Vitamin C Effervescent Tablets Market Size

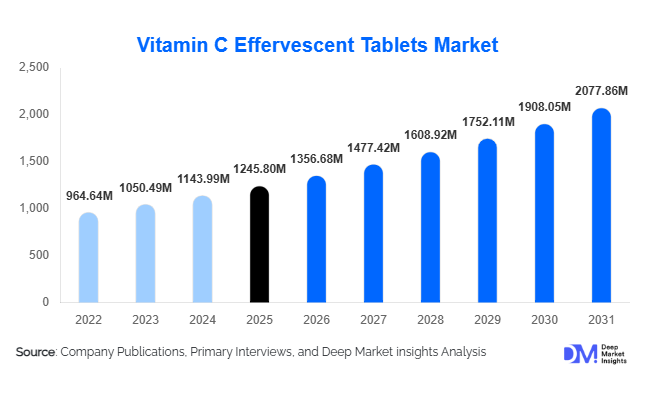

According to Deep Market Insights, the global vitamin C effervescent tablets market size was valued at USD 1,245.8 million in 2025 and is projected to grow from USD 1,356.68 million in 2026 to reach USD 2,077.86 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer awareness regarding immunity enhancement, rising adoption of convenient nutraceutical dosage formats, and expanding preventive healthcare spending worldwide. Effervescent formulations are gaining strong traction due to faster absorption, improved taste profiles, and higher patient compliance compared to traditional tablets and capsules.

Key Market Insights

- Preventive healthcare adoption is accelerating globally, boosting demand for daily immune-support supplements such as vitamin C effervescent tablets.

- Convenience-driven consumption trends are encouraging consumers to shift toward dissolvable dosage formats offering rapid absorption.

- Pharmacy and e-commerce channels dominate distribution, supported by subscription-based supplement purchasing behavior.

- Asia-Pacific represents the fastest-growing regional market, driven by urbanization and rising middle-class health awareness.

- Sugar-free and clean-label formulations are emerging as major innovation areas among manufacturers.

- Technological advancements in effervescent manufacturing are improving stability, shelf life, and flavor masking capabilities.

What are the latest trends in the vitamin C effervescent tablets market?

Shift Toward Preventive and Functional Nutrition

Consumers are increasingly prioritizing preventive healthcare solutions, positioning vitamin C effervescent tablets as daily wellness products rather than seasonal remedies. The COVID-era behavioral shift toward immunity maintenance continues to influence purchasing decisions globally. Functional nutrition trends now integrate vitamin C with zinc, vitamin D, elderberry extracts, and probiotics, transforming effervescent tablets into multifunctional health solutions. Consumers seek products that address immunity, energy support, hydration, and skin health simultaneously, encouraging manufacturers to expand product portfolios. Personalized supplementation and health tracking apps further support repeat consumption patterns.

Flavor Innovation and Sugar-Free Formulations

Flavor innovation has become a major differentiator in the market, with citrus blends, berry variants, and botanical flavors driving consumer engagement. Increasing awareness about sugar intake is pushing companies toward sugar-free, stevia-based, and low-calorie formulations. Clean-label positioning—free from artificial preservatives and allergens—is gaining importance, particularly in developed markets. Manufacturers are also improving effervescence stability to prevent degradation under humid conditions, enabling wider geographic distribution across tropical markets.

What are the key drivers in the vitamin C effervescent tablets market?

Growing Global Immunity Awareness

Rising awareness of immune health remains the strongest growth driver. Consumers increasingly incorporate vitamin C supplements into daily routines to prevent illness rather than treat symptoms. Aging populations across Europe, Japan, and North America are adopting preventive supplementation, while younger demographics view vitamin supplements as lifestyle wellness products.

Expansion of OTC Nutraceutical Markets

The rapid expansion of over-the-counter nutraceutical categories has increased accessibility to vitamin C effervescent tablets. Retail pharmacies, supermarkets, and online marketplaces provide wide product availability, supported by regulatory frameworks allowing non-prescription sales. This accessibility has significantly expanded consumer reach in emerging economies.

Improved Bioavailability and Convenience

Effervescent tablets dissolve rapidly in water, improving absorption rates and reducing gastrointestinal discomfort compared to conventional tablets. The hydration benefit associated with effervescent drinks also enhances product appeal among active consumers, athletes, and working professionals seeking convenient supplementation formats.

What are the restraints for the global market?

Price Sensitivity in Emerging Markets

Effervescent tablets are typically priced higher than standard vitamin tablets due to specialized manufacturing processes and packaging requirements. This price differential limits adoption among cost-sensitive consumers in developing economies.

Stability and Packaging Challenges

Effervescent formulations are highly moisture-sensitive, requiring specialized aluminum tubes or blister packaging. Increased packaging costs and logistics complexities create operational challenges for manufacturers and impact overall profit margins.

