Sweet Baked Goods Market Size

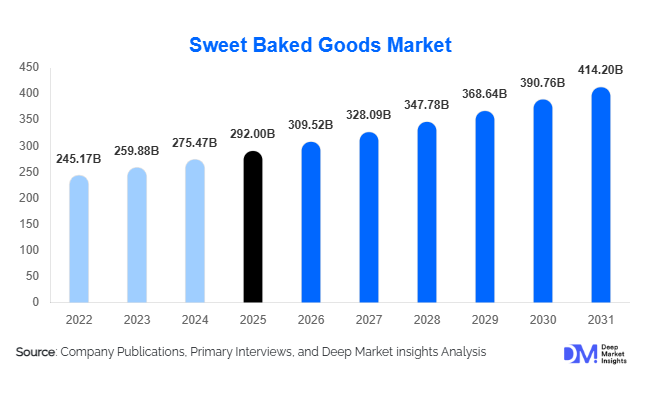

According to Deep Market Insights, the global sweet baked goods market size was valued at USD 292 million in 2025 and is projected to grow from USD 309.52 million in 2026 to reach USD 414.20 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for convenient ready-to-eat snacks, increasing urbanization, and the growing popularity of premium and indulgent bakery products across both developed and emerging economies.

Key Market Insights

- Packaged sweet baked goods dominate the market, supported by longer shelf life and expanding retail distribution networks globally.

- Cookies and biscuits hold the largest product share, driven by affordability, convenience, and high consumption frequency.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and Western dietary influence.

- Health-focused innovations are gaining traction, including gluten-free, low-sugar, and functional baked goods.

- E-commerce and quick commerce platforms are transforming distribution and boosting direct-to-consumer sales.

- Premium and artisanal segments are expanding, particularly in urban centers with higher consumer spending capacity.

What are the latest trends in the sweet baked goods market?

Health-Oriented Reformulation and Clean Labeling

Consumers are increasingly demanding healthier alternatives within indulgent categories, leading manufacturers to reformulate products with reduced sugar, whole grains, and natural ingredients. Clean-label trends are driving transparency in ingredient sourcing, with brands focusing on eliminating artificial preservatives and additives. Gluten-free and plant-based baked goods are gaining traction, particularly among health-conscious and allergen-sensitive consumers. Functional ingredients such as protein, fiber, and probiotics are also being incorporated into products to enhance nutritional value while maintaining taste and texture.

Rise of Premium and Artisanal Offerings

The premiumization trend is reshaping the sweet baked goods market, with consumers seeking high-quality, handcrafted products that offer unique flavors and superior ingredients. Artisanal bakeries and gourmet brands are gaining popularity, particularly in metropolitan areas. These products often command higher price points due to perceived quality, authenticity, and aesthetic appeal. Limited-edition flavors, seasonal offerings, and fusion recipes are also driving consumer engagement and repeat purchases.

What are the key drivers in the sweet baked goods market?

Growing Demand for Convenience Foods

The increasing pace of modern lifestyles has significantly boosted demand for ready-to-eat and on-the-go food options. Sweet baked goods such as cookies, muffins, and pastries are widely consumed as quick snacks or meal replacements. The expansion of retail chains and availability of packaged products have further enhanced accessibility, making convenience a key growth driver for the market.

Expansion of Organized Retail and E-commerce

The rapid growth of supermarkets, hypermarkets, and online platforms has improved product visibility and availability. E-commerce platforms, in particular, are enabling brands to reach a broader consumer base through direct-to-consumer models. Subscription services, online bakery stores, and quick delivery platforms are further accelerating market growth, especially in urban areas.

What are the restraints for the global market?

Health Concerns Related to Sugar and Calorie Intake

Rising awareness of lifestyle diseases such as obesity and diabetes is leading consumers to limit their intake of high-sugar baked goods. This shift in consumer behavior is impacting traditional product demand and forcing manufacturers to innovate healthier alternatives.

Volatility in Raw Material Prices

Fluctuations in the prices of key ingredients such as wheat, sugar, and dairy products pose a significant challenge for manufacturers. These cost variations can impact profit margins and lead to price adjustments, potentially affecting consumer demand in price-sensitive markets.

What are the key opportunities in the sweet baked goods industry?

Expansion in Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and Africa present significant growth opportunities due to rising urbanization, increasing disposable incomes, and changing dietary preferences. Localization of flavors combined with global quality standards can help brands capture these high-growth markets.

