Vegetable Chutney Market Size

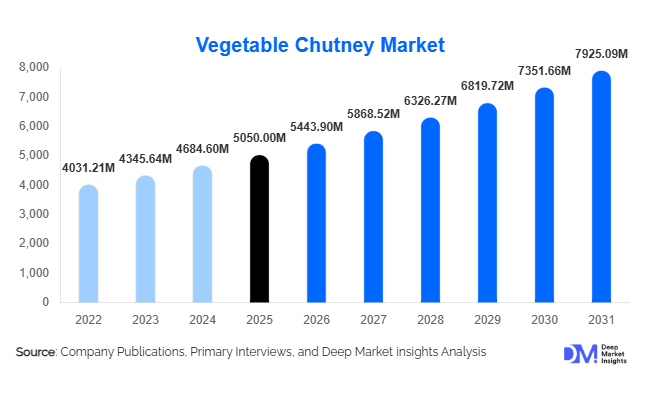

According to Deep Market Insights, the global vegetable chutney market size was valued at USD 5,050 million in 2025 and is projected to grow from USD 5,443.90 million in 2026 to reach USD 7,925.09 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The vegetable chutney market growth is primarily driven by the rising demand for convenient, ready-to-use condiments, increasing global exposure to ethnic cuisines, and the growing preference for plant-based and clean-label food products. The expansion of modern retail formats and e-commerce platforms is further enhancing accessibility and driving global consumption patterns.

Key Market Insights

- Vegetable chutneys are increasingly transitioning from traditional accompaniments to mainstream condiments, driven by their use in fusion cuisines and ready-to-eat meals.

- Organic and clean-label chutneys are gaining traction, as consumers prioritize natural ingredients, transparency, and health-conscious consumption.

- Asia-Pacific dominates the global market, supported by strong cultural consumption patterns and high domestic production.

- North America is the fastest-growing region, fueled by rising demand for ethnic flavors and premium condiments.

- E-commerce channels are reshaping distribution, enabling small and regional brands to access global consumers directly.

- Packaging innovation and shelf-life enhancement technologies are improving export potential and product scalability.

What are the latest trends in the vegetable chutney market?

Premiumization and Artisanal Product Growth

The vegetable chutney market is witnessing a strong shift toward premium and artisanal offerings. Consumers are increasingly seeking unique, handcrafted flavors made with high-quality ingredients and minimal processing. Small-batch chutneys, region-specific recipes, and gourmet variants infused with exotic herbs and spices are gaining popularity across developed markets. This trend is particularly visible in Europe and North America, where consumers are willing to pay a premium for authenticity and superior taste profiles. Brands are also focusing on storytelling, highlighting traditional recipes and sourcing practices to create differentiation and emotional connection with consumers.

Rise of Health-Conscious and Functional Ingredients

Health and wellness trends are influencing product development, with manufacturers incorporating functional ingredients such as turmeric, ginger, garlic, and probiotic-rich elements into chutneys. Low-sugar, low-sodium, and preservative-free formulations are becoming standard offerings. Consumers are also showing increased interest in organic and non-GMO certifications, pushing companies to adopt clean-label strategies. This trend is expanding the market beyond traditional consumers to include health-focused segments, thereby increasing overall demand and product diversification.

What are the key drivers in the vegetable chutney market?

Growing Demand for Convenience Foods

The increasing pace of urban lifestyles has significantly boosted demand for ready-to-eat and easy-to-use food products. Vegetable chutneys provide a quick and flavorful addition to meals, eliminating the need for time-consuming preparation. Their compatibility with a wide range of dishes, including snacks, main courses, and fusion foods, makes them a preferred choice among busy consumers. The rapid expansion of packaged food industries and modern retail channels further strengthens this driver.

Globalization of Food Culture

The widespread exposure to international cuisines through travel, media, and digital platforms is driving the adoption of vegetable chutneys beyond their traditional markets. Consumers in North America and Europe are increasingly incorporating chutneys into everyday meals as dips, spreads, and marinades. This globalization trend is encouraging manufacturers to innovate with flavors and packaging formats tailored to diverse consumer preferences, thereby expanding the market’s global footprint.

What are the restraints for the global market?

Limited Shelf Life of Fresh Products

Fresh vegetable chutneys often have a short shelf life, posing challenges in storage, transportation, and distribution. While preserved variants address this issue, they may face resistance from consumers concerned about additives and preservatives. This creates a trade-off between product freshness and scalability, limiting growth potential in certain segments.

