Tobacco Market Size

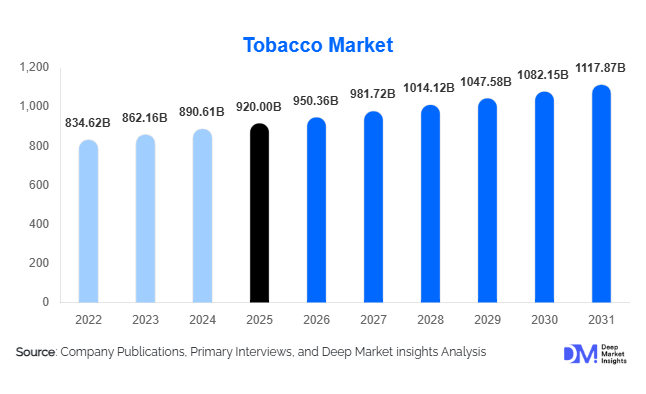

According to Deep Market Insights, the global tobacco market size was valued at USD 920 billion in 2025 and is projected to grow from USD 950.36 billion in 2026 to reach USD 1,117.87 billion by 2031, expanding at a CAGR of 3.3% during the forecast period (2026–2031). The tobacco market growth is primarily driven by sustained demand in emerging economies, strong pricing power of major players, and increasing adoption of next-generation products such as heated tobacco and nicotine pouches. Despite regulatory pressures and declining smoking rates in developed markets, innovation and diversification strategies continue to support steady revenue growth.

Key Market Insights

- Asia-Pacific dominates the global tobacco market, accounting for nearly 58% of total consumption, led by China and India.

- Cigarettes remain the leading product segment, contributing over 70% of global market revenue despite gradual declines in developed regions.

- Next-generation products are gaining momentum, particularly heated tobacco and nicotine pouches, showing strong double-digit growth in select markets.

- Offline retail channels continue to dominate, accounting for approximately 88% of total sales globally.

- Premiumization trends are strengthening, especially in developed markets, boosting margins for key players.

- Regulatory pressures and health awareness are reshaping product innovation and market strategies.

What are the latest trends in the tobacco market?

Shift Toward Reduced-Risk Products

The tobacco market is undergoing a structural shift toward reduced-risk products such as heated tobacco and nicotine pouches. These alternatives are gaining acceptance among consumers seeking less harmful options compared to traditional cigarettes. Companies are heavily investing in research and regulatory approvals to expand their portfolios in this segment. Markets in Europe and Japan have shown particularly strong adoption rates, with heated tobacco products capturing a significant share within a short period. This trend is expected to accelerate as governments provide clearer regulatory pathways for harm-reduction products.

Premiumization and Brand Differentiation

Premium tobacco products, including high-end cigars and specialized cigarette variants, are witnessing increased demand among affluent consumers. This trend is particularly strong in North America and Europe, where consumers are willing to pay higher prices for quality, brand value, and exclusivity. Companies are focusing on limited-edition products, innovative packaging, and enhanced product experiences to capture this segment. Premiumization is helping offset declining volumes by improving overall profitability and strengthening brand loyalty.

What are the key drivers in the tobacco market?

Strong Demand in Emerging Markets

Emerging economies such as India, Indonesia, and several African countries continue to drive global tobacco consumption. Large populations, rising disposable incomes, and relatively lower regulatory restrictions contribute to sustained demand. These regions remain critical for volume growth, compensating for declining consumption in developed markets.

Product Innovation and Diversification

Innovation in next-generation products is a key growth driver. Heated tobacco devices, nicotine pouches, and other alternatives are attracting new consumer segments, including those seeking smoking cessation or reduced-risk options. Continuous product development and technological advancements are enabling companies to expand their market presence and cater to evolving preferences.

What are the restraints for the global market?

Stringent Regulatory Environment

Governments worldwide are imposing stricter regulations, including higher taxes, advertising bans, and plain packaging laws. These measures directly impact consumption and limit market expansion. Regulatory compliance also increases operational costs for manufacturers.

