Vegan Protein Market Size

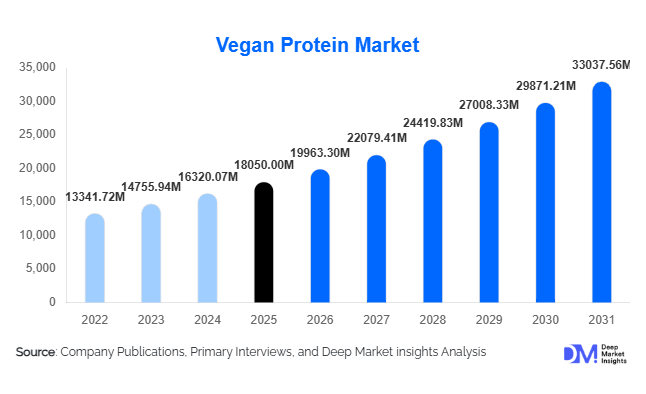

According to Deep Market Insights,the global vegan protein market size was valued at USD 18,050 million in 2025 and is projected to grow from USD 19,963.30 million in 2026 to reach USD 33,037.56 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The vegan protein market growth is primarily driven by rising adoption of plant-based diets, increasing demand for sustainable protein alternatives, and rapid expansion of fortified food and sports nutrition applications worldwide.

The market has transitioned from a niche vegetarian-focused ingredient category into a mainstream functional nutrition segment. Growing consumer awareness regarding cardiovascular health, lactose intolerance, and environmental sustainability is accelerating demand for plant-derived protein isolates and concentrates. Innovations in protein extraction technologies, flavor masking, and texturization have significantly improved taste and digestibility, further expanding applications across ready-to-drink beverages, meat substitutes, dairy alternatives, and high-protein snacks. In addition, strong B2B demand from food processors and nutraceutical manufacturers is ensuring stable volume growth. Emerging economies are scaling pulse cultivation and protein extraction capacity, strengthening global supply chains and export competitiveness. As sustainability commitments intensify across the food industry, vegan protein is becoming a strategic ingredient category for long-term portfolio transformation.

Key Market Insights

- Soy protein leads the global market, accounting for nearly 38% of total share in 2025 due to cost efficiency and complete amino acid profile.

- Protein isolates dominate by product form, holding approximately 42% market share, supported by high-protein fortification trends.

- Food & beverages remain the largest application segment, contributing around 55% of overall demand in 2025.

- North America accounts for nearly 34% of global revenue, driven by strong consumer awareness and established plant-based brands.

- Asia-Pacific is the fastest-growing region, expanding at over 12% CAGR due to rising middle-class income and production investments.

- B2B distribution channels represent nearly 64% of market value, reflecting bulk procurement by food and supplement manufacturers.

What are the latest trends in the vegan protein market?

Hybrid Protein Formulations and Clean-Label Innovation

Manufacturers are increasingly developing blended plant protein solutions combining pea, rice, and fava bean proteins to enhance amino acid completeness and improve taste profiles. Clean-label positioning has become central to product development, with non-GMO, organic-certified, and allergen-free claims gaining prominence. Food brands are reformulating bakery, snacks, and dairy alternatives with fortified plant proteins to meet high-protein labeling requirements. This trend is expanding beyond niche vegan consumers toward mainstream flexitarian populations seeking healthier protein sources without compromising sensory appeal.

Expansion of Fermentation and Functional Processing Technologies

Technological advancements are transforming plant protein functionality. Precision fermentation and enzymatic hydrolysis techniques are improving digestibility and solubility while minimizing off-flavors. Companies are investing in advanced filtration and fractionation systems to increase protein purity levels. These innovations are enabling vegan protein to compete directly with whey protein in sports nutrition and clinical applications. Digital traceability systems and sustainability certifications are also being integrated to meet corporate ESG commitments and regulatory standards across developed markets.

What are the key drivers in the vegan protein market?

Rising Adoption of Plant-Based Diets

The increasing global shift toward vegetarian, vegan, and flexitarian diets is a major growth driver. Consumers are actively reducing animal protein consumption due to health, ethical, and environmental concerns. The growing incidence of lactose intolerance and cholesterol-related conditions further accelerates substitution toward plant-based proteins. This shift has encouraged food manufacturers to expand vegan protein inclusion across mainstream product categories.

Environmental Sustainability and ESG Commitments

Plant proteins require significantly lower land and water resources compared to animal-derived proteins. Corporations are integrating carbon-reduction targets into procurement strategies, promoting plant-based ingredients in reformulated products. Regulatory encouragement for sustainable food systems in Europe and North America is further strengthening demand. As sustainability reporting becomes mandatory in several jurisdictions, vegan protein adoption is increasingly aligned with corporate climate strategies.

