Water Kefir Grain Market Size

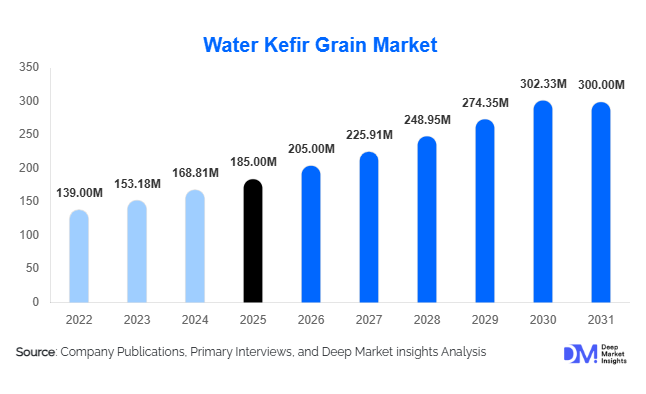

According to Deep Market Insights, the global water kefir grain market size was valued at USD 185 million in 2025 and is projected to grow from USD 205 million in 2026 to reach USD 300 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer demand for natural probiotics, rising adoption of plant-based functional beverages, and growing awareness of gut microbiome health across developed and emerging economies.

Key Market Insights

- Water kefir grains are gaining strong traction as a dairy-free probiotic alternative, particularly among vegan and lactose-intolerant consumers.

- Functional beverage innovation is accelerating global adoption, with water kefir increasingly used in probiotic sodas and fermented drinks.

- North America and Europe dominate consumption due to high health awareness and strong clean-label product penetration.

- Asia-Pacific is the fastest-growing region, supported by rising disposable incomes and expanding wellness-oriented consumer behavior.

- E-commerce platforms are reshaping distribution, enabling direct-to-consumer sales of starter cultures and fermentation kits.

- Home fermentation trends are expanding rapidly, especially among younger demographics seeking personalized nutrition solutions.

What are the latest trends in the water kefir grain market?

Rise of Functional and Clean-Label Beverages

One of the most prominent trends is the rapid expansion of functional beverages that prioritize gut health and natural ingredients. Water kefir is increasingly being used as a base for probiotic sparkling drinks, kombucha alternatives, and fortified wellness beverages. Consumers are shifting away from artificial sodas and sugar-heavy drinks toward naturally fermented, low-calorie alternatives. This trend is further supported by beverage manufacturers launching innovative flavors infused with fruits, botanicals, and adaptogens. The clean-label movement is reinforcing demand for transparent ingredient sourcing and traditional fermentation methods, positioning water kefir as a premium functional ingredient in the global beverage industry.

Expansion of DIY Fermentation Culture

The growing popularity of home fermentation is significantly boosting demand for live water kefir grains and starter kits. Consumers are increasingly interested in preparing probiotic drinks at home due to cost efficiency, personalization, and perceived health benefits. Social media platforms and wellness influencers are playing a crucial role in educating users about fermentation techniques. Subscription-based fermentation kits and digital guides are emerging as strong product offerings. This trend is particularly strong in North America and Europe, where DIY food culture and wellness experimentation are highly established.

What are the key drivers in the water kefir grain market?

Rising Awareness of Gut Health and Microbiome Science

The growing scientific understanding of the human microbiome is one of the strongest drivers of the water kefir grain market. Consumers are increasingly aware of the connection between gut health, immunity, digestion, and mental well-being. As a result, demand for natural probiotic sources such as water kefir has increased significantly. Unlike synthetic supplements, water kefir offers a live, diverse microbial profile, making it a preferred choice among health-conscious consumers.

Shift Toward Plant-Based and Dairy-Free Diets

The global shift toward veganism and plant-based nutrition is another key driver. Increasing lactose intolerance, ethical consumption trends, and sustainability concerns are pushing consumers away from dairy-based probiotics. Water kefir serves as a strong alternative to dairy kefir and yogurt, offering similar functional benefits without animal-derived ingredients. This dietary transformation is particularly strong in Europe, North America, and urban Asia-Pacific markets.

Growth of Functional Beverage Industry

The rapid expansion of the functional beverage sector is significantly supporting market growth. Beverage manufacturers are integrating water kefir cultures into probiotic sodas, wellness drinks, and fermented juices. The demand for low-sugar, natural, and gut-friendly beverages is increasing across retail and foodservice channels, strengthening commercial adoption.

What are the restraints for the global market?

Limited Shelf Life and Culture Sensitivity

One of the key challenges in the water kefir grain market is the short shelf life of live cultures. Maintaining microbial viability during storage, transportation, and distribution is complex and costly. Temperature sensitivity and contamination risks limit large-scale commercialization and global supply chain efficiency.

Low Awareness in Emerging Economies

While adoption is strong in developed regions, awareness of water kefir remains relatively low in several emerging markets. Limited consumer education, lack of distribution infrastructure, and unfamiliarity with fermentation practices restrict faster adoption. This creates a dependency on awareness campaigns and product localization strategies.