Rising Health Awareness

Increasing awareness of the health risks associated with tobacco consumption is leading to declining smoking rates, particularly in developed regions. Anti-smoking campaigns and social stigma are influencing consumer behavior, posing long-term challenges to market growth.

What are the key opportunities in the tobacco industry?

Expansion of Next-Generation Products

The growing acceptance of reduced-risk products presents a significant opportunity for market players. Companies investing in heated tobacco and nicotine alternatives can capture new consumer segments and diversify revenue streams. Regulatory support in certain regions further enhances growth potential.

Growth in Emerging Markets

Untapped markets in Africa, Southeast Asia, and Latin America offer substantial growth opportunities. Increasing urbanization, rising incomes, and expanding distribution networks are expected to drive demand in these regions. Strategic investments and localized product offerings can unlock long-term growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 920 Billion |

| Market Size in 2026 | USD 950.36 Billion |

| Market Size in 2031 | USD 1117.87 Billion |

| CAGR | 3.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Cigarettes continue to dominate the global tobacco market, accounting for approximately 72% of total revenue in 2025. The leadership of this segment is primarily driven by its deeply entrenched consumer base, extensive distribution reach, and strong brand loyalty developed over decades. In addition, cigarettes benefit from well-established manufacturing infrastructure and supply chains, particularly in high-consumption regions such as Asia-Pacific. Pricing flexibility and the ability of manufacturers to pass on tax increases to consumers have further reinforced the segment’s dominance. However, growth within this category remains volume-constrained in developed markets due to regulatory pressures and declining smoking rates.

In contrast, next-generation products (NGPs), including heated tobacco and nicotine pouches, represent the fastest-growing segment. Their expansion is driven by increasing health awareness, regulatory support for reduced-risk alternatives, and aggressive investments by leading companies in innovation and product development. Meanwhile, smokeless tobacco products maintain strong regional relevance, particularly in South Asia, where cultural consumption patterns support demand. Cigars and cigarillos continue to occupy a niche but profitable segment, driven by premiumization trends and growing interest among affluent consumers in North America and Europe.

Distribution Channel Insights

Offline retail channels dominate the tobacco market, accounting for nearly 88% of global sales in 2025. This dominance is largely attributed to the accessibility and convenience offered by traditional retail formats such as convenience stores, kiosks, and supermarkets. In many emerging markets, tobacco sales remain heavily reliant on small-scale retailers and informal trade networks, which further strengthen offline distribution. Additionally, regulatory restrictions in several countries limit online sales of tobacco products, reinforcing the importance of physical retail channels.

However, online distribution is gradually gaining traction, particularly for next-generation and non-combustible products. Digital platforms are enabling direct-to-consumer engagement, better product education, and targeted marketing. The growth of e-commerce is also supported by rising smartphone penetration and digital payment adoption. Despite these advantages, stringent age verification requirements and advertising restrictions continue to constrain the full-scale expansion of online tobacco sales.

Price Segment Insights

The mid-range segment leads the market with approximately 50% share, driven by its optimal balance between affordability and perceived quality. This segment is particularly dominant in emerging economies, where consumers seek branded products at accessible price points. The ability of manufacturers to offer a wide range of mid-tier products tailored to local preferences has further strengthened this segment’s position.

The premium segment is experiencing robust growth, especially in developed markets such as North America and Europe. This growth is driven by increasing disposable incomes, evolving consumer lifestyles, and a shift toward high-quality and differentiated products. Premium offerings often command higher margins and benefit from strong brand equity. Meanwhile, the economy segment remains significant in price-sensitive regions, supported by low-income consumer groups and the availability of low-cost alternatives, including locally manufactured products and illicit trade in certain markets.

End-Use Insights

Mass-market consumers represent the largest share of tobacco consumption globally, driven by widespread product accessibility and affordability. This segment continues to underpin overall market demand, particularly in developing regions where smoking prevalence remains relatively high. However, premium consumers are emerging as the fastest-growing segment, fueled by urbanization, rising disposable incomes, and changing lifestyle preferences. These consumers are increasingly drawn to premium cigarettes, cigars, and next-generation products that offer enhanced experiences and perceived quality.

