Tomato Puree Market Size

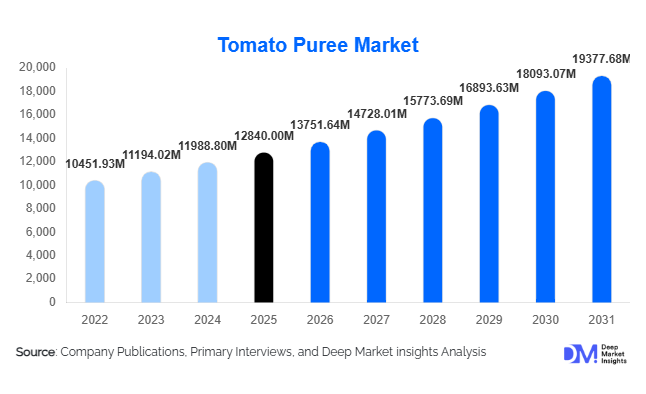

According to Deep Market Insights, the global tomato puree market size was valued at USD 12,840 million in 2025 and is projected to grow from USD 13,751.64 million in 2026 to reach approximately USD 19,377.68 million by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). Growth in the tomato puree market is primarily supported by rising consumption of processed foods, expanding quick-service restaurant (QSR) networks, and increasing demand for convenient cooking ingredients across both developed and emerging economies.

Tomato puree serves as a foundational ingredient across multiple food applications including sauces, soups, ready meals, bakery fillings, and packaged culinary products. Urbanization, rising dual-income households, and changing dietary habits have significantly increased reliance on packaged and semi-processed foods, strengthening global demand. Additionally, consumers are increasingly favoring natural and clean-label ingredients, positioning tomato puree as a preferred alternative to artificial flavor bases. Rapid growth of foodservice chains and expansion of global cuisines—particularly Italian and Mediterranean foods—are further accelerating adoption.

Key Market Insights

- Convenience food consumption is accelerating globally, increasing industrial demand for standardized tomato puree formulations.

- Asia-Pacific represents the fastest-growing production and consumption hub, supported by expanding urban populations and processed food penetration.

- Foodservice and QSR expansion continues to drive bulk procurement of tomato puree worldwide.

- Clean-label and preservative-free formulations are reshaping product innovation strategies among manufacturers.

- Technological improvements in aseptic packaging are extending shelf life and enabling global exports.

- Private-label brands are increasing competitive pricing pressure across retail channels.

What are the latest trends in the tomato puree market?

Clean-Label and Organic Product Expansion

Consumers are increasingly demanding transparency in food ingredients, encouraging manufacturers to develop organic, non-GMO, and additive-free tomato puree products. Retailers are allocating greater shelf space to premium and natural variants, particularly in North America and Europe. Organic tomato cultivation is expanding in regions such as Italy, Spain, and California, enabling producers to command higher margins while aligning with sustainability expectations. Clean-label positioning has also strengthened brand differentiation in private-label dominated retail environments.

Growth of Aseptic and Bulk Packaging Solutions

Aseptic packaging technologies are transforming supply chains by enabling extended shelf life without preservatives. Industrial buyers increasingly prefer bag-in-drum and bulk aseptic formats that reduce transportation costs and improve storage efficiency. These packaging formats support global exports from processing hubs such as China, the U.S., and Mediterranean countries. The shift toward bulk packaging is particularly evident among foodservice operators and ready-meal manufacturers seeking consistent ingredient quality.

What are the key drivers in the tomato puree market?

Expansion of Processed and Convenience Foods

The rapid growth of ready-to-eat meals, frozen foods, and packaged sauces has significantly increased demand for tomato puree as a base ingredient. Urban lifestyles and reduced cooking time availability have pushed consumers toward convenience-oriented food products. Manufacturers rely on tomato puree for flavor consistency, color stability, and nutritional value, making it indispensable in large-scale food production.

Global Growth of Quick-Service Restaurants

The proliferation of pizza chains, burger outlets, and casual dining restaurants worldwide has boosted demand for tomato-based ingredients. Tomato puree is extensively used in pizza sauces, pasta bases, dips, and marinades. Emerging economies such as India, Indonesia, and Brazil are witnessing rapid QSR expansion, creating sustained institutional demand.

Rising Export-Oriented Processing Industries

Major producing countries including China, the United States, Italy, and Spain are expanding processing capacities aimed at exports. Favorable agricultural mechanization and large-scale tomato farming enable cost-efficient production. Export-driven demand stabilizes pricing cycles and supports long-term market expansion.

What are the restraints for the global market?

