Texturizing Agents Market Size

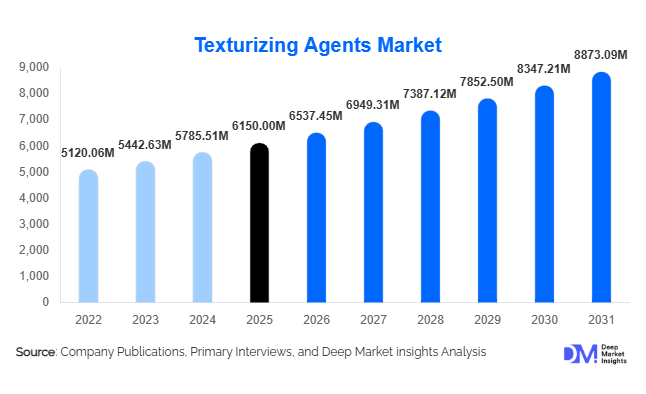

According to Deep Market Insights, the global texturizing agents market size was valued at USD 6,150 million in 2025 and is projected to grow from USD 6,537.45 million in 2026 to reach USD 8,873.09 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). Market growth is primarily driven by increasing demand for processed and convenience foods, rising popularity of plant-based proteins, and the growing need for clean-label and functional ingredients across the food, beverage, cosmetics, and pharmaceutical industries.

Key Market Insights

- Hydrocolloids and protein-based texturizing agents dominate the market due to their ability to improve texture, stability, and mouthfeel in a wide range of food and beverage applications.

- North America holds a major share of the global market, supported by a mature food processing sector and high consumer awareness of product quality and texture.

- Asia-Pacific is the fastest-growing region, fueled by increasing packaged food consumption, rising disposable income, and urbanization in China, India, and Southeast Asia.

- Functional and clean-label products are gaining popularity globally, encouraging manufacturers to innovate with natural texturizing agents like xanthan gum, carrageenan, and plant proteins.

- Beverage, dairy, and bakery applications remain high-volume segments due to consistent demand for product stability, improved mouthfeel, and extended shelf life.

- Technological advancements, including hydrocolloid blends, protein-starch combinations, and microencapsulation techniques, are enabling product differentiation and premium pricing strategies.

What are the latest trends in the texturizing agents market?

Shift Toward Clean-Label and Natural Ingredients

Manufacturers are increasingly replacing synthetic stabilizers with natural texturizing agents such as hydrocolloids, proteins, and plant fibers. This shift is driven by consumer preference for clean-label products free from artificial additives. The trend is particularly strong in bakery, dairy, and beverage segments, where demand for natural thickeners, gelling agents, and emulsifiers is rising. Companies are investing in R&D to develop novel plant-based texturizers that combine functionality with health benefits, positioning them for premium pricing and higher consumer acceptance.

Integration of Functional Ingredients

Texturizing agents are increasingly being formulated with functional benefits such as dietary fiber enrichment, high protein content, and prebiotic effects. This trend is evident in beverages, health snacks, and functional dairy products. The integration of texturizing and functional ingredients not only enhances product texture and stability but also aligns with growing health-conscious consumer demand, creating opportunities for differentiation and market expansion.

Technological Innovations and Formulation Advancements

Advanced formulations such as hydrocolloid-protein blends, microencapsulation, and modified starches are enabling manufacturers to achieve superior texture, stability, and shelf-life performance. Innovations in processing technologies, including high-shear mixing and extrusion, are improving ingredient solubility, water-binding capacity, and functional versatility. Such advancements are particularly critical in frozen desserts, dairy products, plant-based alternatives, and confectionery applications, where texture quality significantly impacts consumer perception and repeat purchase.

What are the key drivers in the texturizing agents market?

