Vegan Dairy Stabilizer Blends Market Size

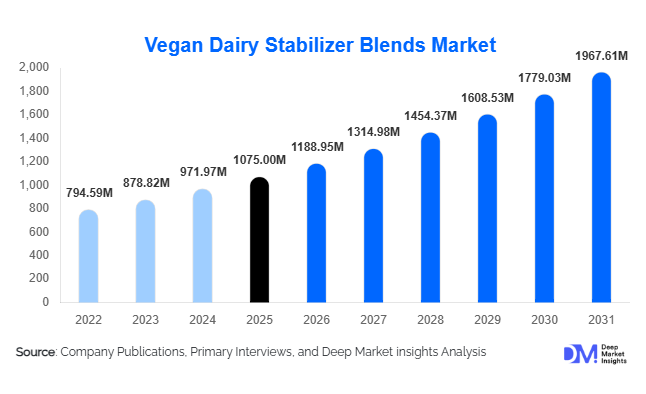

According to Deep Market Insights,the global vegan dairy stabilizer blends market size was valued at USD 1,075 million in 2025 and is projected to grow from USD 1,188.95 million in 2026 to reach USD 1,967.61 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). The market growth is primarily driven by the accelerating demand for plant-based dairy alternatives, rising consumer preference for clean-label and allergen-free ingredients, and continuous innovation in hydrocolloid blending technologies. As plant-based milk, yogurt, cheese, and frozen dessert manufacturers scale globally, the need for advanced stabilizer systems that ensure texture, viscosity, and shelf-life stability is increasing significantly.

Key Market Insights

- Plant-based milk remains the largest application segment, accounting for nearly 31% of total demand in 2025 due to high global consumption volumes.

- Powder-based stabilizer blends dominate the market, holding approximately 67% share, supported by ease of transportation and longer shelf life.

- North America leads the global market, contributing around 34% of total revenue in 2025, driven by strong vegan adoption rates.

- Asia-Pacific is the fastest-growing region, expanding at over 13% CAGR due to rising lactose intolerance awareness and urbanization.

- Direct B2B sales account for nearly 63% of total distribution, reflecting long-term contracts between ingredient suppliers and plant-based dairy manufacturers.

- Top five companies hold approximately 48% market share, indicating moderate consolidation with strong R&D-led competition.

What are the latest trends in the vegan dairy stabilizer blends market?

Clean-Label Reformulation and Natural Hydrocolloids

Manufacturers are increasingly reformulating stabilizer systems to align with clean-label standards and consumer demand for recognizable ingredients. Seaweed-derived extracts such as carrageenan and alginates, fermentation-derived gums like xanthan and gellan, and native starch blends are being optimized to reduce synthetic additives while maintaining functional performance. Brands are minimizing E-number labeling, enhancing transparency, and promoting plant-origin certification. Sustainable sourcing of seaweed and guar is becoming a competitive differentiator, with traceability programs and ESG reporting influencing procurement strategies.

Customization and Co-Development Partnerships

Ingredient companies are expanding application labs and pilot facilities to co-develop customized stabilizer systems tailored to specific plant proteins such as almond, oat, soy, coconut, and pea. These collaborations improve product stability under varying processing conditions including UHT treatment, homogenization, and freeze-thaw cycles. AI-assisted formulation tools and digital modeling platforms are also accelerating product development timelines, enabling faster commercialization of new plant-based dairy products globally.

What are the key drivers in the vegan dairy stabilizer blends market?

Rapid Growth of Plant-Based Dairy Industry

The global plant-based dairy industry, valued at over USD 35 billion in 2026, is expanding at double-digit growth rates. Rising flexitarian and vegan populations across North America and Europe, along with expanding middle-class demand in Asia-Pacific, are fueling production volumes of dairy alternatives. Stabilizer blends are critical for replicating dairy-like mouthfeel and ensuring emulsion stability, directly supporting market growth.

Increasing Lactose Intolerance and Allergen Awareness

High lactose intolerance prevalence in Asia-Pacific and Latin America is accelerating dairy substitution trends. Consumers are actively seeking dairy-free and allergen-free alternatives, increasing the need for optimized stabilizer systems that enhance shelf life and texture without compromising clean-label standards.

