Taurine (Infant Grade) Market Size

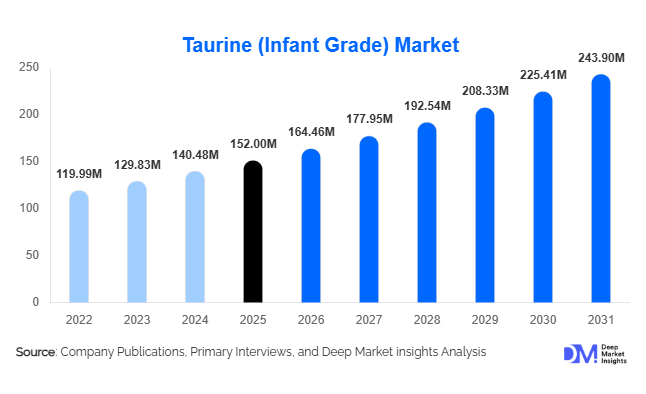

According to Deep Market Insights,the global taurine (infant grade) market size was valued at USD 152 million in 2025 and is projected to grow from USD 164.46 million in 2026 to reach USD 243.90 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The market growth is primarily driven by rising global demand for premium infant formula, increasing regulatory emphasis on fortified pediatric nutrition, and expanding neonatal healthcare infrastructure across emerging economies. As taurine is a conditionally essential amino sulfonic acid present in human breast milk, its inclusion in infant formula is widely recommended and regulated in several countries, reinforcing stable long-term demand for ultra-high purity infant-grade variants.

Key Market Insights

- Ultra-high purity (≥99.9%) taurine dominates demand, driven by stringent infant nutrition safety and pharmacopeial standards.

- Asia Pacific leads the global market, accounting for over 40% of 2025 demand, supported by strong infant formula consumption in China and India.

- Direct B2B supply contracts account for more than two-thirds of sales, reflecting long-term procurement agreements with infant formula manufacturers.

- Bio-fermentation production is the fastest-growing segment, gaining traction due to sustainability and ESG compliance goals.

- Specialty and medical infant nutrition are expanding rapidly, particularly in NICU and preterm infant applications.

- Top five manufacturers control approximately 58% of global supply, indicating moderate consolidation and strong quality barriers.

What are the latest trends in the taurine (infant grade) market?

Premiumization and Clean-Label Infant Nutrition

Infant formula brands are increasingly emphasizing clean-label positioning, traceability, and pharmaceutical-grade purity in ingredient sourcing. Taurine suppliers are responding by investing in advanced purification systems, heavy metal reduction technologies, and compliance with USP, EP, and Chinese pharmacopeial standards. Manufacturers offering non-GMO, allergen-controlled, and fully traceable taurine are securing long-term supply contracts with global infant nutrition brands. This premiumization trend is enabling higher pricing benchmarks and improved margins across the value chain.

Shift Toward Sustainable and Bio-Based Production

Environmental scrutiny around petrochemical-based synthesis routes has accelerated research into microbial fermentation-based taurine production. Bio-fermentation reduces carbon intensity and aligns with sustainability commitments of multinational infant formula producers. Several Asian manufacturers are piloting fermentation facilities to differentiate their offerings and meet ESG-driven procurement requirements. As sustainability reporting becomes mandatory in many developed markets, environmentally compliant taurine production is emerging as a competitive advantage.

What are the key drivers in the taurine (infant grade) market?

Growth in Global Infant Formula Consumption

Urbanization, rising disposable incomes, and increasing participation of women in the workforce are driving higher reliance on packaged infant nutrition. Asia Pacific remains the largest contributor to formula consumption growth, particularly China, where premium and specialty formulas are gaining traction. Since taurine is routinely added to mimic breast milk composition, higher formula volumes directly translate into increased taurine demand.

Stringent Regulatory Standards for Infant Nutrition

Regulatory bodies across North America, Europe, and Asia mandate strict compositional standards for infant formula, including controlled amino acid profiles. Compliance requirements elevate the need for pharmaceutical-grade taurine with validated purity and safety. These regulations create high entry barriers, benefiting established players with certified production facilities.

What are the restraints for the global market?

Raw Material Price Volatility

Taurine production via chemical synthesis relies on petrochemical intermediates such as ethylene oxide and monoethanolamine. Fluctuations in crude oil and energy prices directly affect manufacturing costs, compressing margins for suppliers without backward integration.

Complex Regulatory Approval Processes

Infant-grade ingredients require extensive documentation, stability testing, and multi-jurisdiction approvals. Smaller manufacturers face capital-intensive validation requirements, which can delay commercialization and restrict new market entry.

What are the key opportunities in the taurine (infant grade) industry?

