Vegan DHA & EPA Market Size

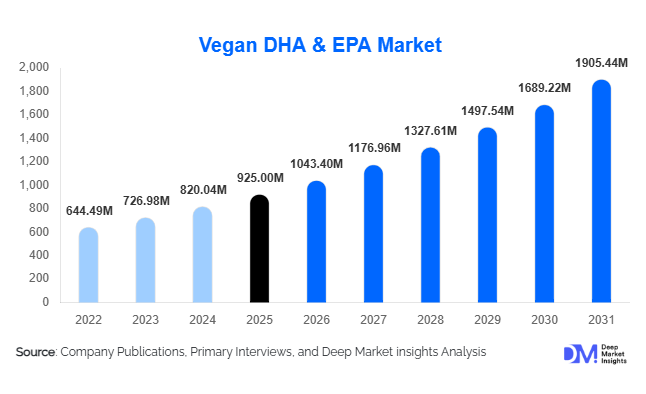

According to Deep Market Insights,the global vegan DHA & EPA market size was valued at USD 925 million in 2025 and is projected to grow from USD 1,043.40 million in 2026 to reach USD 1,905.44 million by 2031, expanding at a CAGR of 12.8% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for plant-based omega-3 alternatives, increasing regulatory mandates for DHA inclusion in infant nutrition, and expanding consumer awareness regarding cardiovascular and cognitive health benefits.

The transition from fish oil–derived omega-3 to microalgae-based DHA and EPA reflects broader sustainability trends and concerns over marine resource depletion. Vegan DHA & EPA ingredients are increasingly preferred for their purity, absence of ocean-borne contaminants, and compatibility with vegan, vegetarian, and allergen-free product formulations. Technological advancements in heterotrophic fermentation and strain optimization are enhancing production yields, lowering cost barriers, and enabling large-scale industrial supply. As dietary supplements, infant formula, and functional food manufacturers accelerate clean-label reformulations, vegan omega-3 solutions are moving from niche positioning to mainstream adoption across global markets.

Key Market Insights

- Dietary supplements account for the largest revenue share, contributing nearly 44% of total market demand in 2025.

- Schizochytrium-based microalgae dominates production, representing approximately 48% of global supply due to higher DHA yields and scalability.

- North America leads the global market, holding around 34% of the 2025 revenue share.

- Asia-Pacific is the fastest-growing region, projected to expand at over 14% CAGR through 2031.

- High-concentration (40–60%) formulations command premium pricing, accounting for nearly 42% of total market value.

- B2B ingredient supply remains the primary distribution channel, contributing 46% of overall revenues.

What are the latest trends in the vegan DHA & EPA market?

Shift Toward Ultra-High Concentration Formulations

Manufacturers are increasingly focusing on ultra-high concentration (>60%) DHA and EPA products targeting pharmaceutical-grade supplements and clinical nutrition applications. These premium formulations allow lower dosage volumes while delivering higher potency, improving consumer compliance and enabling differentiation in competitive nutraceutical markets. Investment in advanced strain engineering and optimized fermentation systems is supporting this trend, as companies aim to enhance EPA ratios alongside traditionally dominant DHA concentrations.

Expansion into Functional Foods and Plant-Based Products

Food and beverage companies are integrating vegan DHA & EPA into dairy alternatives, plant-based beverages, fortified snacks, and meal replacements. As plant-based diets gain traction globally, fortification with algal omega-3 enhances nutritional profiles and strengthens product positioning. Powdered and emulsified formats are particularly favored for stability and seamless incorporation into processed food matrices. This diversification beyond capsules is significantly broadening market penetration.

What are the key drivers in the vegan DHA & EPA market?

Rising Plant-Based and Flexitarian Consumer Base

The rapid expansion of vegan and flexitarian populations globally is a primary driver. Consumers are actively seeking plant-derived nutritional alternatives aligned with sustainability and ethical consumption principles. Vegan DHA & EPA, derived from microalgae, eliminates dependence on marine fisheries while maintaining equivalent bioavailability, making it an attractive substitute for fish oil.

