Vegan Cheese and Processed Cheese Market Size

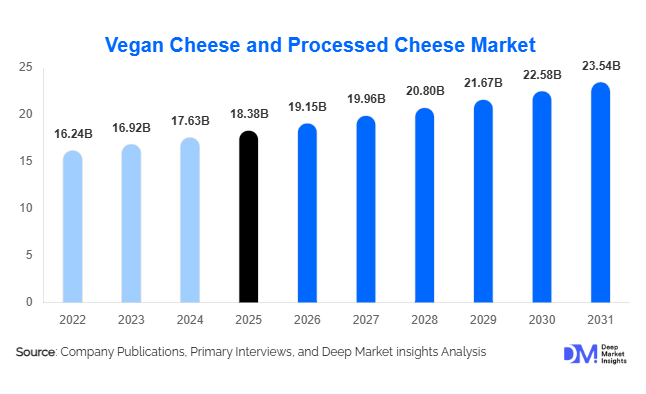

According to Deep Market Insights, the global vegan cheese and processed cheese market size was valued at USD 18.38 billion in 2025 and is projected to grow from USD 19.15 billion in 2026 to reach USD 23.54 billion by 2031, expanding at a CAGR of 4.21% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of plant-based diets, increasing consumption of convenience and ready-to-eat foods, and continuous innovation in cheese processing technologies that improve taste, texture, and shelf stability. The rapid expansion of quick-service restaurants (QSRs), alongside growing lactose intolerance awareness and sustainability-focused food consumption, is accelerating global demand across both vegan and processed cheese categories.

Key Market Insights

- Plant-based cheese adoption is accelerating globally, supported by flexitarian diets and sustainability-driven consumer behavior.

- Processed cheese continues to dominate revenue contribution due to widespread usage in fast food, snacks, and packaged meals.

- North America leads global consumption, driven by strong retail penetration and innovation-led product launches.

- Asia-Pacific represents the fastest-growing region, supported by urbanization and expanding western food consumption patterns.

- Foodservice integration is reshaping demand, with QSR chains increasingly adopting vegan cheese alternatives.

- Advancements in fermentation and plant protein technology are significantly improving product quality and scalability.

What are the latest trends in the vegan cheese and processed cheese market?

Rise of Plant-Based Dairy Innovation

The market is witnessing rapid innovation in plant-based formulations aimed at replicating the functional characteristics of traditional dairy cheese. Manufacturers are increasingly utilizing coconut oil, pea protein, cashew bases, and fermentation-derived proteins to improve meltability and flavor complexity. Precision fermentation technologies are emerging as a transformative trend, enabling production of animal-free casein proteins that closely mimic dairy cheese performance. Retailers are expanding shelf space for vegan cheese products, reflecting strong consumer demand for ethical and sustainable alternatives. Premium artisanal vegan cheese varieties are also gaining traction, particularly in developed markets where consumers prioritize clean-label and allergen-friendly foods.

Convenience and Ready-Meal Integration

Processed cheese demand continues to grow alongside the expansion of frozen foods, ready meals, and snack categories. Food manufacturers rely on processed cheese for consistent texture, extended shelf life, and cost efficiency. Increasing urban lifestyles and dual-income households are fueling consumption of packaged foods globally. Cheese sauces, slices, and spreads are becoming staple ingredients in quick-service restaurants and industrial food processing. The integration of vegan cheese into frozen pizzas, plant-based burgers, and ready-to-eat meals is further bridging traditional and plant-based consumption patterns.

What are the key drivers in the vegan cheese and processed cheese market?

Expansion of Flexitarian and Health-Conscious Diets

Consumers are increasingly reducing dairy intake due to lactose intolerance, cholesterol concerns, and environmental awareness. Flexitarian eating habits are expanding rapidly across North America and Europe, creating sustained demand for vegan cheese alternatives. Health-focused consumers are also seeking fortified cheese products enriched with protein, vitamins, and minerals, strengthening category growth.

Growth of Global Foodservice Industry

The rapid expansion of QSR chains and casual dining outlets worldwide is significantly increasing cheese consumption. Processed cheese remains essential for burgers, sandwiches, and snacks due to its uniform melting properties and affordability. Simultaneously, restaurant chains are incorporating plant-based menu options, driving bulk demand for vegan cheese products compatible with commercial cooking processes.

What are the restraints for the global market?

Price Premium of Vegan Cheese Products

Despite strong demand growth, vegan cheese remains relatively expensive compared to processed dairy cheese due to higher input costs and smaller production scale. This pricing gap limits penetration in emerging economies where affordability strongly influences purchasing decisions.

Raw Material Price Volatility

Fluctuating costs of coconut oil, nuts, plant proteins, and dairy milk affect production economics and pricing stability. Manufacturers must continuously optimize sourcing strategies and formulation efficiency to maintain margins amid volatile agricultural commodity markets.