Expansion in Emerging Infant Nutrition Markets

Countries such as India, Indonesia, Brazil, and Saudi Arabia are witnessing rapid expansion in packaged infant nutrition consumption. Local production incentives under initiatives like “Make in India” and “Made in China 2025” are encouraging domestic amino acid manufacturing, creating partnership opportunities for global taurine producers.

Specialty and Clinical Infant Nutrition

Preterm infant survival rates are improving globally due to advanced neonatal care. Specialty formulas for premature and low-birth-weight infants require enhanced taurine inclusion, supporting higher per-unit demand. Hospitals and NICU-focused formula brands are emerging as high-value procurement channels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 152 Million |

| Market Size in 2026 | USD 164.46 Million |

| Market Size in 2031 | USD 243.90 Million |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Production Process Insights

Chemical synthesis through the monoethanolamine route continues to dominate the global infant-grade taurine market, accounting for approximately 62% of the 2025 global market share. The leadership of this segment is primarily driven by its established large-scale manufacturing infrastructure, cost efficiency, and consistent output quality that aligns with stringent infant nutrition regulatory frameworks. Manufacturers favor this route due to its proven industrial scalability, optimized yield rates, and predictable impurity control profiles, which are critical for meeting pharmaceutical-grade and infant-grade standards. Additionally, regulatory familiarity across major markets has reduced compliance complexities for chemically synthesized taurine, reinforcing its widespread adoption among established suppliers.

Meanwhile, bio-fermentation is emerging as the fastest-growing production process segment. Its expansion is fueled by sustainability-focused procurement strategies adopted by multinational infant formula manufacturers seeking cleaner-label positioning and reduced carbon footprints. Increasing environmental regulations and growing consumer preference for naturally derived ingredients are encouraging investments in biotechnology-driven production methods. Although currently smaller in share compared to chemical synthesis, bio-fermentation is expected to gain traction as production efficiencies improve and cost parity narrows.

Purity Level Insights

Ultra-high purity taurine (≥99.9%) holds nearly 48% of the 2025 market share, making it the leading purity segment. The dominance of this category is driven by tightening global regulations surrounding infant nutrition safety, particularly regarding heavy metals, residual solvents, and trace contaminants. Premium and specialty infant formula manufacturers increasingly prioritize ultra-high purity inputs to ensure compliance with evolving safety benchmarks and to strengthen brand positioning in competitive markets. As regulatory bodies continue to enforce stricter contaminant thresholds and traceability requirements, procurement strategies are shifting toward higher purity grades to minimize recall risks and ensure consistent product performance.

Form Insights

Crystalline powder form accounts for approximately 71% of the global market in 2025, maintaining its position as the dominant format. The segment’s leadership is primarily attributed to its superior stability, extended shelf life, and compatibility with dry-blend infant formula manufacturing processes. Powdered taurine integrates seamlessly into automated mixing systems, enabling uniform dispersion and precise dosage control during large-scale production. Its ease of storage, lower transportation risk compared to liquid formats, and reduced susceptibility to microbial contamination further enhance its preference among infant nutrition manufacturers worldwide.

Application Insights

Standard cow milk-based infant formula represents around 52% of the global demand in 2025, making it the leading application segment. The dominance of this category is driven by its widespread affordability, established clinical acceptance, and large-scale commercial availability across both developed and emerging markets. Taurine plays a vital role in supporting neurological and visual development in infant formulations, reinforcing its consistent inclusion in mainstream products.

At the same time, specialty formulas designed for lactose intolerance, cow milk protein allergy, and premature infants are expanding at a faster pace. Growth in these subsegments is supported by rising clinical nutrition awareness, improved neonatal diagnostics, and increasing parental willingness to adopt targeted nutritional solutions. As healthcare providers emphasize personalized infant nutrition, taurine demand is expected to rise in specialized therapeutic formulations.

Distribution Channel Insights

Direct B2B supply agreements account for nearly 67% of total sales, establishing this channel as the dominant distribution mode. The leadership of direct contracts is driven by infant formula manufacturers’ preference for long-term procurement arrangements that ensure quality consistency, supply chain reliability, and regulatory compliance. Taurine, being a critical micronutrient in infant formulations, requires strict batch traceability and documentation standards, which are more effectively managed through direct supplier relationships. Strategic partnerships, multi-year contracts, and integrated quality audits further strengthen the prominence of the B2B procurement model in this market.

End-Use Industry Insights

Infant nutrition manufacturers account for over 80% of total infant-grade taurine consumption, solidifying their position as the primary end-use industry. The segment’s dominance is supported by mandatory taurine fortification standards in many infant formula regulations and increasing premiumization trends in early-life nutrition products. Pediatric clinical nutrition is the fastest-growing end-use segment, expanding at nearly 9% annually, driven by rising preterm birth rates, specialized neonatal care advancements, and hospital-based nutritional supplementation programs.

