Tennis Apparel Market Size

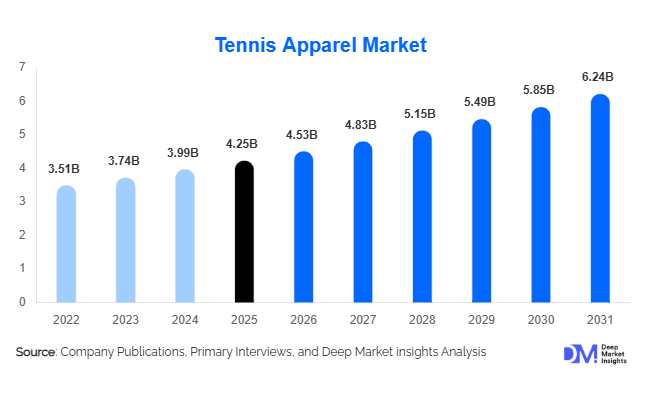

According to Deep Market Insights, the global tennis apparel market size was valued at USD 4.25 billion in 2025 and is projected to grow from USD 4.53 billion in 2026 to reach USD 6.24 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The growth of the tennis apparel market is primarily driven by rising participation in tennis across both recreational and professional levels, increasing consumer preference for performance-enhancing sportswear, and the growing influence of athleisure fashion trends. Tennis apparel has evolved beyond sports-specific usage and is increasingly being adopted as lifestyle wear, particularly among younger consumers seeking premium athletic aesthetics and comfort. Product innovations in moisture-wicking fabrics, UV-protection materials, stretchable textiles, and sustainable fiber technologies are further accelerating market demand. In addition, increasing investments in tennis infrastructure, youth development programs, and international tournaments across North America, Europe, and Asia-Pacific are expanding the global consumer base. The growing popularity of women’s tennis, coupled with rising disposable incomes in emerging economies such as China and India, is creating substantial opportunities for apparel manufacturers. Furthermore, direct-to-consumer sales channels, digital retail expansion, and athlete endorsement strategies continue to enhance brand visibility and consumer engagement, supporting long-term market expansion.

Key Market Insights

- Tennis-inspired athleisure apparel is becoming a major growth driver, with consumers increasingly wearing tennis clothing beyond the court for casual and lifestyle purposes.

- Sustainable and recycled-material apparel is gaining significant market traction, particularly in Europe and North America where environmental awareness influences purchasing decisions.

- North America dominates the global tennis apparel market, accounting for approximately 34% of global revenue due to high participation rates and premium product adoption.

- Asia-Pacific is the fastest-growing regional market, supported by expanding tennis academies, rising middle-class incomes, and increasing sports participation.

- Women's tennis apparel is outpacing overall market growth, fueled by rising female participation and strong demand for tennis-inspired fashion products.

- Technical fabric innovations, including cooling technologies, compression features, UV protection, and moisture management systems, are reshaping product development strategies.

Tennis Apparel Market Trends

Rise of Tennis-Inspired Athleisure Fashion

The boundary between sportswear and everyday fashion continues to blur, positioning tennis apparel as a major contributor to the global athleisure movement. Tennis skirts, polo shirts, dresses, performance tops, and court-inspired apparel are increasingly being adopted for casual wear, particularly among younger demographics. Luxury fashion brands and sportswear manufacturers are collaborating to create premium collections that combine functionality with fashion appeal. Social media influence, celebrity endorsements, and professional tennis tournaments have significantly amplified the visibility of tennis-inspired fashion. Consumers increasingly seek versatile apparel that can transition seamlessly between athletic and lifestyle settings, making athleisure one of the most influential trends shaping future market growth.

Sustainable Performance Apparel Gaining Momentum

Sustainability is becoming a core purchasing criterion across the global sportswear industry. Tennis apparel manufacturers are increasingly investing in recycled polyester, organic cotton, bio-based fibers, low-water dyeing technologies, and circular production models. Brands are introducing environmentally responsible collections while maintaining performance characteristics such as moisture management, flexibility, and durability. European consumers have been particularly receptive to sustainable sportswear initiatives, while North American brands continue expanding recycled-material product portfolios. Growing regulatory pressure regarding textile sustainability and increasing consumer awareness are expected to accelerate adoption of environmentally friendly tennis apparel throughout the forecast period.

