Tartaric Acid Market Size

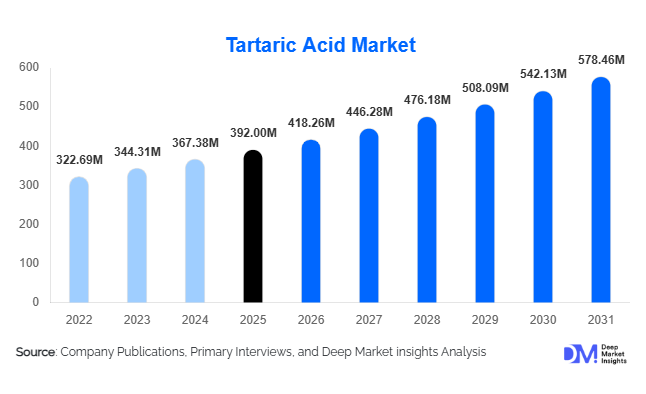

According to Deep Market Insights, the global tartaric acid market size was valued at USD 392 million in 2025 and is projected to grow from USD 418.26 million in 2026 to reach USD 578.46 million by 2031, expanding at a CAGR of 6.7% during the forecast period (2026–2031). The tartaric acid market growth is primarily driven by rising demand for natural food acidulants, increasing global wine production, expanding pharmaceutical manufacturing, and growing adoption of bio-based specialty chemicals across industrial applications. The market benefits from tartaric acid’s multifunctional properties as an acidity regulator, stabilizer, antioxidant, and chelating agent used widely in food processing, pharmaceuticals, cosmetics, and construction chemicals.

Key Market Insights

- Natural tartaric acid dominates global demand, supported by clean-label food trends and regulatory preference for naturally derived ingredients.

- Food and beverage applications account for the largest consumption share, driven by bakery, confectionery, and beverage acidulation needs.

- Europe leads global production due to strong wine industries in Italy, Spain, and France.

- Asia-Pacific is the fastest-growing regional market, supported by pharmaceutical manufacturing expansion and processed food consumption.

- Pharmaceutical-grade tartaric acid is emerging as a high-margin segment owing to rising demand for excipients and chiral intermediates.

- Sustainability and winery waste valorization are reshaping supply chains and improving circular economy adoption.

What are the latest trends in the tartaric acid market?

Shift Toward Natural and Bio-Based Acidulants

Food manufacturers worldwide are transitioning toward natural additives to meet consumer demand for clean-label and minimally processed ingredients. Tartaric acid derived from grape by-products aligns with sustainability goals and regulatory approvals across major markets. Producers are increasingly investing in traceable sourcing models linked directly to wineries, ensuring stable raw material supply while reducing environmental waste. Organic-certified tartaric acid variants are gaining popularity among premium food brands, particularly in Europe and North America. This trend is strengthening long-term demand while enabling manufacturers to command premium pricing compared to synthetic alternatives.

Technological Advancements in Extraction and Purification

Technological innovation is improving efficiency across tartaric acid production. Advanced crystallization, membrane filtration, and solvent recovery systems are enhancing yield while reducing production costs and environmental impact. Automation in processing plants is improving product consistency required for pharmaceutical-grade applications. Companies are also integrating digital monitoring tools to optimize fermentation residues and winery waste recovery processes. These technological improvements are enabling manufacturers to diversify into higher-purity grades and expand applications in pharmaceuticals and specialty chemicals.

What are the key drivers in the tartaric acid market?

Growth in Processed Food and Beverage Consumption

Rapid urbanization and changing dietary habits are increasing consumption of processed foods, baked goods, and functional beverages. Tartaric acid plays a crucial role as a flavor enhancer and acidity regulator, particularly in bakery leavening systems and beverage stabilization. Expansion of packaged food exports from Asia-Pacific countries has significantly increased industrial demand for food-grade tartaric acid, making food processing the largest application segment globally.

Expansion of Global Wine Production

The wine industry remains a primary source and consumer of tartaric acid. Rising wine production in Europe, South America, Australia, and parts of Asia is boosting recovery of potassium bitartrate and supporting market growth. Premium wine consumption trends are encouraging producers to invest in stabilization technologies, further strengthening demand for high-quality tartaric acid derivatives.

Rising Pharmaceutical Manufacturing Activities

Tartaric acid is widely used in pharmaceutical formulations, including effervescent tablets and chiral drug synthesis. Growth of generic drug manufacturing hubs in India and Southeast Asia is accelerating demand for pharmaceutical-grade variants. Increasing nutraceutical production and functional medicine adoption are further supporting consumption growth.

What are the restraints for the global market?

Dependence on Agricultural Raw Materials

Tartaric acid production is closely linked to grape harvest volumes, making supply vulnerable to climate variability and agricultural fluctuations. Poor harvest seasons can increase raw material costs and create pricing volatility across global markets. This dependency remains one of the primary operational risks for producers.

Competition from Alternative Organic Acids

Lower-cost acidulants such as citric and malic acid compete strongly in beverage and industrial applications. Manufacturers may substitute tartaric acid based on price sensitivity, particularly in mass-market products, limiting penetration in cost-driven segments.