What are the key opportunities in the vitamin C effervescent tablets industry?

Expansion into Personalized Nutrition

Digital health platforms and wearable technologies are enabling personalized supplementation recommendations. Manufacturers can leverage data-driven nutrition programs to develop targeted effervescent solutions based on age, lifestyle, or health conditions. Customized vitamin blends present strong opportunities for premium pricing and customer loyalty.

Emerging Market Penetration

Rapid urbanization and healthcare awareness in India, Southeast Asia, Latin America, and the Middle East present strong expansion opportunities. Increasing pharmacy penetration and e-commerce growth allow companies to reach first-time supplement users in these regions.

Integration with Hydration and Functional Beverage Markets

The convergence between dietary supplements and functional beverages is creating new growth avenues. Effervescent tablets positioned as hydration boosters or daily wellness drinks are gaining popularity among fitness-oriented consumers, expanding applications beyond traditional supplementation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1245.80 Million |

| Market Size in 2026 | USD 1356.68 Million |

| Market Size in 2031 | USD 2077.86 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global vitamin C effervescent tablets market demonstrates strong product diversification; however, single-vitamin vitamin C effervescent tablets continue to dominate overall demand, accounting for approximately 46% of the global market share in 2025. This leadership position is primarily attributed to long-standing consumer familiarity with standalone vitamin C supplementation, widespread physician and pharmacist recommendations, and strong scientific validation supporting vitamin C’s role in immune defense, antioxidant protection, and recovery support. Consumers across both developed and emerging economies perceive single-vitamin formulations as reliable, affordable, and effective daily health solutions, making them the preferred entry-level supplement category.The dominance of single-vitamin products is further reinforced by their price accessibility compared with complex multi-ingredient formulations. In price-sensitive markets, consumers often prioritize core immunity benefits over multifunctional supplementation, which strengthens demand for standard vitamin C-only products. Additionally, pharmaceutical companies continue to promote these formulations through pharmacy-led education campaigns, enhancing credibility and repeat purchasing behavior.At the same time, combination formulations containing vitamin C with complementary nutrients such as zinc and vitamin D represent the fastest-growing product category. Growth in this segment is largely driven by evolving consumer expectations toward holistic immunity solutions rather than single-function supplementation. Increasing awareness regarding micronutrient synergy has encouraged manufacturers to develop multi-benefit formulations positioned for immune resilience, respiratory health, and overall wellness optimization. The inclusion of zinc, known for immune modulation, and vitamin D, associated with immune regulation and bone health, significantly enhances perceived product value.Overall, the leading driver behind the product type segment remains consumer trust in clinically established immunity solutions combined with continuous innovation aimed at enhancing convenience, absorption efficiency, and taste experience.

Dosage Strength Insights

The 1000 mg dosage segment leads the global vitamin C effervescent tablets market, accounting for nearly 41% market share in 2025. This dosage level has become widely accepted as the optimal balance between efficacy and safety for daily immune support, positioning it as the standard recommendation across both healthcare professionals and consumer self-care routines. The dominance of the 1000 mg segment is primarily driven by rising preventive healthcare awareness and increased consumer understanding of micronutrient requirements for immune resilience.Following global health awareness shifts, consumers increasingly associate higher vitamin intake with improved protection against fatigue, infections, and environmental stressors. As a result, demand has shifted toward stronger formulations perceived as delivering faster or more noticeable benefits. Marketing strategies emphasizing immune defense, recovery acceleration, and antioxidant protection further reinforce the appeal of higher-strength dosages.The leading growth driver within this segment is the perception of functional efficacy combined with convenience. Effervescent delivery enables rapid dissolution and faster absorption compared with conventional tablets, enhancing consumer confidence in product performance. Additionally, the hydration aspect of effervescent beverages aligns with broader wellness trends emphasizing functional drinks over traditional pills.Lower-dose variants, including 250 mg and 500 mg formulations, maintain stable demand among pediatric users, elderly populations, and consumers focused on preventive daily nutrition rather than therapeutic supplementation. These variants are particularly important in markets with stricter regulatory limits on vitamin dosage claims. Pediatric-focused formulations frequently incorporate milder flavors and reduced acidity to improve compliance.Overall, the continued leadership of the 1000 mg segment is driven by consumer perception of optimal immunity support, strong clinical backing, and widespread global availability across pharmacy and digital retail ecosystems.

