Vitamin K2 Market Size

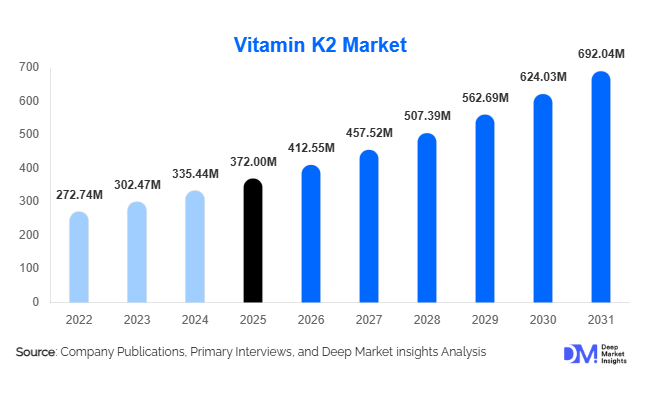

According to Deep Market Insights,the global Vitamin K2 market size was valued at USD 372 million in 2025 and is projected to grow from USD 412.55 million in 2026 to reach USD 692.04 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). The Vitamin K2 market growth is primarily driven by rising awareness of bone and cardiovascular health, increasing adoption of preventive healthcare supplements, and expanding integration of menaquinones (MK-4 and MK-7) into nutraceutical and functional food formulations. Growing aging populations across North America, Europe, Japan, and China, coupled with strong demand for Vitamin D3 + K2 combination products, are further accelerating industry expansion.

Key Market Insights

- MK-7 dominates the product landscape, accounting for over 60% of total market share due to superior bioavailability and longer half-life.

- Natural fermentation-based Vitamin K2 leads sourcing trends, supported by clean-label demand and non-GMO preferences.

- Dietary supplements represent the largest application segment, contributing more than 70% of total revenue.

- North America holds the largest regional share, driven by high supplement penetration and preventive health awareness.

- Asia-Pacific is the fastest-growing region, supported by rising middle-class spending and expanding functional food markets.

- Top five manufacturers account for nearly 55–60% of global supply, reflecting moderate market consolidation.

What are the latest trends in the Vitamin K2 market?

Rising Popularity of Vitamin D3 + K2 Combination Formulations

One of the most prominent trends in the Vitamin K2 industry is the growing adoption of combination supplements, particularly Vitamin D3 paired with MK-7. Clinical research emphasizing the synergistic role of K2 in directing calcium to bones while preventing arterial calcification has significantly increased product innovation. Leading nutraceutical brands are launching high-potency formulations targeting aging populations, post-menopausal women, and cardiovascular health-conscious consumers. This trend is expanding average product pricing and strengthening premium positioning within the supplement category.

Shift Toward Fermentation-Derived, Clean-Label Ingredients

Manufacturers are increasingly investing in fermentation technologies to produce high-purity natural MK-7. Consumers are showing preference for non-synthetic, non-GMO, and allergen-free ingredients, especially in North America and Europe. Advanced microbial fermentation processes are improving yield efficiency and stability profiles, reducing oxidation risks and enhancing shelf life. This clean-label movement is reshaping procurement strategies for nutraceutical brands and increasing demand for traceable supply chains.

What are the key drivers in the Vitamin K2 market?

Aging Population and Osteoporosis Prevalence

Globally, aging demographics are significantly increasing demand for bone health supplements. Vitamin K2 plays a critical role in activating osteocalcin, improving calcium binding in bones. Rising osteoporosis incidence across the U.S., Germany, Japan, and China is boosting long-term supplement consumption. Healthcare professionals increasingly recommend K2 as part of preventive regimens, reinforcing steady demand growth.

Expansion of the Global Nutraceutical Industry

The global nutraceutical sector is growing at approximately 8% annually, providing a strong foundation for Vitamin K2 expansion. Increasing disposable income, urbanization, and digital supplement sales channels are enhancing accessibility. E-commerce platforms are enabling smaller brands to launch niche bone-health and cardiovascular formulations, widening market penetration.

What are the restraints for the global market?

