Sweet and Salty Snacks Market Size

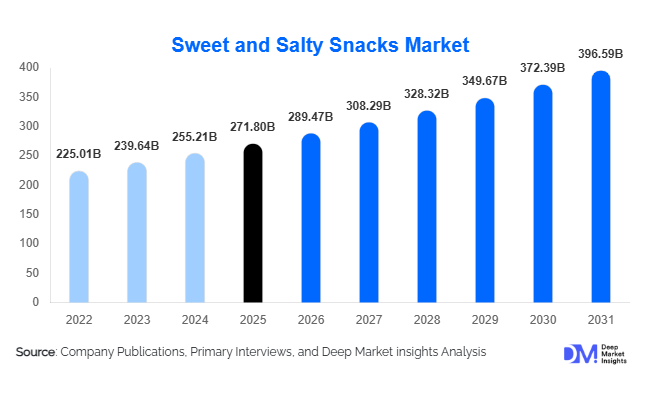

According to Deep Market Insights, the global sweet and salty snacks market size was valued at USD 271.8 billion in 2025 and is projected to grow from USD 289.47 billion in 2026 to reach USD 396.59 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The sweet and salty snacks market growth is primarily driven by changing consumer eating habits, increasing demand for convenient on-the-go foods, rapid urbanization, and strong innovation across healthy, premium, and indulgent snack categories. Rising penetration of organized retail, quick-commerce delivery platforms, and e-commerce grocery channels is further accelerating global consumption of packaged snacks across developed and emerging economies.

Key Market Insights

- Consumers are increasingly shifting toward healthier snacking options, driving demand for baked snacks, low-sugar products, high-protein snacks, and clean-label formulations.

- Hybrid sweet-salty flavor combinations are gaining strong consumer traction, particularly among millennials and younger demographics seeking innovative taste experiences.

- North America dominates the global sweet and salty snacks market, supported by high per-capita snack consumption and strong retail penetration.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising disposable income, westernized eating habits, and expansion of modern retail infrastructure.

- Digital commerce and quick-delivery ecosystems are transforming snack distribution, enabling premium and niche brands to expand rapidly through direct-to-consumer models.

- Technological innovation in packaging and manufacturing, including AI-driven product analytics, sustainable packaging, and automated production systems, is reshaping competitive dynamics.

Sweet and Salty Snacks Market Latest Trends

Health-Focused Snacking Transforming Product Innovation

Health and wellness trends are significantly influencing product development strategies across the sweet and salty snacks industry. Consumers are increasingly seeking products with lower sodium, reduced sugar, high protein, whole grains, natural sweeteners, and clean-label ingredients. Manufacturers are reformulating traditional snacks while introducing healthier alternatives such as baked chips, protein-rich trail mixes, plant-based puffs, gluten-free crackers, and low-calorie popcorn. Functional snacks enriched with probiotics, vitamins, adaptogens, and fiber are also witnessing rising popularity among health-conscious consumers. This shift is encouraging companies to balance indulgence with nutritional positioning, creating opportunities for premium pricing and improved brand loyalty across both mature and emerging markets.

Premiumization and Flavor Diversification Accelerating Growth

Consumers globally are increasingly willing to pay premium prices for unique flavors, artisanal ingredients, and elevated snacking experiences. Premium snack categories featuring gourmet seasonings, international flavors, exotic spices, organic ingredients, and limited-edition offerings are expanding rapidly. Flavor innovation such as salted caramel, sweet chili, spicy chocolate, truffle-infused popcorn, and fusion snack combinations are attracting younger consumers seeking experimentation and novelty. Manufacturers are leveraging regional flavor preferences and seasonal launches to maintain strong consumer engagement. Additionally, sustainable packaging, aesthetically appealing branding, and small-batch production strategies are strengthening the premiumization trend across global snack portfolios.