Digital and Direct-to-Consumer Models

The growth of e-commerce and digital platforms is creating new avenues for market expansion. Brands are leveraging online channels to offer personalized products, subscription services, and direct engagement with consumers. Cloud bakeries and online-only brands are reducing operational costs while expanding reach.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 292 Billion |

| Market Size in 2026 | USD 309.52 Billion |

| Market Size in 2031 | USD 414.20 Billion |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global sweet baked goods market demonstrates strong diversification across multiple product categories, with cookies and biscuits emerging as the dominant segment, accounting for approximately 28% of the total market share in 2025. This dominance is primarily driven by their long shelf life, affordability, ease of mass production, and widespread acceptance across all age groups and geographies. Cookies and biscuits also benefit from continuous product innovation in flavors, functional ingredients, and health-oriented formulations such as high-fiber, low-sugar, gluten-free, and protein-enriched variants. Manufacturers are increasingly focusing on premiumization within this category by introducing chocolate-coated, filled, and artisanal variants that cater to evolving consumer taste preferences and impulse snacking behavior.Donuts and muffins are gaining strong traction as convenient, on-the-go snack options, especially among younger consumers and working professionals. Their portability, variety, and suitability for breakfast and mid-day snacking occasions make them increasingly popular in urban lifestyles. Muffins, in particular, are benefiting from health-focused formulations incorporating oats, fruits, nuts, and reduced sugar content. Meanwhile, donuts are being repositioned from indulgent treats to premium dessert offerings through gourmet fillings and artisanal preparation techniques.Premium baked goods such as artisanal cakes, handcrafted pastries, and specialty desserts are experiencing rapid growth, driven by rising consumer willingness to pay for unique experiences and high-quality ingredients. This segment is also supported by social media influence, where visually appealing desserts play a significant role in consumer purchasing decisions. Overall, the product landscape is evolving toward a balance between mass-market affordability and premium experiential offerings.

Application (End-Use) Insights

Household consumption remains the largest application segment in the sweet baked goods market, contributing nearly 70% of total demand. This dominance is primarily attributed to daily snacking habits, increased availability of packaged baked products, and the growing preference for ready-to-eat food items that require minimal preparation. Busy lifestyles, dual-income households, and rising urbanization have further strengthened at-home consumption patterns. Consumers are increasingly purchasing baked goods as part of routine grocery shopping, often driven by convenience, affordability, and variety.Institutional demand, which includes airlines, schools, hospitals, corporate cafeterias, and catering services, is also witnessing steady growth. This segment benefits from large-scale procurement requirements and standardized product offerings. In emerging economies, government-supported nutrition programs and school meal initiatives are contributing to increased consumption of packaged baked goods. Additionally, airlines and travel-related food services continue to rely on packaged cookies, muffins, and cakes due to their durability and ease of storage.Export-driven demand plays a significant role in shaping the global baked goods market, with major production hubs supplying packaged and frozen baked products across international markets. Globalization of food preferences, coupled with improved cold chain logistics and e-commerce expansion, has enabled manufacturers to reach new consumer bases. Overall, application trends highlight a strong balance between everyday household consumption and rapidly expanding commercial and institutional usage.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channels in the sweet baked goods market, accounting for approximately 35% of total sales. These retail formats offer extensive product variety, strong brand visibility, and attractive promotional strategies that encourage impulse purchases. The availability of both mass-market and premium bakery products under one roof enhances consumer convenience and drives higher basket value. Strategic product placement, seasonal promotions, and private label offerings further strengthen this channel’s dominance.Specialty bakery stores cater to premium and artisanal product segments, offering freshly baked, high-quality, and customized products. These stores are gaining popularity among consumers seeking differentiated taste experiences and handcrafted bakery items. The growth of boutique bakeries in metropolitan areas is further enhancing the appeal of this channel.Online retail is the fastest-growing distribution channel, driven by rapid digital adoption, increasing smartphone penetration, and evolving consumer preferences for home delivery services. E-commerce platforms and direct-to-consumer bakery brands are leveraging subscription models, personalized offerings, and digital marketing strategies to expand their customer base. The convenience of doorstep delivery, coupled with access to a wider product assortment, continues to accelerate online channel growth.Foodservice distribution also plays an essential role, particularly in urban centers where consumption of bakery products is closely linked to café visits, restaurant dining, and quick-service meals. The integration of bakery items into foodservice menus continues to expand overall market penetration.