Volatility in Raw Tomato Prices

Tomato puree production is highly dependent on agricultural yields, making the market vulnerable to weather variability, water scarcity, and crop diseases. Price fluctuations directly affect processor margins and contract pricing with food manufacturers.

High Energy and Processing Costs

Tomato processing requires intensive heating, evaporation, and packaging operations, resulting in significant energy consumption. Rising fuel and electricity prices in Europe and parts of Asia have increased operational expenses, challenging profitability for small and mid-scale processors.

What are the key opportunities in the tomato puree industry?

Emerging Market Consumption Growth

Rapid urbanization across Asia-Pacific and Africa is creating strong demand for packaged cooking ingredients. Rising middle-class populations are adopting westernized diets involving pasta sauces, ready curries, and fusion foods. Manufacturers expanding localized production facilities in India and Southeast Asia can significantly reduce logistics costs while capturing high-growth demand.

Premiumization and Functional Food Applications

Fortified tomato puree enriched with antioxidants such as lycopene is gaining traction within health-conscious consumer segments. Functional food manufacturers are exploring tomato-based formulations emphasizing heart health and immunity benefits. Premium positioning allows brands to improve margins while diversifying beyond commodity pricing structures.

Technological Integration in Processing

Automation, AI-based quality inspection, and energy-efficient evaporators are improving production yields and reducing waste. Companies investing in advanced processing technologies can enhance product consistency and reduce long-term CapEx costs, creating competitive advantages for large-scale producers.

Product Type Insights

The global tomato puree market demonstrates a well-established product segmentation structure shaped by industrial demand patterns, consumer purchasing behavior, agricultural supply dynamics, and evolving food processing technologies. Among all product categories, conventional tomato puree continues to dominate the global landscape, accounting for approximately 68% of the total market share in 2025. This dominance is primarily driven by its cost competitiveness, widespread availability, and compatibility with large-scale food manufacturing processes. Conventional puree is extensively utilized by food processors due to standardized quality parameters, stable pricing structures, and reliable year-round supply enabled through advanced preservation and storage techniques. Manufacturers operating in high-volume categories such as sauces, ready meals, frozen foods, and institutional catering prefer conventional puree because it ensures consistency in flavor, color, and texture while maintaining operational efficiency.The leading growth driver supporting this segment is the expanding global processed food industry, which requires scalable and economical ingredients capable of supporting mass production. Industrial buyers prioritize affordability and supply security, making conventional tomato puree the preferred raw material across multinational food manufacturing operations. Additionally, improvements in hybrid tomato cultivation, mechanized harvesting, and processing automation have reduced production costs, further reinforcing the segment’s leadership position.While conventional products dominate volume consumption, organic tomato puree is emerging as one of the fastest-growing product categories globally. Rising consumer awareness regarding pesticide residues, sustainability, and clean-label food products has significantly accelerated demand for organic variants, particularly in developed economies. Consumers increasingly associate organic food with higher nutritional value and environmental responsibility, encouraging retailers and food brands to expand certified organic product lines. Growth in organic puree is also supported by regulatory initiatives promoting sustainable agriculture, along with premiumization trends in retail food markets.Another important category, double-concentrated tomato puree, maintains strong demand within industrial applications due to its superior cost efficiency in logistics and storage. Higher solid content reduces transportation weight and packaging requirements, enabling manufacturers to optimize supply chain expenses.

Application Insights

Application segmentation highlights the central role of tomato puree as a foundational ingredient within global food systems. The sauces and condiments segment represents the leading application category, contributing nearly 42% of total market demand in 2025. Tomato puree serves as the essential base ingredient for pasta sauces, pizza sauces, ketchup, marinades, dips, and cooking sauces across both household and industrial food preparation. The primary driver supporting this segment’s dominance is the rapid globalization of Western and fusion cuisines, which has significantly increased consumption of tomato-based sauces across emerging economies.The expansion of quick-service restaurants (QSRs), casual dining chains, and cloud kitchens has further strengthened demand for standardized sauce ingredients. Foodservice operators rely heavily on tomato puree to ensure uniform taste profiles across multiple locations. Additionally, increasing urbanization and busy lifestyles are encouraging consumers to adopt ready-to-use cooking bases, further accelerating the use of puree in condiment manufacturing.Beyond sauces, ready meals and soups represent one of the fastest-growing application areas. The growth driver for this segment lies in rising demand for convenience foods driven by dual-income households, time-constrained consumers, and expanding retail penetration of frozen and packaged meals. Tomato puree enhances flavor complexity, nutritional value, and visual appeal in ready-to-eat products, making it indispensable for manufacturers seeking clean-label ingredient solutions.Snack foods and processed meat products also increasingly incorporate tomato puree as a flavoring and coloring agent, reflecting innovation in processed food formulations. Furthermore, the expansion of plant-based food alternatives has opened new application opportunities, as tomato-based ingredients complement vegetarian and vegan product formulations by delivering natural umami flavor profiles.As global food consumption shifts toward convenience, consistency, and international cuisine adoption, application demand for tomato puree continues diversifying, reinforcing its status as a multifunctional ingredient across food categories.