Tennis Apparel Market Drivers

Growing Global Tennis Participation

Increasing participation in tennis across both developed and emerging markets remains one of the strongest drivers for the tennis apparel market. Governments, sports federations, and educational institutions are actively promoting tennis through infrastructure development, youth training programs, and grassroots initiatives. The growth of recreational tennis players, club memberships, and amateur tournaments directly contributes to higher demand for specialized apparel. Countries such as the United States, China, India, Australia, and the United Kingdom continue witnessing steady growth in tennis participation, creating a broader customer base for manufacturers.

Expansion of Performance Textile Technologies

Advancements in textile engineering have significantly enhanced the functionality of tennis apparel. Modern garments incorporate moisture-wicking systems, thermal regulation, odor-control technologies, UV protection, and compression benefits that improve athletic performance and comfort. Consumers are increasingly willing to pay premium prices for apparel offering measurable performance advantages. This trend has encouraged brands to invest heavily in research and development, creating a continuous cycle of product innovation and replacement demand.

Tennis Apparel Market Restraints

Intense Competitive Pressure and Brand Saturation

The tennis apparel market is characterized by strong competition among global sportswear giants and emerging niche brands. Established companies possess significant advantages in marketing, athlete sponsorships, retail distribution, and brand recognition, making market entry challenging for new participants. Price competition in the mid-range segment has intensified, placing pressure on profitability and limiting expansion opportunities for smaller manufacturers.

Counterfeit Products and Pricing Pressures

The availability of counterfeit sportswear products through online and informal retail channels continues to affect premium brand sales. Counterfeit apparel often imitates major tennis brands at significantly lower prices, impacting consumer trust and reducing margins. In addition, fluctuations in raw material costs, labor expenses, and logistics costs can create pricing volatility that affects purchasing decisions and profitability across the value chain.

Tennis Apparel Market Opportunities

Expansion in Emerging Tennis Markets

Asia-Pacific presents one of the largest growth opportunities for tennis apparel manufacturers. Countries such as China, India, Indonesia, Vietnam, and Thailand are investing heavily in sports infrastructure and youth development programs. Rising disposable incomes and increasing awareness of health and fitness are encouraging greater participation in tennis. Manufacturers that establish localized supply chains, regional sponsorship agreements, and tailored product offerings are expected to benefit significantly from future market expansion.

Technology-Integrated Performance Apparel

Advanced performance apparel incorporating smart textiles, cooling systems, body-mapping construction, and enhanced compression technologies represents a major growth avenue. Premium consumers increasingly seek apparel that delivers tangible athletic benefits. Brands capable of integrating innovative textile technologies while maintaining comfort and sustainability standards are expected to achieve higher margins and stronger customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.25 Billion |

| Market Size in 2026 | USD 4.53 Billion |

| Market Size in 2031 | USD 6.24 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Tennis tops represent the largest product category, accounting for approximately 31% of global market revenue in 2025. Their dominance is attributed to frequent replacement cycles, broad consumer adoption across professional and recreational players, and their strong crossover appeal within athleisure fashion. Tennis bottoms, including shorts, skirts, skorts, and leggings, constitute another major segment, benefiting from increasing female participation and lifestyle wear adoption. Tennis dresses continue gaining popularity within women's apparel categories, particularly among premium consumers seeking performance and fashion integration. Outerwear products such as jackets, hoodies, and warm-up suits are experiencing growing demand due to year-round usage and off-court wearability. Compression layers, sports bras, and performance accessories are also witnessing steady growth as consumers increasingly prioritize comfort and performance optimization.

Gender Insights

Men's tennis apparel accounted for approximately 42% of global market revenue in 2025, maintaining its position as the leading gender segment due to historically higher participation rates and spending levels. However, women's tennis apparel is emerging as the fastest-growing category globally, supported by rising female participation, expanding professional visibility, and increasing demand for tennis-inspired fashion products. Women's apparel manufacturers are introducing premium collections that combine performance functionality with contemporary design aesthetics. Junior and kids' tennis apparel also presents substantial growth opportunities as youth development programs and academy participation continue expanding across major markets.

Distribution Channel Insights

Sporting goods retail stores remain the largest distribution channel, accounting for approximately 34% of global sales. Consumers continue valuing in-store product evaluation, fitting experiences, and expert recommendations. E-commerce channels represent the fastest-growing distribution segment, driven by convenience, product variety, direct-to-consumer strategies, and digital marketing initiatives. Brand-owned stores remain important for premium positioning and customer engagement, while tennis specialty stores continue serving dedicated players seeking technical expertise and premium product selections. Department stores maintain relevance in mature markets by offering broad consumer accessibility and multi-brand portfolios.

