Sweet Wine Market Size

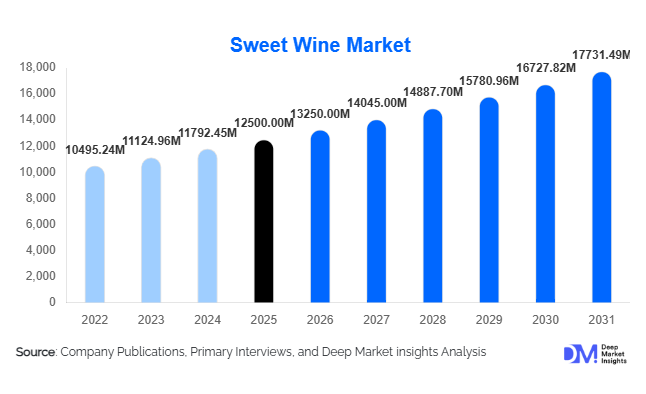

According to Deep Market Insights, the global sweet wine market size was valued at USD 12,500 million in 2026 and is projected to grow from USD 13,250 million in 2027 to reach USD 17731.49 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The market growth is primarily driven by rising premiumization of alcoholic beverages, increasing global exposure to wine culture, expanding e-commerce alcohol sales, and growing demand for sweeter, smoother wine profiles among younger consumers and first-time wine drinkers.

Key Market Insights

- Premiumization of alcoholic beverages is reshaping demand, with consumers shifting toward artisanal and luxury sweet wines.

- Europe remains the dominant production and consumption hub, supported by deep-rooted wine culture and export strength.

- Asia-Pacific is the fastest-growing region, driven by rising disposable income and westernization of consumption patterns.

- E-commerce and direct-to-consumer wine sales are expanding rapidly, improving global accessibility.

- Fortified and sparkling sweet wines are gaining strong traction due to their taste profile and premium positioning.

- Sustainability and organic wine production trends are influencing purchasing decisions, especially in developed markets.

What are the latest trends in the global sweet wine market?

Premiumization and Craft Winemaking Expansion

The sweet wine market is witnessing a strong shift toward premium, organic, and small-batch production. Consumers are increasingly preferring wines with authentic terroir identity, limited production runs, and sustainable cultivation practices. This trend is particularly strong in Europe and North America, where consumers are willing to pay higher prices for exclusivity and craftsmanship. Boutique wineries are expanding their portfolios to include aged dessert wines, ice wines, and fortified variants with premium positioning, significantly boosting overall market value.

Digital Wine Retail and Subscription Growth

The rise of online wine platforms and subscription-based delivery models is transforming distribution. Consumers now prefer curated wine boxes, AI-driven recommendations, and personalized tasting experiences delivered directly to homes. This trend is particularly strong among millennials and urban consumers. Direct-to-consumer sales are helping wineries increase margins while expanding global reach without reliance on traditional distributors. Digital engagement tools such as virtual tastings and interactive wine education platforms are further strengthening customer retention.

What are the key drivers in the global sweet wine market?

Rising Demand for Accessible Luxury Alcoholic Beverages

Sweet wines are increasingly positioned as entry-level luxury beverages due to their smoother taste profiles and broader consumer appeal. Rising disposable income, particularly in emerging economies, is enabling consumers to trade up from basic alcoholic beverages to premium wine products. This is driving consistent growth across both off-trade and on-trade channels, especially in urban markets.

Growth in Hospitality and Tourism Consumption

The expansion of hotels, fine dining restaurants, and luxury tourism has significantly increased demand for sweet wines. These wines are widely used in pairing menus, dessert offerings, and celebratory occasions. Tourism-driven consumption in Europe, the Middle East, and Asia-Pacific is a major contributor to market expansion.

Expansion of E-Commerce Alcohol Distribution

The rapid growth of online alcohol retail platforms is making sweet wines more accessible globally. Consumers now have access to international wine varieties that were previously restricted by geography. Subscription-based wine clubs and curated delivery services are further accelerating demand growth across urban populations.

What are the restraints for the global market?

Rising Health Concerns and Alcohol Moderation Trends

Increasing awareness of health risks associated with alcohol consumption is restraining growth in mature markets. Consumers are gradually shifting toward low-alcohol or alcohol-free alternatives, which may reduce demand for traditional sweet wines in certain demographics.

