Tea Bag Market Size

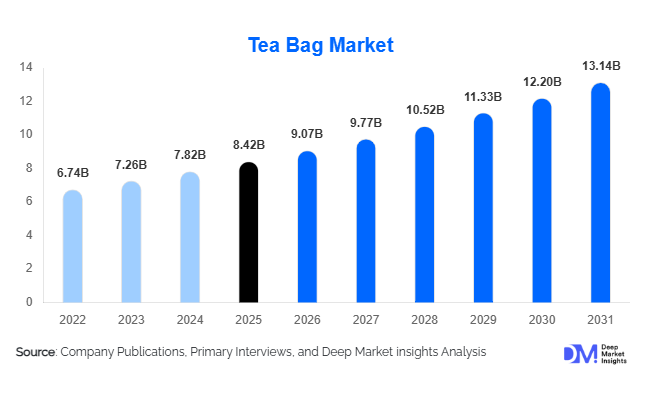

According to Deep Market Insights, the global tea bag market size was valued at USD 8.42 billion in 2025 and is projected to grow from USD 9.07 billion in 2026 to reach USD 13.14 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The tea bag market growth is primarily driven by increasing consumer preference for convenient beverage formats, growing demand for functional and wellness beverages, and rising adoption of premium and sustainable tea products across both developed and emerging economies.

Tea bags continue to dominate packaged tea consumption globally due to their convenience, portion control, portability, and ease of brewing. Urban consumers increasingly prefer tea bags over loose-leaf tea because they align with fast-paced lifestyles and modern retail trends. The market is also benefiting from the expansion of herbal infusions, detox teas, immunity-support beverages, and organic tea products. Premiumization is becoming a major industry trend, particularly in North America, Europe, Japan, and South Korea, where consumers are increasingly willing to pay higher prices for specialty blends, ethically sourced teas, and biodegradable packaging solutions.

The rapid expansion of e-commerce, direct-to-consumer tea brands, and subscription-based beverage models is further accelerating market penetration. Commercial demand from cafés, hotels, airlines, and corporate offices is also supporting growth in premium tea bag formats such as pyramid sachets and individually wrapped products. In addition, sustainability concerns are encouraging manufacturers to transition toward compostable materials and plastic-free tea bags, creating new innovation opportunities within the market.

Key Market Insights

- Functional and wellness tea bags are becoming one of the fastest-growing segments globally, supported by rising demand for immunity, detoxification, digestive health, and stress-relief beverages.

- Premium pyramid tea bags are gaining strong traction, particularly among urban consumers seeking café-style brewing experiences and higher-quality flavor infusion.

- Asia-Pacific dominates the global tea bag market, driven by large-scale tea consumption in China, India, Japan, and Southeast Asia.

- Europe remains a leading premium and sustainable tea bag market, supported by strong consumer preference for organic, biodegradable, and ethically sourced tea products.

- Online retail and direct-to-consumer tea subscriptions are expanding rapidly, enabling specialty tea brands to access international consumer bases.

- Sustainable packaging innovation is reshaping the competitive landscape, with manufacturers investing heavily in compostable materials and plastic-free tea bags.

Tea Bag Market Trends

Rise of Functional and Wellness Tea Bags

Consumers are increasingly shifting toward wellness-oriented beverages that provide health benefits beyond traditional refreshment. Functional tea bags containing ingredients such as turmeric, ginger, chamomile, peppermint, ashwagandha, probiotics, and adaptogenic herbs are witnessing strong demand growth globally. Tea bags positioned for immunity support, stress relief, digestion, sleep improvement, detoxification, and energy enhancement are rapidly expanding across retail shelves. Younger demographics and health-conscious consumers are particularly driving demand for these products, positioning wellness teas as one of the fastest-growing categories in the global tea bag market. Manufacturers are also introducing sugar-free, caffeine-free, and organic formulations to align with broader healthy lifestyle trends.

Sustainable and Plastic-Free Tea Bag Innovation

Environmental sustainability has emerged as a major trend influencing tea bag manufacturing globally. Consumers are increasingly aware of concerns related to microplastic contamination from conventional nylon-based tea bags, prompting manufacturers to transition toward biodegradable and compostable alternatives. Tea companies are investing heavily in plant-based fibers, PLA materials, recyclable cartons, and carbon-neutral packaging systems to strengthen sustainability positioning. European markets, particularly Germany, the U.K., and Nordic countries, are leading demand for eco-friendly tea packaging solutions. Many premium brands are also emphasizing fair-trade sourcing, regenerative tea farming, and transparent supply chains to attract environmentally conscious consumers. Sustainability-focused product innovation is expected to remain a defining market trend through the forecast period.

