Tahini Market Size

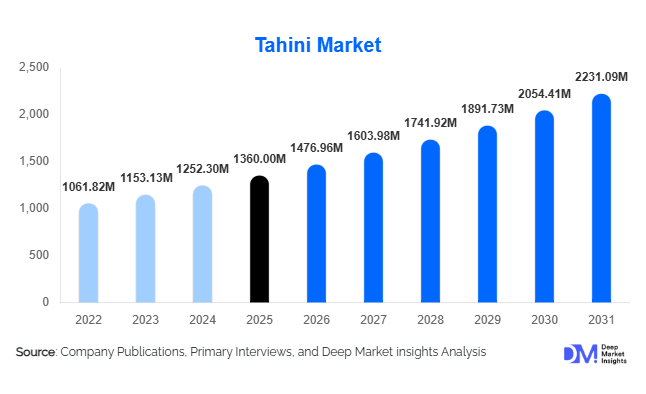

According to Deep Market Insights, the global tahini market size was valued at USD 1,360 million in 2025 and is projected to grow from USD 1,476.96 million in 2026 to reach USD 2,231.09 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). The tahini market growth is primarily driven by the rapid adoption of plant-based diets, increasing global consumption of Mediterranean cuisine, and expanding use of sesame-based ingredients in processed foods, sauces, and functional nutrition products. Tahini has transitioned from a traditional regional food staple into a globally traded health-oriented ingredient supported by rising demand for clean-label spreads and nutrient-dense plant proteins.

Key Market Insights

- Plant-based dietary adoption is accelerating tahini consumption globally, positioning sesame-based spreads as alternatives to dairy and nut-based products.

- Food processing applications are expanding rapidly, with tahini increasingly used in hummus, dressings, snacks, and ready-to-eat meals.

- Europe leads global consumption, supported by strong Mediterranean dietary influence and organic food demand.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization and rising exposure to international cuisines.

- Organic and premium tahini variants are gaining traction among health-conscious consumers seeking minimally processed foods.

- E-commerce and direct-to-consumer distribution channels are improving accessibility and expanding global consumer reach.

What are the latest trends in the tahini market?

Premiumization and Organic Product Expansion

The tahini market is witnessing strong premiumization as consumers increasingly demand organic, non-GMO, and minimally processed food products. Organic tahini variants are gaining shelf space across supermarkets and specialty stores, supported by rising awareness of sustainable agriculture and clean-label nutrition. Manufacturers are introducing stone-ground and cold-processed tahini to retain nutritional integrity and improve flavor profiles. Premium positioning allows brands to command higher margins while appealing to health-focused consumers seeking transparency in ingredient sourcing. Certifications related to organic farming and ethical sourcing are becoming key differentiators, particularly in North American and European retail markets.

Product Innovation and Flavor Diversification

Innovation is reshaping tahini consumption beyond traditional culinary applications. Companies are launching flavored variants such as chocolate, garlic, herb-infused, and spicy tahini to attract younger demographics and expand snack applications. Tahini is increasingly incorporated into desserts, protein spreads, dairy alternatives, and plant-based ready meals. Powdered tahini formats are emerging for industrial food manufacturing and convenience applications. These innovations are helping brands penetrate new consumer segments while increasing repeat purchases and cross-category usage.

What are the key drivers in the tahini market?

Growth of Plant-Based and Functional Nutrition

The global shift toward plant-based diets is a major growth driver for tahini. Consumers seeking alternative protein sources are adopting sesame-based products due to their high mineral content, healthy fats, and natural formulation. Tahini aligns strongly with vegan and flexitarian dietary trends, contributing to increased retail and foodservice demand. Functional food manufacturers are also incorporating tahini into fortified products targeting bone health and nutritional supplementation, further strengthening demand.

Expansion of Processed and Convenience Foods

The growing ready-to-eat food industry has significantly increased industrial demand for tahini as an ingredient. Hummus production, salad dressings, sauces, and packaged snacks increasingly rely on tahini for flavor and nutritional value. Food manufacturers benefit from tahini’s versatility, emulsification properties, and natural ingredient profile. As convenience food consumption rises globally, ingredient demand continues to support long-term market expansion.

What are the restraints for the global market?

Sesame Seed Price Volatility

Tahini production costs are heavily dependent on sesame seed availability, which is influenced by climatic conditions and geopolitical factors in major producing regions such as Africa and Asia. Price fluctuations impact manufacturer margins and retail pricing stability, creating challenges for long-term planning and profitability. Supply disruptions can also affect export volumes and production consistency.

Limited Consumer Awareness in Emerging Markets

Despite global expansion, tahini remains relatively unfamiliar in several developing regions. Consumer education and culinary awareness campaigns are required to drive adoption outside traditional markets. Marketing investments and localization strategies are necessary to accelerate penetration, particularly in parts of Asia and Latin America where spreads such as peanut butter dominate consumer preference.

What are the key opportunities in the tahini industry?