Export-driven infant formula production in countries such as :contentReference[oaicite:0]{index=0} and :contentReference[oaicite:1]{index=1} further amplifies taurine procurement volumes, as manufacturers in these nations serve high-demand Asian markets. Emerging applications, including fortified baby cereals and early-life nutraceutical sachets, are gradually diversifying taurine utilization beyond traditional formula products.

Explore more data points, trends and opportunities Download Free Sample Report

Taurine (Infant Grade) Market Segmentations

By Production Process

- Chemical Synthesis

- Bio-Fermentation

By Form

- Crystalline Powder

- Granular

- Liquid Solution

By Application

- Standard Infant Formula

- Follow-On Formula

- Specialty Infant Formula

- Fortified Baby Foods & Early-Life Nutraceuticals

By Distribution Channel

- Direct B2B Supply to Infant Formula Manufacturers

- Contract Manufacturing & Private Label Supply

- Specialty Ingredient Distributors

By End-Use Industry

- Infant Nutrition Manufacturers

- Pediatric Clinical Nutrition Companies

- Medical & NICU Feeding Solution Providers

Regional Insights

Asia Pacific

Asia Pacific holds approximately 41% of the 2025 global market share, positioning it as the leading regional market. The region’s dominance is driven by high birth rates in developing economies, rapid urbanization, rising disposable incomes, and strong premium infant formula penetration. :contentReference[oaicite:2]{index=2} alone contributes nearly 24% of global demand, supported by regulatory standardization, increasing trust in premium packaged infant nutrition, and strong cross-border formula trade. Government reforms aimed at improving domestic production quality have also strengthened demand for high-purity taurine.

:contentReference[oaicite:3]{index=3} is the fastest-growing market in the region, driven by expanding middle-class populations, increasing female workforce participation, greater neonatal nutrition awareness, and improved distribution of packaged infant formula in urban and semi-urban areas. Southeast Asian countries are also contributing to incremental demand growth due to rising healthcare access and expanding retail infrastructure.

North America

North America accounts for around 23% of global demand in 2025, with the :contentReference[oaicite:4]{index=4} representing approximately 19%. The region’s steady demand is underpinned by stringent infant nutrition regulations, high specialty formula adoption rates, and advanced neonatal healthcare systems. Increasing demand for hypoallergenic, organic, and clinically enhanced infant formulas continues to sustain taurine consumption. Strong research and development investments by leading nutrition companies further reinforce procurement volumes across the region.

Europe

Europe represents roughly 21% of global consumption, led by :contentReference[oaicite:5]{index=5}, :contentReference[oaicite:6]{index=6}, :contentReference[oaicite:7]{index=7}, and :contentReference[oaicite:8]{index=8}. Regional growth is supported by well-established regulatory frameworks, high-quality manufacturing standards, and strong export-oriented infant formula production. European manufacturers play a critical role in supplying Asian markets, particularly for premium and specialty products, thereby elevating taurine procurement levels. Sustainability initiatives and traceability requirements are also encouraging adoption of ultra-high purity and bio-fermented taurine across the region.

Latin America

Latin America accounts for about 7% of the global market, with :contentReference[oaicite:9]{index=9} and :contentReference[oaicite:10]{index=10} leading regional consumption. Brazil is the fastest-growing country in the region, driven by rising urban populations, expanding modern retail channels, and increasing adoption of packaged infant nutrition products. Improving healthcare awareness and government-supported maternal nutrition programs are further contributing to steady market expansion.

Middle East & Africa

The Middle East & Africa region holds nearly 8% of the global share, with :contentReference[oaicite:11]{index=11} and the :contentReference[oaicite:12]{index=12} leading demand. Growth in this region is driven by high per-capita formula consumption, strong purchasing power in Gulf Cooperation Council countries, and heavy reliance on imported premium infant nutrition products. Increasing hospital infrastructure development, expanding expatriate populations, and growing awareness of early-life nutritional supplementation are further supporting taurine demand across key regional markets.

Key Players in the Taurine (Infant Grade) Market

- Yantai Yongan Pharmaceutical Co., Ltd.

- Jiangyin Huachang Food Additive Co., Ltd.

- Grand Pharma (China) Co., Ltd.

- Honjo Chemical Corporation

- Qianjiang Yongan Pharmaceutical Co., Ltd.

- Taisho Pharmaceutical Co., Ltd.

- Kyowa Hakko Bio Co., Ltd.

- Hubei Grand Life Science & Technology Co., Ltd.

- Shandong Xinhua Pharmaceutical Company Limited

- Zhejiang NHU Co., Ltd.

- Ajinomoto Co., Inc.

- Dongxiao Biotechnology Co., Ltd.

- Hunan Jiudian Pharmaceutical Co., Ltd.

- Sinoway Industrial Co., Ltd.

- Atlantic Chemicals Trading GmbH