Growing Demand for Processed and Convenience Foods

The rising consumption of ready-to-eat meals, bakery products, dairy, and beverages is a primary driver of growth. Texturizing agents improve product stability, mouthfeel, and shelf life, making them essential for modern food processing. Urbanization, increased dual-income households, and the shift toward quick meal solutions are reinforcing this demand globally. Processed food consumption in Asia-Pacific, North America, and Europe has significantly boosted the adoption of hydrocolloids, starches, and protein-based texturizers.

Rising Popularity of Plant-Based and Functional Foods

Plant-based diets and health-focused eating habits are driving growth for texturizing agents that can mimic animal-based textures, such as gelation and emulsification properties. Protein isolates, pea protein, and fiber-based agents are increasingly used in dairy alternatives, meat substitutes, and high-protein snacks. Functional food trends, such as fiber-enriched beverages and prebiotic yogurt, also support market expansion, enabling manufacturers to meet consumer preferences for health-oriented products.

Expansion of Clean-Label and Natural Ingredient Preferences

Consumer preference for transparency and natural formulations is boosting demand for hydrocolloids, natural gums, fibers, and plant-based proteins. Manufacturers are reformulating products to replace synthetic additives, leading to higher adoption of naturally derived texturizing agents. This driver is particularly strong in Europe and North America, where regulatory requirements and consumer awareness of ingredient sourcing are high, resulting in a shift toward clean-label formulations.

What are the restraints for the global market?

Volatility in Raw Material Prices

The global texturizing agents market is affected by fluctuations in raw material costs, including gums, proteins, and starches. Price volatility of key natural ingredients such as xanthan gum, carrageenan, and soy protein can increase production costs for manufacturers. These fluctuations, driven by agricultural yield variability and supply chain disruptions, can affect pricing strategies and profit margins, potentially limiting adoption in price-sensitive segments.

Regulatory and Compliance Challenges

Stringent regulations regarding food additives, labeling, and safety standards can pose challenges for market players. Varying requirements across countries may complicate product approvals, exports, and market entry. Companies must invest in compliance, quality testing, and certification processes, increasing operational costs and potentially slowing the introduction of new texturizing agents in global markets.

What are the key opportunities in the texturizing agents market?

Expansion in Emerging Markets

Rapid urbanization, increasing disposable income, and growing packaged food consumption in Asia-Pacific and Latin America create significant opportunities. Countries such as China, India, Brazil, and Mexico are experiencing rising demand for bakery, dairy, and beverage products, driving growth for hydrocolloids, protein isolates, and starch-based texturizers. Manufacturers can capture market share through local production facilities, strategic partnerships, and tailored formulations for regional tastes.

Integration with Functional and Health-Focused Products

The rise in functional foods, dietary supplements, and plant-based alternatives presents opportunities for texturizing agents that also provide health benefits. Incorporating fibers, prebiotics, and proteins allows manufacturers to deliver improved texture while appealing to health-conscious consumers. This integration opens premium pricing potential and differentiation, particularly in ready-to-drink beverages, dairy alternatives, and nutraceuticals.

Sustainable and Clean-Label Ingredient Adoption

Growing emphasis on natural and sustainable ingredients is a strategic opportunity. Texturizing agents derived from renewable sources or waste-reducing processes can align with sustainability goals, enhance brand reputation, and attract environmentally conscious consumers. Companies that innovate with plant-based or eco-friendly texturizers are well-positioned to capture expanding demand across developed and emerging markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6150 Million |

| Market Size in 2026 | USD 6537.45 Million |

| Market Size in 2031 | USD 8873.09 Million |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Hydrocolloids dominate the global market, accounting for approximately 28% of 2025 revenues, due to their versatile application across bakery, dairy, beverages, and meat products. Protein-based texturizers follow closely with 22%, driven by the growing popularity of plant-based and functional foods. Starches and modified starches hold around 20%, widely used in sauces, frozen foods, and processed snacks. Emulsifiers and fibers contribute the remaining share, with rising adoption in specialty and clean-label applications. Overall, hydrocolloids remain the leading segment due to their multi-functional properties and strong acceptance in established markets.