Integration into Plant-Based Food Ecosystems

The expanding plant-based food sector presents significant opportunities for tahini manufacturers. Partnerships with vegan food brands and ready-meal producers enable scaling through ingredient supply contracts. Tahini’s nutritional profile makes it suitable for dairy-free sauces, protein snacks, and alternative spreads, opening new revenue streams beyond traditional retail consumption.

Export Expansion and Regional Production Investments

Governments in sesame-producing countries are encouraging value-added exports, creating favorable conditions for tahini production expansion. Investments in food processing infrastructure and export incentives are enabling manufacturers to scale globally. Localization of production near raw material sources reduces logistics costs while improving supply stability, creating opportunities for new entrants and joint ventures.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1360 Million |

| Market Size in 2026 | USD 1476.96 Million |

| Market Size in 2031 | USD 2231.09 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global tahini market is primarily led by hulled tahini, which accounts for approximately 46% of total revenue and remains the most commercially dominant product type. Its smooth texture, light color, and mild flavor profile make it highly adaptable across both household kitchens and large-scale food manufacturing applications. Food processors prefer hulled tahini because it blends easily into dips, sauces, dressings, and spreads without overpowering other ingredients, supporting its widespread integration into packaged food formulations. The leading driver behind this segment’s dominance is the growing consumer preference for versatile, ready-to-use ingredients aligned with clean-label and plant-based dietary trends. As global demand for hummus, salad dressings, and plant-based protein spreads expands, hulled tahini continues to benefit from scalability and standardized quality requirements demanded by industrial buyers.Roasted tahini represents a significant share of the market, supported by increasing demand for stronger flavor profiles in gourmet and foodservice applications. Roasting enhances aroma and depth of taste, making it particularly suitable for premium sauces, dips, and ethnic cuisine preparations. The rising popularity of Mediterranean and Middle Eastern cuisine across international markets has reinforced demand for roasted variants, especially within restaurants and specialty food brands seeking authentic flavor experiences.Unhulled tahini occupies a smaller yet steadily growing niche, driven by health-conscious consumers seeking higher fiber, calcium, and mineral content. Although its stronger taste limits mainstream appeal, growing awareness of minimally processed foods and whole-seed nutrition is encouraging adoption within organic and wellness-focused product categories. Meanwhile, flavored tahini varieties are emerging as an innovation-led segment, with manufacturers introducing chocolate, honey, herb-infused, and dessert-oriented formulations. These innovations are expanding tahini beyond traditional culinary use into snack spreads, bakery fillings, and functional food categories, reflecting broader diversification of consumer demand. Overall, traditional paste formats continue to dominate as they support both culinary authenticity and industrial scalability across global markets.

Application Insights

Household consumption remains the largest application segment, contributing nearly 52% of global demand, supported by increasing use of tahini as a nutritious spread, cooking ingredient, and alternative to dairy- or nut-based sauces. The leading driver of this segment is the rising adoption of plant-based diets combined with growing consumer awareness of sesame’s nutritional benefits, including healthy fats, protein, and micronutrients. Consumers increasingly incorporate tahini into everyday meals such as breakfast spreads, salad dressings, smoothies, and home-prepared Mediterranean dishes, reinforcing sustained retail demand.Food processing applications represent the fastest-growing segment as tahini becomes a foundational ingredient in packaged hummus, ready-to-eat meals, sauces, dips, and plant-based food innovations. Manufacturers increasingly utilize tahini for texture enhancement, emulsification properties, and nutritional positioning, enabling clean-label product development without artificial additives. The rapid expansion of convenience foods and refrigerated prepared meals globally further strengthens industrial demand.Foodservice applications continue to expand alongside the globalization of Mediterranean and Middle Eastern cuisines. Restaurants, quick-service chains, and fast-casual dining concepts increasingly integrate tahini into menu offerings such as wraps, bowls, dressings, and vegan dishes. Additionally, nutraceutical and functional food applications are emerging as manufacturers leverage tahini’s nutrient density to develop fortified foods, protein-rich snacks, and wellness-oriented formulations targeting health-conscious consumers seeking natural functional ingredients.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 41% of global tahini sales and remain the dominant distribution channel due to strong product visibility, wide assortment availability, and expanding international food aisles. The leading driver for this channel is increasing consumer exposure to global cuisines through organized retail environments, where tahini benefits from cross-merchandising alongside hummus, sauces, and health foods. Retailers are also expanding private-label offerings, improving affordability and accessibility across broader consumer demographics.Specialty health food stores maintain an important role, particularly for organic, non-GMO, and premium tahini products targeting wellness-focused consumers. These outlets support brand differentiation through education-driven marketing and curated product selections emphasizing sustainability and nutritional quality.Online retail represents the fastest-growing distribution channel, supported by the expansion of direct-to-consumer brands, subscription-based health food platforms, and increasing consumer preference for convenience purchasing. Digital channels enable smaller brands to access international markets while providing consumers with wider product variety, transparency regarding sourcing, and niche product availability. Foodservice and B2B distribution networks also contribute significantly to total volume demand through long-term supply agreements with hummus manufacturers, restaurants, and industrial food processors.

