Vegan Cheese Powder Alternative Market Size

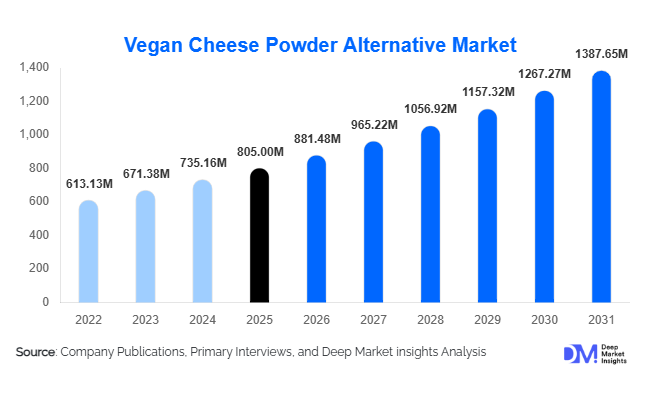

According to Deep Market Insights,The global vegan cheese powder alternative market size was valued at USD 805 million in 2025 and is projected to grow from USD 881.48 million in 2026 to reach USD 1,387.65 million by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing adoption of plant-based diets, rising prevalence of lactose intolerance, growing health awareness, and the expansion of vegan-friendly foodservice and retail offerings worldwide.

Key Market Insights

- Nut-based and soy-based cheese powders dominate the product landscape, preferred for their flavor, texture, and nutritional profile, particularly in foodservice and packaged food applications.

- Foodservice and HoReCa applications are driving demand, with restaurants, cafes, and fast-food chains incorporating vegan cheese powders into pizzas, sauces, and ready meals.

- North America and Europe lead the global market, accounting for over 75% of 2025 consumption due to strong vegan adoption and health-conscious consumer behavior.

- Asia-Pacific is the fastest-growing region, fueled by rising urbanization, middle-class income growth, and growing awareness of plant-based diets in China, India, and Japan.

- Online retail channels are gaining prominence, allowing specialty vegan products to reach a wider audience globally, especially in regions with limited physical store penetration.

- Technological innovation in formulations, including nut-based blends, functional fortification with proteins and vitamins, and enhanced meltability, is reshaping product adoption and consumer preference.

What are the latest trends in the vegan cheese powder alternative market?

Plant-Based Protein Innovation

Manufacturers are investing in R&D to develop vegan cheese powders with improved flavor, texture, and nutritional content. Nut-based, soy-based, and coconut-based powders are being optimized for creaminess, melting properties, and protein enrichment. Innovations include fortified powders enriched with calcium, probiotics, and vitamins, catering to both industrial and home-use applications. These advancements are enabling manufacturers to expand into functional food markets and premium product segments.

Expansion of Retail and E-Commerce Channels

E-commerce and direct-to-consumer sales channels are rapidly growing, providing niche vegan cheese powders with global reach. Online platforms allow consumers to access specialized flavors, fortified products, and international brands, overcoming geographical limitations. Retailers are increasingly offering subscription-based models and bundle packages to attract repeat customers. Social media marketing and influencer-driven campaigns are also shaping consumer awareness and driving trial and adoption.

What are the key drivers in the vegan cheese powder alternative market?

Rising Adoption of Plant-Based Diets

Increasing veganism, lactose intolerance awareness, and flexitarian lifestyles are fueling demand for vegan cheese powders. Consumers are seeking dairy-free alternatives that provide comparable taste and functionality in cooking, baking, and ready-to-eat meals. Rising health consciousness, coupled with the desire to reduce cholesterol and saturated fat intake, further drives market adoption across both retail and foodservice segments.

Growth of Foodservice and Packaged Foods

Restaurants, fast-food chains, cafes, and packaged food manufacturers are increasingly integrating vegan cheese powders into menus and products. This includes pizzas, sauces, snacks, and ready meals. The versatility of powdered formats and pre-flavored blends allows operators to enhance convenience and reduce preparation costs, which supports consistent adoption in high-volume foodservice settings.

Technological Advancements in Product Formulation

Innovation in processing and formulation, such as blending plant proteins and enhancing meltability, is attracting new consumers. Nut-based powders remain particularly popular due to creamy textures, while soy and coconut-based powders offer cost-effective and tropical alternatives. Continuous innovation ensures products meet sensory expectations, widening market appeal.

What are the restraints for the global market?

High Production and Raw Material Costs

Premium ingredients like cashew, almond, and soy increase production costs, resulting in higher prices for vegan cheese powders. This limits adoption in price-sensitive regions, restricting market penetration for mass-market applications. Cost volatility of raw materials also affects profitability for manufacturers.

Supply Chain and Formulation Challenges

Consistency in raw material quality, availability of plant proteins, and technological limitations in achieving ideal meltability or flavor can hinder growth. Manufacturers must manage complex supply chains and innovate formulation techniques to maintain product standards, creating barriers for smaller entrants.

What are the key opportunities in the vegan cheese powder alternative industry?

Emerging Markets in Asia-Pacific

Rapid urbanization and increasing disposable income in countries like China, India, and Japan provide significant opportunities for market expansion. Rising health awareness and exposure to Western dietary trends are encouraging adoption of plant-based cheese alternatives, especially in foodservice and packaged food segments. Manufacturers targeting these regions can benefit from first-mover advantages and growing retail penetration.

Technological Innovation and Functional Fortification

Investment in enhanced formulations, such as protein-enriched, calcium-fortified, or probiotic-infused vegan cheese powders, presents a major growth opportunity. These innovations appeal to health-conscious consumers and premium markets, allowing companies to differentiate products and command higher margins.