Regulatory Mandates in Infant Nutrition

Many countries mandate DHA inclusion in infant formula, creating consistent demand for high-quality, contaminant-free sources. Algal-derived DHA offers controlled purity levels and supply stability, making it increasingly preferred by infant formula manufacturers. This regulatory-backed demand provides long-term revenue stability and high-margin opportunities for ingredient producers.

What are the restraints for the global market?

High Production and Fermentation Costs

Algal fermentation requires capital-intensive bioreactors, controlled environments, and energy inputs, leading to higher production costs compared to traditional fish oil extraction. These cost structures can limit price competitiveness in emerging, price-sensitive markets.

Limited Awareness in Developing Economies

Despite growing global awareness of omega-3 benefits, consumer education remains limited in certain developing regions. Lower purchasing power and insufficient distribution infrastructure may restrain faster adoption outside mature markets.

What are the key opportunities in the vegan DHA & EPA industry?

Integration into Aquaculture and Sustainable Animal Nutrition

With growing pressure to reduce fishmeal dependency in aquaculture, algal-derived DHA & EPA offer a sustainable alternative feed ingredient. Salmon farming and premium pet food industries are increasingly adopting plant-based omega-3 sources, creating new high-volume demand verticals.

Emerging Asia-Pacific Expansion

Rapid urbanization and rising disposable incomes in China, India, Indonesia, and Vietnam are accelerating nutraceutical consumption. Localization of manufacturing facilities and joint ventures can reduce import reliance and unlock substantial growth potential across APAC markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 925 Million |

| Market Size in 2026 | USD 1043.40 Million |

| Market Size in 2031 | USD 1905.44 Million |

| CAGR | 12.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Schizochytrium-based microalgae dominates the global market, accounting for nearly 48% of the 2025 market share. The leading position of this segment is primarily driven by its superior DHA yield efficiency, scalability of heterotrophic fermentation processes, and cost-effective large-scale commercial production. Manufacturers prefer Schizochytrium strains due to their stable lipid profiles, high DHA concentration, and compatibility with pharmaceutical and nutraceutical quality standards. Continuous technological advancements in strain optimization, controlled fermentation systems, and downstream purification processes further reinforce its commercial viability. Crypthecodinium-based oils maintain strong relevance in infant nutrition applications due to their established safety records and regulatory approvals across major markets. Meanwhile, blended microalgae strains are increasingly adopted to achieve customized EPA-to-DHA ratios, particularly for cardiovascular and cognitive health formulations, reflecting the growing demand for targeted nutritional solutions.

Product Form Insights

Softgel capsules represent approximately 37% of the 2025 market share, emerging as the leading product form due to consumer preference for convenient dosing, enhanced bioavailability, improved shelf stability, and widespread retail availability. The strong penetration of dietary supplements through pharmacies, specialty health stores, and online platforms has significantly contributed to segment growth. Additionally, encapsulation technologies that reduce oxidation and mask taste further enhance product acceptance. Bulk liquid oil continues to dominate the B2B ingredient segment, driven by its extensive use in infant formula fortification, functional food manufacturing, and pharmaceutical applications. Powdered forms are gaining traction in functional foods and beverages due to improved stability, easier blending capabilities, and suitability for ready-to-drink formulations, protein blends, and nutritional bars.

Application Insights

Dietary supplements remain the leading application segment, contributing around 44% of the total market in 2025. This dominance is driven by increasing preventive healthcare awareness, rising consumer focus on heart, brain, and eye health, and the rapid expansion of e-commerce-based supplement brands. Growing vegan and plant-based consumer segments further support demand for algae-derived omega-3 alternatives to fish oil. Infant nutrition continues to represent a stable and high-margin application area, supported by regulatory mandates for DHA inclusion in infant formula across multiple developed markets and increasing birth rates in emerging economies. Pharmaceutical applications are expanding due to clinical research validating omega-3 efficacy in inflammatory and metabolic disorders, while functional foods and beverages demonstrate accelerating growth as manufacturers incorporate fortified ingredients to meet clean-label and wellness-oriented consumer preferences.