Export-driven demand also plays a crucial role in shaping the market, with major producing countries such as Brazil and Indonesia acting as key suppliers to global markets. Additionally, the rise of alternative nicotine products is creating new end-use applications, particularly in smoking cessation and lifestyle segments. This diversification is expanding the addressable consumer base and supporting long-term market evolution.

Explore more data points, trends and opportunities Download Free Sample Report

Tobacco Market Segmentations

By Product Type

- Cigarettes

- Cigars & Cigarillos

- Smokeless Tobacco

- Roll-Your-Own (RYO) & Pipe Tobacco

- Next-Generation Products (NGPs)

By Distribution Channel

- Offline Retail

- Online Retail

By Price Segment

- Economy

- Mid-Range

- Premium

By Flavor Type

- Unflavored/Classic

- Flavored

By End-Use Consumer

- Mass Market Consumers

- Premium/Lifestyle Consumers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global tobacco market, accounting for approximately 58% of the total market share in 2025. The region’s leadership is driven by large population bases, high smoking prevalence, and strong domestic production capabilities. China remains the single largest contributor, supported by state-controlled production and widespread consumption. India and Indonesia also represent significant markets due to the cultural acceptance of both smoking and smokeless tobacco products. Key growth drivers in the region include rising disposable incomes, expanding urban populations, and relatively moderate regulatory enforcement in certain countries. Additionally, the availability of low-cost products and strong distribution networks further sustains demand across both urban and rural areas.

North America

North America holds around 15% of the global market share, with the United States as the primary contributor. While traditional cigarette consumption is declining due to stringent regulations and increasing health awareness, the region is witnessing strong growth in next-generation products such as e-cigarettes and heated tobacco. High disposable incomes, advanced retail infrastructure, and rapid adoption of innovative nicotine delivery systems are key drivers of market evolution. Furthermore, premiumization trends and strong brand loyalty continue to support revenue growth despite declining volumes.

Europe

Europe accounts for approximately 20% of the global tobacco market, with major contributions from Germany, France, and the UK. The region is characterized by strict regulatory frameworks, including high taxation and advertising restrictions, which have led to declining cigarette consumption. However, growth is being driven by the increasing adoption of reduced-risk products, particularly heated tobacco. Consumer preference for premium and alternative products, coupled with strong awareness of harm-reduction options, is shaping the regional market. Additionally, innovation and product diversification by leading companies are supporting sustained revenue generation.

Latin America

Latin America represents around 5% of the global market, with Brazil and Mexico as key contributors. The region benefits from strong agricultural production and export activity, particularly in tobacco leaf cultivation. Domestic consumption is moderately growing, supported by urbanization and improving economic conditions in select countries. Key growth drivers include expanding middle-class populations, increasing retail penetration, and rising demand for affordable tobacco products. However, regulatory measures and economic volatility in certain countries may pose challenges to consistent growth.

Middle East & Africa

The Middle East & Africa region holds a smaller share of approximately 2% but is the fastest-growing market, with a CAGR exceeding 5%. Growth in this region is driven by rapid population expansion, increasing urbanization, and rising disposable incomes. Countries such as South Africa and Nigeria are emerging as key markets due to expanding consumer bases and improving retail infrastructure. Additionally, relatively lower taxation levels and evolving regulatory frameworks in some parts of the region are supporting market expansion. The growing presence of international tobacco companies and investments in distribution networks are further accelerating growth prospects.

Key Players in the Tobacco Market

- Philip Morris International

- British American Tobacco

- Japan Tobacco International

- Imperial Brands

- China National Tobacco Corporation

- Altria Group

- ITC Limited

- KT&G Corporation

- Swedish Match

- Gudang Garam

- Sampoerna

- Scandinavian Tobacco Group

- Universal Corporation

- Vector Group

- Turning Point Brands