What are the key opportunities in the vegan cheese and processed cheese industry?

Emerging Market Expansion

Asia-Pacific and Latin America present substantial growth opportunities due to rising disposable incomes and increasing adoption of western dietary habits. Countries such as India, China, and Brazil are witnessing expanding demand for processed cheese through QSR growth, while vegan cheese adoption is gaining momentum among urban consumers seeking healthier food alternatives.

Precision Fermentation and Functional Ingredients

Technological advancements enabling dairy-like proteins without animal agriculture are opening new growth avenues. Companies investing in fermentation-based cheese development can achieve superior texture and flavor while improving sustainability metrics. These innovations are expected to reduce price gaps and expand consumer acceptance globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.38 Billion |

| Market Size in 2026 | USD 19.15 Billion |

| Market Size in 2031 | USD 23.54 Billion |

| CAGR | 4.21% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global processed and vegan cheese market demonstrates a diversified product landscape shaped by evolving consumer preferences, convenience-oriented food consumption patterns, and innovation in plant-based formulations. Processed cheese continues to dominate overall market revenue, primarily driven by its cost efficiency, extended shelf life, standardized taste profile, and strong integration across industrial food manufacturing and foodservice operations. Large-scale food processors and quick-service restaurant chains rely heavily on processed cheese slices, blocks, and spreads due to their melting consistency, functional stability, and suitability for mass production applications such as burgers, sandwiches, frozen meals, and ready-to-eat snacks. The leading segment driver for processed cheese remains its operational versatility and affordability, enabling manufacturers to maintain consistent product quality while optimizing production costs.Vegan cheese represents the fastest-expanding product category, supported by accelerating adoption of plant-based diets, lactose intolerance awareness, and increasing consumer focus on sustainability and animal welfare considerations. Shredded and sliced vegan cheese formats are witnessing particularly strong demand as they replicate traditional dairy functionality for pizzas, pasta, and sandwiches. Advances in food technology, including improved fermentation techniques and plant protein blending using cashew, almond, coconut, and oat bases, are enhancing texture and flavor profiles, thereby improving consumer acceptance. Premium artisanal vegan cheeses are gaining traction within specialty retail channels, where consumers seek gourmet experiences aligned with ethical consumption values. Additionally, fortified vegan cheese products enriched with calcium, vitamin B12, and protein are expanding appeal among health-conscious consumers seeking functional nutrition benefits alongside dairy alternatives.Clean-label innovation is further reshaping product development, with manufacturers reducing artificial additives and emphasizing natural ingredients and transparent sourcing. This shift is strengthening consumer trust and supporting premium pricing strategies, particularly in developed markets where ingredient awareness continues to rise.

Application Insights

Foodservice applications account for the largest share of global consumption, reflecting the critical role cheese plays in modern quick-service and casual dining menus. Burgers, pizzas, wraps, and ready-to-eat meals remain primary demand generators, with cheese functioning as both a flavor enhancer and texture component. The leading segment driver within foodservice is menu standardization and operational efficiency, as processed cheese ensures consistent melting behavior and portion control across high-volume restaurant operations. Rapid expansion of global quick-service restaurant chains and delivery-based dining models continues to reinforce this dominance.Household consumption is expanding steadily as consumers increasingly experiment with home cooking and plant-based meal preparation. Growth in cooking tutorials, digital recipes, and health-focused lifestyle trends has encouraged consumers to incorporate both processed and vegan cheese into daily meals. Vegan cheese adoption is accelerating across plant-based packaged foods, including dairy-free pizzas, frozen entrées, and snack kits, reflecting broader dietary diversification.Processed cheese also plays an essential role in frozen food manufacturing and snack processing industries, where functional stability during freezing and reheating is crucial. Meanwhile, emerging applications such as bakery fillings, creamy sauces, plant-based dips, and dairy-free snack innovations are creating incremental demand opportunities. Manufacturers are leveraging cross-category innovation to expand cheese usage beyond traditional applications, contributing to long-term market expansion.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels globally due to their extensive cold-chain capabilities, wide product assortments, and strong consumer trust. The leading segment driver within this channel is product accessibility, as consumers benefit from one-stop shopping experiences that allow comparison across price tiers, brands, and dietary formats. Large retail chains also enable promotional strategies and private-label expansion, further supporting volume growth.Online retail channels are experiencing rapid expansion, particularly for premium vegan cheese brands that leverage direct-to-consumer strategies and subscription-based purchasing models. Digital commerce platforms enable smaller and innovative brands to reach niche audiences without heavy investment in physical retail infrastructure. Increased smartphone penetration, improved logistics networks, and growing consumer comfort with online grocery purchases are accelerating channel growth globally.Specialty health food stores continue to play a strategic role in launching plant-based innovations, serving as early adoption hubs for new vegan formulations and premium artisanal offerings. Foodservice distributors remain essential in driving bulk demand, supplying restaurants, hotels, institutional catering providers, and cloud kitchens with standardized processed cheese products tailored for large-scale operations.