What are the key opportunities in the water kefir grain industry?

Expansion into Nutraceutical Applications

Water kefir cultures are increasingly being explored in nutraceutical formulations such as probiotic capsules, powders, and gut-health supplements. This creates strong opportunities for manufacturers to diversify beyond beverages into high-margin supplement categories. The integration of water kefir-derived probiotics into clinical nutrition products also presents long-term growth potential.

Growth in Emerging Markets

Asia-Pacific, Latin America, and parts of the Middle East present significant untapped opportunities. Rising disposable incomes, urbanization, and increasing health awareness are driving demand for affordable functional beverages. Localized production and distribution strategies can help companies capture large-scale growth in these regions.

Technology-Driven Fermentation Innovation

Advancements in freeze-drying, encapsulation, and microbial stabilization technologies are creating opportunities to extend product shelf life and improve scalability. Companies investing in fermentation biotechnology and smart packaging solutions are expected to gain competitive advantage in global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 185 Million |

| Market Size in 2026 | USD 205 Million |

| Market Size in 2031 | USD 300 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Form Insights

The global water kefir market is distinctly segmented by form, with live water kefir grains emerging as the dominant category, accounting for approximately 55% of the global market share in 2025. This dominance is primarily driven by their inherent reusability and the ability to sustain continuous fermentation cycles, making them highly cost-effective for long-term use. Live grains also offer superior microbial diversity, which is increasingly valued by health-conscious consumers seeking robust probiotic benefits. The growing popularity of home fermentation practices, particularly among millennials and wellness-focused households, has further reinforced the demand for live kefir grains. Consumers are increasingly drawn to natural, minimally processed solutions for gut health, positioning live cultures as a preferred choice over synthetic alternatives. In addition, the educational content available through digital platforms and fermentation communities has significantly improved consumer confidence in handling live cultures, thereby supporting sustained adoption.Encapsulated and powdered kefir cultures collectively hold the remaining market share and are primarily utilized in industrial and large-scale production environments. These forms are engineered for enhanced stability, controlled microbial release, and integration into complex product formulations. Their application extends beyond beverages into functional foods, dietary supplements, and fortified products. As food and beverage manufacturers increasingly focus on incorporating probiotics into a broader range of offerings, the demand for these stable and versatile formats is expected to grow steadily. The key driver for this segment lies in its compatibility with industrial processing requirements, including long shelf life, precise dosing, and resistance to environmental fluctuations during manufacturing and distribution.

Application Insights

The application landscape of the water kefir market is led by functional beverages, which account for approximately 45% of the total market share. This segment’s dominance is underpinned by the global surge in demand for probiotic drinks and fermented wellness beverages. Consumers are increasingly shifting away from sugary carbonated drinks toward healthier alternatives that offer digestive and immune health benefits. Water kefir beverages, being naturally fermented and often plant-based, align strongly with clean-label and vegan consumption trends. The leading driver for this segment is the rising consumer awareness of gut microbiome health and its direct link to overall well-being. Beverage manufacturers are capitalizing on this trend by launching innovative flavored kefir drinks, often enriched with fruits, herbs, and functional ingredients, thereby expanding the category’s appeal across diverse consumer demographics.Other food applications, including bakery products, dairy alternatives, and fermented snacks, make up the remaining share of the market. Although currently smaller in scale, this segment holds significant potential as manufacturers explore innovative ways to incorporate probiotics into everyday food items. The integration of water kefir cultures into plant-based and gluten-free products is particularly noteworthy, as it aligns with broader dietary trends. The key growth driver for this segment is the expanding scope of functional food innovation, supported by consumer demand for convenient yet health-enhancing food options.

Distribution Channel Insights

Online retail has emerged as the dominant distribution channel in the global water kefir market, capturing nearly 40% of the total market share. The rapid expansion of e-commerce platforms and direct-to-consumer (DTC) strategies has fundamentally transformed how consumers access fermentation products. Online channels offer a wide variety of options, detailed product information, and customer reviews, enabling informed purchasing decisions. The leading driver for this segment is the increasing digitalization of retail and the convenience of doorstep delivery, particularly for niche and specialty products like water kefir cultures. Additionally, subscription-based models and targeted digital marketing campaigns have further strengthened online sales.B2B direct sales to beverage manufacturers, nutraceutical companies, and food processors represent the remaining share of the market. This channel is gaining importance as industrial adoption of water kefir cultures increases. Manufacturers rely on direct sourcing to ensure quality consistency and supply chain reliability. The key driver for this segment is the rising commercialization of probiotic products and the need for scalable, high-quality raw materials.