Distribution Channel Insights

Distribution channel dynamics within the tomato puree market are strongly influenced by industrial procurement patterns and evolving retail consumption habits. B2B industrial sales dominate the global distribution landscape, accounting for approximately 61% of total market share. The leading driver behind this segment is the extensive reliance of food processing companies on bulk ingredient sourcing. Large manufacturers purchase tomato puree in drums, aseptic bags, and bulk containers to support continuous production cycles for sauces, canned foods, ready meals, and institutional catering products.Long-term supply contracts between processors and food manufacturers provide price stability and supply assurance, strengthening the dominance of industrial channels. Additionally, globalization of food brands has increased cross-border ingredient sourcing, enabling exporters to establish strong relationships with multinational buyers.Retail distribution channels, including supermarkets, hypermarkets, and online platforms, are expanding steadily as consumer cooking habits evolve. Increased interest in home cooking, influenced by health awareness and culinary experimentation, has supported retail sales of tomato puree products. Private-label offerings introduced by major retailers have also improved product affordability, attracting price-sensitive consumers while expanding shelf presence.E-commerce platforms are emerging as an important growth contributor, particularly in urban markets where digital grocery adoption continues rising. Online retail allows brands to introduce specialty formats such as organic, gourmet, or regionally flavored tomato purees, targeting niche consumer segments. Subscription-based grocery delivery services further enhance repeat purchases, strengthening long-term retail demand.The coexistence of strong industrial procurement and expanding retail accessibility ensures balanced distribution growth, with B2B channels driving volume while retail channels contribute value expansion.

Packaging Type Insights

Packaging innovation plays a critical role in preserving product quality, improving logistics efficiency, and enhancing consumer convenience within the tomato puree market. Aseptic packaging formats lead globally, accounting for approximately 55% of market share. The primary growth driver for this segment is extended shelf life without refrigeration, which significantly reduces storage and transportation costs while maintaining product freshness and safety.Aseptic packaging is particularly advantageous for international trade, allowing exporters to ship large volumes across long distances while minimizing spoilage risk. Industrial buyers favor aseptic bags and containers because they support bulk handling and automated processing systems. Additionally, sustainability considerations are encouraging manufacturers to adopt lightweight packaging solutions that reduce carbon emissions associated with logistics.Canned packaging remains widely used in retail markets due to durability, familiarity, and strong product protection. Metal cans provide long shelf life and resistance to contamination, making them suitable for regions with limited cold-chain infrastructure. Consumer trust in canned foods continues supporting stable demand in both developed and developing markets.Meanwhile, flexible pouches are gaining traction as a fast-growing packaging format driven by convenience and cost efficiency. Lightweight materials reduce packaging waste and shipping expenses, aligning with sustainability goals adopted by food brands and retailers. Resealable pouch designs also enhance usability for households, contributing to increased consumer preference.Overall, packaging trends reflect the industry’s shift toward efficiency, sustainability, and consumer convenience, with aseptic technology remaining the dominant solution for global trade and industrial applications.

End-Use Industry Insights

The tomato puree market serves a diverse range of end-use industries, each contributing to overall demand expansion through distinct consumption patterns. Food processing manufacturers account for nearly 48% of total global demand, making this the leading end-use segment. The primary driver supporting this leadership is the rapid growth of processed and packaged food production worldwide. Manufacturers rely on tomato puree as a standardized base ingredient that simplifies formulation while ensuring flavor consistency across large product portfolios.Global food brands continue expanding production capacities to meet rising demand for ready-to-eat meals, sauces, and frozen foods, directly increasing procurement volumes of tomato puree. Automation in food processing facilities further enhances ingredient utilization efficiency, reinforcing long-term demand stability.The foodservice industry represents a rapidly expanding end-use category fueled by the globalization of restaurant chains, quick-service outlets, and delivery-focused dining models. Restaurants depend on tomato puree for menu staples such as pizzas, pasta dishes, curries, and sauces, making it a critical ingredient within commercial kitchens. Growth in tourism, urbanization, and digital food delivery platforms continues accelerating foodservice consumption worldwide.Institutional catering, including schools, hospitals, and corporate cafeterias, also contributes steadily to market demand due to the ingredient’s versatility and cost-effectiveness. As large-scale meal preparation expands globally, tomato puree remains an essential component in institutional food production.