High Production Costs of MK-7

Fermentation-based MK-7 production requires sophisticated bioreactors, purification systems, and strict quality control standards. These capital-intensive processes increase production costs compared to other fat-soluble vitamins. Price sensitivity in developing markets may limit adoption in mass-market supplements.

Regulatory Variability Across Regions

Health claims associated with Vitamin K2 differ across jurisdictions. While the U.S. provides relatively flexible supplement frameworks, European regulatory approvals for functional claims are stricter. This inconsistency limits marketing messaging and slows expansion in certain markets.

What are the key opportunities in the Vitamin K2 industry?

Fortification of Functional Foods and Dairy Products

Functional dairy, plant-based milk, yogurts, and fortified beverages present significant growth potential. Asia-Pacific, particularly China and India, is witnessing rapid growth in fortified foods. Government micronutrient fortification initiatives create long-term opportunities for integrating Vitamin K2 into mainstream food products.

Pharmaceutical Integration for Cardiovascular Applications

Clinical studies linking K2 to arterial health open doors for pharmaceutical-grade formulations. Prescription bone-density treatments and cardiovascular prevention therapies may increasingly incorporate MK-7. This shift could expand high-margin pharmaceutical applications beyond traditional supplements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 372 Million |

| Market Size in 2026 | USD 412.55 Million |

| Market Size in 2031 | USD 692.04 Million |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

MK-7 leads the market, accounting for approximately 62% of total revenue in 2025, driven by superior bioavailability and longer half-life compared to MK-4. MK-4 continues to serve niche pharmaceutical applications, particularly in Japan, while minor menaquinones (MK-9 and others) remain specialized segments with limited commercial volume. The shift toward premium MK-7 formulations has strengthened price realization across the value chain.

Source Insights

Natural fermentation-derived Vitamin K2 dominates the global market, accounting for nearly 68% of total revenue share in 2025. This leadership is primarily driven by increasing consumer preference for clean-label, non-synthetic, and naturally sourced ingredients, particularly across developed markets. Fermentation-based production, commonly utilizing bacterial cultures, aligns well with regulatory expectations in major regions and meets stringent purity standards required for nutraceutical and pharmaceutical applications. Continuous advancements in fermentation technology have significantly improved production yields, reduced impurity levels, enhanced stability profiles, and lowered overall manufacturing costs, further strengthening the competitive positioning of natural variants. In contrast, synthetic Vitamin K2, while cost-effective and widely available, is gradually losing share within premium supplement categories due to growing consumer skepticism toward synthetic additives and shifting brand strategies toward transparency and natural positioning.

Application Insights

Dietary supplements represent the largest application segment, contributing approximately 71% of the global Vitamin K2 market. The segment’s dominance is driven by rising awareness of bone health, cardiovascular wellness, and the synergistic role of Vitamin K2 with Vitamin D3 in calcium metabolism. Increasing preventive healthcare adoption, physician recommendations, and direct-to-consumer supplement marketing continue to support robust growth in this segment. Functional foods are emerging as a high-growth category, expanding at double-digit rates as manufacturers incorporate Vitamin K2 into fortified dairy products, beverages, and nutritional bars to cater to health-conscious consumers. Pharmaceutical applications are gradually expanding through targeted therapies addressing osteoporosis, arterial calcification, and post-menopausal bone health management. Meanwhile, animal nutrition remains a smaller yet stable segment, particularly in poultry feed formulations where Vitamin K2 supports improved bone strength, egg production efficiency, and overall livestock productivity.

End-Use Industry Insights

The nutraceutical industry leads the market with nearly 69% share of global demand, supported by rapid product innovation, expanding online retail channels, and increasing consumer preference for preventive health solutions. The sector benefits from strong branding strategies, growing e-commerce penetration, and international trade flows, particularly from major manufacturing hubs in the United States, Germany, China, and India. Pharmaceutical applications are expanding steadily, especially in osteoporosis management and cardiovascular risk reduction therapies, where clinical validation continues to strengthen market credibility. Veterinary and animal feed industries are recording annual growth rates of 6–7%, driven by improvements in poultry productivity, livestock health management practices, and rising demand for high-quality animal protein. Export-oriented supplement manufacturing in key economies further reinforces global supply chain integration and enhances overall market scalability.