What are the restraints for the global market?

Raw Material Price Volatility

Seaweed-derived ingredients such as carrageenan and alginates face supply fluctuations due to climatic variability and harvesting constraints. Price volatility impacts production costs and compresses margins, particularly for smaller manufacturers.

Regulatory and Labeling Scrutiny

Regulatory bodies in Europe and North America are increasingly scrutinizing food additives, creating compliance pressures. Reformulation costs and certification requirements may delay product launches and increase R&D expenses.

What are the key opportunities in the vegan dairy stabilizer blends industry?

Emerging Market Expansion

Countries such as China, India, Brazil, and Indonesia are witnessing rising urbanization and increasing plant-based product penetration. Government-supported food processing initiatives and modern retail growth present significant opportunities for stabilizer manufacturers to expand regional production and distribution networks.

Sustainable and Traceable Ingredient Sourcing

Global food brands are prioritizing ESG-aligned procurement. Companies investing in sustainable seaweed cultivation, fermentation efficiency, and carbon-reduced processing technologies can command premium pricing and long-term supply contracts.

Product Type Insights

Thickener-stabilizer blends dominate the global plant-based dairy stabilizers market, accounting for nearly 28% of the total revenue share in 2025. The leadership of this segment is primarily driven by the increasing demand for viscosity control, texture optimization, and phase stability in high-volume plant-based milk and yogurt formulations. As manufacturers scale production of almond, oat, soy, and coconut-based beverages, the need for multifunctional systems that combine hydrocolloids and emulsifiers has intensified. These blends ensure consistent mouthfeel, prevent sedimentation, and enhance suspension stability during storage and transportation, making them indispensable in large-scale commercial operations. Gelling-stabilizer systems are witnessing expanding adoption in vegan cheese formulations, where structure formation, firmness, and sliceability are critical to consumer acceptance. Meanwhile, protein-integrated blends are gaining strong traction in premium dairy alternatives, particularly high-protein plant-based yogurts and beverages, where improved creaminess and enhanced nutritional value are key product differentiators. The growing focus on clean-label, allergen-free, and non-GMO ingredient systems further supports innovation across all product categories.

Application Insights

Plant-based milk remains the largest application segment, holding approximately 31% of the total market share in 2025. The segment’s dominance is supported by high consumption volumes in mature markets such as North America and Europe, where dairy alternatives have transitioned from niche to mainstream. Continuous product innovation in barista-style beverages, fortified milks, and flavored variants sustains demand for advanced stabilizer systems that deliver uniform consistency and extended shelf stability. Vegan yogurt and cultured products are expanding rapidly, fueled by rising probiotic awareness and digestive health trends. Stabilizers play a crucial role in improving thickness, reducing syneresis, and maintaining texture during fermentation. Plant-based ice cream is experiencing strong growth driven by premiumization, indulgence trends, and the demand for improved melt resistance and creaminess. Vegan cheese applications are also rising steadily as manufacturers refine meltability, stretchability, and structural integrity to better replicate conventional dairy cheese performance, increasing reliance on sophisticated stabilizer solutions.

Form Insights

Powder blends account for around 67% of the total market in 2025, making them the dominant form segment. Their leadership is driven by superior logistical efficiency, longer shelf life, ease of storage, and cost-effectiveness in bulk transportation. Powdered systems allow manufacturers to customize formulations at scale while ensuring consistent dispersion in high-shear processing environments. They are particularly favored in global supply chains where stability across long shipping distances is essential. Liquid concentrates, while representing a smaller share, serve specialized high-speed industrial production lines that require precise dosing, rapid hydration, and uniform dispersion. These systems are increasingly used in automated processing facilities seeking enhanced operational efficiency and reduced formulation errors.

Distribution Channel Insights

Direct B2B sales dominate the market with approximately 63% share, reflecting long-term supply agreements between ingredient manufacturers and plant-based dairy brands. Large-scale producers prioritize direct procurement to secure consistent quality, customized formulations, and stable pricing structures. Strategic partnerships and co-development agreements further strengthen this channel, enabling innovation aligned with evolving consumer preferences. Ingredient distributors play a vital role in supporting mid-sized and regional manufacturers by offering flexible order volumes and technical assistance. Online ingredient platforms are gradually expanding, particularly in emerging markets, where digital procurement systems improve accessibility to specialty stabilizer blends and reduce entry barriers for smaller producers.