End-User Insights

Household consumers dominate the water kefir market, accounting for approximately 50% of the total market share. This dominance is largely attributed to the growing interest in home fermentation, personalized nutrition, and natural health solutions. Consumers are increasingly experimenting with fermentation as a way to enhance dietary quality and reduce reliance on processed foods. The leading driver for this segment is the rising awareness of gut health and the desire for cost-effective, sustainable probiotic sources. Social media platforms and online communities have played a crucial role in popularizing home fermentation practices, further boosting demand among households.Nutraceutical companies hold approximately 15% of the market share, focusing on the development of probiotic supplements and functional health products. These companies are capitalizing on the growing consumer preference for preventive healthcare and natural remedies. The segment is supported by ongoing research into the health benefits of probiotics, which continues to validate their role in maintaining overall well-being.Research institutions and niche applications account for the remaining share, contributing to innovation and scientific advancement in the field of fermentation and probiotics. While relatively small, this segment plays a critical role in driving long-term market growth through research and development initiatives.

Explore more data points, trends and opportunities Download Free Sample Report

Water Kefir Grain Market Segmentations

By Form

- Live Water Kefir Grains

- Freeze-Dried Water Kefir Cultures

- Encapsulated / Powdered Cultures

By Application

- Functional Beverages

- Home Fermentation Kits & DIY Culture Products

- Nutraceutical & Dietary Supplements

- Food Applications

By Distribution Channel

- Online Retail / E-commerce Platforms

- Specialty Health & Organic Stores

- Supermarkets & Hypermarkets

- B2B Direct Sales

By End User

- Household Consumers

- Food & Beverage Manufacturers

- Nutraceutical Companies

- Research & Academic Institutions

Regional Insights

North America

North America holds approximately 28% of the global water kefir market share, with the United States alone accounting for around 22%. The region’s strong position is driven by high consumer awareness of gut health, widespread adoption of plant-based diets, and a well-established functional beverage industry. The presence of leading probiotic brands and a mature retail infrastructure further supports market growth. A key driver of regional growth is the increasing demand for clean-label and organic products, which aligns with the natural fermentation process of water kefir. Additionally, the strong culture of home fermentation, supported by extensive online resources and communities, continues to drive demand for live kefir grains. The rise of health-focused startups and innovation in flavored probiotic beverages also contributes to the region’s dynamic market landscape.

Europe

Europe is the largest regional market, accounting for approximately 32% of the global share. Countries such as Germany, France, and the United Kingdom are at the forefront of consumption, driven by high awareness of clean-label foods and strong regulatory support for natural and organic products. The region benefits from a well-established functional food industry and a long tradition of fermented food consumption. A major driver of regional growth is the increasing emphasis on sustainability and environmentally friendly food production, which complements the low-resource nature of water kefir fermentation. Additionally, the growing popularity of vegan and plant-based diets across Europe is boosting demand for non-dairy probiotic beverages. The region also leads in organic certification and premium product offerings, further enhancing market expansion.

Asia-Pacific

Asia-Pacific holds around 25% of the global market share and is the fastest-growing region. China accounts for approximately 12% of global demand, while India contributes around 6%. The region’s rapid growth is driven by rising disposable incomes, urbanization, and increasing awareness of health and wellness. A key driver of regional growth is the expanding middle-class population, which is increasingly adopting functional foods and beverages as part of a healthier lifestyle. In addition, the region’s long-standing cultural familiarity with fermented products provides a strong foundation for the adoption of water kefir. Countries such as Japan and Australia are contributing to growth through premium health-oriented consumption and innovation in probiotic beverages. The increasing penetration of e-commerce platforms is also facilitating access to water kefir products across urban and semi-urban areas.

Latin America

Latin America accounts for nearly 8% of the global market, with Brazil, Mexico, and Argentina leading demand. The region is characterized by growing health awareness and gradual adoption of functional beverages among urban populations. A key driver of regional growth is the increasing influence of Western dietary trends, which emphasize probiotic consumption and gut health. Additionally, the region’s favorable climate for fermentation and availability of raw materials support local production of water kefir. The expansion of retail infrastructure and the entry of international probiotic brands are further contributing to market development. While still emerging, Latin America presents significant opportunities for growth as consumer awareness continues to rise.

Middle East & Africa

The Middle East & Africa region holds approximately 7% of the global market share and represents a developing market with strong long-term potential. Demand is primarily driven by affluent consumers in countries such as the UAE and Saudi Arabia, where there is a growing focus on health and wellness. A key driver of regional growth is the increasing urbanization and expansion of modern retail channels, which are improving access to functional food products. In Africa, the gradual adoption of fermented beverages is supported by traditional dietary practices and increasing awareness of probiotic benefits. The region is also witnessing improvements in supply chain infrastructure, enabling better distribution of water kefir products. As awareness of gut health continues to grow, the Middle East & Africa is expected to emerge as a promising market for future expansion.

Key Players in the Water Kefir Grain Market

- Novonesis

- International Flavors & Fragrances (IFF)

- Kerry Group

- Lallemand Inc.

- DSM-Firmenich

- Probi AB

- BioGaia

- Cultures for Health

- Wyeast Laboratories

- Sabinsa Corporation

- UAS Labs

- NutraBio Sciences

- Organic Cultures Ltd.

- Chr. Hansen (legacy fermentation operations under Novonesis ecosystem)

- DuPont Nutrition & Biosciences (historical fermentation portfolio integration)