Teff Market Size

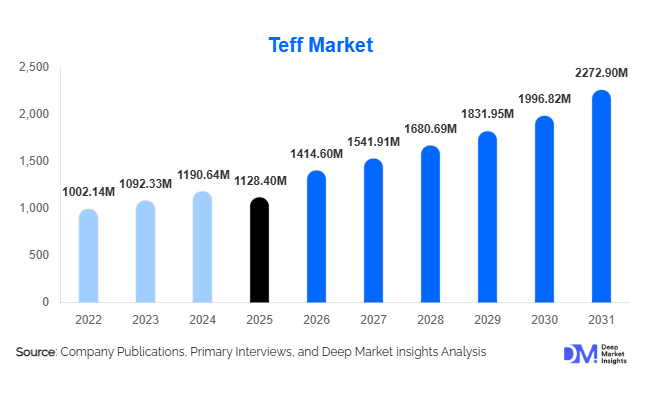

According to Deep Market Insights, the global teff market size was valued at USD 1,128.4 million in 2025 and is projected to grow from USD 1,414.6 million in 2026 to reach USD 2,272.9 million by 2031, expanding at a CAGR of 9.0% during the forecast period (2026–2031). Market expansion is primarily supported by rising global demand for gluten-free grains, increasing adoption of ancient grains in functional foods, and expanding export volumes from East Africa to North America and Europe. Teff, traditionally cultivated in Ethiopia and Eritrea, is transitioning into a premium health grain globally due to its high protein, fiber, iron, and calcium content. Increasing consumer awareness of plant-based nutrition, digestive health, and low glycemic index diets is further strengthening global consumption patterns.

Key Market Insights

- Gluten-free food demand is the strongest growth catalyst, positioning teff as a premium alternative to wheat and refined grains.

- North America leads global imports, driven by health-conscious consumers and specialty bakery innovation.

- Ethiopia remains the dominant producer, accounting for the majority of global cultivation and exports.

- Teff flour represents the largest product segment due to its application flexibility in baking and packaged foods.

- Functional and plant-based food industries are accelerating adoption across cereals, snacks, and nutrition products.

- Digital retail and specialty health stores are improving accessibility in developed markets.

What are the latest trends in the teff market?

Expansion of Ancient Grain-Based Functional Foods

Food manufacturers are increasingly incorporating teff into functional food formulations, including high-protein snack bars, fortified breakfast cereals, gluten-free pasta, and plant-based bakery products. Consumers are shifting toward nutrient-dense grains perceived as minimally processed and sustainable. Teff’s naturally high mineral profile and slow carbohydrate digestion make it attractive for sports nutrition, diabetic-friendly diets, and clean-label products. Product innovation pipelines increasingly feature blends combining teff with quinoa, sorghum, and millet, expanding its usage beyond traditional Ethiopian cuisine into mainstream packaged foods.

Premiumization and Organic Certification Growth

Organic and sustainably sourced teff is gaining traction, particularly in Europe and North America. Retailers are positioning teff as a premium heritage grain, emphasizing traceability, ethical sourcing, and farmer cooperatives. Certification programs are improving export pricing power and increasing farmer income stability. Organic variants command price premiums ranging between 20–35%, supporting higher margins for exporters and processors while reinforcing consumer perception of teff as a superfood ingredient.

What are the key drivers in the teff market?

Rising Gluten-Free and Digestive Health Awareness

The rapid growth of gluten intolerance awareness and lifestyle-driven gluten-free diets is significantly boosting teff demand. Unlike processed gluten substitutes, teff provides natural nutrition density, encouraging adoption among health-focused consumers. Global gluten-free food categories continue expanding within bakery and snack industries, creating sustained ingredient demand.

Growth of Plant-Based Nutrition and Functional Diets

Teff aligns strongly with plant-based dietary patterns due to its amino acid profile and mineral richness. Vegan and vegetarian consumers increasingly seek diversified grain sources beyond rice and oats. Food manufacturers are reformulating products using ancient grains to meet evolving nutritional standards and clean-label expectations.