What are the restraints for the global market?

Raw Material Price Volatility

Crop yield fluctuations, climate variability, and trade disruptions affect soy and pea pricing, leading to cost uncertainty for manufacturers. Since raw materials represent a significant share of production costs, price volatility can compress margins and limit competitive pricing strategies.

Perception of Incomplete Amino Acid Profile

Despite advancements in protein blending and processing, some consumers continue to perceive plant proteins as nutritionally inferior to animal-based proteins. Overcoming this perception requires sustained R&D investment and marketing education, particularly in sports nutrition and clinical segments.

What are the key opportunities in the vegan protein industry?

Clinical and Geriatric Nutrition Applications

The growing aging population globally presents opportunities for highly digestible, allergen-free protein solutions. Vegan protein isolates tailored for renal diets, muscle preservation, and clinical nutrition programs are gaining attention. This segment offers premium pricing potential and stable institutional demand.

Localized Production and Emerging Market Expansion

Asia-Pacific and Latin America are expanding pulse cultivation and agro-processing capacity. Establishing integrated extraction facilities in India, Brazil, and Vietnam reduces logistics costs and enhances export competitiveness. Government-backed food processing initiatives are encouraging domestic protein production, creating opportunities for new entrants and joint ventures.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18050 Million |

| Market Size in 2026 | USD 19963.30 Million |

| Market Size in 2031 | USD 33037.56 Million |

| CAGR | 10.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Soy protein dominates the global plant-based protein market, accounting for approximately 38% of total revenue in 2025. Its leadership position is supported by an established global cultivation ecosystem across major producing countries such as the United States, Brazil, and Argentina, ensuring stable raw material availability and cost efficiency. The complete amino acid profile of soy protein enhances its functional and nutritional suitability for meat analogues, dairy alternatives, bakery fortification, and ready-to-drink beverages. The leading segment driver for soy protein remains its strong price-to-performance ratio combined with mature processing technologies that enable scalability and consistent product quality.

Pea protein represents the fastest-expanding source segment, driven primarily by its allergen-friendly profile, non-GMO positioning, and strong appeal among clean-label consumers. Growth in pea cultivation in Canada and parts of Europe has strengthened supply chain reliability, further supporting adoption across protein powders, meat substitutes, and nutritional beverages. Emerging sources such as fava bean protein and algae-based proteins are gaining traction in premium and functional formulations due to sustainability advantages, improved digestibility, and innovative extraction technologies, particularly in high-value nutraceutical and specialty food applications.

Product Form Insights

Protein isolates hold the largest share of approximately 42% in 2025, driven by increasing demand for high-protein formulations containing more than 80% protein concentration. The leading segment driver for isolates is the growing consumer preference for high-purity, low-fat, and low-carbohydrate protein ingredients, particularly in sports nutrition beverages, meal replacement shakes, and fortified snack products. Their superior solubility, neutral taste profile, and enhanced functional performance in beverage applications further strengthen segment dominance.

Protein concentrates continue to witness steady demand, particularly in cost-sensitive food processing applications such as bakery products, cereals, and processed foods where moderate protein enrichment is sufficient. Textured vegetable proteins remain essential in plant-based meat analogues due to their fibrous structure and ability to replicate animal meat texture, supporting innovation in burgers, sausages, and ready-to-cook plant-based products.

Application Insights

Food and beverages account for nearly 55% of the total market revenue in 2025, making it the leading application segment. The primary growth driver for this segment is the accelerating consumer shift toward plant-based diets, flexitarian lifestyles, and demand for protein-enriched packaged foods. Rapid expansion of plant-based meat alternatives, dairy substitutes, protein bars, and functional beverages is strengthening volume consumption across retail channels.

Dietary supplements represent the fastest-growing application segment, expanding at over 12% annually. This growth is fueled by rising global fitness culture, increased participation in gym and sports activities, and expanding online retail penetration that facilitates direct-to-consumer protein powder sales. Additionally, animal nutrition applications are expanding, particularly in aquaculture and specialty feed formulations, where plant proteins serve as sustainable alternatives to fishmeal. Clinical nutrition is emerging as a high-value application area due to rising demand for medical diets, elderly nutrition products, and therapeutic protein formulations.

Distribution Channel Insights

B2B distribution dominates the market with approximately 64% share in 2025, reflecting large-scale procurement by food processors, beverage manufacturers, nutraceutical companies, and contract manufacturers. The leading segment driver for B2B channels is bulk purchasing efficiency combined with long-term supply contracts that ensure price stability and ingredient consistency for industrial applications.

