Vector Control Market Size

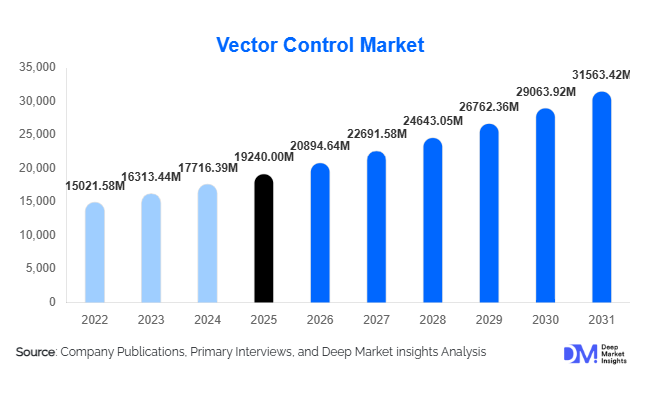

According to Deep Market Insights, the global vector control market size was valued at USD 19,240 million in 2025 and is projected to grow from USD 20,894.64 million in 2026 to reach USD 31,563.42 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). Market growth is primarily driven by the rising prevalence of vector-borne diseases, increasing government investments in preventive public health programs, and the adoption of integrated pest and disease management strategies worldwide. Climate change, rapid urbanization, and expanding mosquito habitats are further accelerating demand for vector monitoring, chemical control solutions, and biological interventions across both developed and emerging economies.

Key Market Insights

- Mosquito control accounts for the largest revenue share globally, supported by malaria and dengue prevention programs funded by governments and international health organizations.

- Government and municipal authorities dominate procurement, representing over half of global demand through long-term public health contracts.

- Asia-Pacific leads global consumption, driven by tropical climate conditions, dense urban populations, and expanding disease-control initiatives.

- Biological vector control solutions are the fastest-growing category, supported by environmental regulations and resistance to chemical insecticides.

- Smart surveillance technologies including AI-based monitoring and IoT-enabled traps are transforming operational efficiency.

- Integrated vector management approaches combining chemical, biological, and mechanical methods are becoming industry standards.

What are the latest trends in the vector control market?

Shift Toward Sustainable and Biological Control Solutions

Environmental concerns and increasing insecticide resistance are accelerating the adoption of biological vector control methods. Governments and regulatory bodies are promoting bacterial larvicides, sterile insect techniques, and Wolbachia-based mosquito suppression programs as environmentally safer alternatives to traditional chemicals. These solutions reduce ecological impact while maintaining long-term effectiveness, encouraging public health agencies to transition toward integrated vector management frameworks. Biotechnology companies are investing heavily in next-generation biological formulations that deliver targeted control while minimizing non-target species exposure, positioning sustainability as a central industry trend.

Digital Surveillance and Predictive Vector Monitoring

Technology integration is reshaping vector control operations worldwide. AI-driven surveillance platforms, satellite mapping, and IoT-connected traps enable real-time monitoring of vector populations and disease risk zones. Municipal authorities are increasingly adopting predictive analytics to optimize spraying schedules and allocate resources efficiently. Smart city initiatives in Asia-Pacific and the Middle East are integrating vector monitoring into urban infrastructure management systems. These digital solutions reduce operational costs while improving outbreak response times, creating a shift from reactive pest management toward preventive disease intelligence systems.

What are the key drivers in the vector control market?

Rising Incidence of Vector-Borne Diseases

Increasing outbreaks of malaria, dengue, chikungunya, West Nile virus, and Lyme disease are driving sustained investments in vector control programs. Climate variability has expanded mosquito and tick habitats into new geographic areas, forcing governments to strengthen surveillance and prevention initiatives. Public health authorities increasingly recognize vector control as a cost-effective preventive strategy compared with disease treatment, resulting in higher annual procurement budgets globally.

Rapid Urbanization and Infrastructure Expansion

Urban population growth across developing economies creates favorable breeding conditions for disease vectors due to water stagnation, waste accumulation, and dense living environments. Cities across India, Southeast Asia, and Africa are implementing continuous vector management programs involving fogging operations, larval source reduction, and environmental sanitation. Urban infrastructure development projects now routinely include pest and vector management planning, expanding long-term demand.

What are the restraints for the global market?

Regulatory Restrictions on Chemical Insecticides

Strict environmental and safety regulations in North America and Europe limit the use of certain chemical insecticides. Lengthy approval processes and compliance costs increase product development timelines, affecting profitability and slowing commercialization of new formulations.

Growing Insecticide Resistance

Repeated chemical usage has resulted in resistance among mosquito populations, reducing treatment effectiveness and necessitating continuous innovation. Manufacturers must invest significantly in research and resistance-management solutions, increasing operational costs for industry participants.

