Western Fast Food Market Size

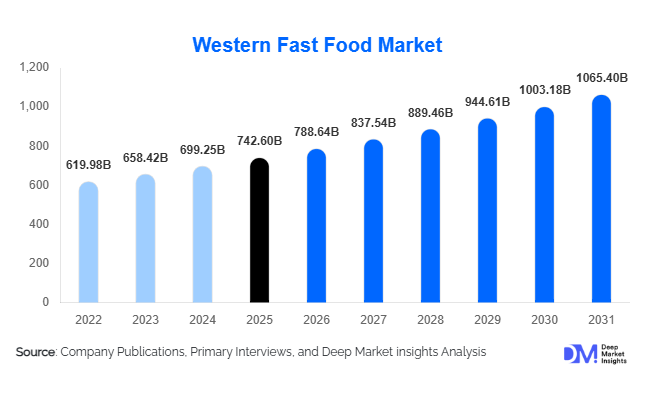

According to Deep Market Insights, the global western fast food market size was valued at USD 742.6 billion in 2025 and is projected to grow from USD 788.64 billion in 2026 to reach USD 1,065.4 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). Growth in the western fast food market is driven by increasing urbanization, rising dual-income households, evolving consumer lifestyles favoring convenience foods, and rapid expansion of international quick-service restaurant (QSR) chains into emerging economies. Digital ordering ecosystems, delivery integration, and menu localization strategies have further accelerated adoption across both developed and developing regions.

Key Market Insights

- Quick-service restaurants (QSRs) dominate global consumption, supported by standardized menus, rapid service formats, and scalable franchise models.

- Digital ordering and delivery platforms are reshaping revenue channels, with mobile ordering accounting for a growing portion of transactions worldwide.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and strong Western brand penetration.

- Health-oriented menu innovation, including plant-based burgers and low-calorie offerings, is expanding customer demographics.

- Drive-thru and takeaway formats remain core revenue drivers, especially in North America and Europe.

- Localization of menus—such as regional flavors and culturally adapted offerings—has become a critical competitive strategy.

What are the latest trends in the western fast food market?

Digitalization and Omnichannel Ordering

The western fast food industry is undergoing rapid digital transformation through mobile applications, AI-driven ordering kiosks, and integrated delivery ecosystems. Major brands are investing heavily in predictive analytics to personalize promotions and improve operational efficiency. Online ordering now represents a significant share of QSR revenues, particularly in urban markets where convenience and speed influence consumer decisions. Loyalty programs integrated into mobile apps are increasing repeat purchases, while automated kitchens and smart inventory systems reduce operational costs and food waste.

Menu Innovation and Health-Conscious Offerings

Consumer preferences are shifting toward balanced indulgence, pushing brands to introduce plant-based proteins, gluten-free options, and calorie-transparent menus. Western fast food chains are expanding beyond traditional burgers and fries into salads, wraps, grilled proteins, and premium beverages. Flexitarian diets and sustainability awareness are driving experimentation with alternative proteins and environmentally friendly packaging. These innovations help brands retain younger consumers while addressing regulatory pressure surrounding nutrition labeling and sustainability.

What are the key drivers in the western fast food market?

Urbanization and Changing Consumer Lifestyles

Rapid urban expansion and longer working hours have increased demand for convenient meal solutions. Consumers increasingly prioritize speed, affordability, and accessibility, positioning western fast food as a primary dining option. Growth of working professionals and students in metropolitan areas significantly boosts weekday consumption patterns, particularly during lunch and evening hours.

Expansion of Franchise-Based QSR Models

Franchising enables rapid geographic expansion with relatively lower capital risk for parent companies. International chains are aggressively expanding into Tier-2 and Tier-3 cities across Asia-Pacific, Latin America, and the Middle East. Local franchise partners help adapt menus, manage supply chains, and navigate regulatory environments, accelerating global footprint growth.

Growth of Food Delivery Ecosystems

Third-party delivery platforms and direct-to-consumer apps have transformed accessibility. Delivery-driven consumption surged post-pandemic and remains structurally embedded in consumer behavior. Virtual kitchens and delivery-only brands are also expanding market reach without requiring large dine-in infrastructure investments.

What are the restraints for the global market?

Rising Raw Material and Labor Costs

Fluctuations in meat, dairy, wheat, and edible oil prices directly impact operating margins. Labor shortages and wage inflation in developed markets further increase operational costs, forcing brands to optimize pricing strategies and automation investments.

Health Regulations and Nutritional Concerns

Government regulations related to calorie labeling, trans fats, and sugar consumption pose challenges for traditional fast food menus. Increasing consumer awareness about obesity and lifestyle diseases may limit frequent consumption unless brands continue innovating healthier alternatives.

What are the key opportunities in the western fast food industry?

Emerging Market Expansion

Rapidly urbanizing economies such as India, Indonesia, Vietnam, and Brazil present significant growth opportunities. Rising disposable incomes and exposure to Western culture through media and tourism are increasing demand for branded fast food experiences. Localization strategies—such as vegetarian menus or regional spices—are enabling deeper penetration.