Tea Bag Market key Drivers

Growing Preference for Convenient Beverage Consumption

Rapid urbanization, busy lifestyles, and rising working populations are significantly increasing consumer preference for convenient beverage solutions. Tea bags provide a simple and time-efficient brewing process compared to loose-leaf tea, making them highly suitable for modern households, offices, and commercial foodservice establishments. Consumers increasingly value portability, portion control, and ease of disposal, particularly in urban markets across Asia-Pacific and North America. Convenience-driven demand has also strengthened adoption of individually wrapped tea bags, instant infusion formats, and on-the-go beverage products.

Expansion of Premium and Specialty Tea Consumption

The global tea industry is witnessing strong premiumization trends, with consumers increasingly seeking gourmet tea experiences comparable to specialty coffee culture. Premium tea bags featuring exotic flavors, single-origin teas, organic ingredients, artisanal blending, and pyramid infusion technology are experiencing rapid growth. Premium hospitality chains, cafés, and wellness-focused retailers are further driving demand for luxury tea products. Consumers are also demonstrating greater willingness to pay premium prices for ethically sourced and sustainable tea products, enabling manufacturers to achieve stronger margins and brand differentiation.

Tea Bag Market Restraints

Volatility in Raw Material Prices

Fluctuating prices of tea leaves, packaging materials, transportation, and biodegradable fibers remain major challenges for tea bag manufacturers. Climatic uncertainties, labor shortages, geopolitical disruptions, and agricultural supply fluctuations in major tea-producing countries such as India, Sri Lanka, Kenya, and China continue affecting production costs. Rising energy and logistics expenses further pressure operating margins, especially for smaller and mid-sized manufacturers with limited pricing flexibility.

Regulatory Pressure on Packaging Materials

Governments and environmental agencies are increasingly scrutinizing the use of synthetic materials in tea bags due to concerns over plastic waste and microplastic contamination. Manufacturers using nylon and non-biodegradable materials face growing regulatory compliance requirements, particularly in Europe and North America. Transitioning toward compostable alternatives often involves higher production costs, new machinery investments, and supply chain restructuring. Smaller players may face difficulties adapting to these sustainability-driven regulatory changes, potentially limiting market competitiveness.

Tea Bag Market Opportunities

Growth of E-Commerce and Direct-to-Consumer Tea Brands

The rapid expansion of online grocery platforms and direct-to-consumer beverage brands presents significant growth opportunities for tea bag manufacturers. Digital channels allow specialty tea companies to reach international customers without relying heavily on traditional retail distribution networks. Personalized tea subscriptions, curated wellness tea kits, and premium gifting collections are increasingly popular among urban consumers. Online retailing also enables brands to educate consumers regarding tea origins, brewing techniques, wellness benefits, and sustainability initiatives, strengthening customer engagement and loyalty.

Expansion of Premium Hospitality and Café Tea Offerings

The growing importance of premium beverage experiences in hotels, cafés, restaurants, airlines, and luxury hospitality environments is creating strong opportunities for high-end tea bag products. Premium pyramid tea bags, artisanal blends, and organic infusions are increasingly replacing conventional tea offerings within upscale foodservice channels. Luxury hospitality brands are positioning specialty tea programs as part of broader wellness and lifestyle experiences, encouraging suppliers to develop customized premium tea solutions for commercial applications.

Tea Type Insights

The global tea bag market continues to be strongly influenced by evolving consumer preferences across traditional, wellness-oriented, and premium beverage categories. Among all tea types, black tea bags continue to maintain a dominant position in the global market, accounting for nearly 38% of total market value in 2025. The leadership of black tea bags is closely associated with deeply rooted tea consumption habits across major tea-drinking nations including the U.K., India, Turkey, Russia, and several Middle Eastern countries where tea remains a part of daily cultural and social routines. Black tea bags continue to benefit from strong affordability, easy accessibility through supermarkets and convenience stores, and widespread consumer familiarity across both developed and emerging economies. The segment is further supported by the growing popularity of breakfast tea blends, milk tea preparations, and flavored black tea variants that appeal to a broad demographic base. In commercial applications, black tea bags remain highly preferred by hotels, restaurants, airlines, and office spaces because they offer consistent taste profiles, ease of storage, and quick brewing convenience.Fruit-infused tea bags and specialty blends are also gaining momentum, particularly among millennials and Gen Z consumers who are actively seeking flavor innovation and premium beverage experiences. Exotic fruit flavors, floral blends, seasonal infusions, and dessert-inspired teas are helping manufacturers diversify product portfolios and improve brand differentiation. The premiumization trend across the global beverage industry is further encouraging the development of artisanal tea bag products using single-origin teas, organic ingredients, and ethically sourced botanicals. As consumers continue shifting toward healthier and more experiential beverages, tea type diversification is expected to remain one of the strongest growth drivers for the global tea bag market during the forecast period.