What are the key opportunities in the vector control industry?

Expansion of Government Disease Prevention Programs

Global health initiatives aimed at malaria elimination and dengue reduction present major opportunities for market participants. Governments are increasing funding allocations toward preventive healthcare infrastructure, creating large-scale procurement opportunities for insecticides, surveillance equipment, and integrated control services. Long-term contracts provide stable revenue streams for companies capable of delivering comprehensive solutions.

Smart and Integrated Vector Management Platforms

The convergence of data analytics, automation, and biological control technologies is creating opportunities for solution providers offering end-to-end vector management platforms. Companies integrating monitoring hardware, analytics software, and treatment solutions can establish recurring revenue models while improving operational efficiency for municipal clients. Smart-city deployments are expected to accelerate adoption globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 19240 Million |

| Market Size in 2026 | USD 20894.64 Million |

| Market Size in 2031 | USD 31563.42 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Vector Type Insights

Mosquito control continues to dominate the global vector control market, accounting for nearly 58% of total market revenue in 2025, primarily supported by extensive malaria, dengue, chikungunya, and Zika prevention programs implemented across developing and tropical economies. The leading position of mosquito control is driven by the high global disease burden, continuous government funding, and the need for large-scale preventive interventions in densely populated urban regions. Increasing climate variability and expanding mosquito habitats have further intensified demand for integrated mosquito management solutions, including larval source management, spraying programs, and community-based prevention strategies.Tick control is witnessing accelerated expansion, particularly in North America and Europe, as the incidence of tick-borne diseases such as Lyme disease and Rocky Mountain spotted fever rises across temperate climates. Growth in this segment is primarily supported by increasing outdoor recreational activities, expanding wildlife populations, and improved disease surveillance systems. Rodent and fly control remain essential components of urban sanitation and industrial hygiene programs, especially in food processing, warehousing, and municipal waste management environments. Growing awareness regarding zoonotic disease transmission and cross-species infection risks is encouraging diversified vector management strategies, strengthening demand across multiple vector categories globally.

Control Method Insights

Chemical control methods hold the leading position with approximately 48% market share, primarily driven by their rapid effectiveness, scalability, and suitability for emergency outbreak response. The leading segment driver is the ability of chemical solutions to deliver immediate population reduction during disease outbreaks, making them indispensable for public health authorities managing large-scale infestations. Governments continue to rely on insecticide spraying and residual treatments due to established regulatory approvals and cost efficiency in mass deployment programs.Biological control solutions are experiencing the fastest growth as environmental concerns and regulatory pressures encourage adoption of sustainable alternatives. The increasing use of microbial larvicides, natural predators, and environmentally friendly formulations reflects the shift toward integrated pest management frameworks. Mechanical and physical control methods, including trapping systems, habitat modification, and environmental sanitation, are increasingly integrated into preventive programs to reduce chemical dependence. Genetic control technologies remain an emerging segment but are gaining attention through pilot initiatives focused on mosquito population suppression and long-term ecological management strategies.

Product Type Insights

Insecticides represent the largest product category, contributing about 42% of global revenue, supported by strong government procurement programs and widespread adoption in emergency vector suppression campaigns. The leading segment driver is the high operational efficiency and immediate action provided by insecticides in controlling disease-carrying vectors across large geographic areas. Continued innovation in formulation technologies, including longer residual effects and reduced toxicity profiles, is further sustaining segment dominance.Larvicides are gaining significant adoption as preventive solutions targeting breeding stages rather than adult vectors, enabling cost-effective long-term population management. Increasing emphasis on proactive disease prevention strategies is accelerating larvicide deployment in urban drainage systems and stagnant water zones. Demand for fogging and spraying equipment is rising alongside expanding urban vector management initiatives, while surveillance and monitoring systems are emerging as high-value segments driven by digital technologies, real-time data analytics, and smart public health infrastructure investments.

Application Insights

Public health programs dominate applications with nearly 46% market share, reflecting the central role of government-led disease prevention initiatives worldwide. The leading segment driver is sustained public sector investment aimed at reducing healthcare burdens associated with vector-borne diseases, particularly in emerging economies. National eradication campaigns, seasonal spraying operations, and community awareness initiatives continue to strengthen this application segment.Commercial pest management services are expanding steadily across hospitality, logistics, retail, and food processing industries where hygiene compliance and regulatory adherence are critical operational requirements. Residential vector control demand is also increasing due to rising consumer awareness, urban population growth, and the availability of accessible retail repellents, home protection solutions, and preventive treatment services. Growing concerns regarding indoor health safety and lifestyle-related hygiene standards are further supporting market expansion across non-government applications.