| By Product Type | By Packaging Type | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 24% of the global tomato puree market share in 2025, supported by highly advanced agricultural systems and sophisticated food processing infrastructure. The United States leads regional production, particularly through large-scale tomato cultivation concentrated in California, where favorable climatic conditions and mechanized farming enable high productivity. A major growth driver in North America is the strong consumption of packaged foods, including pasta sauces, frozen meals, canned products, and ready-to-cook meal kits.The region benefits from mature retail networks and high penetration of convenience foods, driven by busy consumer lifestyles and widespread adoption of quick meal solutions. Continuous innovation in flavor varieties and premium product positioning further stimulates retail demand. Additionally, technological advancements in processing efficiency and supply chain logistics support consistent product availability.Canada contributes steady growth through expanding private-label brands and increasing consumer preference for home cooking ingredients. Rising demand for organic and clean-label foods also supports diversification within the regional market. Sustainability initiatives, including water-efficient farming and waste reduction practices, are increasingly influencing production strategies across North America.

Europe

Europe holds nearly 27% of the global market share, making it one of the most influential regions in tomato puree production and export. Countries such as Italy and Spain serve as major cultivation and processing hubs, benefiting from Mediterranean climates ideal for tomato farming. A key driver of regional growth is Europe’s strong culinary heritage centered around tomato-based cuisine, which sustains consistent domestic consumption.Italian tomato puree enjoys global recognition for quality and authenticity, strengthening export demand across international markets. Meanwhile, Germany and France remain significant import markets due to high consumption of processed foods and ready-made sauces. European Union policies promoting sustainable agriculture and traceability standards are encouraging producers to adopt environmentally responsible farming practices.Increasing consumer interest in organic foods and premium culinary ingredients further drives market expansion. Additionally, investments in advanced processing technologies and geographical indication certifications enhance product differentiation, allowing European producers to maintain competitive advantages in global trade.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market globally, driven by rapid urbanization, population growth, and evolving dietary habits. China plays a dual role as both a major exporter and processor, supported by large-scale manufacturing capacity and cost-efficient production systems. Export-oriented production allows Chinese suppliers to serve global food manufacturers competitively.India is emerging as a significant growth engine due to rising consumption of packaged foods and expansion of quick-service restaurant chains across urban centers. Increasing disposable income, changing lifestyles, and growing acceptance of Western cuisine are accelerating demand for tomato-based sauces and cooking ingredients. Government initiatives supporting food processing industries also encourage domestic production expansion.Japan and South Korea maintain stable demand characterized by preference for premium-quality packaged foods. Innovation in convenience meals and ready-to-use cooking solutions further strengthens regional consumption patterns. The rapid growth of e-commerce grocery platforms across Asia-Pacific also enhances product accessibility, contributing to sustained market expansion.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth driven primarily by rising reliance on imported processed food ingredients. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are witnessing increasing demand for tomato puree due to expanding foodservice industries and growing urban populations. Limited domestic tomato processing capacity acts as a major driver for imports from Europe and Asia.Population growth, tourism expansion, and increasing penetration of international restaurant chains are strengthening consumption of tomato-based sauces and prepared foods. Additionally, government investments in food security initiatives encourage diversification of food supply sources, supporting long-term import demand. Retail modernization and supermarket expansion across major cities further enhance product availability.

Latin America

Latin America demonstrates steady market development led by Brazil and Mexico, where expanding fast-food industries and rising processed food consumption drive demand for tomato puree. Urbanization and changing dietary preferences are encouraging adoption of convenience foods, increasing ingredient utilization within food manufacturing.Export-oriented agricultural production is also expanding in countries such as Chile and Peru, supported by favorable climatic conditions and improving processing infrastructure. Regional trade agreements facilitate cross-border distribution, strengthening export competitiveness. Increasing investments in food processing facilities and modernization of agricultural practices continue supporting long-term market growth across Latin America.Across all regions, growth patterns are shaped by a combination of agricultural capacity, processed food demand, retail expansion, and evolving consumer preferences, positioning tomato puree as a critical ingredient within the global food supply chain.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Tomato Puree Market

- The Morning Star Company

- Kagome Co., Ltd.

- COFCO Tunhe Tomato Co., Ltd.

- Conagra Brands, Inc.

- Kraft Heinz Company

- Mutti S.p.A.

- Del Monte Foods, Inc.

- Olam Food Ingredients

- Ingomar Packing Company

- Los Gatos Tomato Products

- Neil Jones Food Company

- TomaTek Inc.

- Sugal Group

- Chalkis Health Industry Co., Ltd.

- Ariza B.V.