Sweeteners Market Size

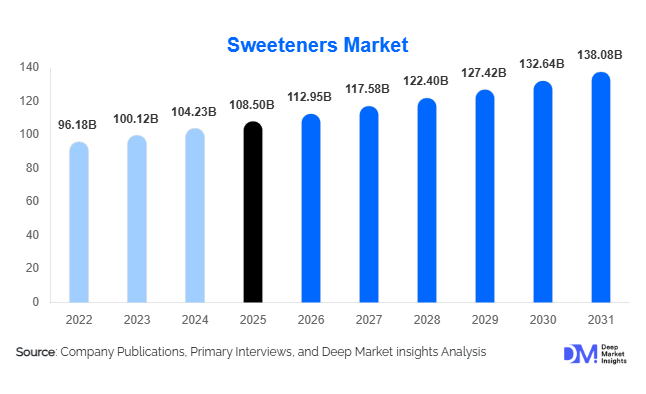

According to Deep Market Insights, the global sweeteners market size was valued at USD 108.5 billion in 2025 and is projected to grow from USD 112.95 billion in 2026 to reach USD 138.08 billion by 2031, expanding at a CAGR of 4.1% during the forecast period (2026–2031). The sweeteners market growth is primarily driven by rising demand for low-calorie and natural sugar alternatives, increasing regulatory pressure to reduce sugar consumption, and expanding applications across beverages, processed foods, pharmaceuticals, and nutraceuticals.

Key Market Insights

- Nutritive sweeteners continue to dominate volume consumption, accounting for nearly 58% of the global market in 2025, led by sucrose and high fructose corn syrup (HFCS).

- Natural high-intensity sweeteners such as stevia and monk fruit are the fastest-growing category, supported by clean-label demand and sugar reduction policies.

- Asia-Pacific leads global production and consumption, holding approximately 38% market share in 2025.

- Beverages represent the largest application segment, contributing around 34% of total sweetener demand globally.

- Direct B2B sales dominate distribution channels, accounting for nearly 62% of global transactions through long-term supply contracts.

- Fermentation-based and biotech-derived sweeteners are reshaping cost structures and improving taste profiles in high-intensity segments.

What are the latest trends in the sweeteners market?

Shift Toward Natural and Clean-Label Sweeteners

Consumers are increasingly favoring plant-based and minimally processed sweeteners over synthetic alternatives. Steviol glycosides (Reb M, Reb D) and monk fruit extracts are witnessing accelerated adoption due to improved taste profiles achieved through enzymatic and fermentation technologies. Food and beverage companies are reformulating products to remove artificial sweeteners and align with clean-label positioning. This trend is especially prominent in North America and Europe, where sugar taxes and front-of-pack labeling regulations are influencing purchase behavior. Additionally, sustainable sourcing of sugarcane and stevia leaves is becoming a competitive differentiator, with manufacturers investing in traceability and eco-certifications.

Growth of Sugar Reduction and Reformulation Programs

Governments across more than 50 countries have implemented sugar taxes or mandatory labeling norms, compelling manufacturers to reduce sugar content. Beverage giants and packaged food companies are increasingly relying on blended sweetener systems that combine caloric and non-caloric ingredients to achieve taste optimization while lowering total sugar content. This reformulation wave has significantly increased demand for sucralose, Ace-K, erythritol, and stevia blends. Customized solutions and co-development partnerships between ingredient suppliers and multinational food brands are becoming common, strengthening long-term supply relationships.

What are the key drivers in the sweeteners market?

Rising Global Diabetes and Obesity Prevalence

Increasing cases of diabetes and obesity worldwide are accelerating demand for low-glycemic and zero-calorie sweeteners. Consumers are actively seeking reduced-sugar products, especially in beverages, dairy alternatives, and confectionery. Polyols and natural high-intensity sweeteners are gaining traction as healthier substitutes, supporting steady market expansion.

Technological Advancements in Production

Advancements in biotechnology, precision fermentation, and enzymatic conversion processes have significantly improved the commercial scalability of specialty sweeteners. These technologies reduce dependency on agricultural yield variability and enhance cost competitiveness. Fermentation-derived Reb M and allulose production is improving margin stability while expanding application versatility.

