Tilapia Market Size

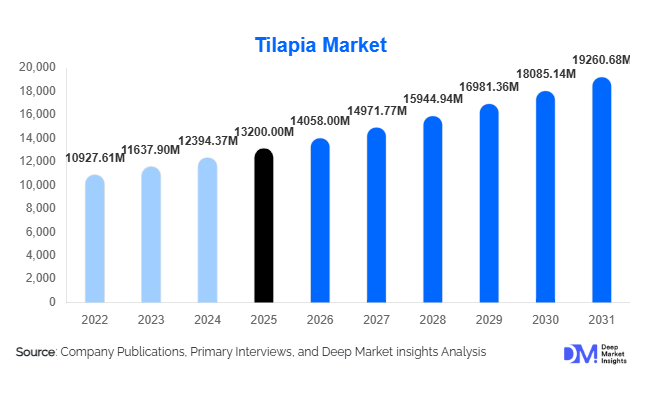

According to Deep Market Insights, the global tilapia market size was valued at USD 13,200 million in 2025 and is projected to grow from USD 1,4058.00 million in 2026 to reach USD 1,9260.68 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The tilapia market growth is primarily driven by increasing global demand for affordable protein sources, rapid expansion of aquaculture practices, and rising consumption of frozen and processed seafood products. The fish’s mild flavor, versatility, and cost-effectiveness position it as a preferred whitefish alternative across both developed and emerging markets.

Key Market Insights

- Tilapia remains one of the most consumed aquaculture species globally, supported by scalable farming methods and cost-efficient production cycles.

- Frozen tilapia fillets dominate global trade, driven by strong export demand from North America and Europe.

- Asia-Pacific leads global production, with China, Indonesia, and India accounting for a significant share of supply.

- Africa is emerging as the fastest-growing consumption region, fueled by rising population and protein demand.

- Value-added tilapia products are gaining traction, including breaded, marinated, and ready-to-cook formats.

- Technological advancements in aquaculture, such as biofloc and recirculating aquaculture systems (RAS), are improving yield and sustainability.

What are the latest trends in the tilapia market?

Shift Toward Sustainable Aquaculture Practices

Sustainability has become a central theme in the tilapia market, with producers increasingly adopting environmentally friendly farming methods such as recirculating aquaculture systems (RAS) and biofloc technology. These systems reduce water consumption, minimize waste discharge, and enhance productivity, addressing regulatory and environmental concerns. Certification programs and eco-labeling are gaining importance, particularly in export markets like Europe and North America, where consumers prefer responsibly sourced seafood. Producers investing in sustainable practices are also benefiting from premium pricing and stronger market access.

Growth of Value-Added and Processed Tilapia Products

The demand for convenience foods is significantly influencing tilapia consumption patterns. Processed formats such as frozen fillets, breaded fish, and ready-to-cook meals are gaining popularity among urban consumers. Retailers and foodservice operators are expanding their offerings of packaged tilapia products to cater to busy lifestyles. Innovations in packaging, cold chain logistics, and flavor enhancement are further supporting this trend, enabling manufacturers to increase margins and differentiate their product portfolios.

What are the key drivers in the tilapia market?

Rising Demand for Affordable Protein

Tilapia is widely recognized as a cost-effective protein source compared to other seafood options such as salmon and tuna. Increasing global population, rising incomes, and growing health awareness are driving demand for protein-rich diets, particularly in developing economies. Tilapia’s affordability and accessibility make it a staple food in regions like Asia-Pacific and Africa, significantly contributing to market growth.

Advancements in Aquaculture Technology

Technological innovations in aquaculture, including automated feeding systems, water quality monitoring, and disease management solutions, are enhancing production efficiency. These advancements enable year-round production, reduce mortality rates, and improve overall yield, making tilapia farming more profitable and scalable. The adoption of RAS and biofloc systems is particularly transforming production dynamics in both developed and emerging markets.

What are the restraints for the global market?

Environmental and Sustainability Challenges

Intensive aquaculture practices can lead to water pollution, habitat degradation, and disease outbreaks, raising concerns among regulators and environmental groups. Compliance with environmental standards often requires significant investment, increasing operational costs for producers. These challenges can limit production expansion, particularly in regions with stringent regulations.

Volatility in Feed Costs and Market Pricing

Feed accounts for a major portion of tilapia production costs, and fluctuations in prices of raw materials such as soybean and fishmeal directly impact profitability. Additionally, competition from alternative protein sources like poultry and plant-based products can influence pricing dynamics and market demand, posing challenges for industry participants.

What are the key opportunities in the tilapia industry?

Expansion in Emerging Markets

Rapid urbanization and population growth in regions such as Africa and Southeast Asia present significant growth opportunities for tilapia producers. Increasing disposable incomes and changing dietary patterns are driving higher consumption of fish protein, creating a favorable environment for market expansion. Local production and distribution investments can help companies capture untapped demand in these regions.