Bag Type Insights

The bag type segment of the tea bag market continues to evolve significantly as manufacturers increasingly focus on brewing efficiency, visual appeal, product differentiation, and premium consumer experiences. Pyramid tea bags are becoming increasingly popular within premium and specialty tea categories due to their superior infusion performance and ability to accommodate larger tea leaves, herbs, flowers, and fruit ingredients. Unlike conventional flat tea bags, pyramid-shaped designs allow tea leaves to expand more freely during brewing, resulting in improved flavor extraction, enhanced aroma release, and stronger visual presentation. The segment is witnessing particularly strong adoption within premium retail channels, luxury hospitality sectors, and specialty wellness tea categories where consumers are willing to pay higher prices for enhanced quality and brewing performance.Double-chamber tea bags continue to maintain a strong presence within the mass-market segment due to their cost-effectiveness and efficient brewing characteristics. These tea bags provide faster infusion while supporting large-scale automated manufacturing processes, making them highly attractive for mainstream commercial tea brands. Manufacturers continue utilizing double-chamber designs for high-volume retail products because they balance affordability, functionality, and production efficiency. While premium formats are gaining traction globally, conventional tea bag structures continue to dominate overall volume sales due to strong affordability and consumer familiarity in emerging markets.

Material Type Insights

Material innovation has become an increasingly important factor shaping the competitive landscape of the global tea bag market as sustainability concerns continue influencing both consumer purchasing behavior and regulatory frameworks. Paper tea bags remain the dominant material category due to their affordability, scalability, lightweight properties, and compatibility with high-speed manufacturing systems. Paper-based tea bags are widely used across mainstream tea brands because they support efficient mass production while maintaining relatively low packaging costs. Their extensive adoption across supermarkets, hypermarkets, and commercial retail channels continues supporting segment leadership globally.Nylon and silk tea bags continue to maintain a presence within premium and luxury tea categories because of their transparency, aesthetic appeal, and superior brewing efficiency. These materials enhance product presentation by allowing consumers to visually observe high-quality tea leaves, flowers, and fruit ingredients inside the bag. Premium hospitality brands and specialty tea retailers continue utilizing silk and nylon materials to strengthen premium brand positioning and elevate consumer experiences. Nevertheless, long-term growth potential for synthetic tea bag materials may face limitations due to increasing environmental concerns and shifting consumer preferences toward sustainable alternatives. As sustainability becomes a central priority across the global food and beverage packaging industry, material innovation will remain a critical driver influencing future market competitiveness.

Distribution Channel Insights

Distribution channel dynamics within the global tea bag market are evolving rapidly due to changing shopping behaviors, digital commerce expansion, and growing consumer demand for convenience. Supermarkets and hypermarkets continue to dominate global tea bag sales, accounting for approximately 44% of total market revenue in 2025. Their leadership position is supported by broad product availability, strong shelf visibility, promotional pricing strategies, and extensive geographic reach. Large retail chains continue serving as the primary purchasing destination for mainstream tea consumers because they provide convenient access to multiple tea brands, flavors, price categories, and packaging formats under a single retail environment.Specialty tea stores and wellness retailers are also gaining increasing importance within premium and functional tea categories. These retail channels attract consumers seeking artisanal products, wellness-oriented formulations, organic certifications, and educational tea experiences. The growing popularity of premium gifting, tea tasting culture, and experiential retail concepts is further supporting expansion within specialty retail formats. As digital commerce continues expanding and consumers increasingly seek personalized beverage experiences, omnichannel retail strategies are expected to become increasingly important across the global tea bag market.

End-Use Insights

Residential households remain the largest end-use segment within the global tea bag market, accounting for nearly 63% of total demand in 2025. Strong household consumption patterns, increasing preference for convenient beverages, and rising at-home consumption trends continue supporting segment dominance. Tea bags are highly preferred in residential applications because they offer quick preparation, consistent flavor, minimal cleanup, and wide product variety. The increasing popularity of remote work and home-based lifestyles has further contributed to rising household tea consumption across multiple regions.Institutional demand from hospitals, wellness centers, educational institutions, and corporate facilities is also increasing steadily. Herbal and caffeine-free tea bags are gaining popularity within healthcare and wellness environments due to growing emphasis on relaxation, hydration, and preventive wellness. Corporate offices are increasingly incorporating tea stations and wellness beverage programs as part of employee wellness initiatives, further contributing to commercial market expansion. As consumer lifestyles continue evolving toward convenience and wellness-oriented consumption, both residential and institutional demand are expected to remain important long-term growth drivers.

