Tomato Paste Market Size

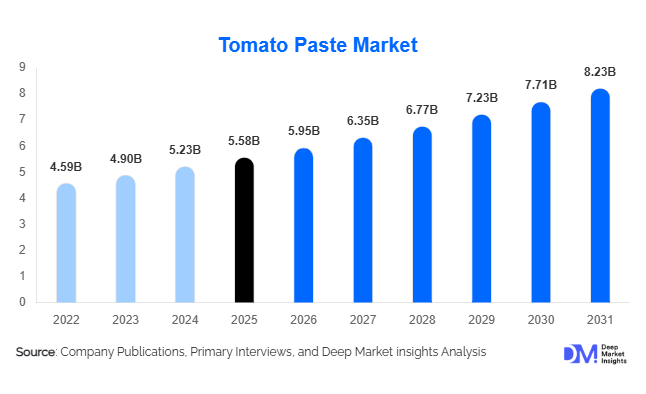

According to Deep Market Insights, the global tomato paste market size was valued at USD 5.58 billion in 2025 and is projected to grow from USD 5.95 billion in 2026 to reach USD 8.23 billion by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The tomato paste market growth is primarily driven by the increasing consumption of processed and convenience foods, rising demand from the global foodservice industry, and the expanding use of tomato-based ingredients across sauces, soups, frozen foods, and ready-to-eat meal applications.

Key Market Insights

- Industrial food processing continues to dominate tomato paste demand globally, with manufacturers increasingly utilizing concentrated tomato ingredients in sauces, soups, snacks, and frozen meal production.

- Aseptic packaging technologies are transforming international tomato paste trade, enabling longer shelf life, reduced contamination risk, and cost-efficient bulk transportation.

- Europe dominates the global tomato paste market, supported by strong production and export capabilities in Italy, Spain, and Portugal.

- Asia-Pacific remains the fastest-growing regional market, driven by rising processed food consumption and rapid urbanization in China, India, and Southeast Asia.

- Organic and clean-label tomato paste products are witnessing accelerated adoption, particularly in North America and Western Europe where health-conscious consumer demand is increasing.

- Technological advancements in evaporation systems, automation, and water recycling are improving production efficiency and sustainability across major processing facilities worldwide.

tomato paste market latest trends

Rising Demand for Organic and Clean-Label Tomato Paste

Consumers are increasingly seeking preservative-free, non-GMO, and organic tomato paste products as awareness surrounding food ingredients and health impacts continues to rise globally. This trend is especially prominent across Europe and North America, where clean-label food purchasing behavior has become mainstream. Manufacturers are responding by introducing low-sodium, additive-free, and sustainably sourced tomato paste variants targeted toward retail consumers and premium foodservice operators. Organic certifications, farm traceability, and environmentally responsible farming practices are becoming important competitive differentiators. In addition, retailers are expanding shelf space dedicated to premium tomato-based products, further accelerating clean-label product adoption. Food manufacturers are also reformulating processed foods using natural tomato concentrates to replace artificial flavoring and coloring agents, strengthening long-term demand for premium tomato paste solutions.

Expansion of Aseptic and Bulk Packaging Technologies

The global tomato paste industry is increasingly shifting toward aseptic packaging systems to improve export efficiency and extend product shelf life. Large industrial buyers prefer aseptic drums and bag-in-box packaging formats due to their convenience in transportation, reduced spoilage risk, and improved storage capabilities. This trend is particularly strong among multinational food manufacturers operating across global supply chains. Advanced aseptic processing technologies are enabling processors to preserve product consistency while minimizing the need for preservatives. At the same time, manufacturers are investing in automated filling systems, smart packaging technologies, and recyclable industrial containers to improve operational efficiency and sustainability. The growing globalization of food ingredient trade is expected to further strengthen demand for bulk packaging innovations within the tomato paste market.

tomato paste market drivers

Growth of the Global Processed Food Industry

The rapid expansion of the processed food sector remains one of the most important growth drivers for the tomato paste market. Tomato paste serves as a foundational ingredient in sauces, soups, frozen meals, ready-to-eat foods, snacks, and condiments. Increasing urbanization, changing dietary habits, and growing consumer preference for convenience foods are significantly boosting industrial demand. Fast-food chains and multinational foodservice operators continue to expand globally, particularly across emerging economies in Asia-Pacific and the Middle East, creating sustained procurement demand for concentrated tomato products. In addition, packaged food manufacturers are increasingly relying on tomato paste for flavor enhancement, natural coloring, and formulation consistency, further strengthening market expansion.

