Table Tennis Market Size

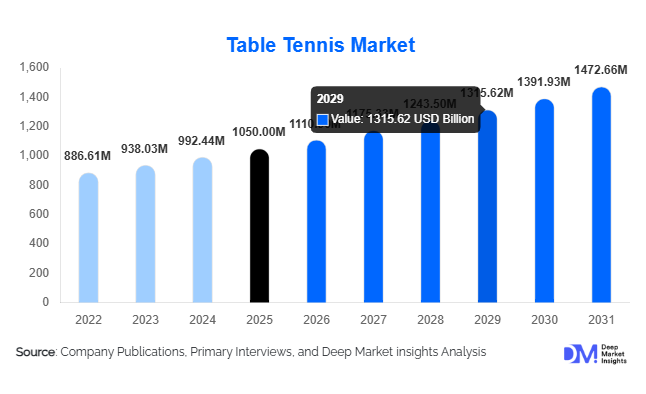

According to Deep Market Insights, the global table tennis market size was valued at USD 1,050 million in 2025 and is projected to grow from USD 1,110.90 million in 2026 to reach USD 1,472.66 million by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The market growth is primarily driven by increasing participation in recreational and competitive sports, expanding investments in sports infrastructure, growing popularity of indoor fitness activities, and continuous product innovations in rackets, tables, balls, and smart training systems. Rising government support for grassroots sports programs, increasing school-level participation, and growing demand for home-based recreational equipment are further contributing to market expansion globally.

Key Market Insights

- Asia-Pacific dominates the global table tennis market, accounting for approximately 44% of global revenue, supported by strong participation rates in China, Japan, South Korea, and India.

- Rackets represent the largest product category, contributing nearly 38% of global market revenue due to frequent replacement cycles and ongoing technological advancements.

- Recreational and home users account for the largest end-user segment, representing over 42% of global demand in 2025.

- Online retail channels are transforming equipment sales, contributing approximately 40% of global distribution revenues.

- Carbon-fiber and composite racket technologies are gaining rapid adoption among professional and advanced amateur players.

- AI-powered training robots and connected coaching systems are emerging as significant innovation areas within the market.

Table Tennis Market Trends

Smart Training Equipment and AI-Driven Coaching Solutions

The table tennis industry is increasingly embracing digital transformation through AI-powered training robots, connected coaching systems, motion sensors, and performance analytics platforms. Professional academies and advanced recreational players are adopting intelligent training equipment capable of simulating match conditions, analyzing shot patterns, and providing personalized feedback. These systems improve training efficiency while creating recurring revenue opportunities for manufacturers through software subscriptions and analytics services. The integration of mobile applications, cloud-based coaching platforms, and performance tracking dashboards is becoming increasingly common across premium equipment offerings.

Outdoor Table Tennis Infrastructure Expansion

Demand for weather-resistant outdoor table tennis tables is growing rapidly across public parks, residential complexes, schools, universities, and hospitality facilities. Municipal authorities and community organizations are investing in outdoor sports infrastructure to encourage physical activity and social engagement. Manufacturers are responding by introducing anti-corrosion materials, vandal-resistant designs, UV-resistant surfaces, and low-maintenance equipment. This trend is expanding the market beyond traditional indoor sports facilities and creating new demand channels in urban recreation and wellness projects globally.

Table Tennis Market Drivers

Growing Participation in Recreational Sports and Fitness Activities

Rising awareness regarding physical fitness and active lifestyles continues to support demand for table tennis equipment worldwide. The sport appeals to a broad demographic range due to its accessibility, relatively low cost of participation, minimal space requirements, and suitability across all age groups. Governments, schools, and corporate organizations increasingly promote table tennis as part of wellness and recreational programs, leading to sustained equipment demand across multiple end-user segments.

Expansion of Professional Leagues and International Competitions

Growing visibility of international tournaments, regional championships, university competitions, and professional leagues is contributing significantly to market growth. Increased media coverage, sponsorship investments, and digital broadcasting platforms are attracting younger players and expanding participation rates. The growing professional ecosystem is also driving demand for tournament-grade equipment, premium rackets, and advanced training solutions among aspiring athletes.