What are the key opportunities in the tartaric acid industry?

Pharmaceutical and High-Purity Grade Expansion

The pharmaceutical sector presents strong opportunities as drug manufacturers increasingly require high-purity excipients and chiral resolving agents. Investments in pharmaceutical-grade production facilities can significantly improve margins, as these products command higher pricing compared to industrial grades.

Circular Economy and Winery Integration

Integration with wineries for by-product recovery is creating sustainable business models. Producers adopting waste valorization strategies can secure raw material supply while reducing environmental impact. Governments in Europe and Asia are encouraging such bio-based production systems through sustainability incentives and industrial modernization programs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 392 Million |

| Market Size in 2026 | USD 418.26 Million |

| Market Size in 2031 | USD 578.46 Million |

| CAGR | 6.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural tartaric acid continues to dominate the global tartaric acid market, accounting for nearly 62% of total market share in 2025. This leadership position is primarily supported by growing consumer preference for clean-label and naturally derived ingredients across food, beverage, and pharmaceutical applications. Increasing regulatory acceptance of bio-based additives, particularly in Europe and North America, has further strengthened adoption as manufacturers prioritize transparency, sustainability, and traceability within ingredient sourcing. The expansion of winery by-product valorization has also enhanced supply availability, allowing producers to recover tartaric acid from grape residues while supporting circular economy initiatives. As sustainability becomes a central procurement criterion for multinational food companies, demand for naturally sourced tartaric acid is expected to accelerate steadily.Synthetic tartaric acid remains relevant in industrial and technical applications where cost efficiency, consistent purity levels, and scalable production are critical factors. Industries such as construction chemicals, electroplating, and specialty manufacturing continue to rely on synthetic variants due to predictable supply chains and lower production costs. Meanwhile, cream of tartar maintains consistent demand growth within bakery and confectionery applications, supported by rising global consumption of packaged baked goods and convenience foods. Its functional role as a stabilizer and leavening agent ensures long-term usage across commercial baking operations. Tartrate salts are witnessing expanding adoption in electroplating, ceramics, and specialty chemical formulations, driven by increasing industrial automation and demand for performance-enhancing additives. Overall, diversification of applications across both natural and synthetic product categories is improving market resilience and reducing dependence on a single supply stream.

Application Insights

The food and beverage segment represents the largest application category, contributing approximately 44% of global consumption. Growth in this segment is strongly supported by expanding processed food production, increasing consumption of bakery and confectionery products, and rising demand for acidity regulators and stabilizing agents in beverages. Tartaric acid plays a critical functional role in flavor enhancement, preservation, and pH stabilization, making it indispensable in carbonated drinks, fruit-based beverages, and packaged desserts. The global shift toward premium and natural food formulations further reinforces adoption, particularly as manufacturers replace synthetic additives with naturally sourced alternatives.Pharmaceutical applications represent the fastest-growing segment, driven by rising drug production volumes, expansion of generic medicine manufacturing, and increasing demand for nutraceutical and dietary supplement products. Tartaric acid is widely used as an excipient and stabilizing agent in pharmaceutical formulations, supporting solubility and bioavailability improvements. Growth in healthcare expenditure across emerging economies and expanding contract manufacturing activities are accelerating adoption within this segment.Industrial applications continue to expand steadily as manufacturers increasingly adopt environmentally safer chemical alternatives. In construction chemicals, tartaric acid functions as a setting retarder and performance enhancer in cement formulations, improving workability and durability. Electroplating and metal finishing industries are also increasing usage due to improved surface quality outcomes and reduced environmental impact compared with traditional chemicals. Cosmetics and personal care applications are emerging as a promising niche, particularly in pH-balancing skincare formulations and exfoliating products where mild organic acids are preferred over harsher synthetic compounds.

Distribution Channel Insights

Direct industrial sales dominate distribution channels, accounting for nearly 58% of total market transactions, largely due to long-term procurement contracts between tartaric acid manufacturers and large-scale food, beverage, and pharmaceutical companies. These agreements ensure supply stability, price predictability, and quality consistency, which are essential for high-volume manufacturing environments. The growing consolidation of global ingredient supply chains has further strengthened direct sourcing relationships, enabling producers to optimize logistics and reduce intermediary costs.Specialty chemical distributors play a critical role in expanding market accessibility, particularly for small and medium-sized enterprises requiring tailored formulations or lower-volume purchases. These distributors provide technical support, regulatory compliance assistance, and localized warehousing solutions that facilitate adoption in niche industrial applications. Ingredient suppliers and regional distributors remain essential for market penetration in emerging economies where fragmented supply chains and infrastructure limitations necessitate localized distribution networks. Additionally, digital procurement platforms are gradually transforming purchasing behavior by improving pricing transparency, supplier comparison, and real-time inventory visibility, thereby enhancing procurement efficiency across industries.

