Tick Control Market Size

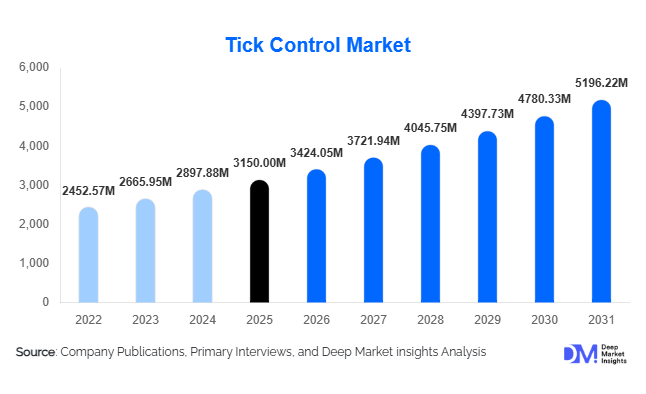

According to Deep Market Insights, the global tick control market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,424.05 million in 2026 to reach USD 5,196.22 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by the increasing prevalence of tick-borne diseases, rising companion animal ownership, expanding livestock production, and growing awareness of preventive animal healthcare practices worldwide. Climate change-driven expansion of tick habitats and the adoption of long-duration parasiticides are further accelerating demand across both developed and emerging economies.

Key Market Insights

- Preventive tick management is replacing reactive treatment approaches, supported by veterinary recommendations and subscription-based pet healthcare models.

- Companion animal treatments represent the largest revenue segment, fueled by pet humanization and recurring preventive care spending.

- North America dominates global demand due to high veterinary expenditure and increasing tick-borne disease awareness.

- Asia-Pacific is the fastest-growing region, supported by livestock expansion and rising urban pet adoption in China and India.

- Biological and eco-friendly tick control products are gaining traction as regulatory pressure on chemical acaricides intensifies.

- Technological innovation, including long-acting oral treatments and integrated pest management solutions, is reshaping market competition.

What are the latest trends in the tick control market?

Shift Toward Integrated Tick Management

Tick control strategies are evolving toward integrated tick management (ITM), combining on-animal treatments, environmental control, and monitoring solutions. Livestock operators and public health agencies increasingly prefer holistic programs that reduce reinfestation risks and improve long-term effectiveness. Integrated solutions also help mitigate resistance development associated with repeated chemical usage. Companies are developing bundled offerings that include diagnostics, treatment scheduling, and environmental treatment services, creating recurring revenue models while improving treatment outcomes.

Growth of Long-Acting and Oral Parasiticides

Long-duration tick treatments are gaining widespread adoption, particularly in companion animal healthcare. Oral chewable formulations offering protection lasting several weeks or months are becoming preferred alternatives to traditional topical treatments. These products improve compliance among pet owners while providing consistent efficacy. Advances in controlled-release formulations and combination parasite protection products are enabling manufacturers to differentiate through convenience and effectiveness, especially in premium veterinary markets.

What are the key drivers in the tick control market?

Rising Incidence of Tick-Borne Diseases

The growing prevalence of diseases such as Lyme disease, ehrlichiosis, and babesiosis has significantly increased awareness of tick prevention. Governments, veterinarians, and livestock producers are prioritizing preventive parasite management to protect both animal and human health. Expanding tick populations linked to climate change are further increasing exposure risks across new geographic regions, strengthening long-term market demand.

Expansion of Global Livestock Production

Tick infestations directly affect livestock productivity by reducing milk yield, weight gain, and reproductive efficiency. Export-driven meat and dairy industries are investing heavily in parasite control programs to meet international quality standards. Large-scale cattle farming operations increasingly adopt systematic tick management programs to minimize economic losses and maintain herd health.

What are the restraints for the global market?

Chemical Resistance Among Tick Populations

Repeated use of similar acaricide formulations has resulted in resistance development in several regions. Reduced efficacy increases treatment frequency and operational costs for farmers and pet owners. Manufacturers must continuously invest in research and new formulations to maintain effectiveness, creating barriers for smaller market participants.

Regulatory and Environmental Constraints

Growing environmental concerns regarding pesticide toxicity and chemical residues are leading to stricter regulations worldwide. Approval timelines for new products are becoming longer, increasing compliance costs and slowing product launches. Regulatory pressure is particularly strong in Europe and North America, encouraging the transition toward biological alternatives.

What are the key opportunities in the tick control industry?

Biological and Sustainable Tick Control Solutions

Eco-friendly formulations derived from microbial or plant-based sources represent a major growth opportunity. Increasing regulatory support for sustainable pest management and consumer preference for safer products are accelerating adoption. Companies investing in biological acaricides and environmentally safe formulations are expected to gain competitive advantages and premium pricing opportunities.

Growth in Emerging Pet Care Markets

Rapid urbanization and rising disposable incomes in Asia-Pacific and Latin America are expanding companion animal ownership. Preventive veterinary care adoption remains relatively low compared to developed markets, creating significant untapped potential. Affordable premium products tailored to emerging markets are expected to drive substantial revenue growth for new entrants and established players alike.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150 Million |

| Market Size in 2026 | USD 3424.05 Million |

| Market Size in 2031 | USD 5196.22 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chemical tick control products dominate the global market, owing to their rapid efficacy, cost-effectiveness, and scalability across both large-scale livestock operations and companion animal care, securing the largest revenue share. Combination formulations that integrate insect growth regulators with acaricides are increasingly preferred, as they help delay resistance development in tick populations. Biological tick control products are gaining momentum, driven by stricter regulatory frameworks and rising demand for eco-friendly alternatives. Natural repellents are attracting environmentally conscious consumers seeking non-chemical interventions. Physical solutions, such as tick collars and traps, continue to perform strongly in companion animal applications due to their ease of use, long-lasting protection, and convenience for pet owners. Overall, the market is witnessing a balanced growth across chemical, biological, and physical solutions as diverse end-user needs evolve.