Price Range Insights

The mid-range product category dominates the market with approximately 50% share, as it effectively balances affordability and quality. This segment appeals to a broad consumer base, including middle-income households in both developed and emerging markets. Manufacturers focus on delivering value-added products with improved taste, packaging, and nutritional benefits while maintaining competitive pricing.Economy products cater primarily to price-sensitive consumers, especially in developing regions where affordability remains a key purchasing factor. This segment is characterized by high-volume sales, standardized formulations, and strong penetration in rural and semi-urban markets. Large-scale manufacturers leverage cost-efficient production methods to maintain competitiveness in this category.Premium and artisanal baked goods are gaining significant traction in urban markets due to rising disposable incomes, changing lifestyle patterns, and increasing demand for experiential food consumption. Consumers in this segment are willing to pay a premium for high-quality ingredients, unique flavors, and aesthetically appealing products. The influence of social media and food culture trends has further amplified demand for visually distinctive and gourmet bakery offerings.

Explore more data points, trends and opportunities Download Free Sample Report

Sweet Baked Goods Market Segmentations

By Product Type

- Cakes

- Pastries

- Cookies & Biscuits

- Sweet Pies & Tarts

- Donuts

- Muffins & Cupcakes

- Sweet Rolls & Buns

- Others

By Ingredient Type

- Wheat-Based

- Gluten-Free

- Organic Ingredients

- Low-Sugar / Sugar-Free

- Functional Ingredients

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Bakery Stores

- Online Retail / E-commerce

- Foodservice

Regional Insights

North America

North America holds around 30% of the global market share, led by strong consumption patterns in the United States and Canada. The region’s growth is driven by well-established retail infrastructure, high demand for convenience foods, and strong brand presence of major bakery manufacturers. A key growth driver in this region is the increasing preference for ready-to-eat and packaged snacks, supported by busy lifestyles and high workforce participation. Additionally, rising health consciousness is encouraging manufacturers to innovate with organic, low-calorie, and clean-label baked goods. The strong presence of café chains and quick-service restaurants further strengthens demand for premium bakery items.

Europe

Europe accounts for approximately 28% of the global market, supported by long-standing bakery traditions and high per capita consumption of baked goods. Countries such as Germany, France, and the United Kingdom continue to dominate regional demand. Growth in Europe is driven by increasing demand for artisanal and premium bakery products, strong emphasis on quality ingredients, and a mature retail landscape. Sustainability trends are also influencing product development, with manufacturers focusing on organic sourcing, eco-friendly packaging, and reduced food waste. The region’s strong café culture and bakery heritage further reinforce steady market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of over 7.5%, driven by rapid urbanization, rising disposable incomes, and changing dietary habits. China, India, and Japan are the key contributors to regional growth. A major driver is the increasing adoption of Western-style food habits among younger consumers, coupled with the expansion of modern retail formats and foodservice chains. The region is also witnessing significant growth in online food delivery platforms, which are improving access to bakery products. Additionally, increasing population density in urban areas is fueling demand for convenient and affordable snack options.

Latin America

Latin America holds about 8% of the global market share, with Brazil and Mexico leading regional demand. Growth in this region is primarily driven by expanding retail infrastructure, increasing penetration of packaged food products, and rising urban middle-class populations. Consumers are gradually shifting from traditional homemade baked goods to packaged and branded alternatives due to convenience and improved shelf life. Economic development and growing exposure to global food trends are further supporting market expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the market, with growth driven by rapid urbanization, increasing tourism activity, and rising demand for premium bakery products in countries such as the UAE and Saudi Arabia. The region is witnessing a shift toward modern retail formats and international bakery chains, which is enhancing product availability and consumer awareness. Rising expatriate populations and changing dietary preferences are also contributing to market growth. Additionally, premiumization trends are gaining traction, particularly in urban centers where consumers are increasingly seeking high-quality and indulgent baked goods.

Key Players in the Sweet Baked Goods Market

- Mondelez International

- Nestlé

- Grupo Bimbo

- Kellogg Company

- General Mills

- Britannia Industries

- Associated British Foods

- Yamazaki Baking

- Flowers Foods

- Hostess Brands

- McKee Foods

- Aryzta AG

- Campbell Soup Company

- Lantmännen Unibake

- Barilla Group