Automation and Smart Restaurant Technologies

Automation technologies including robotic cooking systems, AI-based demand forecasting, and self-service kiosks are improving operational efficiency. These innovations reduce labor dependence while improving order accuracy and service speed, particularly in high-volume outlets.

Plant-Based and Sustainable Fast Food Concepts

Environmental concerns and ethical consumption trends are creating new revenue streams through plant-based menus and eco-friendly packaging. Partnerships with alternative protein suppliers and carbon-neutral restaurant initiatives are attracting environmentally conscious consumers and investors.

Product Type Insights

The western fast food market demonstrates strong diversification across product categories; however, burgers and sandwiches continue to dominate global consumption patterns, accounting for approximately 34% of global revenue in 2025. The leadership of this segment is primarily driven by its operational scalability, standardized preparation processes, and strong global brand recognition that enables multinational chains to replicate consistent taste profiles across markets. Burgers and sandwiches also benefit from menu innovation strategies such as plant-based alternatives, premium ingredient upgrades, and limited-time offerings, which sustain consumer engagement and repeat purchases. Their portability and suitability for both dine-in and delivery formats further reinforce category dominance, making them the leading revenue-generating segment worldwide.Pizza remains a significant contributor to market revenues due to its strong compatibility with group dining occasions and digital delivery ecosystems. The category has evolved beyond traditional dine-in consumption, becoming one of the most delivery-optimized food formats globally. Technological integration in ordering systems, customizable toppings, and value-based family meal bundles continue to drive sustained demand across developed and emerging markets alike.The fried chicken segment has emerged as one of the fastest-expanding categories, particularly across Asia-Pacific and Middle Eastern markets. Growth is supported by successful localization strategies, including region-specific spices, sauces, and portion formats that align with local taste preferences. Operators increasingly leverage fried chicken menus to penetrate price-sensitive markets due to flexible pricing tiers and strong appeal among younger demographics.Western-style snacks such as fries, nuggets, onion rings, and side-based offerings remain strategically important to profitability. These items significantly increase average order value and margins due to lower ingredient costs and high consumer attachment as complementary purchases. Snack innovation, including loaded fries and shareable appetizers, has strengthened cross-selling opportunities and enhanced customer spending per visit.

Service Type Insights

Quick Service Restaurants (QSRs) represent the dominant service model within the western fast food market, accounting for nearly 61% of total revenue in 2025. The segment’s leadership is driven by operational efficiency, standardized workflows, and the ability to serve high customer volumes with minimal wait times. Automation technologies, kitchen optimization systems, and digital ordering kiosks have further improved throughput capacity, allowing QSR operators to maintain cost efficiency while expanding globally. The primary growth driver for this leading segment is consumer preference for convenience-oriented dining solutions that align with fast-paced urban lifestyles and time-constrained work schedules.Drive-thru service formats continue to gain prominence, particularly in North America and increasingly across Europe and Asia-Pacific, as mobility-focused consumption patterns expand. Investments in dual-lane drive-thrus, AI-powered ordering systems, and predictive menu technology are improving order accuracy and reducing service times, thereby increasing customer retention and revenue per outlet.Fast-casual restaurant concepts are gaining momentum among urban consumers seeking higher-quality ingredients, transparent sourcing, and customizable meal options while retaining quick service convenience. This format bridges the gap between traditional QSR affordability and casual dining experience, attracting middle-income consumers and health-conscious demographics.

Distribution Channel Insights

Offline dine-in and takeaway channels continue to dominate the western fast food market, accounting for approximately 68% of total sales. Physical restaurant locations remain critical brand touchpoints that enhance customer experience, visibility, and impulse purchasing behavior. Modern store formats increasingly incorporate experiential dining environments, digital self-order kiosks, and hybrid seating layouts designed to accommodate both quick visits and social dining occasions.However, online food delivery platforms represent the fastest-growing distribution channel, fundamentally reshaping consumer purchasing behavior. The leading growth driver for this segment is the rapid adoption of smartphone-based ordering ecosystems combined with integrated loyalty programs and personalized promotions. Millennials and Gen Z consumers increasingly prefer app-based ordering due to convenience, real-time tracking, and contactless payment capabilities. Partnerships between global QSR chains and third-party aggregators have expanded delivery coverage, enabling brands to penetrate suburban and secondary cities without significant capital investment in new outlets.Cloud kitchens and delivery-only restaurant models are also emerging as strategic growth avenues, allowing operators to optimize costs while responding to rising digital demand. These models reduce rental expenses and improve operational flexibility, particularly in densely populated urban markets.

End-Use Insights

Individual consumers represent the largest demand segment, accounting for nearly 72% market share, driven by increasing reliance on fast food as a convenient meal replacement option within busy daily routines. Changing household structures, rising single-person households, and extended working hours continue to strengthen individual consumption frequency. Promotional pricing, combo meals, and loyalty rewards programs further encourage repeat purchases among this dominant consumer group.Institutional demand is expanding rapidly, supported by the growth of organized commercial infrastructure worldwide. Airports, shopping malls, entertainment complexes, universities, and corporate campuses increasingly integrate western fast food outlets as anchor foodservice offerings due to their standardized operations and predictable consumer appeal. Institutional partnerships provide stable, high-volume sales opportunities and long-term revenue visibility for operators.