What are the restraints for the global market?

Raw Material Price Volatility

The sweeteners industry remains exposed to fluctuations in sugarcane, corn, and stevia leaf prices due to climate variability and global trade dynamics. Such volatility impacts cost structures, particularly for commodity sweeteners like sucrose and HFCS, limiting margin expansion.

Regulatory and Consumer Perception Challenges

Artificial sweeteners continue to face scrutiny in certain markets due to safety debates and labeling controversies. Regulatory inconsistencies across regions complicate approvals and slow commercialization timelines for novel sweeteners.

What are the key opportunities in the sweeteners industry?

Expansion in Emerging Economies

Urbanization and rising disposable income in Southeast Asia, India, Africa, and Latin America are expanding processed food consumption. While traditional sugar demand remains robust, multinational brands are introducing reduced-sugar product lines, creating strong demand for blended sweetener systems. Establishing localized production units can help manufacturers reduce logistics costs and capture early market share.

Integration into Functional Foods and Nutraceuticals

The rapid growth of nutraceutical gummies, protein bars, and fortified beverages presents a significant opportunity for specialty sweeteners. As these products require stable sweetness without caloric burden, high-intensity and polyol sweeteners are increasingly being integrated into health-focused product portfolios, generating higher profit margins compared to traditional sugar.

Product Type Insights

Nutritive sweeteners hold the largest market share at approximately 58% in 2025, driven by extensive use in beverages, bakery, and processed foods. However, natural high-intensity sweeteners represent the fastest-growing segment, expanding at over 6% CAGR due to consumer preference for plant-based and low-calorie alternatives. Sugar alcohols account for roughly 14% of market share, supported by demand in sugar-free confectionery and pharmaceutical formulations. Artificial sweeteners continue to maintain relevance in large-scale beverage reformulations despite slower growth rates.

Application Insights

Beverages dominate the sweeteners market with approximately 34% share in 2025, fueled by reformulation of carbonated drinks, juices, and energy beverages. Bakery and confectionery follow closely, supported by global packaged food demand. Dairy and frozen desserts are witnessing steady adoption of natural sweeteners, particularly in flavored yogurts and plant-based milk products. Pharmaceutical applications are growing at around 5% CAGR, driven by sugar-free syrups and chewable tablets.

Distribution Channel Insights

Direct B2B sales account for nearly 62% of global sweetener distribution, reflecting long-term procurement contracts between ingredient suppliers and food manufacturers. Retail and online channels are expanding for tabletop and specialty sweeteners, particularly in developed markets where consumers increasingly purchase zero-calorie alternatives directly.

End-Use Industry Insights

The food and beverage manufacturing industry represents approximately 68% of global sweetener consumption in 2025. The nutraceutical sector is among the fastest-growing end-use industries, driven by rising demand for dietary supplements and functional foods. Pharmaceutical applications are expanding steadily, particularly in developed markets with aging populations. Export-driven demand remains strong from Brazil, Thailand, China, and the U.S., which are major producers and exporters of sugar, stevia, and corn-derived sweeteners.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global market with approximately 38% share in 2025. China dominates stevia production and exports, while India and Thailand are major sugar exporters. Rapid urbanization and expanding processed food sectors in India and Southeast Asia are driving strong growth, with the region projected to grow at over 5% CAGR.

North America

North America holds around 26% market share, led by the United States, which accounts for nearly 22% of global demand. High adoption of low-calorie sweeteners in beverages and strong regulatory pressure to reduce sugar consumption support sustained demand growth.

Europe

Europe accounts for roughly 22% of global demand. Countries such as Germany, France, and the U.K. are actively reformulating food products in response to sugar taxes and labeling regulations, boosting natural sweetener adoption.

Latin America

Latin America represents approximately 6% of the global market, with Brazil and Mexico driving regional consumption. Mexico’s sugar tax has accelerated demand for alternative sweeteners in beverage reformulation.

Middle East & Africa

The Middle East & Africa region holds about 8% market share, with GCC countries showing strong beverage consumption trends. Intra-African sugar production also contributes to regional supply strength.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|