Increasing Demand from Foodservice and HoReCa Industries

The global expansion of restaurants, hotels, catering services, and institutional kitchens is accelerating tomato paste consumption worldwide. Foodservice operators prefer concentrated tomato paste products because they reduce preparation time, minimize storage requirements, and ensure flavor consistency across large-scale cooking operations. Pizza chains, quick-service restaurants, and catering businesses remain major consumers of double and triple concentrated tomato paste. Tourism growth and the continued recovery of hospitality industries are further supporting market expansion. In addition, rising demand for international cuisines such as Italian, Mediterranean, and Mexican food is increasing tomato paste utilization in commercial kitchens globally.

global market restraints

Volatility in Raw Tomato Prices

Tomato paste manufacturing is highly dependent on agricultural output, making the industry vulnerable to fluctuations in fresh tomato prices. Climatic disruptions such as droughts, excessive rainfall, heatwaves, and crop diseases can significantly impact tomato yields and processing volumes. Major production regions including California, Southern Europe, and parts of China have experienced periodic supply instability in recent years due to changing climate conditions. Such volatility increases procurement costs for processors and impacts profitability margins, particularly for companies operating under long-term supply contracts with food manufacturers and retail chains.

High Energy Consumption and Logistics Costs

The tomato paste industry relies heavily on energy-intensive evaporation and sterilization processes, resulting in substantial operational costs. Rising global energy prices and freight charges continue to pressure manufacturing margins, especially for export-oriented processors. Transportation expenses for bulk shipments, container shortages, and fluctuating fuel costs further impact international trade competitiveness. Additionally, environmental regulations related to water usage, emissions, and waste disposal are becoming increasingly stringent across major producing regions, requiring processors to invest in costly sustainability and compliance initiatives.

tomato paste industry key opportunities

Expansion in Emerging Processed Food Markets

Emerging economies such as India, Indonesia, Vietnam, Saudi Arabia, and several African nations present substantial growth opportunities for tomato paste manufacturers. Rapid urbanization, rising disposable income, and increasing consumption of packaged foods are expanding demand for sauces, ready meals, and convenience products that utilize tomato paste as a core ingredient. Governments in several developing countries are also supporting food processing industries through infrastructure investments, cold-chain expansion, and agro-processing incentives. Manufacturers establishing local processing and distribution networks in these high-growth markets are expected to benefit from rising domestic demand and lower transportation costs.

Technological Modernization and Sustainable Processing

The increasing adoption of automation, AI-driven quality inspection systems, and water recycling technologies is creating significant opportunities for processors to improve production efficiency and sustainability. Companies investing in energy-efficient evaporation systems and renewable energy integration are expected to reduce operational costs while strengthening environmental compliance. Sustainability-focused production models are also becoming important for export competitiveness, particularly in Europe and North America where buyers increasingly prioritize environmentally responsible sourcing. In addition, innovations in concentrated formulations and premium organic tomato products are enabling manufacturers to expand into higher-margin market segments.

Product Type Insights

Double concentrated tomato paste dominates the market, accounting for a significant share of global consumption due to its balanced consistency, cost-effectiveness, and extensive industrial application across sauces, soups, and ready meals. Triple concentrated tomato paste is gaining traction among foodservice operators and industrial food manufacturers because it reduces transportation and storage costs while delivering stronger flavor concentration. Organic tomato paste represents one of the fastest-growing segments, supported by rising consumer demand for clean-label and preservative-free food ingredients. Hot break tomato paste remains widely preferred for ketchup and sauce manufacturing because of its higher viscosity and improved texture stability, while cold break variants are increasingly utilized in products requiring fresher tomato flavor profiles.

Application Insights

Sauces and condiments remain the leading application segment within the tomato paste market, driven by strong global demand for pasta sauces, pizza sauces, ketchup, and cooking bases. Ready-to-eat meals and frozen foods are witnessing rapid growth as consumers increasingly prefer convenient meal solutions with longer shelf life. Soup and broth manufacturers continue to utilize tomato paste extensively for flavor enhancement and natural coloring properties. Processed meat products and snack seasonings are also emerging as important application areas. In addition, the increasing popularity of plant-based foods and clean-label packaged products is expanding tomato paste utilization across alternative protein and health-oriented food categories.