Development of Export-Oriented Value Chains

The growing demand for tilapia in international markets, particularly in North America and Europe, is encouraging producers to strengthen export capabilities. Investments in cold chain infrastructure, processing facilities, and quality certifications are enabling companies to access high-value markets and improve profit margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13200.00 Million |

| Market Size in 2026 | USD 14058.00 Million |

| Market Size in 2031 | USD 19260.68 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Frozen tilapia fillets dominate the global tilapia market, accounting for approximately 34% of the global market share. This dominance is strongly supported by the increasing globalization of seafood trade and the rising reliance on cold chain logistics that enable long-distance transportation without compromising quality. Frozen fillets are particularly preferred in export-driven economies due to their longer shelf life, standardized portioning, and ease of integration into retail packaging formats. The growing demand from supermarkets, hypermarkets, and foodservice distributors in developed markets has further strengthened this segment’s leadership position. Additionally, the rising popularity of ready-to-cook and ready-to-eat seafood meals among urban consumers has significantly contributed to sustained demand for frozen tilapia fillets, especially in North America and Europe where convenience consumption patterns are highly established.Value-added tilapia products, including marinated fillets, breaded fish portions, seasoned cuts, and pre-cooked offerings, are witnessing accelerating growth as consumer lifestyles shift toward convenience-oriented food consumption. This segment is particularly driven by urbanization, increasing female workforce participation, and time-constrained lifestyles in metropolitan regions. Food manufacturers are increasingly investing in product innovation, flavor diversification, and attractive packaging formats to cater to evolving consumer preferences. The expansion of quick-service restaurants and frozen food aisles in retail chains is also reinforcing demand for processed tilapia products. Moreover, health-conscious consumers are showing greater interest in high-protein, low-fat seafood options, further boosting the attractiveness of value-added tilapia offerings.

Application Insights

Household consumption represents the largest application segment, contributing nearly 52% of the global market share. This dominance is largely attributed to tilapia’s affordability, mild taste profile, and versatility in cooking applications. In emerging economies, tilapia is a staple protein source due to its cost-effectiveness compared to other animal proteins such as beef and poultry. Rising awareness of nutritional benefits, particularly its high protein content and low cholesterol levels, has further strengthened household demand. Increasing penetration of modern retail outlets and improved supply chain efficiency have also made tilapia more accessible to end consumers, reinforcing its household consumption base across both urban and rural markets.The food processing industry is also witnessing steady expansion, leveraging tilapia as a key raw material in frozen meals, canned seafood products, and packaged ready-to-eat food solutions. The increasing demand for convenience foods in urban centers has encouraged manufacturers to incorporate tilapia into diversified product portfolios. Technological advancements in food preservation, freezing, and vacuum packaging have enabled extended shelf life while maintaining product quality, further supporting industrial usage. The growing trend of private-label seafood products in retail chains is also contributing to higher consumption of processed tilapia within the food manufacturing ecosystem.

Distribution Channel Insights

Direct or B2B distribution channels account for around 46% of the global market share, primarily driven by bulk procurement activities from processors, exporters, and institutional buyers. These channels are essential for maintaining supply chain efficiency, especially in large-scale aquaculture-producing regions where tilapia is exported to international markets. Strong relationships between producers and foodservice distributors also play a critical role in sustaining this segment. The growth of integrated aquaculture companies that manage production, processing, and export operations has further strengthened the dominance of B2B distribution frameworks.Modern retail channels, including supermarkets and hypermarkets, are expanding rapidly due to increasing urbanization and evolving consumer shopping behavior. These retail formats provide consumers with easy access to a wide variety of fresh, frozen, and value-added tilapia products under one roof. The emphasis on branded seafood offerings, quality assurance, and attractive packaging has significantly improved consumer trust in modern retail outlets. Additionally, in-store refrigeration systems and improved cold storage infrastructure have enabled retailers to maintain product freshness, thereby enhancing sales volumes across developed and emerging economies.Online retail is emerging as a high-growth distribution channel, driven by increasing digital adoption, smartphone penetration, and the expansion of e-commerce grocery platforms. Consumers are increasingly opting for home delivery services due to convenience, especially in urban areas where time constraints are significant. The integration of cold chain logistics with online grocery platforms has enabled efficient delivery of frozen seafood products, including tilapia. Subscription-based seafood delivery services and direct-to-consumer aquaculture models are also gaining traction, further accelerating the growth of this channel. Promotional discounts, digital payment systems, and personalized shopping experiences are additional factors contributing to the expansion of online seafood sales.