Table Tennis Market Restraints

Intense Pricing Competition Across Regional Markets

The table tennis equipment market remains highly fragmented, particularly across Asia-Pacific, where numerous regional manufacturers compete aggressively on price. This competitive environment creates pressure on profit margins and limits pricing flexibility for both established brands and new entrants. Lower-cost alternatives often challenge premium manufacturers in emerging markets, creating ongoing competitive pressures.

Dependence on Consumer Discretionary Spending

Purchases of table tennis equipment are influenced by consumer confidence and discretionary spending patterns. Economic downturns, inflationary pressures, and declining household disposable income can delay replacement cycles and reduce spending on premium sports equipment. Institutional procurement budgets may also be affected during periods of economic uncertainty, impacting overall market growth.

Table Tennis Market Opportunities

Institutional Sports Infrastructure Development

Government investments in sports infrastructure, educational institutions, and community recreation centers present significant growth opportunities for equipment manufacturers. Countries such as China, India, Japan, Germany, and South Korea continue to expand public sports facilities under national fitness programs. Institutional procurement contracts provide manufacturers with stable demand and long-term revenue visibility while supporting grassroots participation growth.

Growth of Connected and Subscription-Based Training Ecosystems

The emergence of connected sports technologies offers substantial opportunities for manufacturers to develop integrated hardware and software ecosystems. AI-enabled training systems, cloud-based coaching platforms, virtual training programs, and performance analytics applications can generate recurring revenue streams beyond traditional equipment sales. This trend is expected to reshape customer engagement models and strengthen brand loyalty among competitive players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1050 Million |

| Market Size in 2026 | USD 1110.90 Million |

| Market Size in 2031 | USD 1472.66 Million |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rackets dominated the global table tennis market, accounting for approximately 38% of total revenue in 2025, making them the largest product category across both professional and recreational applications. The segment's leadership is primarily driven by frequent replacement cycles compared to other equipment categories, as players regularly upgrade rackets, rubbers, and blades to improve performance. Growing participation in organized competitions, club-level tournaments, and coaching programs has increased demand for premium rackets featuring carbon-fiber, arylate-carbon, and hybrid composite technologies that provide enhanced speed, spin control, and durability. Manufacturers continue to launch technologically advanced racket designs targeting intermediate and professional players, contributing to premiumization across the category. Furthermore, endorsement partnerships with elite athletes and increased consumer awareness regarding equipment customization have accelerated sales of high-performance rackets globally.

Tables represent the second-largest segment, supported by growing procurement from educational institutions, sports academies, recreation centers, and government-funded sports infrastructure projects. Demand for competition-grade tables continues to increase in developed sports markets, while outdoor tables are emerging as one of the fastest-growing categories due to rising investments in public parks, residential communities, corporate campuses, and hospitality facilities. The outdoor segment is particularly benefiting from urban wellness initiatives and smart-city recreational development programs.

Balls maintain stable and recurring demand due to their consumable nature and frequent replacement requirements during training sessions and tournaments. Meanwhile, accessories including training robots, replacement rubbers, blades, footwear, maintenance products, and performance analytics devices are experiencing above-average growth rates. Increasing adoption of advanced coaching technologies and data-driven training methods is creating a rapidly expanding market for connected training equipment and smart accessories.

Application Insights

Fitness and recreational activities accounted for approximately 47% of global market demand in 2025, making this the largest application segment. The segment's dominance is driven by increasing consumer interest in low-impact fitness activities that can be played across age groups and skill levels. Unlike many organized sports, table tennis requires limited space and relatively low investment, making it highly accessible for households, schools, offices, and community centers. Growing awareness of physical fitness, active aging programs, and indoor recreational activities continues to expand participation worldwide.

Training and coaching applications represent the second-largest demand segment, supported by increasing investments in sports academies, youth development programs, and professional coaching infrastructure. Countries including China, Japan, South Korea, Germany, and India continue to invest heavily in grassroots talent development, creating sustained demand for professional-grade equipment, training robots, and performance monitoring systems. Competitive tournaments remain a critical revenue generator for premium equipment manufacturers. Rising sponsorship investments, expanding professional leagues, and growing international tournament participation are driving demand for ITTF-certified tables, rackets, and balls. Educational sports programs are also contributing significantly to market expansion as governments increasingly integrate table tennis into school physical education curricula due to its affordability and accessibility.