Sweet and Salty Snacks Market Drivers

Growing Demand for Convenience and On-the-Go Foods

One of the primary drivers of the sweet and salty snacks market is the growing global preference for convenient and portable food products. Busy lifestyles, increasing urbanization, dual-income households, and changing work patterns have significantly increased snacking frequency worldwide. Consumers increasingly prefer packaged snacks as meal replacements, workplace snacks, travel foods, and entertainment companions. The expansion of convenience stores, supermarkets, vending channels, and quick-commerce platforms has further improved accessibility and impulse purchases across all demographic groups. This convenience-driven consumption trend continues to support strong long-term demand growth globally.

Rapid Expansion of Organized Retail and E-Commerce

The rapid growth of organized retail infrastructure and online grocery ecosystems is playing a crucial role in market expansion. Large supermarket chains, warehouse clubs, hypermarkets, and convenience retailers provide extensive shelf visibility, promotional campaigns, and diversified snack assortments that stimulate consumer spending. Simultaneously, e-commerce platforms and instant delivery services are accelerating accessibility to premium, imported, and niche snack categories. Online channels are particularly beneficial for health-focused and direct-to-consumer brands that rely heavily on digital marketing and subscription-based engagement strategies. The growth of digital commerce is also improving consumer data analytics and personalized product recommendations.

Global Market Restraints

Regulatory Pressure on Sugar and Sodium Content

Governments and public health organizations across multiple countries are increasingly implementing stricter regulations regarding sugar, sodium, and unhealthy ingredient consumption. Nutritional labeling requirements, sugar taxes, advertising restrictions targeting children, and front-of-pack warning systems are creating operational challenges for snack manufacturers. Companies are under pressure to reformulate products while maintaining taste profiles and consumer loyalty. Compliance costs related to reformulation, testing, and packaging updates may negatively impact profit margins, especially among smaller regional manufacturers with limited R&D capabilities.

Volatility in Raw Material and Packaging Costs

The sweet and salty snacks market remains highly exposed to fluctuations in agricultural commodity prices and supply chain disruptions. Key raw materials such as potatoes, corn, edible oils, cocoa, dairy ingredients, nuts, and sugar are vulnerable to climate change, geopolitical instability, and transportation cost inflation. Packaging material prices, particularly for flexible plastics, aluminum, and paperboard, have also experienced significant volatility. These cost pressures impact manufacturing margins and often force companies to adopt aggressive pricing strategies, shrinkflation, or product reformulation to maintain profitability in competitive markets.

Sweet and Salty Snacks Industry Key Opportunities

Functional and Protein-Based Snacks Creating New Demand

The growing popularity of functional nutrition presents substantial opportunities for snack manufacturers globally. Consumers increasingly seek snacks that provide satiety, energy enhancement, digestive health support, immunity benefits, and fitness-oriented nutrition. High-protein bars, nut-based snacks, plant-protein crisps, fortified granola products, and probiotic snack formulations are witnessing strong growth across both developed and emerging economies. Fitness-conscious millennials and working professionals are particularly driving adoption of meal-replacement and functional snack products. Companies investing in plant-based ingredients, sports nutrition partnerships, and wellness-focused innovation are expected to gain significant competitive advantages in the coming years.

Expansion Across Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East & Africa present major untapped opportunities for the sweet and salty snacks industry. Rising disposable incomes, urbanization, westernized dietary preferences, and increasing penetration of organized retail are significantly expanding the addressable consumer base. Countries such as India, China, Indonesia, Brazil, Saudi Arabia, and Vietnam are witnessing rapid growth in branded packaged snack consumption, especially among younger demographics. Manufacturers are increasingly localizing flavors and introducing region-specific products such as masala snacks, spicy chips, seaweed snacks, and ethnic fusion offerings to improve market penetration and brand acceptance.

