Superfood Meal Replacement Powders Market Size

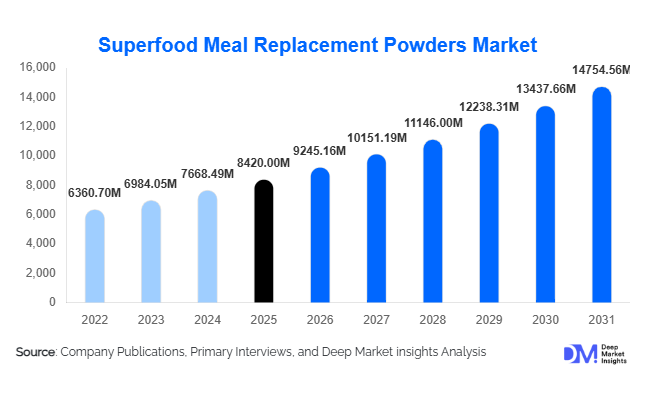

According to Deep Market Insights,the global superfood meal replacement powders market size was valued at USD 8,420 million in 2025 and is projected to grow from USD 9,245.16 million in 2026 to reach USD 14,754.56 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The market growth is primarily driven by rising demand for plant-based nutrition, increasing health consciousness, growing fitness participation, and the shift toward convenient, functional meal alternatives. Superfood meal replacement powders have evolved from niche wellness products into mainstream dietary solutions catering to weight management, sports nutrition, preventive healthcare, and busy urban lifestyles. The integration of nutrient-dense ingredients such as spirulina, chia seeds, quinoa, and adaptogens has strengthened product differentiation and premium positioning across developed and emerging markets.

Key Market Insights

- Plant-based formulations dominate the market, accounting for over 55% of total revenue share in 2025, driven by vegan and lactose-intolerant consumer demand.

- Online retail channels lead distribution, contributing nearly 41% of global sales due to subscription-based and direct-to-consumer models.

- North America holds the largest market share, representing approximately 36% of global demand in 2025.

- Asia-Pacific is the fastest-growing region, registering double-digit CAGR supported by urbanization and rising middle-class income.

- Weight management applications lead functional positioning, accounting for nearly 34% of the total market.

- Premiumization and clean-label claims, including organic, non-GMO, and allergen-free certifications, are reshaping competitive dynamics.

What are the latest trends in the superfood meal replacement powders market?

Rise of Personalized and AI-Integrated Nutrition

Consumers are increasingly seeking customized nutrition solutions tailored to metabolic profiles, fitness goals, and lifestyle preferences. Brands are integrating AI-based recommendation engines, digital health tracking platforms, and subscription-based customization models to enhance customer retention. Personalized macronutrient blends and functional add-ons such as adaptogens and probiotics are becoming common differentiators. This shift toward precision nutrition is strengthening premium pricing strategies and expanding recurring revenue streams for manufacturers.

Clean-Label and Sustainable Ingredient Sourcing

Sustainability and transparency are shaping purchasing decisions. Consumers increasingly demand ethically sourced superfoods, traceable supply chains, and eco-friendly packaging formats. Manufacturers are adopting plant-based protein extraction technologies, biodegradable pouches, and carbon-neutral production processes. Certifications such as organic, gluten-free, and non-GMO are gaining importance, particularly in North America and Europe. This trend is influencing procurement strategies and long-term supplier partnerships globally.

What are the key drivers in the superfood meal replacement powders market?

Growing Preventive Healthcare Awareness

The global shift toward preventive healthcare and functional nutrition is a major growth catalyst. Consumers are proactively managing weight, metabolic health, and immunity through nutrient-dense dietary alternatives. Rising obesity rates and lifestyle disorders are encouraging adoption of calorie-controlled meal replacements enriched with proteins, fiber, vitamins, and antioxidants.

Expansion of Fitness and Sports Nutrition Culture

The global fitness industry, valued at over USD 100 billion, is expanding rapidly. Increased gym memberships, sports participation, and influencer-driven wellness culture are boosting demand for protein-rich, convenient nutrition products. Superfood meal replacement powders are increasingly positioned as post-workout recovery and muscle-building supplements, particularly among millennials and Gen Z consumers.

