Vitamin D Market Size

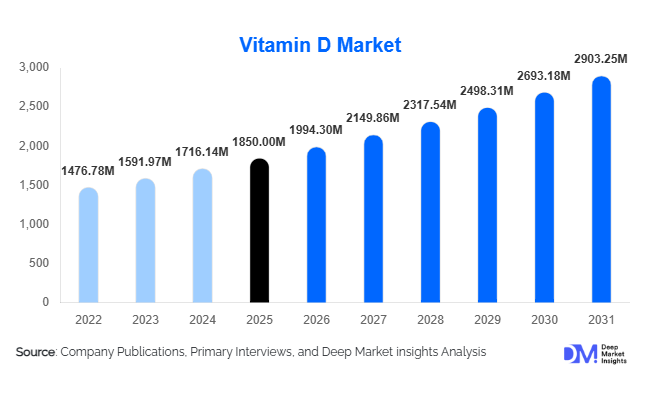

According to Deep Market Insights, the global vitamin D market size was valued at USD 1,850 million in 2025 and is projected to grow from USD 1,994.30 million in 2026 to reach USD 2,903.25 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The vitamin D market growth is primarily driven by rising global prevalence of vitamin D deficiency, increasing preventive healthcare awareness, expanding nutraceutical consumption, and growing food fortification initiatives across both developed and emerging economies.

Key Market Insights

- Vitamin D3 dominates the global market, accounting for nearly 78% of total revenue in 2025 due to superior bioavailability and clinical preference.

- Dietary supplements represent the largest application segment, contributing approximately 55% of global demand.

- North America leads the global market, holding about 32% share in 2025, driven by high supplement penetration and aging demographics.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR, supported by rising health awareness in India and China.

- Plant-based (vegan) vitamin D3 is emerging as a premium segment, commanding 15–25% higher margins compared to conventional animal-derived forms.

- Online distribution channels are rapidly expanding, reshaping global supplement retail and subscription-based consumption models.

What are the latest trends in the vitamin D market?

Shift Toward Preventive and Immune Health Supplementation

Post-pandemic healthcare behavior has permanently increased baseline demand for immune-support supplements, with vitamin D positioned as a foundational micronutrient. Consumers are incorporating daily medium-dose (1,000–5,000 IU) supplementation into long-term wellness routines rather than short-term therapeutic use. This has expanded repeat purchases and subscription-based online sales models. Physicians and health authorities increasingly recommend routine screening for vitamin D deficiency, particularly among elderly populations and urban residents with limited sun exposure. As a result, the market is transitioning from reactive deficiency treatment to preventive health maintenance, creating sustained long-term demand.

Growth of Vegan and Plant-Based Vitamin D3

Traditionally sourced from lanolin, vitamin D3 is now increasingly derived from lichen to cater to vegan and plant-based consumers. This segment is growing at double-digit rates, particularly in Europe and North America, where clean-label and plant-based nutrition trends are strong. Manufacturers are investing in scalable fermentation and plant extraction technologies to meet rising demand. The premium positioning of vegan-certified vitamin D products supports higher profit margins, while sustainability-conscious branding enhances consumer loyalty. Regulatory bodies are also supporting transparency in ingredient sourcing, strengthening trust in plant-based formulations.

What are the key drivers in the vitamin D market?

Rising Global Vitamin D Deficiency

Urbanization, indoor lifestyles, and reduced sunlight exposure have significantly increased vitamin D deficiency rates worldwide. Countries in the Middle East, Europe, and parts of Asia report widespread deficiency across both adult and pediatric populations. Healthcare systems are increasingly recommending supplementation and food fortification, directly boosting pharmaceutical and nutraceutical demand. Government-led awareness campaigns further reinforce long-term consumption patterns.

Aging Global Population

The growing elderly population, expected to surpass 1 billion individuals aged 60+ by 2031, represents a key growth driver. Vitamin D plays a critical role in bone density, fracture prevention, immune support, and muscle function. As osteoporosis and bone-health concerns increase, geriatric-focused supplementation and prescription vitamin D formulations are expanding. Developed economies such as the U.S., Germany, and Japan are witnessing particularly strong demand from aging demographics.

What are the restraints for the global market?

