formulated for other companion animals, including small mammals and specialty pets, remain comparatively niche but are gradually expanding as manufacturers introduce species-specific nutrition offerings. Increasing consumer awareness regarding tailored dietary requirements and the availability of specialized premium formulations are expected to support steady growth in this segment over the forecast period.

Product Format Insights

Chunks in gravy represent the leading product format, accounting for approximately 27% of global market revenue. The segment’s dominance is largely attributed to consumer perception that chunk-based meals closely resemble natural, home-prepared food, thereby enhancing pet acceptance and feeding satisfaction. The visible texture and sauce content improve palatability while also supporting hydration, making this format highly appealing to both dogs and cats. Continuous innovation in flavor combinations and protein inclusions further reinforces the segment’s leadership.Pâté-style wet pet food continues to maintain strong global adoption due to its affordability, smooth texture, and extended shelf stability. This format is particularly popular among multi-pet households and value-oriented consumers seeking nutritionally complete meals at competitive price points. Its ease of portioning and suitability for pets with dental sensitivities or aging-related chewing challenges also contribute to sustained consumption.Shredded, flaked, and broth-based formulations are gaining traction within premium and super-premium product categories. These gourmet-style offerings appeal to consumers seeking differentiated feeding experiences and higher-quality ingredient presentation. Premiumization trends, combined with rising disposable incomes and evolving pet care standards, are encouraging manufacturers to expand innovative textures and culinary-inspired recipes within this category.

Ingredient Source Insights

Animal-based protein formulations dominate the ingredient landscape, accounting for nearly 72% of total market share. This leadership is primarily driven by consumer preference for diets aligned with the biological and carnivorous nutritional requirements of dogs and cats. Meat-rich recipes containing chicken, beef, fish, and lamb are widely perceived as nutritionally superior, delivering essential amino acids, improved digestibility, and enhanced taste profiles that encourage consistent feeding behavior.The leading segment is further supported by growing demand for high-protein functional diets designed to support muscle maintenance, immune health, and overall vitality, particularly among aging pets. Premium product positioning emphasizing real meat ingredients, grain-free formulations, and clean-label claims continues to reinforce consumer trust and brand differentiation.Novel protein sources such as duck, rabbit, venison, and insect-based ingredients are emerging as rapidly expanding niche segments. These alternatives are increasingly adopted for pets with food sensitivities and allergies while also addressing sustainability concerns associated with conventional livestock production. Europe and North America remain key markets for innovation in alternative proteins, supported by environmentally conscious consumers and regulatory encouragement for sustainable sourcing.

Packaging Insights

Canned wet pet food remains the dominant packaging format, holding approximately 46% of global market share. The segment’s leadership is supported by its durability, strong product preservation capabilities, and long shelf life, which ensure food safety and maintain nutritional integrity. Established consumer familiarity and trust in metal can packaging further strengthen adoption across both developed and emerging markets.However, flexible packaging formats such as pouches and trays are experiencing faster growth as manufacturers respond to changing consumer lifestyles. These packaging solutions offer improved convenience through easy storage, single-serve portioning, and reduced food waste. Urban consumers increasingly prefer lightweight and portable packaging compatible with smaller living spaces and on-the-go lifestyles.Additionally, sustainability considerations are reshaping packaging innovation, with companies investing in recyclable materials, reduced plastic usage, and environmentally optimized designs. The rapid growth of e-commerce distribution channels also favors flexible packaging formats due to lower transportation costs and improved logistics efficiency.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate global wet pet food sales, accounting for approximately 39% of total distribution. Their leadership is driven by extensive product availability, strong brand visibility, and the ability to offer competitive pricing through promotional strategies. Consumers often prefer physical retail environments for pet food purchases due to immediate product access and the opportunity to compare brands directly.The leading distribution channel benefits from established supply chains and strategic partnerships between manufacturers and large retail networks, ensuring consistent product availability across regions. In-store merchandising and impulse purchasing behavior further contribute to sustained sales performance.Online retail represents the fastest-growing distribution channel, fueled by digital transformation and evolving consumer purchasing habits. Subscription-based delivery services, automated replenishment programs, and personalized product recommendations enhance customer convenience and brand loyalty. Increasing smartphone penetration, expanding logistics infrastructure, and growing consumer confidence in online purchasing are expected to significantly accelerate channel expansion worldwide.

End-Use Insights

Household pet ownership constitutes the primary end-use segment within the global wet pet food market. Rising pet humanization trends and increasing emotional attachment between owners and pets are driving consistent demand for high-quality nutrition products. Urbanization and the growth of nuclear families have further contributed to increased pet adoption, resulting in recurring purchasing patterns and long-term consumption stability.The leading household segment is supported by growing awareness of balanced diets, life-stage-specific nutrition, and preventive healthcare feeding practices. Multi-pet households in metropolitan areas are particularly influential in driving volume growth, as owners increasingly diversify feeding routines with premium wet food products.Veterinary nutrition applications are expanding rapidly as therapeutic wet diets gain wider acceptance for disease management, post-surgery recovery, and chronic condition support. Moisture-rich formulations are commonly recommended for digestive disorders, renal health, and appetite stimulation. Additionally, export-oriented manufacturing hubs such as Thailand and the United States play a critical role in supplying premium wet pet food products globally, strengthening international trade flows.The growing aging pet population worldwide is expected to generate sustained long-term demand for specialized medical nutrition solutions, reinforcing the importance of wet food formulations within advanced pet healthcare strategies.