End-Use Industry Insights

Food and beverage manufacturing accounts for nearly 72% of total demand in 2025, driven by industrial-scale production of plant-based dairy alternatives. Large manufacturers require consistent ingredient functionality, scalability, and regulatory compliance, reinforcing demand for advanced stabilizer systems. Foodservice and quick-service restaurant chains are increasingly integrating dairy-free beverages, desserts, and cheese alternatives into menus to cater to vegan and flexitarian consumers, accelerating commercial demand. Export-oriented production hubs in the United States, Germany, and China further strengthen industrial consumption, as global trade in plant-based dairy alternatives continues to expand. Additionally, private-label growth across retail chains is increasing bulk procurement of stabilizer blends for cost-efficient mass production.

| By Product Type | By Application | By Form | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States contributing nearly 28% alone. Regional growth is driven by high vegan and flexitarian adoption rates, strong consumer awareness of lactose intolerance and dairy allergies, and advanced food processing infrastructure. Extensive retail penetration of plant-based dairy products across supermarkets and specialty stores further accelerates demand. Continuous product innovation by established plant-based brands, coupled with strong investment in research and development, enhances stabilizer system adoption. The region also benefits from a mature cold chain network and robust private-label expansion, which increases production volumes and ingredient requirements.

Europe

Europe accounts for about 29% of the global market share, led by Germany, the United Kingdom, France, and the Netherlands. Regional growth is supported by strict clean-label regulations, sustainability mandates, and strong environmental awareness among consumers. Government policies encouraging plant-based diets to reduce carbon footprints further stimulate demand for dairy alternatives. The region’s well-established food innovation ecosystem promotes the development of advanced stabilizer systems aligned with organic, non-GMO, and allergen-free standards. High per capita consumption of plant-based beverages and expanding vegan cheese offerings contribute to consistent ingredient demand across both Western and Northern Europe.

Asia-Pacific

Asia-Pacific represents roughly 27% of the global market and is the fastest-growing region, expanding at over 13% CAGR. China and India are key contributors due to high lactose intolerance prevalence, rapidly urbanizing populations, and increasing disposable incomes. Growing awareness of plant-based nutrition, combined with traditional familiarity with soy-based products, accelerates regional adoption. Expanding domestic manufacturing capacity, government support for food processing industries, and rising investments in alternative protein innovation further strengthen growth. The proliferation of e-commerce grocery platforms and modern retail formats also enhances product accessibility across emerging Asian economies.

Latin America

Latin America holds approximately 6% of the global market share, with Brazil and Mexico emerging as key growth markets. Rising health awareness, increasing obesity concerns, and growing middle-class populations are encouraging shifts toward plant-based diets. Regional manufacturers are expanding product portfolios to include plant-based beverages and desserts tailored to local taste preferences. Improvements in retail infrastructure and cross-border trade agreements support broader distribution, gradually increasing demand for specialized stabilizer systems.

Middle East & Africa

The Middle East & Africa region accounts for nearly 4% of the global market share, led by the United Arab Emirates and South Africa. Growth is supported by rising expatriate populations, increasing demand for premium imported plant-based products, and expanding modern retail networks. Health-conscious urban consumers are driving interest in lactose-free and vegan alternatives, particularly in metropolitan areas. Investments in food processing and hospitality sectors, especially within the Gulf Cooperation Council countries, are further contributing to gradual market expansion and increasing adoption of advanced stabilizer formulations.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Vegan Dairy Stabilizer Blends Market

- Cargill, Incorporated

- Ingredion Incorporated

- Kerry Group plc

- Tate & Lyle PLC

- DuPont Nutrition & Biosciences

- CP Kelco

- Ashland Global Holdings Inc.

- Palsgaard A/S

- Jungbunzlauer Suisse AG

- Glanbia plc

- Roquette Frères

- DSM-Firmenich

- Archer Daniels Midland Company

- FMC Corporation

- IFF (International Flavors & Fragrances Inc.)