Product Type Insights

Potato chips continued to dominate the global sweet and salty snacks market in 2025, accounting for nearly 24% of total market revenue. The segment’s leadership is primarily driven by strong consumer familiarity, affordable pricing, extensive product availability across supermarkets, convenience stores, and online retail channels, as well as continuous flavor innovation introduced by leading manufacturers. Growing consumer preference for convenient ready-to-eat foods and impulse snacking behavior has further strengthened product demand across both developed and emerging economies. In addition, premiumization trends are accelerating the popularity of kettle-cooked chips, baked chips, air-fried variants, and low-fat formulations as consumers increasingly seek indulgent yet comparatively healthier snack options. Manufacturers are also investing heavily in regional flavor customization, limited-edition launches, and clean-label formulations to strengthen brand loyalty and maintain competitive differentiation.Sweet bakery snacks including cookies, biscuits, brownies, wafers, pastries, and confectionery products continue to witness strong global demand due to their high consumption frequency, gifting appeal, and broad acceptance across all age groups. Demand for premium chocolate-coated snacks, filled biscuits, and indulgent dessert-inspired products is increasing rapidly among urban consumers seeking comfort foods and affordable indulgence. Furthermore, hybrid sweet-salty snack categories such as salted caramel popcorn, chocolate-covered pretzels, sweet-spicy nuts, and flavored trail mixes are emerging as some of the fastest-growing product categories globally. Rising consumer interest in unique taste experiences, fusion flavors, and premium snacking occasions continues to support the expansion of these innovative snack formats.

Ingredient Type Insights

Grain-based snacks remained the leading ingredient category in the global sweet and salty snacks market in 2025, accounting for approximately 29% of overall market revenue. The dominance of this segment is largely attributed to the affordability, versatility, long shelf life, and mass consumer appeal of grain-derived products such as crackers, biscuits, cereal bars, pretzels, popcorn, and extruded snacks. Rising consumer demand for convenient on-the-go foods and increasing adoption of fortified snack products are further supporting category expansion worldwide. In addition, manufacturers are increasingly incorporating whole grains, oats, ancient grains, and fiber-rich ingredients into snack formulations to align with growing health-conscious consumption trends.Potato-based snacks continue to contribute significantly to global market revenues, particularly across North America and Europe where potato chips and savory crisps maintain exceptionally high household penetration. Meanwhile, nut-based snacks are witnessing accelerated growth due to increasing demand for protein-rich, keto-friendly, and functional snack products among fitness-oriented consumers. Almonds, peanuts, cashews, pistachios, and mixed nuts are increasingly being positioned as healthier alternatives to traditional fried snacks. Fruit-based snacks, plant-based proteins, and natural ingredient formulations are also gaining momentum as consumers increasingly prioritize clean-label products, reduced artificial additives, and minimally processed foods. The growing popularity of vegan lifestyles and functional nutrition trends is expected to further support innovation across ingredient categories during the forecast period.

Distribution Channel Insights

Supermarkets and hypermarkets remained the dominant distribution channel in the global sweet and salty snacks market in 2025, accounting for nearly 48% of total market revenue. The segment’s leadership is primarily supported by extensive product assortments, strong brand visibility, attractive promotional pricing strategies, and the convenience of one-stop shopping experiences. Large retail chains continue to play a critical role in encouraging impulse purchases through in-store displays, discount campaigns, bundled offers, and strategic shelf placement. Expanding organized retail infrastructure across developing economies is also contributing significantly to channel growth.Convenience stores continue to represent a major sales channel for snack products due to rising urbanization, busy consumer lifestyles, and high-frequency purchases of ready-to-eat foods. Demand for single-serve packaging, portable snacks, and immediate consumption products remains particularly strong within this channel. However, online retail and direct-to-consumer platforms are witnessing the fastest growth globally as digital grocery adoption continues to accelerate. E-commerce marketplaces, quick-commerce delivery services, subscription snack boxes, and brand-owned digital platforms are enabling manufacturers to expand consumer reach while offering personalized recommendations and premium product selections. Increasing smartphone penetration, improved digital payment infrastructure, and rapid home-delivery services are further supporting the strong expansion of online snack retail worldwide.