End-Use Analysis

The western fast food market is strongly interconnected with broader economic sectors including retail infrastructure, travel and tourism, and commercial real estate development. Modern shopping malls and multiplex entertainment centers increasingly depend on QSR tenants to enhance visitor dwell time and drive overall foot traffic. As experiential retail gains importance, foodservice outlets play a central role in consumer engagement strategies.The recovery and expansion of the global travel and tourism industry are significantly boosting fast food demand across airports, railway stations, and highway service areas. Travelers prioritize quick, recognizable meal options, favoring international fast food brands known for consistent quality and rapid service. This trend is particularly evident in North America and Asia-Pacific, where passenger traffic growth directly correlates with foodservice revenue expansion.Corporate office complexes represent another emerging end-use environment, driven by hybrid work models and increased demand for convenient dining solutions near workplaces. Employers increasingly incorporate branded foodservice outlets within office campuses to improve employee experience and productivity.Additionally, international franchise expansion contributes to export-oriented revenue generation, where global brands benefit from royalty streams, centralized supply chain exports, and standardized ingredient sourcing. The broader foodservice industry is projected to grow at over 6% annually through 2031, providing a strong structural foundation supporting long-term western fast food market expansion.

| By Product Type | By Service Model | By Distribution Channel | By Consumer Demographics | By Price Category |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of global market share in 2025, maintaining its position as the most mature and revenue-intensive regional market. The United States continues to lead global consumption due to deeply embedded QSR culture, high disposable incomes, and advanced restaurant infrastructure. One of the primary regional growth drivers is the widespread adoption of drive-thru and digital ordering technologies, which enable faster service delivery and higher operational efficiency. Continuous menu innovation, including healthier alternatives and premium product launches, sustains consumer engagement despite market maturity. Canada contributes steady growth through expansion of fast-casual dining formats and strong penetration of online delivery platforms, supported by urbanization and technology adoption.

Europe

Europe represents nearly 24% of global demand, supported by diversified consumer preferences across Western and Eastern European markets. Regional growth is driven by increasing demand for healthier menu options, plant-based offerings, and sustainable packaging initiatives aligned with stringent environmental regulations. Urbanization and dense city layouts favor delivery and takeaway formats, accelerating digital ordering adoption. Additionally, tourism recovery across countries such as the United Kingdom, France, Spain, and Italy is significantly boosting fast food consumption in transit hubs and city centers. Premiumization trends and locally adapted menus are helping international brands maintain relevance among European consumers.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR exceeding 8%, supported by rapid urbanization, rising middle-class populations, and increasing exposure to Western dining culture. China and India serve as primary growth engines due to large populations and aggressive outlet expansion strategies by global franchises. A key regional driver is the integration of digital ecosystems, including super-app ordering platforms, mobile payments, and delivery logistics networks that enable high-frequency consumption. India’s growth is further fueled by youthful demographics, expanding shopping mall infrastructure, and localized menu innovation tailored to regional tastes. Japan and South Korea contribute through technologically advanced retail environments and strong consumer acceptance of convenience dining.

Middle East & Africa

The Middle East & Africa region is experiencing steady expansion, led by Gulf Cooperation Council countries such as Saudi Arabia and the United Arab Emirates. High disposable incomes, strong mall culture, and a young expatriate population drive consistent demand for western fast food brands. Regional growth is supported by franchising models that enable rapid market penetration with relatively low capital risk for global operators. In Africa, expansion is gradual but promising, particularly in South Africa, Nigeria, and Kenya, where urban population growth, modernization of retail infrastructure, and increasing brand awareness are encouraging new outlet development.

Latin America

Latin America’s western fast food market growth is primarily driven by Brazil and Mexico, supported by rising urbanization and expanding middle-income populations. The leading regional growth driver is strong consumer preference for value-oriented meal bundles that align with price-sensitive purchasing behavior. International franchise expansion continues to strengthen brand presence, while localized menu pricing strategies improve accessibility across diverse income groups. Growth in delivery platforms and mobile ordering adoption is further enhancing market penetration, particularly in large metropolitan areas where convenience-driven consumption is increasing.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Western Fast Food Market

- McDonald's Corporation

- Yum! Brands Inc.

- Restaurant Brands International Inc.

- Domino’s Pizza Inc.

- Subway IP LLC

- Starbucks Corporation

- Chipotle Mexican Grill Inc.

- Papa John’s International Inc.

- Little Caesars Enterprises Inc.

- Dunkin’ Brands Group

- The Wendy’s Company

- Shake Shack Inc.

- Five Guys Enterprises LLC

- In-N-Out Burger Inc.

- Jollibee Foods Corporation