End-Use Insights

Government and municipal authorities account for approximately 51% of global demand, making them the largest end users in the vector control market. The leading segment driver is large-scale public funding directed toward national disease surveillance, prevention campaigns, and emergency outbreak response programs. Municipal sanitation initiatives and urban health management strategies continue to sustain strong procurement volumes across regions.Pest control service providers represent a rapidly growing segment as outsourcing becomes increasingly common among commercial facilities seeking professional and compliant vector management solutions. Agriculture and livestock farms are expanding adoption of vector control practices to prevent productivity losses caused by pest-borne diseases affecting crops and animals. Healthcare facilities and hospitality infrastructure are emerging as fast-growing end users driven by stricter sanitation regulations, infection prevention standards, and rising expectations for safe public environments.

Explore more data points, trends and opportunities Download Free Sample Report

Vector Control Market Segmentations

By Vector Type

- Mosquito Control

- Rodent Control

- Tick Control

- Fly Control

- Flea Control

- Other Disease Vectors

By Control Method

- Chemical Control

- Biological Control

- Mechanical & Physical Control

- Genetic Control Technologies

By Product Type

- Insecticides

- Larvicides

- Rodenticides

- Repellents

- Fogging & Spraying Equipment

- Monitoring & Surveillance Systems

By Application

- Public Health Programs

- Commercial Pest Management

- Residential Vector Control

- Agriculture & Livestock Protection

- Industrial & Institutional Facilities

By End User

- Government & Municipal Authorities

- Pest Control Service Providers

- Agriculture & Livestock Farms

- Residential Consumers

- Hospitality & Commercial Infrastructure

- Healthcare Facilities

By Distribution Channel

- Direct Government Procurement

- Professional Pest Control Contracts

- Retail & Consumer Sales

- Institutional Supply Agreements

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global vector control market at approximately 38% in 2025. Countries such as India, China, Indonesia, and Thailand drive demand due to high disease prevalence and expanding public health programs. India alone contributes nearly 11% of global demand supported by nationwide vector-borne disease control initiatives. Regional growth is primarily driven by rapid urbanization, population density expansion, tropical and subtropical climatic conditions, and increasing government healthcare expenditure. Rising incidence of dengue and malaria outbreaks, infrastructure development in peri-urban areas, and expanding awareness campaigns are accelerating adoption of integrated vector management solutions. Additionally, improving municipal sanitation systems and growing investments in smart surveillance technologies are strengthening long-term market growth across the region, making Asia-Pacific the fastest-growing market with CAGR exceeding 10%.

North America

North America accounts for around 22% market share, led by the United States. Regional growth is supported by increasing prevalence of tick-borne diseases, periodic West Nile virus outbreaks, and heightened public awareness regarding vector-related health risks. Strong municipal mosquito abatement programs, advanced monitoring technologies, and data-driven surveillance systems are key growth drivers. Favorable regulatory frameworks encouraging environmentally safe products, along with rising investments in biological control solutions and professional pest management services, continue to strengthen market expansion across urban and suburban areas.

Europe

Europe represents nearly 18% of global demand, driven by France, Germany, Italy, and Spain. Regional growth is primarily influenced by climate change-induced expansion of mosquito habitats across southern and central Europe, leading to increased preventive control measures. Stringent environmental regulations are encouraging adoption of biological and low-toxicity vector control solutions aligned with sustainability objectives. Government-supported monitoring programs, cross-border disease surveillance initiatives, and increasing urban green spaces requiring pest management are further contributing to market development across the region.

Latin America

Latin America contributes about 8% of the global market, with Brazil and Mexico leading regional demand. Growth in the region is driven by frequent dengue, Zika, and chikungunya outbreaks that necessitate continuous vector control interventions. Expanding urban populations, improving public sanitation programs, and increased government spending on preventive healthcare campaigns are strengthening regional adoption. International collaboration programs and public-private partnerships focused on disease control infrastructure development also play a significant role in sustaining long-term market expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 14% of market share, supported by extensive malaria eradication initiatives across Sub-Saharan Africa. Regional growth is driven by international funding support, rising healthcare investments, and large-scale distribution of insecticides and mosquito control solutions. Gulf countries are investing in smart-city surveillance systems and advanced pest monitoring technologies to maintain public health standards in rapidly urbanizing environments. Increasing awareness programs, humanitarian health initiatives, and expanding infrastructure development projects continue to support sustained demand for vector control solutions across both urban and rural areas.

Key Players in the Vector Control Market

- BASF SE

- Bayer AG

- Syngenta Group

- Sumitomo Chemical Co., Ltd.

- Rentokil Initial plc

- Ecolab Inc.

- FMC Corporation

- Corteva Agriscience

- Rollins Inc.

- Anticimex Group

- Bell Laboratories Inc.

- PelGar International

- Central Garden & Pet Company

- Clarke Environmental Mosquito Management

- ADAMA Agricultural Solutions