Sustainability and Government Support Initiatives

Governments in Europe, North America, and Asia-Pacific are promoting sustainable food systems and plant-based diets. Incentives such as “Make in India” and renewable agriculture programs enable manufacturers to scale operations and reduce production costs, fostering market growth. Sustainability-focused marketing and environmentally responsible sourcing strengthen brand value and consumer trust.

Product Type Insights

Nut-based cheese powders continue to dominate the global market, representing 37% of the 2025 market. Cashew and almond powders are preferred for their creamy texture, versatility, and rich flavor, making them popular in both retail and foodservice applications. Soy-based powders are gaining traction as cost-effective and protein-rich alternatives, while coconut-based powders are increasingly adopted in niche tropical cuisine applications. Rising consumer demand for natural, clean-label, and allergen-friendly products further strengthens the preference for nut-based formulations, particularly in premium and specialty segments. The growth in plant-based and lactose-free diets globally is expected to further reinforce the dominance of these products.

Application Insights

Foodservice and HoReCa applications lead the market, accounting for 41% of the 2025 market. Vegan cheese powders are widely used in pizza chains, ready-to-eat meals, sauces, and snacks, driven by convenience, consistency, and scalability in foodservice operations. Packaged food manufacturing is a fast-growing segment, fueled by the increasing consumer demand for plant-based, on-the-go foods. Home cooking and retail use are also expanding as awareness of vegan diets and lactose intolerance grows. Industrial adoption is gaining momentum as manufacturers integrate vegan cheese powders into processed foods, fortified products, and functional dairy analogs, supporting large-scale production and long-term market growth.

Distribution Channel Insights

Supermarkets and hypermarkets hold the largest share at 55% due to widespread consumer access, organized retail infrastructure, and the availability of multiple brands and formats. Online retail is emerging rapidly, enabling consumers to access specialty vegan products, including subscription and direct-to-consumer models that drive customer loyalty and repeat purchases. Specialty vegan stores, health food outlets, and foodservice procurement channels, though smaller in volume, play a strategic role in promoting niche products and premium offerings. The rise of e-commerce, combined with improved logistics and consumer convenience, continues to accelerate distribution growth globally.

End-Use Insights

Foodservice and packaged food manufacturing are the leading end-use segments, driven by demand from fast-food chains, bakeries, ready meals, and snack production. Export-oriented demand from Europe and North America to APAC and Latin America is rising, with international trade estimated at USD 150 million in 2025 and projected to grow at a 10% CAGR. Emerging applications include fortified functional foods, plant-based dairy analogs, and bakery innovations. Adoption is driven by increasing consumer preference for plant-based nutrition, convenience, and allergen-free formulations, as well as the global push for sustainable and clean-label products.

| By Product Type | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America is the largest regional market, accounting for 41% of global market share in 2025. The USA and Canada lead consumption due to high awareness of vegan diets, lactose intolerance, and rising disposable incomes. Key growth drivers include innovative product launches, adoption of vegan cheese powders in fast-food chains, quick-service restaurants, and packaged food manufacturing. The expansion of e-commerce and specialty retail channels further supports accessibility and consumer engagement. Health-conscious trends, sustainability initiatives, and increasing demand for functional and fortified products also stimulate regional growth.

Europe

Europe contributes 34% of the 2025 market, with Germany, the UK, and France at the forefront. High consumer awareness of plant-based diets, strong foodservice and retail infrastructure, and regulatory support for vegan products drive market expansion. Flavored and fortified powders are increasingly popular, with Germany representing USD 160 million and the UK USD 120 million of regional consumption. Innovation in product formats, combined with sustainability-focused consumer preferences and robust online retail penetration, further accelerates growth in Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region at a projected 11% CAGR, driven by urbanization, rising middle-class income, and increasing social media influence on food trends. China leads in premium and group-oriented foodservice applications, while India is witnessing growth in mid-range retail and packaged food sectors. Japan and Australia show rising interest in both home cooking and foodservice adoption of vegan cheese powders. Regional drivers include the expansion of plant-based food culture, rising lactose intolerance awareness, and government initiatives promoting sustainable and plant-based agriculture.

Latin America

Brazil and Argentina are the primary markets in Latin America, with growth concentrated in foodservice and retail segments. Rising consumer interest in adventure dining, family-friendly meals, and imported premium vegan powders is driving demand. Additional growth factors include expanding modern retail chains, urban middle-class population growth, and trade agreements facilitating the import of plant-based products. The region also shows increasing awareness of health and wellness trends, which positively impacts adoption of vegan cheese powders.

Middle East & Africa

The Middle East and Africa are emerging markets for vegan cheese powders, led by the UAE, Saudi Arabia, and South Africa. Premium imported products are gaining traction among high-income consumers, particularly in retail and foodservice channels. Growth is supported by the expansion of hospitality and tourism sectors, increasing disposable incomes, and a rising focus on health-conscious dining. Intra-regional trade within Africa is expanding, presenting opportunities for local production, distribution, and regional market integration. Awareness campaigns and the adoption of Western plant-based dietary trends also contribute to regional growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Vegan Cheese Powder Alternative Market

- Follow Your Heart

- Vega Foods

- Daiya Foods

- Violife Foods

- Miyoko’s Creamery

- Tofutti Brands

- Earth Island

- Treeline Cheese

- So Delicious Dairy Free

- Better Than Cheese

- Good Planet Foods

- Plantified

- Nutty Cow

- Raw Food Co.

- Vegusto