Flavor Insights

Flavor innovation plays a critical role in the adoption of effervescent supplements, as taste directly influences consumer compliance and repeat usage. Citrus flavors, particularly orange and lemon, dominate the market with approximately 52% market share, largely due to their natural association with vitamin C-rich fruits. Consumers instinctively connect citrus flavors with authenticity, health benefits, and freshness, making them the default choice across multiple demographics and geographic markets.The dominance of citrus flavors is further supported by sensory familiarity and broad cultural acceptance. Orange-flavored effervescent tablets are often perceived as traditional immunity beverages, reinforcing trust and encouraging daily consumption habits. Pharmaceutical brands have historically relied on citrus profiles to align product taste with nutritional expectations, strengthening long-term consumer loyalty.However, evolving consumer preferences are accelerating growth in mixed fruit, berry, and exotic flavor categories. Younger consumers increasingly seek variety and enjoyable consumption experiences comparable to flavored beverages or functional drinks. Manufacturers are responding by introducing innovative flavor combinations such as berry blends, tropical fruit mixes, mango, and pomegranate, helping reposition effervescent tablets as lifestyle wellness products rather than purely medicinal supplements.Flavor diversification is emerging as a key competitive differentiator, enabling brands to attract new customer segments while increasing product consumption frequency. Seasonal limited-edition flavors and regionally tailored taste profiles are further supporting market expansion, particularly in Asia-Pacific markets where localized flavor preferences strongly influence purchasing behavior.The leading driver of the flavor segment remains improved user experience, transforming supplementation into an enjoyable daily routine that encourages consistent long-term usage.

Distribution Channel Insights

Distribution channels play a central role in shaping consumer accessibility and purchasing confidence within the vitamin C effervescent tablets market. Pharmacies and drugstores account for nearly 38% of global sales, maintaining their leadership due to high levels of consumer trust, professional guidance, and strong regulatory oversight. Pharmacist recommendations significantly influence purchasing decisions, particularly among first-time users and older demographics seeking medically endorsed products.The pharmacy channel benefits from established healthcare infrastructure and the perception of supplements as quasi-medical products rather than general consumer goods. In many regions, pharmacy placement enhances product credibility and supports premium pricing strategies. Additionally, seasonal promotions during flu and allergy seasons contribute to recurring demand spikes.Online retail represents the fastest-growing distribution channel, driven by expanding e-commerce penetration, convenience, and price competitiveness. Direct-to-consumer brand strategies enable manufacturers to build stronger relationships with customers through personalized marketing, subscription programs, and bundled wellness packages. Digital platforms also allow consumers to compare formulations, read reviews, and access educational content, increasing purchase confidence.Supermarkets and health stores continue to play an important supporting role, especially in developed economies where wellness aisles are expanding rapidly. Retailers are increasingly dedicating shelf space to functional nutrition products, reflecting rising consumer demand for preventive health solutions integrated into everyday shopping routines.Omnichannel strategies combining pharmacy credibility with online convenience are becoming a dominant industry trend, enabling brands to maximize market penetration while maintaining consumer trust.

End-Use Insights

Adults represent the largest end-use segment, accounting for approximately 64% market share, driven primarily by increasing adoption of preventive healthcare practices and lifestyle supplementation. Modern consumers are increasingly proactive about maintaining immunity, managing stress, and supporting energy levels, positioning vitamin C effervescent tablets as an essential component of daily wellness routines.The leading driver within the adult segment is growing awareness of immunity maintenance as part of long-term health management rather than short-term illness response. Busy urban lifestyles, environmental pollution exposure, and rising work-related stress levels have encouraged routine supplementation across working-age populations.The sports nutrition and active lifestyle segment is emerging as the fastest-growing end-use category. Effervescent tablets are increasingly positioned as hydration-support solutions that combine electrolyte-style consumption with immune benefits. Fitness enthusiasts favor dissolvable formats that can be consumed before or after workouts, aligning supplementation with performance recovery and endurance support.Pediatric supplementation is also expanding steadily as flavored effervescent formats improve compliance among children who may resist traditional tablets or capsules. Parents increasingly seek convenient immunity solutions for school-age children, particularly during seasonal illness periods. Pediatric-focused marketing emphasizing taste, fun formats, and gentle formulations supports segment expansion.Overall, the end-use segment is driven by lifestyle integration, where supplementation becomes part of everyday health maintenance rather than reactive treatment.