End-Use Industry Insights

The food processing industry is emerging as the fastest-growing end-use sector, driven primarily by rising global demand for ready-to-eat meals, refrigerated dips, and plant-based packaged foods. The leading driver for this segment is the increasing need for multifunctional ingredients that provide flavor, texture, and nutritional value simultaneously. Tahini’s natural emulsifying properties and clean-label positioning make it highly attractive for large-scale food manufacturing applications.Household consumption continues to dominate overall volume demand as consumers increasingly prepare international cuisines at home and seek healthier alternatives to conventional spreads and sauces. Restaurants and quick-service outlets are also expanding tahini usage as menus evolve toward healthier and globally inspired offerings. Export-oriented demand remains strong, particularly as Middle Eastern producers supply European and North American processors seeking authentic ingredient sourcing. Emerging applications in dairy-free desserts, protein-enriched spreads, bakery fillings, and functional nutrition products are further expanding tahini’s industrial relevance and supporting long-term market diversification.

Explore more data points, trends and opportunities Download Free Sample Report

Tahini Market Segmentations

By Product Type

- Hulled Tahini

- Unhulled Tahini

- Roasted Tahini

- Raw/Stone-Ground Tahini

- Flavored & Specialty Tahini

By Application

- Household Consumption

- Food Processing & Manufacturing

- Foodservice & Restaurants

- Nutraceutical & Functional Foods

- Bakery & Confectionery Applications

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty & Health Food Stores

- Online Retail & Direct-to-Consumer

- Foodservice & B2B Supply

Regional Insights

North America

North America accounts for approximately 27% of global tahini demand, led by the United States and Canada, where shifting dietary preferences toward plant-based and clean-label foods are accelerating consumption. Regional growth is primarily driven by the rapid expansion of hummus consumption, increasing vegan and flexitarian populations, and strong penetration of health-focused retail chains. Consumers increasingly view tahini as a nutrient-dense alternative to traditional spreads, supporting premium product adoption. Innovation in flavored and organic varieties, combined with rising demand for globally inspired cuisine, continues to strengthen retail and foodservice penetration across urban markets. Additionally, investments in plant-based product innovation by food manufacturers are expanding industrial usage across sauces, dressings, and prepared meals.

Europe

Europe holds the largest regional share at nearly 30%, supported by strong demand across the United Kingdom, Germany, and France. Regional growth is driven by deep-rooted Mediterranean dietary influence, high organic food consumption, and strong regulatory support for natural and minimally processed ingredients. Consumers demonstrate high awareness of nutritional labeling and sustainability, encouraging demand for premium and ethically sourced tahini products. Retailers are expanding international cuisine assortments, improving mainstream accessibility, while private-label expansion enhances affordability. The growing popularity of vegetarian and vegan diets across Western Europe further supports long-term demand growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at a CAGR exceeding 10%. Growth is fueled by rapid urbanization, rising disposable incomes, and increasing exposure to global culinary trends through travel, social media, and international restaurant chains. Countries such as China, India, Japan, and Australia are witnessing rising demand for healthy spreads and plant-based ingredients. Expanding modern retail infrastructure and e-commerce penetration are improving product accessibility, while younger consumers increasingly experiment with international flavors. The region’s growing health-conscious middle class and increasing adoption of functional foods are expected to significantly accelerate tahini consumption over the forecast period.

Latin America

Latin America demonstrates gradual but steady market expansion, particularly in Brazil and Mexico. Regional growth is supported by rising health food awareness, expanding premium grocery retail networks, and increasing exposure to international cuisine through urban foodservice channels. Although overall consumer familiarity with tahini remains comparatively limited, educational marketing efforts and the expansion of plant-based food categories are improving adoption rates. Import-driven supply chains and growing specialty food retail presence are expected to gradually strengthen market penetration.

Middle East & Africa

The Middle East & Africa region accounts for approximately 24% of global consumption and remains both a major production hub and a culturally established consumption market. Regional growth is driven by strong culinary traditions, widespread sesame cultivation, and deeply embedded use of tahini in daily diets. Countries such as Israel, Turkey, the UAE, and Saudi Arabia demonstrate high per capita consumption supported by foodservice demand and export-oriented production industries. Increasing population growth, tourism expansion, and rising packaged food exports are further reinforcing regional market strength. Additionally, modernization of food processing facilities and growing international exports continue to position the region as a critical supplier to Europe and North America.

Key Players in the Tahini Market

- Al Wadi Al Akhdar

- Halwani Bros. Co.

- Achva Food Industries Ltd.

- Prince Tahina Ltd.

- Haitoglou Bros S.A.

- Al Arz Tahini

- Soom Foods

- Seed + Mill

- Sunshine International Foods Inc.

- Baron’s International Kitchen

- Carwari International Pty Ltd.

- Dipasa USA Inc.

- El Rashidi El Mizan

- Kevala International LLC

- Tarazi Specialty Foods