Online B2C channels are witnessing rapid expansion, particularly in protein powders, ready-to-mix supplements, and functional beverages. Growth in e-commerce platforms, digital marketing strategies, and direct-to-consumer brand models is enabling manufacturers to improve margins while expanding global reach. Offline retail, including supermarkets and specialty nutrition stores, continues to maintain relevance in emerging markets where in-store purchasing remains dominant.

End-Use Industry Insights

The food processing industry accounts for nearly 48% of total demand, supported by ongoing reformulation of packaged foods to enhance protein content and meet clean-label requirements. The leading segment driver in this category is the increasing pressure on manufacturers to deliver healthier, protein-rich products while maintaining taste and texture standards.

The nutraceutical and sports nutrition industry represents the fastest-growing end-use segment, supported by expanding global fitness awareness, rising disposable income, and growing consumer spending on preventive healthcare products. Pharmaceutical and clinical nutrition industries are emerging as high-value segments, driven by institutional procurement, hospital nutrition programs, and increasing cases of malnutrition and chronic illnesses that require protein-based therapeutic solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Vegan Protein Market Segmentations

By Source

- Soy Protein

- Pea Protein

- Wheat Protein

- Rice Protein

- Potato Protein

- Fava Bean Protein

- Hemp Protein

- Algae Protein

- Other Plant Proteins

By Product Form

- Protein Isolates

- Protein Concentrates

- Textured Protein

- Hydrolyzed Protein

- Protein Blends

By Application

- Food & Beverages

- Dietary Supplements

- Animal Nutrition

- Infant Nutrition

- Clinical & Medical Nutrition

By Distribution Channel

- B2B

- Supermarkets & Hypermarkets

- Specialty Stores

- Online Retail

By End-Use Industry

- Food Processing Industry

- Nutraceutical & Sports Nutrition Industry

- Pharmaceutical & Clinical Nutrition Industry

- Animal Feed Industry

Regional Insights

North America

North America holds approximately 34% of the global market in 2025, led by the United States with nearly 28% share. Regional growth is driven by high consumer awareness of plant-based nutrition, strong presence of established plant-based brands, and advanced food processing infrastructure. The region benefits from extensive soybean cultivation, technological advancements in protein extraction, and robust R&D investment. Canada plays a critical role in global pea protein exports, supported by large-scale pulse production and favorable agricultural policies. Increasing demand for clean-label and sustainable protein alternatives continues to strengthen market expansion across both retail and foodservice sectors.

Europe

Europe accounts for around 30% of global revenue, supported by strong regulatory frameworks promoting sustainable food production and carbon footprint reduction. Germany, the United Kingdom, and France are major contributors, with Germany representing nearly 8% of global demand. Regional growth is driven by stringent sustainability regulations, increasing vegan and flexitarian populations, and growing demand for eco-certified and non-GMO products. Investments in alternative protein innovation, supportive government policies, and expansion of private-label plant-based product lines further accelerate market development across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 12% CAGR. Growth is driven by rising disposable incomes, rapid urbanization, and increasing awareness of protein-enriched diets. China and India are expanding domestic production capacity to reduce import dependence, while Japan demonstrates strong demand for clinical and elderly nutrition applications. The region’s large population base, evolving dietary preferences, and government initiatives promoting plant-based and sustainable food systems are significantly contributing to market growth.

Latin America

Latin America is witnessing steady growth, with Brazil and Argentina benefiting from strong pulse and soybean cultivation, enhancing export potential and raw material availability. Regional growth is driven by expanding middle-class populations, increasing urbanization, and rising health awareness among consumers seeking fortified foods and protein supplements. Improvements in food processing capabilities and growing international trade partnerships further support market expansion.

Middle East & Africa

The Middle East and Africa region is gradually expanding, led by the UAE and South Africa. Growth drivers include increasing health consciousness, rising fitness participation, and strong demand for imported premium nutrition products. Expansion of modern retail infrastructure, growth of specialty health stores, and increasing adoption of Western dietary trends are supporting market penetration. Additionally, government initiatives focused on food security and nutritional diversification are expected to contribute to long-term regional growth.

Key Players in the Vegan Protein Market

- Cargill Incorporated

- Archer Daniels Midland Company

- Roquette Frères

- Ingredion Incorporated

- Kerry Group plc

- International Flavors & Fragrances Inc.

- Glanbia plc

- DSM-Firmenich

- Tate & Lyle PLC

- Bunge Limited

- Wilmar International Limited

- SunOpta Inc.

- Cosucra Groupe Warcoing SA

- Axiom Foods Inc.

- Burcon NutraScience Corporation