Application Insights

On-animal treatments remain the leading application segment globally, driven by the widespread adoption of oral medications, spot-on treatments, and medicated collars that provide rapid and targeted tick control. Environmental treatment solutions are expanding at a notable pace, supported by the growing implementation of integrated pest management strategies in both livestock farms and residential settings. Large-scale pasture and facility spraying programs are increasingly essential in regions with high tick prevalence, mitigating economic losses in livestock production. Additionally, integrated tick management programs, which combine on-animal and environmental interventions, are emerging as a high-growth application area, particularly in regions with stringent disease control policies and rising awareness of tick-borne infections.

Distribution Channel Insights

Veterinary clinics and hospitals represent the dominant distribution channel, with professional recommendations significantly influencing purchasing decisions among pet owners and livestock managers. Retail pet stores and agricultural supply outlets maintain steady demand, particularly in rural and semi-urban livestock markets. E-commerce platforms are experiencing rapid growth, driven by urban consumers seeking convenient, subscription-based preventive care solutions. Direct-to-consumer veterinary platforms are also reshaping the distribution landscape by improving accessibility, providing personalized guidance, and supporting timely product delivery, particularly in emerging markets.

End-Use Insights

Household pet owners account for the largest share of tick control demand, due to recurring preventive treatment cycles and increasing awareness of pet health. Commercial livestock farms constitute a significant volume-driven segment, especially in beef, dairy, and mixed farming systems where effective parasite control directly impacts productivity, product quality, and profitability. Veterinary healthcare providers serve as both prescribers and distributors, influencing the adoption of innovative tick control solutions. Government agencies and public health organizations are increasingly procuring tick control products to support disease prevention initiatives, vector surveillance programs, and livestock health policies, further sustaining market demand.

Explore more data points, trends and opportunities Download Free Sample Report

Tick Control Market Segmentations

By Product Type

- Chemical Tick Control Products

- Biological Tick Control Products

- Natural & Organic Tick Repellents

- Tick Control Devices & Physical Solutions

By Application

- On-Animal Treatment

- Environmental Treatment

- Integrated Tick Management Programs

By Animal Type

- Companion Animals

- Livestock Animals

- Wildlife & Public Health Control Programs

By Distribution Channel

- Veterinary Clinics & Hospitals

- Retail Stores

- E-commerce Platforms

- Government & Institutional Procurement

By End Use

- Household Pet Owners

- Commercial Livestock Farms

- Veterinary Healthcare Providers

- Government/Public Health Agencies

- Landscaping & Pest Control Service Providers

Regional Insights

North America

North America leads the global tick control market, underpinned by high expenditure on pet healthcare, advanced veterinary infrastructure, and growing public awareness of tick-borne diseases such as Lyme disease. The United States is the largest national market, driven by widespread adoption of preventive treatments and robust professional veterinary guidance. Canada is experiencing growing demand as warming climates expand tick habitats into previously unaffected areas. Regional growth is further supported by technological advancements in diagnostic tools, integration of tick control in livestock management programs, and strong government initiatives promoting animal health and disease prevention.

Europe

Europe holds a significant market share, fueled by stringent animal welfare regulations, increasing adoption of eco-friendly and biological parasite control products, and high consumer awareness regarding pet health. Germany, France, and the United Kingdom are leading markets in the region. Regulatory pressure and government incentives are accelerating innovation in biological and combination tick control technologies. Moreover, rising pet ownership, modernization of livestock farming practices, and growing demand for organic and sustainable agricultural solutions are key drivers supporting market expansion across Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, led by China and India. The expansion of livestock populations, rapid growth in pet ownership, and modernization of agricultural practices are primary growth drivers. Rising veterinary awareness, adoption of integrated pest management strategies, and increasing disposable incomes are further stimulating market demand. Additionally, government-led animal health programs, climate-related changes increasing tick prevalence, and expansion of commercial livestock farming contribute significantly to the sustained growth of tick control solutions across the region.

Latin America

Latin America exhibits strong demand growth, particularly in Brazil and Mexico, where cattle farming represents a major economic sector. The adoption of tick control measures is critical for maintaining export-quality meat production and preventing productivity losses in livestock operations. Regional growth is driven by large-scale ranching practices, increased investment in livestock health management, and heightened awareness of tick-borne diseases affecting both animals and humans. Furthermore, government support and private sector initiatives promoting veterinary care are strengthening market penetration across the region.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, fueled by livestock modernization programs, food security investments, and increasing veterinary infrastructure. South Africa leads regional adoption due to its well-developed livestock industry, while Gulf countries are investing in advanced livestock health management programs to ensure sustainable production. Expansion of commercial farms, government-driven animal health initiatives, and heightened awareness of zoonotic diseases are significant factors driving market growth across this region. Additionally, emerging interest in environmentally safe tick control products and integration of modern pest management techniques is supporting long-term demand.

Key Players in the Tick Control Market

- Zoetis Inc.

- Merck Animal Health

- Elanco Animal Health Incorporated

- Boehringer Ingelheim International GmbH

- Bayer AG (Animal Health portfolio)

- Virbac SA

- Ceva Santé Animale

- Vetoquinol SA

- Dechra Pharmaceuticals PLC

- IDEXX Laboratories

- Neogen Corporation

- Phibro Animal Health Corporation

- Norbrook Laboratories Ltd.

- PetIQ Inc.

- Ourofino Saúde Animal