Price Sensitivity in Emerging Markets

In price-sensitive regions, particularly in developing economies, consumers often prefer homemade chutneys due to cost advantages and familiarity. This limits the penetration of branded packaged products and creates challenges for manufacturers aiming to expand in these markets. Competitive pricing strategies and value-based offerings are essential to overcome this restraint.

What are the key opportunities in the vegetable chutney industry?

Expansion into Global Retail and Foodservice Chains

The increasing presence of international retail chains and quick-service restaurants presents a significant opportunity for vegetable chutney manufacturers. By integrating chutneys into menus as dips, sauces, and flavor enhancers, companies can expand their reach and drive volume growth. Strategic collaborations with global foodservice providers can further accelerate market penetration.

Technological Advancements in Packaging

Innovations in packaging, such as vacuum sealing, retort processing, and eco-friendly materials, are enabling longer shelf life and improved product quality. These advancements support export-oriented growth by ensuring compliance with international food safety standards. Sustainable packaging solutions are also aligning with consumer preferences for environmentally responsible products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5050.00 Million |

| Market Size in 2026 | USD 5443.90 Million |

| Market Size in 2031 | USD 7925.09 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type segmentation of the global vegetable chutney market reflects a dynamic interplay between traditional consumer preferences and evolving taste trends, with tomato chutney emerging as the dominant category, accounting for approximately 28% of the total market share in 2025. The leading driver behind the strong performance of tomato chutney lies in its universally appealing flavor profile, which balances sweetness, acidity, and mild spice, making it highly adaptable across a wide range of cuisines. This versatility allows it to function not only as a traditional accompaniment in regional dishes but also as a modern condiment used in sandwiches, wraps, snacks, and fusion recipes. Its compatibility with both vegetarian and non-vegetarian food preparations has further reinforced its widespread acceptance across diverse consumer groups.Green chutneys, typically made from herbs such as coriander and mint, are also witnessing increasing popularity, particularly among health-conscious consumers. The primary growth driver for green chutneys is their association with freshness, low calorie content, and natural ingredients. These chutneys are widely used as dips, spreads, and accompaniments in snacks and street foods, and their growing integration into quick-service restaurant menus and ready-to-eat meal kits is further boosting demand. The increasing popularity of plant-based diets and clean eating trends is also contributing to the expansion of this segment, as green chutneys are often perceived as minimally processed and nutrient-rich.The overall product landscape is being further enriched by the continuous introduction of innovative flavors and formulations. Manufacturers are experimenting with exotic ingredients, regional spices, and fusion concepts to create differentiated offerings that cater to evolving consumer preferences. The leading driver for this innovation is the growing demand for unique culinary experiences, particularly among younger consumers who are more willing to explore new taste profiles. As a result, niche product categories such as fruit-infused vegetable chutneys and spicy gourmet blends are gradually gaining market presence, contributing to the diversification and growth of the overall market.

Nature Insights

The nature-based segmentation of the vegetable chutney market highlights a strong dominance of conventional products, which account for nearly 82% of the total market share in 2025. The leading driver for the continued dominance of conventional chutneys is their affordability and widespread availability across both developed and emerging markets. Conventional production methods benefit from established agricultural practices, efficient supply chains, and lower certification requirements, enabling manufacturers to offer products at competitive price points. This makes them accessible to a broad consumer base, particularly in price-sensitive regions where cost considerations play a crucial role in purchasing decisions.Furthermore, the growth of organic chutneys is being supported by government initiatives and regulatory frameworks that promote sustainable agriculture and organic farming practices. Certification standards and labeling requirements are enhancing consumer confidence, while advancements in supply chain management are improving the availability of organic raw materials. Manufacturers are also investing in product innovation within the organic segment, introducing new flavors and packaging formats that appeal to modern consumers.The interplay between conventional and organic segments is shaping the future of the vegetable chutney market, with both categories coexisting to address different consumer needs. While conventional products continue to dominate in terms of volume and accessibility, organic chutneys are carving out a niche in the premium segment, driven by evolving consumer values and increasing emphasis on health and sustainability. This dual growth trajectory is expected to create opportunities for market players to diversify their offerings and capture a wider range of consumers in the coming years.