Export Market Liberalization and Agricultural Support

Government initiatives supporting agricultural exports and improved processing infrastructure in producing regions are enabling higher export volumes. Investments in milling technologies and supply chain modernization are improving quality consistency, encouraging global buyers to integrate teff into commercial food manufacturing.

What are the restraints for the global market?

Supply Concentration and Production Constraints

Global supply remains heavily concentrated in Ethiopia, exposing the market to climate risks, yield variability, and logistics disruptions. Limited mechanization and smallholder farming structures constrain scalability, leading to periodic price volatility.

High Pricing Compared to Conventional Grains

Teff remains significantly more expensive than wheat, corn, or rice due to limited production volumes and export logistics. Price sensitivity among mass-market consumers restricts adoption primarily to premium and health-focused segments, slowing penetration into mainstream food categories.

What are the key opportunities in the teff industry?

Expansion into Ready-to-Eat and Convenience Foods

The global shift toward convenience foods presents strong opportunities for teff-based ready meals, instant porridges, and snack formats. Manufacturers integrating teff into frozen and shelf-stable foods can capture health-conscious urban consumers seeking quick yet nutritious meal solutions.

Government-Led Agricultural Modernization

Public investments in agricultural modernization across East Africa are improving seed quality, irrigation systems, and export logistics. Policies promoting value-added processing within producing countries create opportunities for local milling and branded exports rather than raw grain shipments.

New Applications in Sports and Clinical Nutrition

Teff’s iron and protein content supports growing demand in endurance sports nutrition and medical dietary formulations. Clinical nutrition products targeting anemia prevention and metabolic health represent emerging high-margin application areas for ingredient manufacturers.

Product Type Insights

The global teff market demonstrates strong diversification across product types, although teff flour continues to dominate industry revenues, accounting for approximately 46% of the total market share in 2025. The leadership of teff flour is primarily driven by its exceptional versatility, nutritional density, and compatibility with modern dietary preferences, particularly gluten-free and clean-label food formulations. As consumers increasingly shift toward alternative grains that offer functional health benefits without compromising taste or texture, teff flour has emerged as a preferred ingredient among both households and food manufacturers. Its naturally gluten-free composition, high fiber content, essential amino acids, and mineral richness make it particularly suitable for bakery applications, pancakes, flatbreads, tortillas, and packaged health foods.The growth of gluten intolerance awareness and the expanding diagnosis of celiac disease globally have significantly accelerated demand for teff flour-based products. Food manufacturers are actively reformulating traditional wheat-based products using teff blends to improve nutritional profiles while meeting regulatory gluten-free standards. In addition, the rise of artisanal baking movements and home-based cooking trends has reinforced demand for whole-grain flours, positioning teff flour as a premium alternative to refined grains. Consumers increasingly associate ancient grains with authenticity, sustainability, and superior nutrition, further strengthening adoption.Whole grain teff also maintains a stable and culturally rooted demand, particularly in traditional consumption markets where teff has historically served as a dietary staple. Health-conscious consumers in developed economies are adopting whole grain formats due to growing awareness surrounding minimally processed foods and gut health benefits. Whole grain teff supports slow carbohydrate digestion and improved glycemic response, making it attractive among diabetic and weight-management consumer groups.Meanwhile, ready-to-cook teff mixes are emerging rapidly as a high-growth category aligned with convenience-driven consumption patterns. Urban lifestyles characterized by time constraints are encouraging demand for quick meal solutions that retain nutritional integrity. Ready-to-cook porridges, baking blends, and instant pancake mixes are increasingly marketed toward young professionals and fitness-oriented consumers seeking functional convenience foods.Processed teff ingredients such as flakes, puffed teff, and extruded formats are gaining traction within breakfast cereals and snack applications. Food innovation teams are incorporating puffed teff into granola bars, protein snacks, and fortified cereals to enhance texture while improving micronutrient density. The expansion of healthy snacking culture globally has created favorable conditions for these value-added formats. As manufacturers continue to explore novel processing technologies, product type diversification is expected to remain a major growth catalyst for the global teff industry.