End-Use Industry Insights

The food processing industry remains the largest end-use sector, representing about 41% of global demand. Growth is driven by rapid expansion of packaged food manufacturing, increasing urbanization, and rising consumer reliance on convenience foods. Tartaric acid’s multifunctional properties, including acidity regulation, preservation, and texture stabilization, make it a critical ingredient across bakery, beverage, and confectionery production lines. Continuous innovation in ready-to-eat and shelf-stable products further reinforces long-term demand.The pharmaceutical industry is the fastest-growing end-use segment, supported by increasing global healthcare spending, aging populations, and expanding generic drug production. The compound’s role in improving drug stability and formulation efficiency positions it as a valuable component in both traditional medicines and modern nutraceutical products. Contract manufacturing organizations and pharmaceutical outsourcing trends are also accelerating consumption levels worldwide.Wine and alcoholic beverage industries continue to generate stable demand, particularly in established wine-producing regions where tartaric acid is essential for acidity adjustment and flavor balance. Meanwhile, emerging applications in construction chemicals are gaining traction as infrastructure development projects increase globally. Tartaric acid improves cement hydration control and enhances workability, supporting adoption in modern construction materials designed for improved performance and sustainability.

Explore more data points, trends and opportunities Download Free Sample Report

Tartaric Acid Market Segmentations

By Product Type

- Natural Tartaric Acid

- Synthetic Tartaric Acid

- Cream of Tartar

- Tartrate Salts and Derivatives

By Application

- Food & Beverage Additives

- Pharmaceutical Formulations

- Industrial Applications

- Cosmetics & Personal Care

By Distribution Channel

- Direct Industrial Sales

- Specialty Chemical Distributors

- Ingredient Suppliers

- Online B2B Procurement Platforms

By End-Use Industry

- Food Processing Industry

- Wine & Alcoholic Beverage Industry

- Pharmaceutical Industry

- Construction Chemicals Industry

- Personal Care & Cosmetics Industry

Regional Insights

North America

North America accounts for approximately 18% of the global tartaric acid market, led primarily by the United States. Regional growth is supported by a well-established processed food industry, strong demand for natural food additives, and technological advancements in pharmaceutical manufacturing. Expansion of premium wine production in California continues to sustain steady consumption, while growing consumer awareness regarding clean-label ingredients encourages food manufacturers to shift toward naturally derived acidulants. Additionally, increasing investments in nutraceutical production and dietary supplements are expanding pharmaceutical-grade tartaric acid demand. The presence of advanced supply chain infrastructure and high regulatory standards further promotes consistent adoption across industries.

Europe

Europe dominates the global market with nearly 38% market share in 2025, supported by its extensive wine production ecosystem and mature tartaric acid extraction infrastructure. Countries such as Italy, Spain, and France benefit from abundant grape-processing by-products, enabling efficient natural tartaric acid recovery. Strict food safety regulations and strong regulatory preference for natural additives continue to reinforce regional demand stability. Sustainability policies and circular economy initiatives across the European Union are encouraging waste valorization practices, further strengthening production capabilities. Additionally, growing demand for premium food products and organic beverages supports continued regional leadership in both production and consumption.

Asia-Pacific

Asia-Pacific represents around 29% of global demand and is the fastest-growing regional market. Rapid industrialization, expanding pharmaceutical manufacturing capacity, and rising food processing activities are major growth drivers. China leads regional industrial consumption due to large-scale chemical manufacturing and construction sector expansion, while India is experiencing accelerated demand driven by pharmaceutical exports and increasing domestic drug production. Japan and South Korea focus on high-purity and specialty-grade applications, supporting premium pricing segments. Rising disposable incomes, urban dietary shifts toward packaged foods, and increasing investments in food safety standards are collectively strengthening long-term regional growth prospects.

Latin America

Latin America holds nearly 9% market share, with Argentina and Chile serving as key contributors due to strong wine export industries and increasing investments in tartaric acid recovery technologies. Regional producers are expanding export-oriented production to meet rising demand from Asia-Pacific and North America. Growth is further supported by modernization of food processing industries and increasing adoption of value-added agricultural by-product utilization. Government initiatives promoting agro-industrial development and export diversification are also encouraging local production capacity expansion, positioning the region as an emerging supplier in global trade.

Middle East & Africa

The Middle East and Africa account for roughly 6% of global demand, supported by expanding food import dependence and gradual industrial diversification. Growing urban populations and increasing consumption of packaged and processed foods are driving demand for food-grade additives across the region. Countries such as the UAE and South Africa are emerging as key consumption hubs due to expanding food processing industries and improving logistics infrastructure. Rising investments in pharmaceutical manufacturing and construction development projects are also contributing to incremental demand growth. Although production capacity remains limited, improving trade connectivity and industrial investments are expected to enhance regional market participation over the forecast period.

Key Players in the Tartaric Acid Market

- Distillerie Mazzari S.p.A.

- Industria Chimica Valenzana (ICV Group)

- Tarac Technologies

- American Tartaric Products Inc.

- Derivados Vinicos S.A.

- Alvinesa Natural Ingredients

- ATP Group

- Changmao Biochemical Engineering Company

- Ninghai Organic Chemical Factory

- Omkar Speciality Chemicals Ltd.

- Merck KGaA

- Jungbunzlauer Suisse AG

- Caviro Group

- Vinicas Inc.

- Distillerie Bonollo S.p.A.