End-Use Insights

Household retail consumption represents the largest end-use segment, supported by sustained growth in at-home meal preparation and increased experimentation with global cuisines. The leading segment driver is convenience combined with versatility, as cheese products offer quick meal enhancement while aligning with evolving dietary preferences, including flexitarian and plant-based lifestyles. Rising dual-income households and demand for easy meal solutions continue to reinforce retail consumption growth.Quick-service restaurants represent the fastest-growing end-use segment, integrating both processed and vegan cheese into diversified menus designed to appeal to broader consumer demographics. Menu innovation focused on plant-based burgers, dairy-free pizzas, and hybrid protein offerings is accelerating adoption across global restaurant chains. Food processing industries producing frozen foods, snacks, and ready meals also contribute significantly to market expansion, relying on cheese as a core ingredient that enhances flavor and product appeal.Export-driven consumption is rising as established European and North American brands expand into emerging Asian and Middle Eastern markets through strategic partnerships and localized product offerings. Increasing globalization of food preferences is enabling cross-border demand growth and strengthening international supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Vegan Cheese and Processed Cheese Market Segmentations

By Type

- Processed Cheese

- Vegan Cheese

By Application

- Retail

- Ingredients

- Catering

Regional Insights

North America

North America holds the largest share of the global market, accounting for approximately 32% of total demand, supported by mature food processing industries and strong consumer acceptance of both processed and plant-based cheese products. The United States leads regional consumption due to high per capita cheese intake, advanced retail infrastructure, and widespread adoption of convenience foods. Regional growth is primarily driven by continuous product innovation, strong investment in plant-based research and development, and expanding flexitarian consumer populations seeking dairy alternatives without compromising taste or functionality. The rapid expansion of quick-service restaurant chains offering plant-based menu options further strengthens demand, while established cold-chain logistics ensure efficient nationwide distribution. Increasing health awareness and demand for clean-label formulations continue to support premium product penetration across the region.

Europe

Europe accounts for nearly 29% of global market share, with key contributions from Germany, the United Kingdom, France, and the Netherlands. Regional growth is strongly influenced by stringent sustainability regulations, carbon reduction goals, and consumer preference for ethically sourced food products. Government support for plant-based innovation and heightened environmental awareness are accelerating vegan cheese adoption across Western Europe. Premiumization remains a defining market characteristic, with consumers favoring organic, clean-label, and artisanal offerings. Well-established specialty retail networks and strong culinary traditions incorporating cheese into daily diets further sustain demand. Additionally, increasing lactose intolerance awareness and dietary diversification are expanding the consumer base for dairy alternatives throughout the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations across China, India, Japan, and South Korea. Regional growth is supported by the proliferation of international quick-service restaurant chains and growing exposure to Western dietary habits among younger consumers. Processed cheese consumption is increasing significantly due to its affordability and compatibility with fast food and packaged meals. Vegan cheese demand is gaining momentum among urban millennials and Gen Z consumers influenced by global health and sustainability trends. Expansion of modern retail formats, e-commerce grocery platforms, and localized product innovation tailored to regional taste preferences are further accelerating market penetration.

Latin America

Latin America is experiencing steady market expansion, led by Brazil and Mexico, where rising urban populations and improving retail infrastructure are driving packaged food consumption. Regional growth is supported by increasing supermarket penetration, expanding cold storage capacity, and rising demand for affordable convenience foods. Processed cheese products remain widely consumed due to their price accessibility and versatility in traditional cuisines. Vegan cheese adoption is gradually increasing as health awareness improves and international brands introduce plant-based options adapted to local flavor preferences. Economic development and modernization of foodservice sectors are expected to further strengthen long-term market growth.

Middle East & Africa

The Middle East & Africa region is witnessing emerging growth opportunities supported by expanding hospitality industries, tourism development, and rising demand for premium imported food products. Countries such as the United Arab Emirates and Saudi Arabia are driving regional demand through rapid restaurant expansion and strong consumer spending on international cuisines. Growth drivers include increasing expatriate populations, modern retail expansion, and growing interest in health-oriented food alternatives. In Africa, South Africa leads market consumption due to retail modernization, urbanization, and the expansion of organized foodservice sectors. Improving cold-chain infrastructure and increasing availability of packaged foods are expected to enhance market accessibility across the broader region in the coming years.

Key Players in the Vegan Cheese and Processed Cheese Market

- Nestlé S.A.

- Danone S.A.

- Lactalis Group

- Kraft Heinz Company

- Arla Foods amba

- Bel Group

- Saputo Inc.

- Fonterra Co-operative Group

- Daiya Foods Inc.

- Violife Foods

- Miyoko’s Creamery

- Follow Your Heart

- Kerry Group plc

- FrieslandCampina

- Savencia Fromage & Dairy