Nature Insights

Based on nature, conventional teff remains the dominant category, accounting for nearly 68% of global market share in 2025, largely due to large-scale agricultural production capacity, cost efficiency, and broader accessibility across price-sensitive markets. Conventional farming methods allow producers to maintain higher yields and stable supply chains, which is essential for meeting growing international demand. The affordability of conventional teff ensures widespread adoption across emerging economies where price remains a critical purchasing factor.The dominance of conventional teff is further supported by expanding food processing applications where manufacturers prioritize consistent raw material availability and scalable sourcing. Large food companies require predictable supply volumes to maintain production continuity, making conventional cultivation the preferred sourcing model. Additionally, infrastructure limitations in several producing regions currently constrain the rapid conversion of farmland to certified organic standards, sustaining conventional production leadership.Despite this dominance, organic teff represents the fastest-growing nature segment, reflecting a broader global transition toward sustainable and pesticide-free food systems. Consumers increasingly evaluate food purchases based on environmental impact, ethical sourcing, and agricultural transparency. Organic certification enhances perceived product quality and strengthens brand positioning within premium retail channels, particularly in North America and Europe.Organic teff is benefiting from rising awareness of soil health preservation and regenerative farming practices. Retailers and specialty food chains are expanding shelf space dedicated to certified organic ancient grains, enabling greater visibility and consumer education. Export-oriented producers are also recognizing the pricing advantages associated with organic certification, which can command significant premiums in international markets.Furthermore, sustainability commitments from multinational food companies are encouraging the integration of organically sourced ingredients into product portfolios. As environmental regulations tighten and consumers demand traceability, organic teff cultivation is expected to expand steadily, supported by investments in farmer training, certification programs, and sustainable agricultural infrastructure.

Application Insights

Across application segments, bakery and confectionery products lead the global teff market with approximately 39% market share in 2025, driven primarily by the rapid expansion of gluten-free baking and artisan food trends. Teff’s fine texture, mild nutty flavor, and superior nutritional profile make it highly suitable for bread, cookies, muffins, cakes, and specialty desserts. The leading driver behind this segment’s dominance is the growing consumer demand for healthier indulgence products that combine taste with functional health benefits.Food manufacturers are increasingly incorporating teff flour into premium baked goods to enhance fiber content, protein levels, and mineral enrichment without relying on artificial fortification. The rise of specialty bakeries focusing on allergen-friendly products has also accelerated adoption. Gluten-free bakery shelves in supermarkets continue to expand globally, supported by improved formulations that overcome earlier challenges related to texture and shelf stability.Breakfast cereals and snack applications are witnessing strong momentum as consumers shift toward nutrient-dense morning meals and portable nutrition solutions. Teff’s high iron and calcium content makes it particularly attractive for fortified cereal formulations aimed at children and health-focused adults. Snack manufacturers are leveraging teff as a clean-label ingredient aligned with natural and minimally processed food positioning.Beverage applications are emerging as an innovative growth area, particularly within plant-based nutrition drinks and functional beverages. Teff-based smoothies, fermented beverages, and grain-based drinks are gaining popularity among consumers seeking dairy alternatives and digestive health support. Nutritional supplement brands are also exploring teff powder as an ingredient in protein blends and meal replacements.Infant nutrition and fortified food applications are gaining traction due to teff’s micronutrient density, including iron and essential amino acids critical for early development. Governments and food organizations in developing regions are increasingly evaluating ancient grains as solutions to address malnutrition challenges. As research continues to validate teff’s nutritional advantages, application expansion is expected to accelerate across multiple food categories.