Health Positioning Insights

High-protein snacks emerged as one of the fastest-growing health-positioned categories within the global sweet and salty snacks market in 2025 and accounted for nearly 14% of total market revenue. The rapid growth of this segment is being driven by rising health awareness, increasing participation in fitness activities, growing sports nutrition consumption, and expanding preference for meal-replacement snack products among working professionals and younger consumers. Protein bars, nut mixes, roasted seeds, meat snacks, dairy-based snacks, and plant-protein formulations are witnessing particularly strong demand as consumers increasingly prioritize satiety, energy support, and functional nutrition.Gluten-free, low-sugar, low-sodium, and reduced-fat snacks are also experiencing substantial growth due to rising prevalence of dietary sensitivities, obesity concerns, and greater consumer awareness regarding healthier eating habits. In addition, vegan snacks and clean-label products are becoming increasingly popular among millennials and Gen Z consumers who seek ingredient transparency, sustainability, and minimally processed foods. Manufacturers are actively reformulating products to reduce artificial preservatives, synthetic colors, and excess sugar while incorporating natural ingredients, functional additives, and plant-based proteins. The growing influence of wellness trends and preventive healthcare awareness is expected to continue reshaping product innovation across health-focused snack categories.

Consumer Group Insights

Millennials remained the largest consumer group in the global sweet and salty snacks market in 2025, driven by high snacking frequency, fast-paced lifestyles, increasing preference for convenience foods, and strong willingness to experiment with new flavors and premium products. The segment’s dominance is also supported by rising digital engagement and social media-driven food trends that significantly influence purchasing behavior. Millennials continue to drive strong demand for healthier snack alternatives, functional ingredients, premium indulgent products, and internationally inspired flavor profiles. The increasing popularity of flexible eating patterns and frequent between-meal snacking further contributes to sustained consumption growth within this demographic.Working professionals represent another major consumer segment as busy schedules and increasing work-from-home culture continue to accelerate demand for portable meal-replacement snacks and convenient office foods. Children and teenagers continue to drive substantial demand for confectionery snacks, flavored popcorn, cookies, and chips due to strong brand marketing, attractive packaging, and growing exposure to westernized snacking habits. Meanwhile, elderly consumers are gradually shifting toward low-sugar, low-sodium, digestive-health-focused, and functional snack products as awareness regarding nutrition and healthy aging continues to increase globally. Manufacturers are increasingly developing targeted product formulations and packaging strategies to cater to the evolving preferences of diverse consumer demographics.

| By Product Type | By Ingredient Type | By Health Positioning | By Distribution Channel | By Consumer Group |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 34% of global sweet and salty snacks market revenue in 2025, making it the largest regional market worldwide. Regional growth is primarily driven by exceptionally high per-capita snack consumption, strong penetration of organized retail channels, widespread availability of convenience foods, and continuous product innovation introduced by major food manufacturers. The United States dominates regional demand due to busy consumer lifestyles, rising preference for on-the-go eating habits, and strong demand for premium and functional snack products. Increasing consumer interest in protein-rich snacks, baked alternatives, organic formulations, and clean-label products is also supporting market expansion across the country. In Canada, rising health consciousness and growing adoption of organic and natural snacks continue to stimulate demand for healthier packaged food products. Mexico is witnessing increasing consumption of packaged snacks due to rapid urbanization, expanding middle-class spending, and continued development of modern retail infrastructure. Strong e-commerce penetration and aggressive promotional activities by global snack brands are further accelerating regional market growth.