Distribution Channel Insights

B2B ingredient supply accounts for nearly 46% of overall revenues, positioning it as the dominant distribution channel. Growth in this segment is driven by sustained procurement from infant formula manufacturers, nutraceutical companies, and functional food producers seeking reliable and traceable omega-3 inputs. Long-term supply agreements, regulatory compliance requirements, and large-scale industrial demand reinforce B2B dominance. Within the B2C segment, online retail is the fastest-growing channel, supported by the expansion of direct-to-consumer supplement brands, subscription-based wellness models, digital health marketing strategies, and increasing consumer trust in e-commerce platforms. The integration of personalized nutrition platforms and influencer-driven product promotion further accelerates online sales growth.

Explore more data points, trends and opportunities Download Free Sample Report

Vegan DHA & EPA Market Segmentations

By Source

- Schizochytrium-Based Microalgae

- Crypthecodinium-Based Microalgae

- Blended Algal Strains

By Product Form

- Bulk Liquid Oil

- Softgel Capsules

- Powder (Spray-Dried)

- Emulsified Formulations

By Concentration Level

- Standard Concentration

- High Concentration

- Ultra-High Concentration

By Application

- Dietary Supplements

- Infant Nutrition

- Functional Food & Beverages

- Pharmaceuticals

- Animal Nutrition & Aquaculture

- Cosmetics & Personal Care

By Distribution Channel

- B2B Ingredient Supply

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Health Stores

Regional Insights

North America

North America holds approximately 34% of the 2025 global market share, with the United States contributing nearly 28%. Regional growth is primarily driven by a well-established dietary supplement culture, high consumer awareness regarding preventive healthcare, strong clinical research backing omega-3 consumption, and favorable regulatory frameworks supporting algae-based ingredients. The presence of leading nutraceutical manufacturers, advanced fermentation technologies, and robust distribution networks further strengthen market expansion. Canada demonstrates steady growth supported by increasing adoption of plant-based nutrition, government-backed health awareness initiatives, and rising demand for sustainable alternatives to marine-derived omega-3 sources.

Europe

Europe accounts for nearly 29% of the 2025 market, led by Germany, France, the United Kingdom, and the Netherlands. Regional expansion is strongly supported by stringent sustainability regulations, environmental concerns regarding overfishing, and mandatory DHA inclusion requirements in infant formula across the European Union. The region benefits from advanced biotechnology infrastructure, established fermentation expertise, and strong research collaboration between academia and industry. Additionally, rising consumer preference for vegan-certified and clean-label supplements, combined with expanding export capacity to global markets, further drives sustained demand across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 14% CAGR. China leads regional demand due to its large infant nutrition industry, growing middle-class population, and increasing health-conscious consumer base. Rapid urbanization, rising disposable incomes, and supportive government initiatives to strengthen domestic biotechnology production are key growth drivers. India and Japan are witnessing accelerating nutraceutical consumption, supported by preventive healthcare trends and aging populations. Furthermore, increasing domestic fermentation capacity, strategic investments in microalgae production facilities, and improving supply chain localization are enhancing regional competitiveness and reducing reliance on imports.

Latin America

Latin America represents around 5% of the global market, with Brazil and Mexico driving supplement demand. Regional growth is supported by expanding middle-class populations, improving healthcare access, and increasing awareness of cardiovascular health benefits associated with omega-3 intake. The expansion of pharmacy chains, online retail penetration, and local nutraceutical manufacturing capabilities further contribute to gradual market development. Government initiatives aimed at nutritional fortification programs also create additional growth opportunities within the region.

Middle East & Africa

The Middle East & Africa accounts for approximately 4% of global revenue. Growth in the region is driven by rising disposable incomes, expanding urban populations, and increasing adoption of premium dietary supplements. Countries such as the UAE and South Africa are witnessing higher consumer spending on preventive healthcare products, supported by modern retail expansion and improved import distribution networks. Growing awareness of lifestyle-related disorders and gradual regulatory standardization are expected to further stimulate long-term market penetration across the region.

Key Players in the Vegan DHA & EPA Market

- DSM-Firmenich

- Corbion N.V.

- ADM

- BASF SE

- Polaris

- Algaecytes

- GC Rieber

- Qualitas Health

- Nordic Naturals

- Clover Corporation

- KD Pharma Group

- Lonza Group

- Cellana Inc.

- Algisys LLC

- Runke Bioengineering