Packaging Type Insights

The packaging landscape of the vegetable chutney market is evolving in response to shifting consumer expectations, supply chain efficiencies, and sustainability concerns, with glass bottles continuing to dominate the segment, accounting for approximately 40% of the total market share. The enduring leadership of glass packaging is strongly linked to its superior barrier properties, which effectively preserve flavor, aroma, and nutritional integrity over extended shelf life periods. This makes glass the preferred choice for premium, artisanal, and export-oriented chutney products, where quality perception and product authenticity play a critical role in purchase decisions. Additionally, glass packaging aligns with increasing consumer awareness regarding food safety, as it is non-reactive and free from chemical leaching, further reinforcing its demand among health-conscious buyers.The leading position of glass bottles is also driven by the premiumization trend within the global condiment market, where brands are actively differentiating their offerings through high-quality ingredients and sophisticated packaging formats. Glass containers enhance shelf appeal and support brand storytelling, especially in international markets where Indian and ethnic condiments are positioned as gourmet products. Moreover, the recyclability of glass contributes to its sustained preference in regions with strong environmental regulations, particularly in developed markets.Furthermore, flexible packaging formats are increasingly being adopted for single-serve and on-the-go consumption patterns, reflecting changing lifestyles and the growing demand for convenience foods. Manufacturers are also investing in innovative pouch designs, including resealable and spouted variants, to enhance usability and extend product freshness after opening. In addition, sustainability-driven innovations such as recyclable and biodegradable flexible materials are gradually gaining traction, further strengthening the segment’s growth outlook. Other packaging formats, including plastic jars and PET bottles, continue to hold a moderate share, primarily driven by their affordability and durability, though they face increasing scrutiny due to environmental concerns.

Distribution Channel Insights

The distribution dynamics of the vegetable chutney market are largely shaped by consumer accessibility, retail infrastructure development, and evolving purchasing behaviors, with supermarkets and hypermarkets maintaining a dominant position and accounting for approximately 45% of the global market share. The leading driver behind the dominance of this segment is the ability of large-format retail stores to offer extensive product assortments, enabling consumers to compare brands, flavors, and price points within a single shopping environment. This variety, combined with strong product visibility and in-store promotional activities, significantly enhances consumer engagement and impulse purchasing.In contrast, online retail is emerging as the fastest-growing distribution channel, driven by the rapid expansion of e-commerce platforms and increasing internet penetration worldwide. The primary growth driver for this segment is the convenience it offers, allowing consumers to browse and purchase products from the comfort of their homes while accessing a broader range of options than typically available in physical stores. The rise of digital payment systems, improved logistics infrastructure, and the proliferation of mobile commerce have further accelerated online sales of packaged food products, including vegetable chutneys.Traditional retail formats, including convenience stores and local grocery outlets, continue to play a significant role, particularly in rural and semi-urban areas where organized retail penetration remains limited. These channels are crucial for maintaining last-mile connectivity and ensuring product availability in underserved regions. However, their relative share is gradually declining as consumers transition toward modern and digital retail ecosystems.

End-Use Insights

The end-use landscape of the vegetable chutney market is predominantly driven by household consumption, which accounts for approximately 55% of the total market share. The leading driver for this segment is the integral role of chutneys in daily meal preparation across various cultures, particularly in South Asian households where they serve as essential accompaniments to staple foods. The increasing preference for ready-to-use condiments among busy urban consumers has further reinforced household demand, as packaged chutneys offer convenience without compromising on taste and authenticity.In addition, rising disposable incomes and changing dietary habits are encouraging consumers to experiment with new flavors and cuisines, thereby expanding the scope of chutney consumption beyond traditional uses. The growing awareness of health and wellness is also influencing purchasing decisions, with consumers seeking products made from natural ingredients, free from artificial preservatives, and rich in nutritional value. This has led to the introduction of organic and functional chutney variants, further strengthening the household segment.Furthermore, the growth of the hospitality sector, particularly in emerging economies, is contributing to increased demand for bulk and customized chutney products tailored to specific culinary applications. The expansion of cloud kitchens and food delivery services has also amplified the consumption of packaged condiments, as these businesses rely on consistent and high-quality ingredients to maintain customer satisfaction.Industrial applications represent another important growth area, particularly in the ready-to-eat and processed food segments. The leading driver here is the increasing demand for convenience foods that incorporate traditional flavors, prompting manufacturers to use chutneys as key ingredients in packaged meals, snacks, and sauces. This trend is supported by advancements in food processing technologies and the growing need for scalable production solutions that maintain flavor authenticity while ensuring product stability.