Distribution Channel Insights

Offline retail channels dominate global teff sales, accounting for nearly 57% of total market revenue, supported by strong consumer trust in physical retail environments and the growing presence of health-focused supermarket sections. Specialty health stores, organic markets, and large supermarket chains play a crucial role in educating consumers through product placement, sampling, and in-store promotions. Many consumers purchasing ancient grains prefer examining product origin labels and certifications physically before buying, reinforcing offline channel dominance.Supermarkets and hypermarkets have significantly expanded their gluten-free and health-food aisles, increasing accessibility to teff products beyond niche specialty outlets. Retail partnerships with premium grain brands have also improved supply consistency and product visibility, encouraging repeat purchases among mainstream consumers.However, online retail represents the fastest-growing distribution channel, fueled by expanding e-commerce penetration and changing consumer purchasing behaviors. Digital platforms allow emerging brands to reach global audiences without extensive physical retail infrastructure. Direct-to-consumer strategies enable companies to communicate product benefits, sourcing stories, and recipes more effectively, enhancing customer engagement.Subscription-based health food delivery services are increasingly introducing teff products to new consumer segments. Personalized nutrition trends and curated wellness boxes often include ancient grains, helping educate first-time buyers and drive trial consumption. Online platforms also support price comparison, broader product variety, and convenient bulk purchasing, factors that continue to accelerate digital sales growth.As omnichannel retail strategies evolve, companies are integrating online and offline experiences through click-and-collect models, digital promotions, and influencer-led marketing campaigns. This integration is expected to reshape distribution dynamics while maintaining strong growth momentum across both channels.

End-Use Insights

Household consumption represents the largest end-use segment within the global teff market, supported by rising home cooking trends, increasing nutrition awareness, and consumer interest in experimenting with ancient grains. The leading driver for this segment is the growing perception of food as a preventive health tool. Consumers are actively incorporating nutrient-rich grains into daily meals to support digestive health, energy management, and balanced diets.The expansion of recipe content across social media platforms and cooking channels has further encouraged household adoption. Home bakers and wellness enthusiasts are exploring teff-based recipes ranging from flatbreads to breakfast bowls, contributing to sustained retail demand. Increased availability of smaller packaging formats has also made teff more accessible to first-time consumers.The food processing industry represents the fastest-growing end-use segment as multinational manufacturers integrate teff into commercial product formulations. The primary growth driver is the food industry’s shift toward functional ingredients that enhance nutritional claims without synthetic additives. Teff enables manufacturers to position products as natural, gluten-free, and nutrient-rich, aligning with evolving labeling requirements and consumer expectations.Foodservice demand is also rising steadily, particularly among health-focused restaurants, vegan cafes, and specialty dining establishments offering gluten-free menus. Chefs are increasingly experimenting with ancient grains to differentiate menus and appeal to wellness-oriented consumers. The inclusion of teff in restaurant offerings plays an important role in consumer awareness, often encouraging retail purchases after dining experiences.

| By Product Type | By Application | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of the global teff market in 2025, making it the leading regional market driven by strong consumer awareness of functional nutrition and gluten-free diets. The United States represents the primary growth engine due to advanced food innovation ecosystems and widespread adoption of plant-based lifestyles. One of the key regional growth drivers is the maturity of the gluten-free food industry, which continuously seeks novel grains capable of improving product differentiation and nutritional performance.Rising health consciousness, increasing cases of gluten intolerance, and expanding wellness-focused retail chains have significantly strengthened teff adoption across the region. Consumers increasingly prioritize whole grains with high mineral content, supporting premium pricing acceptance. Additionally, North America benefits from strong marketing infrastructure and influencer-driven nutrition trends that accelerate awareness of ancient grains.Another critical driver is the expansion of private-label health food brands introducing teff-based products at competitive prices. Food manufacturers are investing heavily in research and development to integrate teff into mainstream packaged foods, ensuring continued regional growth. Imports remain high due to limited domestic production, reinforcing trade relationships with African producing nations.

