Sweet Sauces Market Size

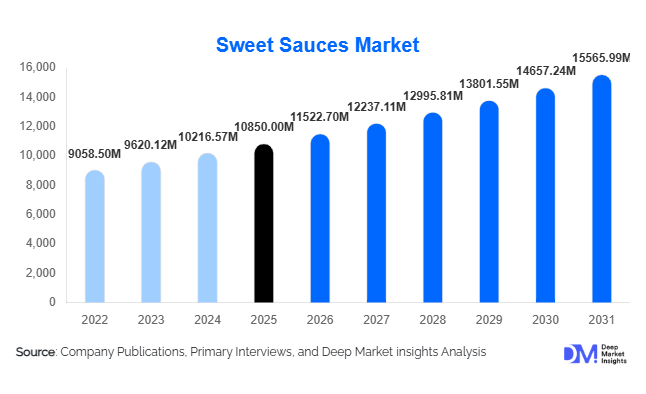

According to Deep Market Insights, the global sweet sauces market size was valued at USD 10,850 million in 2026 and is projected to grow from USD 11,522.70 million in 2026 to reach USD 15,565.99 million by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The sweet sauces market growth is primarily driven by the rising consumption of desserts and bakery products, rapid expansion of café and quick-service restaurant (QSR) chains, and increasing consumer demand for premium, clean-label, and flavored dessert toppings across global markets.

Key Market Insights

- Chocolate-based sweet sauces dominate global consumption, supported by strong demand in bakery, confectionery, and ice cream applications.

- Asia-Pacific leads global demand, driven by urbanization, café culture expansion, and rising disposable incomes in China and India.

- North America remains a high-value market, supported by strong café chains, high per-capita dessert consumption, and premium product adoption.

- Online retail is the fastest-growing distribution channel, driven by D2C brands, specialty gourmet sauces, and subscription-based baking kits.

- Health-conscious formulations are gaining momentum, including sugar-free, organic, vegan, and low-calorie sweet sauces.

- Foodservice and QSR expansion is a key demand driver, with increasing use of sweet sauces in beverages, desserts, and customization menus.

What are the latest trends in the sweet sauces market?

Clean-Label and Functional Sweet Sauce Innovation

The sweet sauces market is witnessing a strong shift toward clean-label, natural, and functional formulations. Consumers are increasingly rejecting artificial flavors and high-sugar formulations in favor of organic, plant-based, and alternative sweetener-based products. Manufacturers are introducing sugar-free chocolate sauces, keto-friendly caramel syrups, and fruit-based toppings with minimal preservatives. Functional enhancements such as added protein, fiber, and vitamin enrichment are also emerging, particularly in premium bakery and beverage applications. This trend is further supported by regulatory pressure on sugar content labeling and rising health awareness, especially in developed economies.

Digital Commerce and D2C Brand Expansion

E-commerce platforms are reshaping the sweet sauces industry by enabling direct-to-consumer sales of niche and premium products. Online channels allow small and emerging brands to compete with established FMCG companies by targeting specific consumer segments such as home bakers and gourmet dessert enthusiasts. Subscription-based baking kits, DIY dessert packs, and bundled sauce offerings are gaining popularity. Social media marketing and influencer-driven food content are also significantly boosting product visibility, particularly among younger consumers seeking convenient dessert solutions at home.

What are the key drivers in the sweet sauces market?

Rising Dessert Consumption and Western Food Influence

The increasing adoption of Western-style desserts such as pancakes, waffles, brownies, milkshakes, and sundaes is significantly driving demand for sweet sauces globally. Urban consumers in emerging economies are rapidly shifting toward café-style food consumption, where sweet sauces are essential components of dessert customization. This cultural transformation is expanding both retail and foodservice demand, particularly in Asia-Pacific and Latin America, where dessert consumption is rising at a faster pace than traditional markets.

Expansion of QSRs and Café Chains

The global expansion of quick-service restaurants and specialty coffee chains is a major growth driver for the sweet sauces market. These establishments use standardized sauces in beverages, desserts, and seasonal menu innovations. The increasing popularity of customizable drinks, flavored coffees, and premium desserts has created consistent bulk demand for chocolate, caramel, and fruit-based sauces. Long-term supply agreements between manufacturers and global foodservice brands further stabilize demand and support market scalability.

Product Premiumization and Flavor Innovation

Manufacturers are increasingly focusing on premiumization strategies, offering gourmet and artisanal sweet sauces with unique flavor profiles. Innovations such as salted caramel, exotic fruit blends, and organic chocolate sauces are attracting high-income consumers. Additionally, innovation in packaging such as squeezable bottles and portion-controlled sachets is improving convenience and driving retail sales growth across developed markets.

What are the restraints for the global market?