What are the restraints for the global market?

Premium Pricing and Cost Sensitivity

High-quality superfood ingredients such as spirulina, quinoa, and pea protein contribute to elevated production costs. Price-sensitive consumers in developing economies may hesitate to adopt premium meal replacement powders, limiting broader penetration.

Regulatory and Labeling Compliance

Strict food safety regulations and health claim restrictions in the U.S. and European Union present compliance challenges. Regulatory variations across regions increase product reformulation costs and limit aggressive marketing claims.

What are the key opportunities in the superfood meal replacement powders industry?

Emerging Market Expansion

Asia-Pacific, the Middle East, and Latin America present strong growth potential due to rising disposable income, expanding urban populations, and increasing awareness of plant-based nutrition. Localized flavors, competitive pricing models, and strategic manufacturing partnerships can accelerate penetration in these regions.

Corporate Wellness and Clinical Nutrition Applications

Corporate wellness programs and medical nutrition segments are emerging as promising growth avenues. Employers are promoting employee health initiatives, while hospitals and healthcare institutions are adopting controlled-nutrition meal replacements for diabetic and elderly patients. This diversification broadens revenue streams beyond retail consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8420 Million |

| Market Size in 2026 | USD 9245.16 Million |

| Market Size in 2031 | USD 14754.56 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

The ingredient landscape is increasingly shaped by consumer demand for clean-label, allergen-free, and sustainable nutrition solutions. Plant-based protein blends dominate the market, accounting for approximately 38% of global revenue in 2025. The leading segment driver for plant-based blends is the accelerating global shift toward vegan, flexitarian, and lactose-intolerant dietary preferences, supported by heightened awareness of environmental sustainability and ethical sourcing. Pea protein, brown rice protein, and hemp-based formulations continue to gain traction due to their balanced amino acid profiles, digestibility, and lower carbon footprint compared to animal-derived proteins. In premium product categories, algae-based superfoods such as spirulina and chlorella are gaining traction owing to their dense micronutrient composition, antioxidant properties, and natural detox positioning. Additionally, adaptogen-infused blends incorporating ingredients such as ashwagandha and maca are emerging as niche but high-margin segments, particularly within stress-management, cognitive support, and immunity-focused formulations, reflecting growing consumer interest in functional nutrition beyond basic protein supplementation.

Functional Application Insights

By application, weight management leads the market with nearly 34% share in 2025. The primary driver for this leading segment is the global rise in obesity rates combined with increased consumer engagement in calorie tracking, intermittent fasting, and structured diet programs. Meal replacement powders positioned for portion control, satiety enhancement, and metabolic support are witnessing consistent demand across both developed and emerging economies. Sports nutrition remains a strong secondary segment, supported by expanding gym memberships, performance-focused lifestyles, and rising participation in amateur fitness activities. Demand is particularly pronounced among gym-goers, endurance athletes, and strength-training consumers seeking convenient post-workout recovery solutions. Meanwhile, general wellness and detox-focused blends are expanding steadily as consumers prioritize immunity enhancement, gut health, and holistic well-being. Products enriched with probiotics, digestive enzymes, and antioxidant complexes are gaining relevance in daily nutrition routines.

Distribution Channel Insights

Online retail leads distribution with around 41% market share in 2025, driven by the convenience of doorstep delivery, competitive pricing transparency, and subscription-based replenishment models that improve customer retention. The leading driver for this channel is the rapid digitalization of consumer purchasing behavior, supported by influencer marketing, personalized nutrition recommendations, and direct brand engagement through social commerce platforms. Specialty health stores maintain strong performance in developed economies where consumers seek expert guidance and curated premium product selections. Supermarkets and pharmacies continue to generate substantial offline sales due to high foot traffic and product accessibility, particularly in urban and suburban markets. Direct-to-consumer platforms are gaining importance in metropolitan areas, enabling brands to collect first-party data, tailor formulations, and enhance customer loyalty through customized offerings.