Farming Method Insights

Pond aquaculture remains the dominant farming method, contributing approximately 48% of global tilapia production. Its widespread adoption is primarily due to low initial investment requirements, operational simplicity, and adaptability to diverse climatic conditions. In developing regions, small-scale farmers continue to rely on pond-based systems as a primary livelihood source. Government support programs, training initiatives, and access to microfinance have further encouraged the expansion of pond aquaculture, particularly in rural areas. The scalability of pond systems allows both subsistence and commercial production, making it a highly versatile farming method.Advanced aquaculture systems such as Recirculating Aquaculture Systems (RAS) and biofloc technology are gaining significant traction, especially in regions facing water scarcity and environmental constraints. These systems offer higher productivity, improved biosecurity, and reduced environmental impact compared to traditional methods. RAS, in particular, is increasingly being adopted in urban aquaculture setups where land availability is limited but demand for fresh fish is high. Biofloc systems are also gaining popularity due to their ability to recycle nutrients and reduce feed costs, making them economically attractive for intensive farming operations.Technological advancements in aquaculture, including automated feeding systems, water quality monitoring sensors, and AI-driven farm management tools, are transforming production efficiency across farming methods. These innovations are enabling farmers to optimize yield, reduce mortality rates, and improve overall sustainability, thereby strengthening the long-term growth outlook of the tilapia farming industry.

Explore more data points, trends and opportunities Download Free Sample Report

Tilapia Market Segmentations

By Product Type

- Whole Tilapia

- Tilapia Fillets

- Value-Added Tilapia Products

By Application

- Household Consumption

- Foodservice Industry

- Food Processing Industry

By Distribution Channel

- Direct/B2B Sales

- Modern Retail

- Traditional Retail

- Online Retail & E-commerce

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global tilapia market, accounting for nearly 45% of the total market share. This leadership position is primarily driven by China, which remains the largest producer and exporter of tilapia globally. The country’s dominance is supported by well-established aquaculture infrastructure, government-backed fisheries policies, and large-scale production capabilities. Increasing domestic consumption in China, driven by rising disposable incomes and dietary diversification, further reinforces its market strength. Additionally, countries such as Indonesia, India, Thailand, and Vietnam are rapidly expanding their production capacities due to favorable climatic conditions, abundant water resources, and growing export opportunities. The rising demand for affordable protein sources across densely populated regions is a key structural driver supporting long-term market growth in Asia-Pacific. Rapid urbanization, expansion of cold chain logistics, and technological adoption in aquaculture farming are further accelerating regional development.

Latin America

Latin America holds approximately 25% of the global market share, with Brazil emerging as a key production and consumption hub. The region benefits from abundant freshwater resources, tropical climatic conditions, and increasing government support for aquaculture development. Brazil’s strong domestic demand is driven by rising health consciousness and increasing preference for seafood as a primary protein source. Additionally, export-oriented production is gaining momentum, particularly toward North American and European markets. Investments in aquaculture infrastructure, improved feed technologies, and expansion of processing facilities are strengthening the region’s competitive position. The growing involvement of private-sector players and international partnerships is further accelerating productivity and market penetration across Latin America.

North America

North America represents a major import-driven market, with the United States being the largest importer of tilapia globally. The region’s demand is strongly supported by the expanding retail and foodservice sectors, where tilapia is widely consumed due to its affordability and mild flavor profile. Increasing consumer preference for healthy protein alternatives and low-fat seafood options is a key growth driver. The popularity of frozen fillets in supermarkets and restaurant chains has significantly contributed to market expansion. Additionally, strong cold chain infrastructure and efficient logistics networks enable seamless distribution across the region. Rising awareness of sustainable seafood sourcing is also influencing purchasing decisions, encouraging importers to source certified and responsibly farmed tilapia products.

Europe

Europe accounts for around 15% of the global market share, with strong demand concentrated in countries such as the United Kingdom, Germany, France, and the Netherlands. The region’s growth is primarily driven by increasing consumer awareness regarding sustainable seafood consumption and strict regulatory frameworks governing seafood imports. European consumers are increasingly seeking certified tilapia products that meet environmental and quality standards. The expansion of retail seafood sections in supermarkets and the growing popularity of international cuisines have further boosted demand. Additionally, the rising trend of healthy eating and protein-rich diets is supporting steady consumption growth. Import dependency remains high, making Europe a key destination for global tilapia exporters.

Middle East & Africa

The Middle East & Africa region is experiencing rapid growth, with Africa emerging as the fastest-growing market at a CAGR exceeding 8%. The region’s expansion is primarily driven by population growth, rising urbanization, and increasing demand for affordable protein sources. Countries such as Egypt and Nigeria are major consumers, supported by strong domestic aquaculture production and government initiatives promoting fish farming. Tilapia is particularly important in Africa due to its adaptability to local farming conditions and affordability compared to other protein sources. In the Middle East, demand is fueled by high-income expatriate populations, expanding tourism sectors, and increasing reliance on imported seafood. Investments in aquaculture infrastructure and growing awareness of food security are expected to further strengthen market growth across the region.

Key Players in the Tilapia Market

- Charoen Pokphand Foods

- Guangdong Haid Group

- Zoneco Group

- Baiyang Investment Group

- China National Fisheries Corporation

- Thai Union Group

- PT Japfa Comfeed Indonesia

- Regal Springs

- Empresas AquaChile

- Godrej Agrovet

- Avanti Feeds

- Guangdong Evergreen Group

- Trapia Malaysia

- Lake Harvest Group

- Zhejiang Ocean Family