Corporate wellness initiatives, employee engagement programs, and hospitality entertainment applications are emerging as high-growth niches. Hotels, resorts, coworking spaces, and corporate campuses are increasingly installing table tennis facilities as part of broader wellness and recreational offerings, creating new avenues for equipment manufacturers.

Distribution Channel Insights

Online retail channels accounted for nearly 40% of global table tennis equipment sales in 2025, making e-commerce the leading distribution segment. The growth of online sales is driven by expanding internet penetration, direct-to-consumer business models, competitive pricing strategies, and broader product accessibility. Consumers increasingly prefer online platforms due to the availability of detailed product specifications, customer reviews, comparison tools, and access to international brands that may not be available through local retailers. Digital marketing, athlete influencer campaigns, and social commerce platforms are further accelerating online equipment purchases, particularly among younger consumers and amateur players. Leading manufacturers are increasingly investing in direct e-commerce platforms to strengthen customer relationships and improve profit margins while reducing dependence on traditional retail intermediaries.

Specialty sports retailers continue to play a critical role, particularly within premium and professional equipment categories where technical guidance and product demonstrations influence purchasing decisions. Institutional procurement channels remain highly important due to bulk purchasing activity from schools, universities, sports clubs, and government organizations. Meanwhile, department stores and hypermarkets maintain relevance within entry-level and recreational equipment categories, particularly across emerging economies where organized sports retail networks remain underdeveloped. The increasing adoption of omnichannel strategies is enabling manufacturers to integrate physical retail experiences with digital sales platforms, improving customer engagement and expanding market reach.

End-User Insights

Recreational and home users accounted for approximately 42% of global market demand in 2025, making them the largest end-user segment. Rising interest in family recreation, indoor entertainment, health-conscious lifestyles, and social sports activities continues to support equipment purchases among casual users. The segment experienced significant momentum following increased consumer focus on home-based recreational activities and wellness-oriented leisure spending. Sports clubs and academies remain a highly influential customer group, particularly within premium equipment categories. Continuous investments in coaching infrastructure, athlete development programs, and competitive training environments drive recurring purchases of professional-grade tables, rackets, balls, and training equipment.

Educational institutions represent one of the fastest-growing end-user segments, supported by government investments in school sports infrastructure and physical education initiatives. Table tennis is increasingly adopted within educational environments due to its relatively low infrastructure requirements, affordability, and suitability across various age groups. Corporate recreation facilities and hospitality venues are emerging as attractive growth segments. Employers are incorporating recreational sports into workplace wellness programs to improve employee engagement and productivity, while hotels, resorts, cruise operators, and leisure centers increasingly utilize table tennis facilities to enhance guest experiences and recreational offerings.

Price Category Insights

Mid-range equipment accounted for approximately 44% of total market revenue in 2025, making it the largest price segment globally. The segment benefits from its ability to balance affordability with performance, appealing to recreational users, educational institutions, and intermediate players seeking enhanced quality without professional-level pricing. Growing participation in amateur competitions and club-level sports is further supporting demand for mid-range equipment. Premium and professional-grade products continue to gain market share as consumers increasingly prioritize durability, technological innovation, and performance optimization. Advanced carbon-fiber rackets, ITTF-certified tables, and AI-enabled training equipment are commanding higher average selling prices and contributing to market premiumization.

Economy products maintain strong demand across developing economies where affordability remains a primary purchasing factor. Meanwhile, professional tournament-grade equipment generates the highest profit margins and benefits from increasing participation in organized competitions, athlete sponsorship programs, and international sporting events. The premium segment is expected to outpace overall market growth as serious amateur and competitive players continue upgrading to technologically advanced equipment.