End-Use Insights

Individual consumers account for approximately 68% of global demand, reflecting predominantly retail-driven growth. The leading driver for this segment is the increasing preference for convenient, nutritionally balanced meal alternatives among busy professionals, students, and health-conscious households. Rising work-from-home trends and on-the-go consumption patterns further reinforce individual-level adoption. Fitness centers and gyms represent a growing institutional segment aligned with sports nutrition expansion, as facilities increasingly retail branded supplements and incorporate meal replacement products into structured fitness programs. Clinical and healthcare institutions are emerging as a niche yet steadily expanding end-use segment, particularly for medically supervised weight management and nutritional support programs. The broader sports nutrition end-use industry is projected to exceed USD 70 billion globally by 2030, indirectly strengthening demand for high-protein and performance-oriented meal replacement powders.

Explore more data points, trends and opportunities Download Free Sample Report

Superfood Meal Replacement Powders Market Segmentations

By Ingredient Type

- Plant-Based Protein Blends

- Algae & Aquatic Superfoods

- Ancient Grains & Seeds

- Fruit & Vegetable Superfood Blends

- Adaptogen-Infused Blends

By Functional Application

- Weight Management & Calorie Control

- Sports Nutrition & Muscle Recovery

- General Wellness & Nutritional Supplementation

- Clinical & Medical Nutrition

- Detox & Digestive Health

By Distribution Channel

- Online Retail

- Specialty Health & Nutrition Stores

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Direct-to-Consumer Subscription Models

Regional Insights

North America

North America holds approximately 36% of global market share in 2025, with the United States accounting for nearly 80% of regional demand. Regional growth is primarily driven by high vegan and flexitarian adoption rates, advanced e-commerce infrastructure, strong fitness culture, and widespread acceptance of functional nutrition products. The presence of established supplement brands, robust regulatory frameworks, and aggressive product innovation further accelerates market penetration. Canada contributes significantly through rising plant-based dietary adoption, increasing health awareness, and regulatory clarity that supports clean-label product expansion.

Europe

Europe represents around 28% of global demand in 2025. Germany, the United Kingdom, and France lead consumption, supported by stringent clean-label regulations and strong demand for organic and sustainably sourced products. Regional growth is driven by heightened environmental consciousness, government support for plant-based food transitions, and a mature retail ecosystem that prioritizes product transparency. Sustainability, ethical sourcing, and reduced carbon footprint claims significantly influence purchasing decisions, while private-label expansion by major retail chains strengthens accessibility and affordability.

Asia-Pacific

Asia-Pacific accounts for nearly 24% of the global market in 2025 and is the fastest-growing region with a CAGR exceeding 11%. Growth is fueled by rapid urbanization, expanding middle-class income, increasing exposure to Western dietary trends, and rising lifestyle-related health concerns. China and India serve as key growth engines, supported by growing fitness awareness, digital commerce expansion, and a surge in young working professionals seeking convenient nutrition solutions. Australia and Japan represent mature but innovation-driven markets characterized by premium product demand, clean-label expectations, and strong adoption of functional and fortified formulations.

Latin America

Latin America holds about 5% market share, led by Brazil and Mexico. Regional growth is driven by rising gym memberships, expanding urban populations, and increasing awareness of preventive healthcare. Improvements in retail distribution networks and the growing presence of international supplement brands are enhancing product availability. Social media-driven fitness culture and affordability-focused product launches are gradually improving penetration rates across middle-income consumer groups.

Middle East & Africa

The Middle East & Africa region contributes roughly 7% of global revenue, with the UAE and Saudi Arabia leading growth. Market expansion is supported by high disposable income levels, expanding fitness infrastructure, government-backed health initiatives targeting obesity reduction, and strong demand for premium imported nutrition products. Increasing mall-based retail expansion, rising expatriate populations, and the proliferation of boutique fitness studios further stimulate regional demand. In Africa, gradual urbanization and growing middle-class awareness are expected to create long-term growth opportunities.

Key Players in the Superfood Meal Replacement Powders Market

- Herbalife Ltd.

- Nestlé Health Science

- Abbott Laboratories

- Glanbia Plc

- Amway Corp.

- Huel Ltd.

- Orgain Inc.

- Garden of Life LLC

- Soylent Nutrition Inc.

- Danone (Vega)

- RSP Nutrition

- GNC Holdings

- THG Plc (Myprotein)

- Ka’Chava

- Arbonne International