Europe

Europe represented nearly 24% of global market revenue in 2025, supported by strong consumer demand across Germany, the United Kingdom, France, Italy, and Spain. Regional market growth is being driven by rising consumer preference for healthier snacking alternatives, increasing adoption of organic and gluten-free products, and strong demand for premium artisanal snack offerings. European consumers are increasingly prioritizing ingredient transparency, sustainable sourcing, and environmentally friendly packaging solutions, encouraging manufacturers to invest heavily in clean-label innovation and product reformulation. The region’s strict food labeling regulations and growing focus on nutritional awareness are further accelerating the shift toward healthier snack portfolios. In addition, premium gourmet flavors, ethnic snack varieties, and indulgent bakery snacks continue to gain popularity across Western Europe as consumers seek differentiated and high-quality snacking experiences. Expanding private-label offerings by major retail chains are also contributing significantly to regional market competitiveness and product accessibility.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing regional market in the global sweet and salty snacks industry and accounted for nearly 29% of global market share in 2025. Rapid urbanization, rising disposable incomes, expanding middle-class populations, westernization of dietary habits, and increasing penetration of modern retail channels are among the primary drivers supporting regional growth. China leads regional consumption due to its large consumer base, rapid digital commerce expansion, and strong demand for packaged convenience foods. The country’s rapidly growing e-commerce ecosystem and extensive quick-commerce delivery networks are further strengthening snack product accessibility. India is emerging as a highly attractive market driven by increasing consumption of packaged namkeen, fusion snacks, savory mixtures, and western-style snack products among younger consumers. Rising urban employment, growing retail modernization, and increasing brand penetration in tier-2 and tier-3 cities are also supporting market expansion in India.

Japan and South Korea remain innovation-oriented markets characterized by strong demand for premium packaging, seasonal flavors, limited-edition launches, and technologically advanced snack products. Consumers in these countries increasingly favor high-quality ingredients, convenience packaging, and unique taste experiences. Meanwhile, Southeast Asian markets including Indonesia, Vietnam, Thailand, and the Philippines are witnessing growing penetration of international snack brands due to rapid urban development, expanding supermarket chains, and increasing exposure to global food trends. Rising youth populations and strong social media influence continue to accelerate snack consumption across the broader Asia-Pacific region.

Latin America

Latin America accounted for nearly 7% of global sweet and salty snacks market demand in 2025, led primarily by Brazil and Mexico. Regional market growth is being supported by increasing urbanization, rising disposable income levels, a large young consumer population, and growing consumption of packaged convenience foods. Demand for affordable savory snacks, confectionery products, and locally inspired flavor profiles remains particularly strong across the region. Manufacturers are increasingly introducing spicy, tangy, and culturally adapted snack products to strengthen consumer engagement and brand differentiation. Expanding supermarket chains, convenience retail networks, and modern distribution infrastructure are improving product accessibility throughout major urban centers. In addition, increasing internet penetration and growth of online grocery platforms are gradually supporting the expansion of digital snack retail across Latin America.

Middle East & Africa

The Middle East & Africa region represented approximately 6% of global sweet and salty snacks market revenue in 2025. Regional growth is primarily driven by rising urban populations, increasing disposable incomes, expanding modern retail infrastructure, and growing consumer exposure to international food brands. Saudi Arabia and the United Arab Emirates remain the leading Middle Eastern markets due to high purchasing power, strong demand for imported packaged foods, and increasing popularity of premium snacking products among younger consumers. Rapid expansion of supermarkets, hypermarkets, and convenience retail formats is further improving product availability across the Gulf region.South Africa continues to represent the largest African market, supported by increasing urban snack consumption, expanding retail penetration, and rising adoption of westernized packaged food products. Growing awareness regarding healthier eating habits is also encouraging demand for baked snacks, reduced-sugar confectionery, and functional snack categories across several countries in the region. Furthermore, the increasing influence of international foodservice chains, digital food delivery platforms, and youth-driven consumption trends is expected to continue supporting long-term market expansion throughout the Middle East & Africa.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Sweet and Salty Snacks Market

- PepsiCo

- Mondelez International

- Kellanova

- General Mills

- Nestlé

- Calbee

- Intersnack Group

- Grupo Bimbo

- Campbell Soup Company

- The Hershey Company

- Conagra Brands

- Meiji Holdings

- Want Want China Holdings

- ITC Limited

- Orkla