Regulatory Barriers and High Taxation

The sweet wine market faces strict regulatory frameworks, varying taxation structures, and complex import/export rules across regions. These factors increase compliance costs and limit market penetration, particularly in developing economies with restrictive alcohol policies.

What are the key opportunities in the global sweet wine industry?

Expansion into Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and parts of Africa present strong growth opportunities due to rising disposable incomes and growing acceptance of wine culture. Countries such as China and India are witnessing rapid growth in imported premium alcoholic beverages, creating new revenue streams for global producers.

Growth of Sustainable and Organic Wine Production

Consumer preference for environmentally responsible products is creating opportunities for organic, biodynamic, and carbon-neutral wine production. Certifications and sustainability labeling are becoming key differentiators, particularly in Europe and North America.

Innovation in Flavored and Low-Alcohol Sweet Wines

Product innovation, including fruit-infused, sparkling sweet wines, and low-alcohol variants, is expanding the consumer base. These products appeal to younger demographics and health-conscious consumers, creating new sub-segments within the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12500 Million |

| Market Size in 2026 | USD 13250 Million |

| Market Size in 2031 | USD 17731.49 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global sweet wine market is structurally anchored by fortified sweet wines, which continue to dominate the product type segment, accounting for approximately 34% of global share in 2025. This leadership position is fundamentally driven by the enduring popularity of traditional European varieties such as Port, Sherry, and Madeira, which benefit from deep-rooted heritage, controlled appellations, and consistent quality standards. The leading segment driver for fortified wines lies in their extended shelf life and higher alcohol content, which enhances stability during storage and transportation while appealing to both collectors and casual consumers. Additionally, fortified wines are increasingly being repositioned through premium branding, limited editions, and heritage storytelling, which significantly strengthens their appeal in both mature and emerging markets.Aromatized sweet wines are also gaining traction, particularly in urban and cosmopolitan markets where consumers are actively exploring new flavor profiles and cocktail applications. The leading segment driver here is product innovation, with manufacturers introducing infused variants featuring botanicals, fruits, and spices to cater to evolving taste preferences. These wines are frequently used as cocktail bases in bars and restaurants, aligning with the broader trend of mixology and customized beverage experiences. As a result, aromatized sweet wines are bridging the gap between traditional wine consumption and modern cocktail culture, thereby expanding their consumer base.

Application / End-Use Insights

The hospitality sector remains the dominant end-use segment in the global sweet wine market, accounting for nearly 48% of global demand. This dominance is primarily driven by the integral role that sweet wines play in enhancing dining experiences across restaurants, hotels, and luxury resorts. The leading segment driver is the premium dining culture, where sweet wines are frequently paired with desserts, cheeses, and gourmet dishes to elevate overall customer satisfaction. In addition, the growth of fine dining establishments and the expansion of global hotel chains are further reinforcing demand within this segment, particularly in urban and tourist-centric locations.Wine tourism and vineyard experiences are emerging as high-value niche applications, particularly in regions with established wine cultures. The primary driver here is experiential tourism, where consumers seek immersive experiences that combine travel, education, and gastronomy. Vineyard tours, wine tastings, and harvest festivals are increasingly incorporating sweet wines as a key component, thereby enhancing their visibility and desirability. This trend is particularly prominent in regions with strong wine heritage, where tourism acts as both a revenue stream and a marketing channel.

Distribution Channel Insights

Off-trade channels dominate the global sweet wine market, accounting for approximately 63% of total share. This segment includes supermarkets, hypermarkets, specialty wine stores, and online retail platforms, all of which play a crucial role in ensuring product availability and accessibility. The leading segment driver for off-trade channels is convenience, as consumers increasingly prefer purchasing wines through easily accessible retail formats. Supermarkets and large retail chains benefit from high foot traffic and competitive pricing strategies, while specialty stores offer curated selections and expert guidance, catering to more discerning consumers.On-trade channels, including hotels, bars, and restaurants, remain essential for premium wine consumption and brand positioning. The leading driver for this segment is experiential consumption, where consumers seek curated dining and drinking experiences that go beyond mere product purchase. On-trade venues provide opportunities for wine tastings, sommelier recommendations, and food pairings, all of which contribute to higher perceived value and brand loyalty. Furthermore, influencer-led marketing and social media engagement are increasingly shaping consumer preferences, particularly among younger audiences who rely on digital content for inspiration and discovery.