Application Insights

Bakery and confectionery applications hold the largest market share at approximately 30% in 2025, driven by demand for texture, moisture retention, and shelf-life extension in bread, cakes, and pastries. Dairy and frozen products follow with 25%, particularly in yogurt, cheese, and ice cream, where mouthfeel and stability are critical. Meat, poultry, and seafood account for 15%, as texturizers improve protein binding and product consistency. Beverages and sauces together hold 20%, while other applications, such as nutraceuticals and pet food, occupy 10%. Growing urban consumption and functional product trends continue to drive demand across these applications.

End-Use Insights

Food and beverage industries remain the largest end users, accounting for over 70% of global demand. The cosmetic and personal care sector is growing steadily, using texturizing agents for hair care, skincare, and styling products. Pharmaceuticals and nutraceuticals represent 10–12% of demand, mainly for tablet coatings and functional foods. Emerging applications in plant-based products, protein bars, and fiber-enriched beverages are expected to accelerate end-use adoption. Export-driven demand is particularly strong from North America and Europe to the Asia-Pacific and Latin America, where processed food manufacturing is expanding rapidly.

Explore more data points, trends and opportunities Download Free Sample Report

Texturizing Agents Market Segmentations

By Product Type

- Hydrocolloids

- Protein-Based Texturizers

- Starches & Modified Starches

- Emulsifiers & Surfactants

- Dietary Fibers & Specialty Texturizers

By Application

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Meat, Poultry & Seafood Products

- Beverages (RTD, Functional, Carbonated)

- Sauces, Dressings & Condiments

- Nutraceuticals & Functional Foods

By End-Use Industry

- Food & Beverages

- Cosmetics & Personal Care

- Pharmaceuticals

- Nutraceuticals & Dietary Supplements

By Form

- Powder

- Liquid

Regional Insights

North America

North America accounted for 28% of the 2025 market, driven by high processed food consumption, mature bakery and dairy industries, and widespread adoption of clean-label products. The U.S. leads regional demand, followed by Canada, supported by R&D investments and consumer preference for texture-enhanced products. Market growth is steady, witha CAGR projected at 5.8% during 2026–2031.

Europe

Europe contributed 25% of the 2025 market share, led by Germany, France, and the U.K. Demand is driven by regulatory emphasis on natural ingredients, strong bakery and dairy sectors, and functional food trends. Europe is also adopting innovative hydrocolloid blends and plant-based protein texturizers more quickly than other regions, with a CAGR of 6% through 2031.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with China and India as key markets. Rising urbanization, disposable income, and expansion of packaged food industries drive CAGR above 7% during 2026–2031. Growth is particularly strong in bakery, dairy alternatives, and beverages. Southeast Asian countries are also adopting functional and clean-label ingredients, contributing to regional expansion.

Latin America

Brazil and Mexico are leading markets, accounting for nearly 10% of the global share in 2025. Growth is driven by packaged food demand and bakery sector expansion. Market penetration is increasing as manufacturers localize production and introduce plant-based and functional formulations.

Middle East & Africa

MEA represents 7% of the market in 2025, with South Africa, UAE, and Saudi Arabia as primary contributors. Growth is fueled by processed food adoption, urbanization, and investments in food technology and manufacturing facilities. The region is also leveraging imported texturizing agents for dairy and bakery applications.

Key Players in the Texturizing Agents Market

- Cargill, Inc.

- ADM (Archer Daniels Midland Company)

- DuPont de Nemours, Inc.

- Kerry Group

- Ingredion Incorporated

- Glanbia plc

- CP Kelco

- Roquette Frères

- BASF SE

- Corbion N.V.

- FMC Corporation

- Arla Foods Ingredients

- Tate & Lyle PLC

- Mead Johnson Nutrition

- Prinova Group LLC