Explore more data points, trends and opportunities Download Free Sample Report

Table Tennis Market Segmentations

By Product Type

- Tables

- Rackets (Bats/Paddles)

- Balls

- Nets & Posts

- Accessories & Training Equipment

By Application

- Fitness & Recreation

- Training & Coaching

- Competitive Tournaments

- Educational Sports Programs

- Corporate Wellness Programs

- Hospitality & Entertainment

By Distribution Channel

- Online Retail

- Specialty Sports Retailers

- Institutional Procurement

- Department Stores & Hypermarkets

- Direct-to-Club Sales

By End User

- Recreational & Home Users

- Sports Clubs & Academies

- Educational Institutions

- Corporate Recreation Facilities

- Hospitality & Leisure Facilities

- Community & Government Sports Centers

By Price Category

- Economy

- Mid-Range

- Premium

- Professional Tournament Grade

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 44% of global market revenue in 2025, making it the largest regional market worldwide. The region's dominance is driven by a deeply established table tennis culture, extensive grassroots participation, strong manufacturing capabilities, and sustained government investment in sports development. China alone contributes nearly 24% of global demand and remains the largest production hub for tables, rackets, balls, and accessories. Government-backed sports programs, widespread school participation, and professional league development continue to support domestic consumption.

Japan and South Korea maintain strong demand for premium equipment, benefiting from advanced sports technology adoption, competitive club ecosystems, and growing demand for performance-oriented products. India is among the fastest-growing national markets globally, supported by increasing disposable incomes, expanding sports infrastructure, government initiatives such as Khelo India, and growing youth participation in competitive sports. Southeast Asian countries including Indonesia, Thailand, Malaysia, and Vietnam are also witnessing increasing equipment demand as recreational sports participation continues to expand.

Europe

Europe represented approximately 27% of global market revenue in 2025, supported by a well-developed club structure, strong professional tournament ecosystem, and widespread community-level participation. Germany remains the largest European market due to its extensive network of table tennis clubs, organized competitions, and high equipment replacement rates among competitive players.

France, Sweden, the United Kingdom, and Poland continue to generate substantial demand through school sports programs, community recreation initiatives, and professional league participation. The region is also characterized by high adoption of premium equipment, particularly among club players seeking advanced racket technologies. Government investments in public sports facilities, growing health-conscious consumer behavior, and increasing participation among older demographics are key growth drivers across Europe.

North America

North America accounted for approximately 18% of global demand in 2025, with the United States representing the dominant market. Regional growth is driven by increasing recreational participation, expanding corporate wellness programs, and growing demand for indoor recreational activities. Table tennis is increasingly being adopted within schools, universities, coworking spaces, and community recreation centers.

The rapid growth of e-commerce channels has significantly improved access to premium international brands across the region. Rising popularity of home entertainment products, increasing immigrant participation from table tennis-oriented countries, and growth in professional leagues and amateur tournaments are further contributing to market expansion. Canada is also witnessing increased demand through educational institutions and municipal recreation programs.

Latin America

Latin America accounted for approximately 6% of global market revenue, led by Brazil, Mexico, and Argentina. Rising urbanization, increasing sports participation, and growing middle-class spending on recreational activities continue to support market development. Governments and sports federations are investing in youth sports programs and community recreation infrastructure, creating long-term growth opportunities.

Brazil remains the largest market in the region due to its strong sporting culture and growing participation in racket sports. Mexico is benefiting from increasing educational sports investments and recreational infrastructure development, while Argentina continues to witness growth in club-based participation and amateur competition activities.

Middle East & Africa

The Middle East and Africa accounted for approximately 5% of global demand in 2025, but the region is expected to record some of the fastest growth rates during the forecast period. Saudi Arabia and the United Arab Emirates are investing heavily in sports infrastructure development, public recreation projects, and national fitness initiatives as part of broader economic diversification strategies.

Government-led programs promoting active lifestyles, rising investments in indoor sports facilities, and increasing participation among younger populations are creating favorable market conditions. South Africa remains the largest African market due to its relatively mature sports ecosystem and established table tennis community. Growing tourism infrastructure, school sports programs, and community recreation initiatives across the Gulf Cooperation Council countries are expected to drive substantial future demand for table tennis equipment throughout the region.

Key Players in the Table Tennis Market

- Butterfly

- DHS (Double Happiness)

- STIGA Sports

- JOOLA

- Donic

- Nittaku

- XIOM

- Tibhar

- Andro

- Double Fish

- Yasaka

- Victas

- Cornilleau

- Killerspin

- Gewo