End-User Insights

Recreational tennis players represent the largest end-user segment, accounting for approximately 46% of total market demand. The substantial size of this consumer base reflects the growing popularity of tennis as a fitness and leisure activity worldwide. Competitive amateur players constitute another significant segment, frequently purchasing performance-enhancing apparel and premium product categories. Tennis academies and clubs are among the fastest-growing institutional buyers, driven by increasing enrollment, training programs, and tournament participation. Educational institutions and universities are also expanding tennis programs, creating additional apparel procurement opportunities. Corporate events and branded sports initiatives further contribute to market demand through customized apparel purchases.

Explore more data points, trends and opportunities Download Free Sample Report

Tennis Apparel Market Segmentations

By Product Type

- Tennis Tops

- Tennis Bottoms

- Tennis Dresses

- Outerwear

- Base Layers & Innerwear

- Tennis Socks & Apparel Accessories

By Material Type

- Polyester-Based Apparel

- Nylon-Based Apparel

- Cotton-Based Apparel

- Elastane/Spandex Blends

- Recycled/Sustainable Fibers

- Hybrid Technical Fabrics

By Performance Category

- Competition Apparel

- Training Apparel

- Recreational Tennis Apparel

- Athleisure Tennis Apparel

By Distribution Channel

- Sporting Goods Retail Stores

- Brand-Owned Stores

- Department Stores

- E-Commerce Marketplaces

- Direct-to-Consumer (DTC) Online

- Tennis Specialty Stores

By End User

- Professional Players

- Competitive Amateur Players

- Recreational Players

- Tennis Academies & Clubs

- Schools & Universities

- Corporate & Event Buyers

Regional Insights

North America

North America accounted for approximately 34% of global tennis apparel market revenue in 2025, making it the largest regional market. The United States alone contributes nearly 28% of global demand due to its extensive tennis infrastructure, strong recreational participation, high consumer purchasing power, and premium sportswear adoption. Canada supports regional growth through expanding club memberships and increasing participation among younger demographics. Strong athlete endorsements, tournament visibility, and direct-to-consumer retail channels continue supporting market expansion across the region.

Europe

Europe represented approximately 30% of global market revenue in 2025. Major markets including France, Germany, the United Kingdom, Italy, and Spain maintain strong demand due to established tennis traditions, widespread club participation, and premium sportswear consumption. Sustainability initiatives are particularly influential in Europe, encouraging adoption of recycled-material apparel and environmentally responsible production practices. Grand Slam tournaments and regional tennis events continue generating significant consumer engagement and apparel demand.

Asia-Pacific

Asia-Pacific accounted for approximately 23% of global market revenue and is projected to register the fastest growth rate through 2031. China remains the largest regional market, contributing roughly 9% of global revenue, supported by government-backed sports initiatives and rising middle-class spending. India is emerging as the fastest-growing country market with annual growth exceeding 9%, driven by expanding tennis academies, youth participation programs, and increasing disposable incomes. Japan, South Korea, and Australia continue contributing significant demand through established tennis communities and premium product adoption.

Latin America

Latin America represented approximately 7% of global market demand in 2025. Brazil, Mexico, Argentina, and Chile are the primary contributors, benefiting from growing sports participation and increasing consumer interest in performance apparel. Market growth is supported by expanding retail networks, international tournament exposure, and gradual adoption of premium sportswear brands among middle-income consumers.

Middle East & Africa

The Middle East and Africa accounted for approximately 6% of global market revenue. The United Arab Emirates and Saudi Arabia are investing heavily in sports infrastructure and international sporting events, supporting growing demand for premium tennis apparel. South Africa remains the region's largest market due to established tennis participation and retail distribution networks. Rising investments in sports tourism and recreational facilities are expected to create additional growth opportunities across the region.

Key Players in the Tennis Apparel Market

- Nike Inc.

- Adidas AG

- ASICS Corporation

- Fila Holdings Corp.

- Puma SE

- Under Armour Inc.

- New Balance Athletics Inc.

- Lacoste S.A.

- Wilson Sporting Goods Co.

- Yonex Co. Ltd.

- Lotto Sport Italia S.p.A.

- Mizuno Corporation

- Diadora S.p.A.

- On Holding AG

- Lululemon Athletica Inc.