Price Range Insights

Mid-range tea bag products continue to dominate global sales volumes due to their strong balance between affordability, product quality, and accessibility. Mainstream consumers across both developed and emerging economies continue preferring mid-priced tea products because they provide reliable taste, broad flavor options, and convenient availability through mass retail channels. Large multinational tea brands continue focusing heavily on the mid-range category because it supports high sales volumes and strong market penetration across diverse demographic groups.Luxury tea bag products featuring rare tea origins, handcrafted blends, aesthetically designed packaging, and gifting-oriented presentation are becoming increasingly important within hospitality, corporate gifting, and festive consumption applications. Premiumization trends remain particularly strong in North America, Europe, Japan, South Korea, and affluent urban markets across the Middle East and Asia-Pacific. Higher-income consumers are increasingly viewing premium tea consumption as part of broader wellness, lifestyle, and experiential consumption patterns.Economy tea bags continue to maintain substantial market relevance in emerging economies where affordability remains a major purchasing factor. Large population bases, price-sensitive consumers, and strong daily tea consumption patterns continue supporting demand for low-cost tea products across parts of Asia, Africa, and Latin America. Manufacturers operating within economy categories continue emphasizing value pricing, high-volume packaging, and widespread distribution to maintain competitive market positioning.

| By Tea Type | By Bag Type | By Material Type | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 19% of the global tea bag market and continues to represent a highly dynamic growth region led primarily by the United States and Canada. Rising consumer preference for healthier beverage alternatives is one of the most significant drivers supporting regional market expansion. Consumers are increasingly shifting away from sugary carbonated beverages toward herbal teas, detox blends, green teas, and functional wellness infusions that align with broader health and fitness trends. Growing awareness regarding immunity enhancement, stress management, digestive wellness, and sleep support is substantially increasing demand for functional tea bag products across the region.

Europe

Europe represents nearly 29% of global tea bag market revenue and remains one of the most mature and sophisticated tea consumption regions worldwide. The region’s growth is strongly supported by deeply established tea-drinking traditions, particularly in countries such as the United Kingdom, Germany, Russia, and France. The U.K. continues to maintain exceptionally high per-capita tea consumption, where black tea remains an essential part of everyday culture and household routines. Germany remains a major growth center for herbal, organic, and wellness-oriented tea products due to rising health consciousness and strong consumer preference for natural remedies.The region’s well-developed retail infrastructure, strong purchasing power, and expanding wellness culture continue supporting steady market growth. Rising café culture, premium hospitality expansion, and increasing interest in functional beverages are further contributing to higher consumption of herbal, fruit-infused, and specialty tea products across Europe.

Asia-Pacific

Asia-Pacific dominates the global tea bag market with approximately 41% market share in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. The region benefits from a combination of large population bases, deeply rooted tea-drinking traditions, expanding urbanization, and strong tea production capabilities. China and India continue to represent the world’s largest tea-producing and tea-consuming countries, supported by substantial domestic demand and rapidly expanding organized retail networks.Japan and South Korea continue witnessing strong demand for green tea, matcha, and functional wellness beverages driven by high health awareness and established tea consumption cultures. Southeast Asian markets are also emerging as highly attractive growth opportunities due to increasing café culture expansion, tourism development, and rising consumer exposure to international beverage trends. India is expected to remain one of the fastest-growing national markets owing to increasing urban tea consumption, rapid e-commerce expansion, and growing adoption of premium packaged tea products among younger consumers.

Latin America

Tea bag consumption is steadily expanding across Latin America, particularly in Brazil, Argentina, Chile, and Mexico. Regional market growth is being driven by increasing health awareness, rising urbanization, and growing consumer interest in healthier beverage alternatives. Consumers are increasingly adopting herbal teas, fruit infusions, and wellness beverages as part of broader lifestyle and dietary improvements. Expanding café culture and rising exposure to international food and beverage trends are also supporting greater adoption of packaged tea products across urban populations.

Middle East & Africa

The Middle East & Africa region is witnessing rising tea bag demand supported by strong tea-drinking traditions, population growth, urbanization, and expanding hospitality industries. Tea remains deeply integrated into social and cultural practices across several countries within the region, supporting consistent baseline consumption. Turkey continues to rank among the world’s highest tea-consuming countries, while Saudi Arabia and the UAE are emerging as important premium tea consumption hubs due to growing luxury hospitality investments, rising disposable incomes, and increasing wellness beverage adoption.South Africa continues witnessing increasing demand for herbal and rooibos tea products due to growing consumer awareness regarding natural wellness beverages and locally sourced ingredients. Across several African markets, improving retail infrastructure, increasing packaged food consumption, and expanding middle-class populations are gradually supporting tea bag market penetration. As urbanization and modern retail development continue progressing across the region, the Middle East & Africa market is expected to witness steady long-term expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Tea Bag Market

- Unilever

- Tata Consumer Products

- Associated British Foods

- ITO EN

- Bigelow Tea Company

- Twinings

- Dilmah Ceylon Tea Company

- Celestial Seasonings

- Yogi Tea

- Harney & Sons

- The Republic of Tea

- Teekanne

- Ahmad Tea

- Barry's Tea

- Vahdam India