Explore more data points, trends and opportunities Download Free Sample Report

Vitamin C Effervescent Tablets Market Segmentations

By Product Type

- Standard Vitamin C Effervescent Tablets

- Multivitamin Effervescent Tablets with Vitamin C

- Vitamin C + Zinc Effervescent Tablets

- Sugar-Free / Low-Calorie Effervescent Tablets

- Natural & Plant-Based Vitamin C Effervescent Tablets

By Dosage Strength

- Below 500 mg

- 500 mg

- 1000 mg

- Above 1000 mg

By Flavor Type

- Citrus-Based

- Berry-Based

- Tropical Fruit Flavors

- Unflavored/Neutral

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Online Retail & E-commerce

- Health & Wellness Specialty Stores

- Direct Selling & Subscription Models

By End User

- Adults

- Middle-Aged Consumers

- Geriatric Population

Regional Insights

North America

North America accounted for nearly 29% of the global market share in 2025, led primarily by the United States and Canada. The region benefits from one of the world’s most mature dietary supplement industries, characterized by high consumer awareness, strong regulatory frameworks, and widespread availability across retail and healthcare channels. Preventive healthcare spending continues to rise as consumers increasingly prioritize wellness maintenance and immune support.A major regional growth driver is the strong integration of supplements into mainstream healthcare culture. Consumers frequently use vitamins as part of daily routines supported by physician and pharmacist recommendations. High disposable income levels allow widespread adoption of premium formulations, including sugar-free, organic, and clinically branded products.The rapid expansion of e-commerce and subscription-based supplement models further strengthens regional demand. Personalized nutrition trends, supported by digital health platforms and wellness tracking applications, are encouraging consistent supplement consumption. Additionally, aging populations seeking immune and antioxidant support contribute significantly to sustained market growth.

Europe

Europe represents approximately 27% market share, with Germany, the United Kingdom, France, and Italy serving as major consumption hubs. Effervescent tablets have long been popular across Europe, particularly in Germany and Central European countries where dissolvable supplements are deeply embedded in consumer habits.The primary growth driver in Europe is the region’s aging demographic combined with strong wellness-oriented lifestyles. Older populations increasingly adopt preventive supplementation to maintain immune health and vitality. Government-supported public health awareness campaigns further encourage vitamin consumption.European consumers also demonstrate strong preference for high-quality, scientifically validated products, encouraging innovation in clean-label formulations, natural ingredients, and sustainable packaging. Environmental consciousness is shaping product development, with recyclable packaging and reduced carbon footprint initiatives gaining importance among manufacturers.Pharmacy-led distribution remains dominant across many European markets, reinforcing consumer trust and ensuring steady demand growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by China, India, Japan, and South Korea. Rapid urbanization, rising disposable income, and expanding middle-class populations are accelerating adoption of nutraceutical products across the region. Increasing healthcare awareness following recent global health events has significantly strengthened demand for immunity-focused supplements.China leads regional consumption volumes due to large population size and rapidly expanding online health retail platforms. Domestic and international brands are leveraging cross-border e-commerce channels to reach digitally engaged consumers seeking premium imported supplements.India records the fastest growth rate within the region, supported by expanding pharmacy chains, increasing preventive healthcare awareness, and growing acceptance of self-care practices. Rising internet penetration and health education campaigns are encouraging first-time supplement users across urban and semi-urban areas.Japan and South Korea contribute through innovation-driven markets emphasizing functional nutrition, high-quality formulations, and convenience-based health solutions. The popularity of functional beverages aligns strongly with effervescent supplement formats, supporting continued regional expansion.

Latin America

Latin America is witnessing steady growth, with Brazil and Mexico dominating regional demand. Expanding over-the-counter supplement markets and rising urban health awareness are key growth drivers. Consumers increasingly seek affordable immunity solutions that balance effectiveness with price accessibility.Economic development and improving retail infrastructure are enhancing product availability across pharmacies and supermarkets. Younger populations adopting preventive wellness practices are contributing to increased supplement penetration rates. Additionally, growing exposure to global health trends through digital media is accelerating consumer education regarding vitamin supplementation benefits.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market, led by the UAE, Saudi Arabia, and South Africa. Expanding healthcare retail infrastructure, modern pharmacy chains, and rising expatriate populations are strengthening demand for international supplement brands.Key growth drivers include government healthcare diversification initiatives, increasing awareness of preventive health practices, and rising disposable income levels in urban centers. Climate-related health considerations and lifestyle changes are also encouraging consumers to adopt daily supplementation routines.Urbanization and growing modern retail penetration continue to improve accessibility, while digital commerce platforms are introducing global nutraceutical brands to new consumer segments. As healthcare awareness expands across the region, vitamin C effervescent tablets are expected to gain stronger adoption as convenient and affordable immunity-support solutions.

Key Players in the Vitamin C Effervescent Tablets Market

- Bayer AG

- Haleon plc

- Sanofi S.A.

- Reckitt Benckiser Group plc

- Hermes Pharma GmbH

- KRKA d.d.

- Nuun Hydration

- Swisse Wellness Pty Ltd

- Blackmores Limited

- Nature’s Way Products LLC

- NOW Foods

- Berocca (Bayer brand portfolio)

- US Pharma Lab

- Taisho Pharmaceutical Holdings

- Healthy Care Australia