Distribution Channel Insights

Direct B2B sales dominate the tomato paste market as large food manufacturers and foodservice operators typically procure bulk quantities through long-term supply contracts. Industrial buyers prioritize consistent product quality, concentration standards, and reliable logistics support when selecting suppliers. Supermarkets and hypermarkets continue to represent the largest retail distribution channels for household tomato paste consumption, particularly in urban markets. Online retail platforms are gaining traction, driven by rising digital grocery adoption and growing demand for premium and organic tomato products. Specialty food stores are increasingly focusing on gourmet, imported, and organic tomato paste offerings to cater to health-conscious and premium consumers.

End-Use Industry Insights

The food processing industry represents the largest end-use segment for tomato paste globally, supported by increasing production of packaged foods, sauces, snacks, and frozen meals. Foodservice and HoReCa applications are among the fastest-growing segments due to the rapid expansion of quick-service restaurants, pizza chains, and institutional catering operations. Retail household consumption is steadily increasing as consumers seek convenient cooking ingredients and ready-to-use meal solutions. Industrial ingredient manufacturers also represent a significant consumer base, utilizing tomato paste in seasoning blends, processed foods, and customized formulations for multinational food brands.

Packaging Type Insights

Aseptic drums dominate industrial packaging applications within the tomato paste market because they provide extended shelf life, improved hygiene, and efficient transportation for export trade. Metal cans remain highly popular in retail applications due to their durability, affordability, and widespread consumer acceptance. Sachets and pouches are experiencing strong growth in emerging markets where single-use and low-cost packaging formats appeal to price-sensitive consumers. Glass jars are increasingly preferred for premium and organic tomato paste products as consumers associate glass packaging with freshness, sustainability, and higher product quality.

| By Product Type | By Application | By Packaging Type | By Distribution Channel | By End-Use Industry | |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

North America

North America remains one of the largest tomato paste markets globally, led primarily by the United States. California serves as a major global hub for industrial tomato processing and exports. Demand in the region is driven by strong consumption of sauces, frozen meals, canned foods, and foodservice products. Increasing demand for organic and clean-label food ingredients is further supporting premium tomato paste consumption across the U.S. and Canada. Mexico is also emerging as an important growth market due to expanding processed food manufacturing and rising domestic demand for packaged food products.

Europe

Europe dominates the global tomato paste market, supported by large-scale production and exports from Italy, Spain, and Portugal. Italy remains particularly important due to its premium tomato processing industry and strong international brand recognition. Germany, France, and the United Kingdom represent major consumption markets driven by high demand for sauces, ready meals, and convenience foods. European consumers increasingly prefer organic, sustainably sourced, and preservative-free tomato products, encouraging processors to invest in clean-label product innovation and environmentally responsible production practices.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by increasing urbanization, rising disposable income, and expanding processed food consumption in China, India, Japan, and Southeast Asia. China remains one of the world’s largest tomato paste exporters due to its extensive processing infrastructure and competitive production costs. India is witnessing rapid growth in packaged food demand and foodservice expansion, creating strong opportunities for tomato paste manufacturers. Japan and South Korea maintain high demand for premium convenience foods and imported food ingredients, further supporting regional market expansion.

Latin America

Latin America is experiencing moderate growth in tomato paste consumption, led primarily by Brazil and Argentina. Rising fast-food penetration, increasing retail packaged food sales, and expanding urban populations are supporting regional demand growth. Brazil remains the largest regional market due to its strong food processing industry and growing household consumption of sauces and ready meals. Chile and Mexico are also strengthening their presence within regional tomato product trade networks.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for imported tomato paste products due to rapid urbanization, population growth, and expansion of foodservice industries. Saudi Arabia and the UAE remain key import-driven markets with strong demand from restaurants, hotels, and packaged food manufacturers. Turkey plays a significant role as both a producer and exporter within the region. African countries are increasingly investing in domestic food processing infrastructure to reduce import dependency and strengthen local agricultural value chains.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Tomato Paste Market

- Mutti S.p.A.

- Kagome Co., Ltd.

- Olam Food Ingredients

- COFCO Tunhe

- Ingomar Packing Company

- The Morning Star Company

- Conesa Group

- Sugal Group

- Los Gatos Tomato Products

- Stanislaus Food Products

- J.G. Boswell Tomato Company

- Tat Gida

- SICA S.p.A.

- Guannong Tomato Products

- Xinjiang Chalkis Company