Explore more data points, trends and opportunities Download Free Sample Report

Sweet Wine Market Segmentations

By Product Type

- Fortified Sweet Wines

- Naturally Sweet Wines

- Sparkling Sweet Wines

- Aromatized Sweet Wines

By Sweetness Level

- Semi-Sweet Wines

- Medium Sweet Wines

- Very Sweet / Dessert Wines

By Grape Variety

- Muscat / Moscato

- Riesling

- Chenin Blanc

- Gewürztraminer

- Cabernet-based Dessert Blends

- Others

By Distribution Channel

- On-Trade

- Supermarkets & Hypermarkets

- Specialty Wine Stores

- Online Retail & Wine Subscription Platforms

By End Use

- Household Consumption

- Hospitality Sector

- Event Catering & Luxury Tourism

Regional Insights

Europe

Europe continues to lead the global sweet wine market, accounting for approximately 38% of total share, underpinned by its deep-rooted wine heritage and well-established production ecosystems. Countries such as France, Italy, Spain, Portugal, and Germany serve as both major producers and exporters, benefiting from favorable climatic conditions, advanced viticulture practices, and strong regulatory frameworks. The key drivers of regional growth include the continued global demand for premium and heritage wines, robust export networks, and the increasing popularity of wine tourism across regions such as Bordeaux, Tuscany, and the Douro Valley. Additionally, innovation in sustainable winemaking practices and organic certifications is further enhancing the competitiveness of European producers in global markets.

North America

North America holds approximately 25% of the global market share, with the United States serving as the primary contributor to regional growth. The market is characterized by a strong preference for premium and artisanal wines, supported by a well-developed retail infrastructure and high consumer awareness. The leading drivers in this region include the rising trend of premiumization, increasing interest in dessert wines, and the expansion of domestic wine production in regions such as California. Furthermore, the growth of wine clubs, subscription services, and direct-to-consumer sales channels is enhancing market penetration and consumer engagement.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the global sweet wine market, driven by rapid economic development and changing consumer preferences. Key markets such as China, India, Japan, and Australia are witnessing increasing demand for imported wines, supported by rising middle-class incomes and greater exposure to global food and beverage cultures. The primary drivers of regional growth include urbanization, expanding retail networks, and the growing influence of Western dining habits. Additionally, government initiatives to promote wine consumption and the development of local wine industries are further contributing to market expansion. E-commerce platforms and digital marketing strategies are playing a particularly important role in reaching younger consumers and driving awareness.

Latin America

Latin America accounts for approximately 6–7% of the global sweet wine market, with countries such as Chile, Argentina, and Brazil playing significant roles in both production and consumption. The region benefits from favorable climatic conditions for viticulture, as well as increasing investments in modern winemaking technologies. The key drivers of growth include the expansion of export markets, rising domestic consumption, and the growing popularity of wine as a lifestyle product. Additionally, regional trade agreements and improved distribution networks are facilitating greater market access and competitiveness.

Middle East & Africa

The Middle East & Africa region holds around 4% of global share, with demand primarily concentrated in tourism-driven markets such as the United Arab Emirates and South Africa. The leading drivers of regional growth include the expansion of the luxury hospitality sector, increasing international tourism, and the rising presence of premium dining establishments. In addition, South Africa’s well-established wine industry is contributing to both domestic consumption and export growth. Despite regulatory challenges in certain markets, the region presents significant opportunities for premium sweet wines, particularly in high-end hospitality and duty-free retail segments.

Key Players in the Global Sweet Wine Market

- E. & J. Gallo Winery

- Constellation Brands

- Pernod Ricard

- Treasury Wine Estates

- Castel Group

- Caviro Group

- The Wine Group

- Bacardi Limited

- Grupo Peñaflor

- Henkell Freixenet

- Kendall-Jackson Wines

- Sogrape Vinhos

- Antinori Family Estates

- Casella Family Brands (Yellow Tail)

- Symington Family Estates