Volatility in Raw Material Prices

The sweet sauces market is highly dependent on raw materials such as cocoa, sugar, dairy, and fruit concentrates. Price fluctuations in these commodities significantly impact production costs and profit margins. Climate change, supply chain disruptions, and geopolitical factors further intensify raw material volatility, particularly in cocoa-producing regions of West Africa, creating uncertainty for manufacturers.

Health Concerns and Sugar Reduction Regulations

Growing awareness of obesity, diabetes, and sugar-related health issues is limiting the consumption of traditional high-sugar sweet sauces. Governments across several regions are implementing sugar taxes and strict labeling regulations, which are forcing manufacturers to reformulate products. While this creates innovation opportunities, it also increases compliance costs and may slow down demand for conventional sweet sauce products.

What are the key opportunities in the sweet sauces industry?

Expansion of Health-Oriented Product Segments

There is a strong opportunity for manufacturers to develop low-sugar, organic, vegan, and functional sweet sauces. The rising demand for healthier indulgence is enabling brands to reposition traditional dessert sauces as guilt-free products. Sugar alternatives such as stevia and monk fruit are increasingly being used to target diabetic and health-conscious consumers, opening new premium revenue streams.

Growth of Foodservice Customization Demand

The foodservice sector presents a major opportunity due to rising demand for customizable desserts and beverages. Cafés and QSR chains are increasingly offering personalized menu options that rely heavily on flavored sauces. Manufacturers that can provide consistent quality, bulk supply, and customized formulations are gaining long-term institutional contracts, ensuring stable revenue growth.

Emergence of Emerging Market Consumption Growth

Emerging economies in Asia-Pacific, Latin America, and parts of the Middle East are experiencing rapid growth in bakery and café culture. Rising disposable incomes, urbanization, and Western food adoption are driving new consumption patterns. This creates significant expansion opportunities for global brands entering untapped regional markets with affordable and mid-range sweet sauce offerings.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10850.00 Million |

| Market Size in 2026 | USD 11522.70 Million |

| Market Size in 2031 | USD 15565.99 Million |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global sweet wine market demonstrates a nuanced segmentation across product types, with fortified sweet wines firmly establishing themselves as the dominant category, accounting for approximately 34% of global share in 2025. This leadership position is underpinned by the enduring popularity of traditional varieties such as Port, Sherry, and Madeira, which benefit from strong brand heritage, long-standing consumer loyalty, and established production techniques. The leading segment driver for fortified wines lies in their extended shelf life, higher alcohol content, and suitability for both standalone consumption and food pairing, particularly in premium dining settings. Additionally, these wines have a well-developed export market, enabling producers to maintain consistent global demand.Aromatized sweet wines are gaining traction, particularly in urban and cosmopolitan markets, where consumers are increasingly open to experimentation and innovative flavor profiles. These wines are often infused with botanicals, herbs, or spices, making them highly versatile for cocktail applications. The leading driver for this segment is the rapid growth of mixology culture and the increasing popularity of wine-based cocktails in bars and restaurants. As consumer tastes evolve toward more diverse and customizable drinking experiences, aromatized sweet wines are likely to witness sustained demand growth.

Application / End-Use Insights

The application landscape of the sweet wine market is largely dominated by the hospitality sector, which accounts for nearly 48% of global demand. This segment encompasses restaurants, hotels, luxury resorts, and bars, where sweet wines are often positioned as dessert accompaniments or premium beverage offerings. The leading segment driver is the strong integration of sweet wines into curated dining experiences, where sommeliers and chefs play a crucial role in influencing consumer choices. The continued expansion of the global hospitality industry, particularly in emerging economies, further reinforces this segment’s dominance.Wine tourism and vineyard experiences are emerging as high-value niche applications, especially in established wine regions across Europe and North America. Consumers are increasingly seeking immersive experiences that combine travel, education, and premium wine tasting. The leading driver for this segment is experiential tourism, which emphasizes authenticity and direct engagement with producers. This trend not only boosts on-site consumption but also strengthens brand loyalty and drives future purchases through direct channels.

Distribution Channel Insights

Distribution channels play a pivotal role in shaping the accessibility and visibility of sweet wines, with off-trade channels dominating the market and accounting for approximately 63% share. Supermarkets, hypermarkets, specialty wine stores, and online retail platforms form the backbone of this segment. The leading driver is widespread availability combined with competitive pricing strategies, which allow consumers to conveniently purchase wines for personal consumption. Retail chains also benefit from economies of scale and strong supplier relationships, enabling them to offer diverse product portfolios.Digital platforms and influencer-led marketing are increasingly influencing purchasing decisions, particularly among younger consumers. Social media channels, wine blogs, and online communities serve as important touchpoints for product discovery and brand awareness. The leading driver here is the growing importance of digital influence and peer recommendations, which can significantly impact consumer preferences and buying behavior. As digital ecosystems continue to evolve, their role in shaping the sweet wine market is expected to expand further.