Europe

Europe holds nearly 27% of global market share, supported by strong demand for organic and sustainably sourced food products. Regional growth is primarily driven by strict food labeling regulations that encourage transparency and nutritional disclosure, favoring ancient grains with measurable health benefits. Countries such as Germany, the United Kingdom, France, and the Netherlands lead consumption due to well-established organic retail networks.The European market benefits significantly from sustainability-focused consumer behavior. Environmental awareness and ethical sourcing considerations encourage the adoption of crops associated with lower processing intensity and traditional agricultural heritage. Organic certification plays a particularly important role in purchasing decisions, accelerating growth within premium product categories.Additionally, Europe’s expanding vegan and plant-based population contributes to increased demand for nutrient-rich grain alternatives. Food manufacturers are introducing innovative bakery and ready-meal solutions incorporating teff to meet evolving dietary preferences. Government initiatives promoting diversified grain consumption for food security further support long-term market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, fueled by rising disposable incomes, urbanization, and growing awareness of functional foods. Increasing prevalence of lifestyle-related conditions such as diabetes has encouraged consumers to explore low-glycemic grain alternatives, positioning teff as an attractive dietary option. India, Australia, Japan, and South Korea are emerging as key demand centers.A major regional growth driver is dietary compatibility, particularly in India where traditional millet consumption creates familiarity with ancient grains. Consumers are increasingly open to experimenting with alternative flours that align with regional cooking styles such as flatbreads and porridges. Government campaigns promoting millet consumption and nutritional diversity indirectly support awareness of teff as a comparable grain.The expansion of e-commerce grocery platforms across Asia-Pacific is also accelerating product accessibility. Imported specialty foods are becoming widely available to urban consumers, enabling rapid market penetration. Rising interest in fitness, wellness, and plant-based diets among younger demographics further strengthens growth prospects.

Middle East & Africa

The Middle East & Africa region serves as the production backbone of the global teff market, led by Ethiopia, Eritrea, and expanding cultivation in Kenya. Ethiopia contributes the majority of global supply, supported by favorable climatic conditions and deep cultural integration of teff within traditional diets. Increasing export demand represents a primary regional growth driver, generating economic incentives for expanded cultivation.Government initiatives aimed at improving agricultural productivity and export infrastructure are strengthening supply chain efficiency. Investments in farming technology, irrigation systems, and farmer cooperatives are improving yields and quality consistency, enabling producers to meet international standards.Urbanization within African economies is also supporting domestic consumption growth as middle-class populations expand and packaged food markets develop. In the Middle East, rising health awareness and demand for gluten-free foods among expatriate populations are creating new import opportunities for teff-based products.

Latin America

Latin America represents a smaller but steadily growing market, led by Brazil and Mexico where health food awareness continues to expand among urban consumers. The key regional growth driver is the rapid expansion of premium retail formats and specialty food imports catering to affluent consumer segments seeking functional nutrition products.Increasing adoption of gluten-free diets, combined with rising interest in plant-based eating patterns, is encouraging retailers to diversify grain offerings. Local food manufacturers are beginning to experiment with teff incorporation into baked goods and snack products, signaling early-stage market development.Improving distribution infrastructure and cross-border trade agreements are expected to enhance product availability across the region. As consumer education increases and awareness of ancient grains grows, Latin America is projected to emerge as a promising long-term growth market within the global teff industry.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Teff Market

- Bob’s Red Mill Natural Foods

- Maskal Teff Company

- Ancient Harvest

- Shiloh Farms

- The Teff Company

- Arrowhead Mills

- Grain Millers Inc.

- Nature’s Path Foods

- Andean Naturals

- Healthy Food Ingredients LLC

- King Arthur Baking Company

- Now Foods

- NutriCargo LLC

- Fieldstone Organics

- Authentic Foods