Raw Material Price Volatility

Vitamin D3 production relies heavily on lanolin extraction and complex chemical synthesis processes. Fluctuations in sheep wool supply and precursor chemical prices can impact production costs. Additionally, energy-intensive manufacturing processes expose producers to volatility in utility pricing, affecting margins for bulk manufacturers.

Regulatory and Dosage Compliance Constraints

Strict labeling, upper intake limits, and safety regulations across North America and Europe can delay product approvals and limit high-dose product expansion. Compliance with the FDA, EFSA, and other national authorities increases time-to-market and regulatory costs for new entrants.

What are the key opportunities in the vitamin D industry?

Expansion of Mandatory Food Fortification Programs

Several governments are strengthening vitamin D fortification mandates in dairy products, flour, edible oils, and infant nutrition. Emerging markets in Asia and the Middle East are expanding public health nutrition programs, creating large-scale B2B procurement contracts for manufacturers. Companies capable of supplying customized premixes aligned with regulatory standards are well-positioned to capture stable institutional demand.

Digital Retail and Subscription-Based Models

E-commerce and online pharmacy platforms are reshaping supplement distribution. Direct-to-consumer subscription models ensure recurring revenue and improved customer retention. Emerging economies such as India, Brazil, and Indonesia are witnessing strong growth in digital supplement sales, lowering entry barriers for new brands and expanding geographic reach without heavy infrastructure investment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1850 Million |

| Market Size in 2026 | USD 1994.30 Million |

| Market Size in 2031 | USD 2903.25 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Type Insights

Vitamin D3 dominates the global market, accounting for approximately 78% of total revenue in 2025. Its higher bioavailability and clinical efficacy compared to vitamin D2 have driven widespread adoption across pharmaceutical and nutraceutical formulations. Vitamin D2, while used in specific prescription applications and plant-based formulations, represents a smaller share due to comparatively lower potency. Continuous clinical validation supporting D3’s effectiveness in improving serum 25(OH)D levels reinforces its global leadership position.

Application Insights

Dietary supplements represent the largest application segment, contributing around 55% of global revenue in 2025. Increasing consumer awareness of preventive health and immunity support continues to drive OTC supplement sales. Pharmaceuticals account for a significant share through prescription high-dose formulations used in deficiency treatment. Functional foods and beverages are emerging as a growth segment, particularly in fortified dairy, plant-based milk, and infant nutrition. Animal feed applications remain essential for poultry, livestock, and aquaculture industries, supporting bone health and productivity.

Distribution Channel Insights

Retail pharmacies hold approximately 38% of the market share, benefiting from physician recommendations and OTC supplement purchases. Online channels are the fastest-growing segment, supported by subscription models, influencer marketing, and direct-to-consumer branding. Hospital pharmacies remain significant for prescription formulations, while bulk B2B supply to nutraceutical manufacturers supports large-volume industrial demand.

End-Use Industry Insights

The nutraceutical industry, accounting for nearly 50% of vitamin D consumption, is the fastest-growing end-use segment, expanding at 8–9% CAGR. The pharmaceutical sector maintains steady growth driven by clinical deficiency treatments. The food and beverage industry is witnessing the rising incorporation of vitamin D fortification in dairy and plant-based products. Animal nutrition demand is increasing steadily, particularly in the Asia-Pacific region, where poultry and aquaculture industries are expanding rapidly. Export-driven demand remains strong from Middle Eastern countries, which rely heavily on imported vitamin D ingredients due to high deficiency prevalence.

Explore more data points, trends and opportunities Download Free Sample Report

Vitamin D Market Segmentations

By Type

- Vitamin D2 (Ergocalciferol)

- Vitamin D3 (Cholecalciferol)