Explore more data points, trends and opportunities Download Free Sample Report

Sweet Sauces Market Segmentations

By Product Type

- Chocolate-Based Sweet Sauces

- Caramel-Based Sauces

- Fruit-Based Sauces

- Dessert Syrups

- Dairy-Based Sweet Sauces

- Specialty & Gourmet Sweet Sauces

By Ingredient Source

- Natural Ingredients-Based Sauces

- Organic Certified Sauces

- Conventional/Synthetic Flavor Sauces

- Sugar-Free & Alternative Sweetener Sauces

By Application

- Bakery & Confectionery

- Ice Cream & Frozen Desserts

- Beverages

- HoReCa

- Household Consumption

- Industrial Food Processing

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Foodservice Distribution

- Specialty Stores

By Packaging Type

- Bottles

- Squeeze Tubes

- Pouches & Sachets

- Bulk Foodservice Containers

Regional Insights

Europe

Europe leads the global sweet wine market with approximately 38% share, supported by its deep-rooted wine culture and long-established production traditions in countries such as France, Italy, Spain, Portugal, and Germany. The region benefits from a highly developed ecosystem that includes vineyards, skilled labor, advanced production techniques, and strong regulatory frameworks that ensure product quality and authenticity. One of the primary growth drivers in Europe is its robust export infrastructure, which enables producers to access international markets efficiently and maintain a strong global presence.Additionally, the increasing popularity of wine tourism across European regions such as Bordeaux, Tuscany, and the Douro Valley is driving both domestic and international demand for sweet wines. Consumers visiting these regions often engage in tastings and vineyard tours, creating a direct connection with producers and enhancing brand loyalty. Another key driver is the rising demand for premium and artisanal wines, as consumers seek unique and high-quality products with distinct regional characteristics. Sustainability initiatives and organic wine production are also gaining traction, further strengthening the region’s competitive advantage.

North America

North America accounts for approximately 25% of the global sweet wine market, with the United States serving as the primary contributor. The region is characterized by a well-developed retail infrastructure, high consumer purchasing power, and a strong inclination toward premium and luxury products. One of the leading growth drivers in North America is the increasing consumer interest in dessert wines and food pairing experiences, particularly within urban and affluent populations.The expansion of e-commerce platforms and direct-to-consumer sales channels has significantly enhanced market accessibility, allowing wineries to reach a broader audience. Additionally, the growing influence of wine education programs, tasting events, and sommelier culture is fostering greater awareness and appreciation of sweet wines. Innovation in product offerings, including low-alcohol and flavored variants, is also contributing to market growth by attracting new consumer segments.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the global sweet wine market, driven by countries such as China, India, Japan, and Australia. Rapid urbanization, rising disposable incomes, and the expansion of the middle class are key factors contributing to increased wine consumption. The leading regional growth driver is the growing awareness and adoption of Western lifestyles, which includes the incorporation of wine into social and dining experiences.In addition, the proliferation of online retail platforms and digital marketing strategies is making imported sweet wines more accessible to consumers across the region. Governments in several countries are also supporting the development of domestic wine industries, further boosting market growth. The increasing popularity of wine as a gift item and its association with status and sophistication are additional factors driving demand. As consumer preferences continue to evolve, Asia-Pacific is expected to play a pivotal role in shaping the future trajectory of the global sweet wine market.

Latin America

Latin America holds approximately 6–7% of the global market share, with countries such as Chile, Argentina, and Brazil serving as key contributors. The region benefits from favorable climatic conditions for viticulture, enabling the production of high-quality wines at competitive prices. One of the primary growth drivers is the expansion of export markets, particularly to North America and Europe, where Latin American wines are gaining recognition for their value and quality.Domestic consumption is also on the rise, supported by increasing urbanization and changing consumer preferences. The growth of the hospitality and tourism sectors is further driving demand for sweet wines, particularly in popular tourist destinations. Additionally, government initiatives aimed at promoting the wine industry and enhancing production capabilities are contributing to market development.

Middle East & Africa

The Middle East and Africa (MEA) region accounts for around 4% of the global sweet wine market, with demand primarily concentrated in tourism-driven economies such as the United Arab Emirates and South Africa. The leading growth driver in this region is the expansion of the luxury hospitality sector, which includes high-end hotels, resorts, and fine dining establishments that cater to international tourists and affluent consumers.In South Africa, a well-established wine industry supports both domestic consumption and exports, while in the Middle East, demand is largely driven by expatriate populations and tourism. The increasing number of international events, exhibitions, and business conferences is also contributing to higher consumption of premium beverages, including sweet wines. Despite regulatory challenges in certain markets, the region presents significant growth potential, particularly as tourism continues to recover and expand.

Key Players in the Sweet Sauces Market

- Nestlé S.A.

- The Hershey Company

- Monin

- Dr. Oetker

- Kerry Group

- Unilever

- Tate & Lyle

- Barry Callebaut

- FrieslandCampina

- The J.M. Smucker Company

- Puratos

- Kraft Heinz Company

- Torani

- Pinnacle Foods

- Conagra Brands