Explore more data points, trends and opportunities Download Free Sample Report

Wet Pet Food Market Segmentations

By Pet Type

- Dog Wet Food

- Cat Wet Food

- Other Companion Animals

By Product Format

- P/Loaf

- Chunks in Gravy

- Shredded/Flaked

- Stews Broth-Based Meals

- Freeze-Processed Wet Meals

By Ingredient Source

- Chicken-Based

- Beef-Based

- Fish Seafood-Based

- Lamb Specialty Meat

- Novel Alternative Proteins

By Packaging Type

- Cans

- Pouches

- Trays Tubs

- Multipack Containers

By Distribution Channel

- Supermarkets Hypermarkets

- Pet Specialty Stores

- Veterinary Clinics

- Online Retail Subscription Platforms

- Convenience Stores

Regional Insights

North America

North America accounted for approximately 38% of the global wet pet food market in 2025, with the United States representing the largest contributor to regional revenue. Market growth is strongly supported by high disposable income levels, widespread pet humanization, and advanced veterinary healthcare infrastructure that promotes nutritionally optimized feeding practices. Consumers in the region demonstrate strong willingness to spend on premium and functional pet nutrition products, including grain-free, organic, and therapeutic wet food formulations.Regional expansion is further driven by the rapid adoption of subscription-based purchasing models, high penetration of e-commerce platforms, and strong innovation pipelines from established pet food manufacturers. Increasing demand for clean-label ingredients, sustainability-focused packaging, and customized nutrition solutions continues to shape purchasing behavior, supporting long-term market maturity and premiumization trends.

Europe

Europe held nearly 29% of global market share, led by Germany, the United Kingdom, and France. The region benefits from well-established pet ownership culture and strong regulatory frameworks governing ingredient safety and transparency. Strict labeling requirements and quality standards enhance consumer confidence and encourage adoption of premium wet pet food products.Regional growth is driven by sustainability-oriented consumption patterns, with European consumers prioritizing ethically sourced proteins, environmentally responsible packaging, and reduced carbon footprints. Increasing demand for natural and organic formulations, combined with rising awareness of animal welfare and nutrition science, continues to accelerate innovation across the market. Aging pet populations across Western Europe also support demand for specialized therapeutic and senior nutrition products.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 9.5%. Rapid urbanization, rising disposable incomes, and shifting lifestyle patterns are driving significant increases in pet ownership across major economies. China leads regional growth due to expanding middle-class populations and growing awareness of premium pet care practices, while Japan’s aging pet demographic supports strong adoption of medical and functional wet diets.India and Southeast Asian countries are emerging as high-potential markets, supported by increasing exposure to commercial pet nutrition through digital media and retail expansion. Growth is further accelerated by rising nuclear households, higher female workforce participation, and growing acceptance of pets as family members. Expanding modern retail infrastructure and cross-border e-commerce platforms are improving accessibility to international premium brands across the region.

Latin America

Latin America is experiencing steady market expansion, with Brazil dominating regional consumption due to its large pet population and improving economic conditions. Rising urbanization and increasing awareness of balanced pet nutrition are encouraging consumers to transition from homemade feeding practices toward commercially prepared wet food products.Regional growth is further supported by expanding middle-income populations, improved retail distribution networks, and increased investment by global pet food manufacturers. Mexico and Argentina are witnessing accelerating adoption of premium brands as modern retail channels and e-commerce penetration continue to expand, enhancing product availability and consumer education.

Middle East & Africa

The Middle East & Africa wet pet food market is growing steadily, led by the United Arab Emirates and South Africa. Rising expatriate populations and westernized lifestyle adoption are contributing to increased pet ownership and higher spending on premium pet care products. Expansion of organized retail formats and specialty pet stores is improving product accessibility across urban centers.Regional demand is further driven by growing awareness of packaged pet nutrition, increasing disposable incomes in key metropolitan areas, and expanding veterinary services promoting balanced feeding practices. The gradual development of cold-chain logistics and import distribution networks is also enabling broader availability of international wet pet food brands, supporting sustained market growth across the region.

Key Players in the Wet Pet Food Market

- Mars Incorporated

- Nestlé S.A. (Purina)

- Colgate-Palmolive Company (Hill’s Pet Nutrition)

- General Mills Inc. (Blue Buffalo)

- J.M. Smucker Company

- Spectrum Brands Holdings

- Diamond Pet Foods

- WellPet LLC

- Unicharm Corporation

- Thai Union Group

- Heristo AG

- Simmons Pet Food

- Affinity Petcare S.A.

- Nisshin Pet Food Inc.

- Farmina Pet Foods