By Source

- Animal-Based Vitamin D

- Plant-Based (Vegan) Vitamin D

- Synthetic Vitamin D

By Application

- Dietary Supplements

- Pharmaceuticals

- Functional Foods & Beverages

- Animal Nutrition & Feed

By Formulation

- Tablets

- Capsules & Softgels

- Powders

- Liquid Drops

- Injectable Solutions

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Channels

- Direct B2B Supply

Regional Insights

North America

North America holds approximately 32% of the global vitamin D market in 2025, maintaining its position as the largest regional contributor. The United States accounts for nearly 80% of regional demand, driven by high dietary supplement penetration, strong physician-led recommendations, and advanced healthcare infrastructure that supports routine vitamin deficiency screening. Preventive healthcare spending in the U.S. continues to rise, with vitamin D frequently included in multivitamins, bone health, and immune-support formulations. The presence of major nutraceutical brands, well-established retail pharmacy chains, and a highly developed e-commerce ecosystem further accelerates consumption. Canada also demonstrates a strong per capita intake, supported by long-standing public health fortification policies in dairy and staple foods. Additionally, limited sunlight exposure during extended winter months in northern U.S. states and Canada sustains year-round supplementation demand. Growing elderly demographics and increased awareness of osteoporosis prevention remain core regional growth drivers.

Europe

Europe accounts for approximately 28% of the global vitamin D market, supported by structured fortification frameworks and widespread preventive healthcare adoption. Germany, the U.K., France, Italy, and Nordic countries represent major demand centers. Northern European countries, in particular, experience limited sunlight exposure for extended periods, contributing to higher deficiency prevalence and consistent supplementation uptake. Regulatory guidance from European health authorities encouraging supplementation during winter months strengthens baseline consumption. Western Europe is witnessing strong growth in plant-based and vegan vitamin D3 formulations, aligning with clean-label and sustainability trends. The region’s aging population and expanding nutraceutical sector further drive pharmaceutical-grade and OTC product demand. Additionally, growing government-backed food fortification initiatives in bakery products, dairy alternatives, and infant nutrition are reinforcing long-term structural demand growth across the region.

Asia-Pacific

Asia-Pacific represents approximately 26% of the global vitamin D market and is the fastest-growing region, expanding at over 9% CAGR. Rapid urbanization, increasing indoor lifestyles, and rising awareness of micronutrient deficiencies are key growth catalysts. China plays a dual role as both a major global producer and a large domestic consumer, supported by expanding nutraceutical manufacturing capacity and export-oriented production. India is the fastest-growing country in the region, expanding at nearly 11% CAGR, driven by widespread deficiency prevalence, improving healthcare access, and strong growth in online supplement sales. Japan and South Korea demonstrate high per capita consumption due to advanced healthcare systems and aging populations. In Southeast Asia, growing middle-class incomes and expanding pharmacy retail chains are further boosting demand. Government-led nutrition programs and increasing fortified dairy consumption also contribute significantly to regional expansion.

Latin America

Latin America holds approximately 6% of the global market share, led by Brazil and Mexico. Rising middle-class income levels, improving healthcare awareness, and expanding digital retail penetration are primary growth drivers. Brazil’s large population base and expanding nutraceutical industry contribute significantly to regional consumption. Mexico is witnessing increasing physician recommendations for vitamin D supplementation, particularly among elderly and pediatric populations. Although fortification programs are less widespread compared to North America and Europe, private-label supplement brands are expanding through pharmacy and supermarket chains. Growing adoption of e-commerce platforms is lowering market entry barriers for global brands, accelerating product availability across urban centers.

Middle East & Africa

The Middle East & Africa region accounts for nearly 8% of global vitamin D demand, with strong import dependence in Gulf Cooperation Council (GCC) countries. Saudi Arabia and the UAE represent major consumption hubs due to high deficiency rates associated with limited sun exposure, indoor lifestyles, and cultural clothing practices. Government health campaigns emphasizing routine supplementation and maternal-child health programs are supporting demand growth. In Africa, South Africa leads regional consumption, supported by improving healthcare access and expanding retail pharmacy networks. Although the overall market base remains smaller compared to developed regions, increasing healthcare awareness and expanding pharmaceutical distribution channels are expected to drive steady long-term growth across the region.

Key Players in the Vitamin D Market

- DSM-Firmenich

- BASF SE

- Zhejiang Garden Biochemical

- Fermenta Biotech

- Dishman Carbogen Amcis

- Zhejiang Xinhecheng

- Taizhou Hisound Pharmaceutical

- Synthesia

- Pfizer

- Sanofi

- Glanbia Nutritionals

- ADM

- Lonza

- Divi’s Laboratories

- Orbia