Explore more data points, trends and opportunities Download Free Sample Report

Vitamin K2 Market Segmentations

By Product Type

- MK-4 (Menaquinone-4)

- MK-7 (Menaquinone-7)

- MK-9

- Other Menaquinones (MK-6, MK-8, MK-10)

By Source

- Natural (Fermentation-Based)

- Natural (Animal-Derived)

- Synthetic

By Form

- Powder

- Oil

- Capsules & Softgels (Bulk Supply)

- Liquid Drops

By Application

- Dietary Supplements

- Functional Food & Beverages

- Pharmaceuticals

- Animal Nutrition

By Distribution Channel

- B2B (Bulk to Manufacturers)

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Online Retail

By End-Use Industry

- Nutraceutical Industry

- Pharmaceutical Industry

- Functional Food Industry

- Veterinary & Animal Feed Industry

Regional Insights

North America

North America accounts for approximately 34% of the global Vitamin K2 market in 2025, making it the leading regional market. The United States contributes nearly 80% of regional consumption, supported by high dietary supplement penetration, strong physician endorsement of bone-health supplements, and advanced retail distribution networks including pharmacy chains and online platforms. Rising awareness of cardiovascular health, an aging population, and increasing consumer spending on preventive healthcare continue to drive demand. Canada adds stable growth through pharmacy-led supplement sales channels and expanding wellness-focused retail infrastructure. Regulatory transparency and established quality standards further strengthen consumer confidence across the region.

Europe

Europe holds nearly 29% share of the global market, led by Germany, the United Kingdom, France, Italy, and the Netherlands. Growth in the region is supported by strong preventive healthcare awareness, a rapidly aging demographic profile, and well-established nutraceutical industries. Germany remains a major manufacturing and consumption hub, while the United Kingdom and France demonstrate increasing adoption of bone and heart health supplements. Clear regulatory frameworks governing supplement quality and labeling enhance consumer trust and product standardization. Additionally, rising healthcare expenditure and increasing demand for clinically supported nutraceutical formulations contribute to stable and sustained regional growth.

Asia-Pacific

Asia-Pacific commands approximately 28% share and represents the fastest-growing regional market, expanding at an estimated CAGR of 12–13%. China and Japan are key contributors, with Japan benefiting from traditional natto consumption, a natural source of Vitamin K2, which supports cultural familiarity and higher awareness levels. China’s growth is fueled by expanding middle-class populations, increasing online supplement sales, and domestic manufacturing capacity expansion. India is emerging rapidly due to rising health awareness, growing supplement adoption, and government-backed manufacturing initiatives aimed at strengthening domestic nutraceutical production. Urbanization, expanding pharmacy chains, and increasing physician-led preventive healthcare recommendations further accelerate demand across the region.

Latin America

Latin America accounts for nearly 5% of the global market, led by Brazil and Mexico. Market growth is supported by expanding middle-class populations, improving retail supplement penetration, and increasing awareness of bone health and aging-related conditions. Strengthening pharmacy networks, growing e-commerce channels, and rising healthcare investments are gradually enhancing product accessibility across urban centers. Although price sensitivity remains a challenge, premium supplement adoption is steadily increasing in metropolitan markets.

Middle East & Africa

The Middle East & Africa region represents approximately 4% of global demand. The United Arab Emirates and South Africa serve as key contributors, supported by premium supplement imports, expanding pharmacy chains, and rising health-conscious expatriate populations. Increasing lifestyle-related health concerns, improving healthcare infrastructure, and growth in organized retail formats are contributing to gradual market expansion. While the region remains relatively nascent compared to developed markets, improving economic diversification strategies and greater consumer exposure to international nutraceutical brands are expected to support steady long-term growth.

Key Players in the Vitamin K2 Market

- Kappa Bioscience

- Gnosis by Lesaffre

- NattoPharma

- DSM-Firmenich

- Kyowa Hakko Bio

- Zhejiang Medicine Co., Ltd.

- Shanghai Reson Biotech

- GeneFerm Biotechnology

- Seebio Biotech

- Balchem Corporation

- BioActives Japan

- Lesaffre Group

- Viridis BioPharma

- Synergia Life Sciences

- NOW Foods