Explore more data points, trends and opportunities Download Free Sample Report

Vegetable Chutney Market Segmentations

By Product Type

- Tomato Chutney

- Onion Chutney

- Garlic Chutney

- Mixed Vegetable Chutney

- Green Chutney

- Others

By Nature

- Conventional

- Organic

By Packaging Type

- Glass Bottles

- Plastic Containers

- Flexible Pouches/Sachets

- Cans

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Foodservice/B2B

By End-Use

- Household Consumption

- Foodservice Industry

- Industrial Use

Regional Insights

Asia-Pacific

Asia-Pacific remains the dominant regional market for vegetable chutneys, accounting for approximately 52% of the global share in 2025, with India serving as the primary growth engine. The region’s leadership is deeply rooted in its strong culinary traditions, where chutneys are an integral component of daily diets. The leading drivers for regional growth include the abundant availability of raw materials such as fruits, vegetables, and spices, which support large-scale production at competitive costs. In addition, the presence of a well-established food processing industry and a vast consumer base further strengthens market expansion.Government initiatives promoting food processing and export-oriented production are also playing a significant role in supporting market growth. The increasing focus on value-added agricultural products is encouraging manufacturers to innovate and diversify their product portfolios. Additionally, the rising popularity of ethnic cuisines in global markets is driving exports from the region, further reinforcing its dominant position.

North America

North America accounts for approximately 18% of the global vegetable chutney market, with the United States leading regional consumption. The primary growth driver in this region is the increasing demand for ethnic and international cuisines, fueled by a multicultural population and growing consumer interest in diverse culinary experiences. The rising popularity of plant-based diets is also contributing to market expansion, as chutneys are often perceived as natural and flavorful alternatives to conventional condiments.In addition, the robust e-commerce ecosystem in the region is facilitating the growth of online retail channels, enabling consumers to access a wide range of domestic and imported chutney products. The increasing integration of chutneys into fusion cuisine, including their use in sandwiches, burgers, and appetizers, is also driving demand across both household and foodservice segments.

Europe

Europe holds nearly 16% of the global market share, with key markets including the United Kingdom, Germany, and France. The leading drivers for growth in this region include the strong presence of multicultural communities, which has significantly influenced food consumption patterns and increased the acceptance of ethnic condiments. The popularity of Indian and Asian cuisines in Europe has created a sustained demand for chutneys as complementary products.Retail innovation, including the expansion of private-label offerings by major supermarket chains, is further enhancing market penetration. Additionally, the rise of food tourism and culinary exploration is encouraging consumers to experiment with new flavors, thereby supporting the growth of the vegetable chutney market in the region.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market for vegetable chutneys, driven by a combination of demographic and economic factors. The leading growth driver is the significant expatriate population, particularly from South Asia, which has created a steady demand for traditional food products, including chutneys. Countries such as the United Arab Emirates and Saudi Arabia serve as key consumption hubs due to their diverse population and high purchasing power.In Africa, rising urbanization and improving economic conditions are gradually expanding the consumer base for packaged food products. The increasing penetration of global food brands and the development of local manufacturing capabilities are also supporting market growth. However, challenges such as supply chain limitations and price sensitivity continue to influence market dynamics.

Latin America

Latin America represents a smaller yet steadily growing market for vegetable chutneys, with Brazil and Mexico emerging as key contributors. The leading drivers for growth in this region include increasing urbanization, rising disposable incomes, and greater exposure to international cuisines through media, travel, and migration. Consumers are becoming more open to experimenting with new flavors, which is driving the adoption of chutneys as versatile condiments.Manufacturers are also exploring opportunities to localize products by incorporating region-specific ingredients and flavor profiles, thereby appealing to local tastes and preferences. While the market remains in a nascent stage compared to other regions, ongoing economic development and changing consumer lifestyles are expected to drive sustained growth in the coming years.

Key Players in the Vegetable Chutney Market

- Unilever PLC

- Nestlé S.A.

- Kraft Heinz Company

- ITC Limited

- Patak’s (Associated British Foods)

- Conagra Brands, Inc.

- McCormick & Company, Inc.

- Premier Foods plc

- Orkla ASA

- Veeba Food Services Pvt Ltd

- MTR Foods Pvt Ltd

- Eastern Condiments Pvt Ltd

- Ashoka Foods

- Priya Foods

- Mother's Recipe (Desai Foods)