Global Sugar-Free Inclusions Market Size

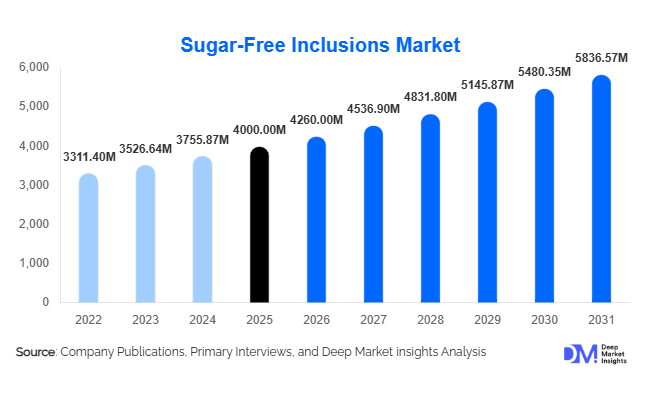

According to Deep Market Insights,the global sugar-free inclusions market size was valued at USD 4,000 million in 2025 and is projected to grow from USD 4,260 million in 2026 to reach USD 5,836.57 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The market growth is primarily driven by increasing consumer health awareness, rising prevalence of diabetes and obesity, growing demand for natural and clean-label sweeteners, and expanding applications in bakery, confectionery, beverages, and nutraceuticals.

Key Market Insights

- Natural sweetener-based inclusions, including Stevia and monk fruit, are dominating the market, favored by consumers seeking clean-label and non-GMO alternatives.

- Powdered sugar-free inclusions are leading in form segment, due to their versatility in bakery, beverages, and confectionery formulations.

- Confectionery remains the largest application segment, driven by chocolate, candy, and gummies manufacturers adopting sugar-free solutions.

- Supermarkets and hypermarkets continue to dominate distribution, although online retail is rapidly emerging as a key channel, especially in Asia-Pacific.

- North America leads globally, accounting for ~30% of the market in 2025, followed closely by Europe with ~28% market share.

- Asia-Pacific is the fastest-growing region, fueled by rising urbanization, increasing disposable incomes, and growing health awareness in India, China, and Japan.

What are the latest trends in the sugar-free inclusions market?

Shift Toward Natural Sweeteners and Clean-Label Products

Consumer preference is increasingly shifting toward natural sugar alternatives such as Stevia, monk fruit, and erythritol. Manufacturers are responding by reformulating products to reduce or eliminate artificial sweeteners. Clean-label positioning has become a significant differentiator, particularly in North America and Europe, where consumers demand transparency in ingredients. This trend also supports premium pricing and aligns with broader wellness and sustainability trends in the food and beverage industry.

Integration in Functional Foods and Nutraceuticals

Sugar-free inclusions are being increasingly integrated into functional foods and nutraceutical products, including protein bars, powdered supplements, and functional beverages. These products cater to health-conscious consumers seeking preventive nutrition and reduced-calorie options. Fiber-based inclusions such as inulin and polydextrose are gaining prominence due to their dual role in sweetness reduction and digestive health benefits, further driving market adoption.

Technological Advances in Formulation

Emerging formulation technologies, including encapsulation and taste-modifying techniques, are enabling manufacturers to maintain flavor and texture in sugar-reduced products. Innovations in blending sweeteners with fibers, stabilizers, and functional ingredients improve product performance and shelf life. These advancements also support scalability for industrial applications, enhancing the competitiveness of sugar-free inclusions in global markets.

What are the key drivers in the sugar-free inclusions market?

Rising Health and Wellness Awareness

The growing prevalence of diabetes, obesity, and lifestyle-related health conditions is driving the adoption of sugar-free inclusions. Consumers are increasingly seeking low-calorie alternatives in confectionery, bakery, beverages, and dairy products. Health-focused regulations and sugar-reduction initiatives are further accelerating adoption across North America, Europe, and emerging Asia-Pacific markets.

Innovation in Natural Sweeteners

Natural sweeteners such as Stevia, monk fruit, and erythritol are gaining traction due to their clean-label appeal and non-GMO status. Manufacturers are investing in R&D to improve taste profiles, solubility, and heat stability, enabling broader application in chocolate, baked goods, beverages, and dietary supplements. This innovation is a major driver for consumer acceptance and market growth.

Expansion in Confectionery and Beverage Applications

Confectionery and beverages remain key end-use industries, driving demand for sugar-free inclusions. Increasing consumer preference for healthier indulgences, combined with product innovations such as sugar-free chocolates, gummies, soft drinks, and functional beverages, is expanding the addressable market. Companies introducing diverse flavor variants and functional benefits are attracting premium consumers globally.

What are the restraints for the global market?

High Production Costs

Sugar-free inclusions, particularly natural sweeteners, involve complex extraction, purification, and formulation processes, resulting in higher production costs. These costs may limit penetration in price-sensitive markets and challenge mass adoption in emerging economies. Manufacturers must balance product pricing with consumer affordability to sustain growth.

Taste and Sensory Limitations

Some sugar substitutes can impart off-tastes or negatively impact texture in end products. Achieving an optimal balance between sweetness, mouthfeel, and product stability remains a key challenge, which can slow market adoption in certain segments, especially in confectionery and beverages.

What are the key opportunities in the sugar-free inclusions market?

Expansion in Emerging Economies

Asia-Pacific and Latin America present significant growth opportunities due to increasing urbanization, rising disposable income, and growing awareness of health and wellness. Countries such as India, China, Brazil, and Mexico are seeing heightened demand for sugar-free bakery, beverage, and confectionery products. Market entrants focusing on local preferences and affordable formulations can capture substantial market share.

Technological Innovation in Formulations

Advances in encapsulation, taste-masking, and blending technologies are enabling manufacturers to deliver sugar-free inclusions with improved taste, stability, and functional benefits. Companies investing in R&D to enhance product quality and scalability are well-positioned to differentiate themselves in competitive markets. Innovative applications in nutraceuticals, protein bars, and functional beverages further expand the market’s growth potential.

Regulatory Support and Health-Focused Policies

Governments worldwide are promoting sugar reduction initiatives, nutritional labeling, and taxation policies that encourage healthier consumption. Such regulations create a favorable environment for sugar-free inclusions and incentivize manufacturers to innovate. Public-private collaborations supporting health-focused initiatives further expand market opportunities, particularly in North America and Europe.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4000 Million |

| Market Size in 2026 | USD 4260 Million |

| Market Size in 2031 | USD 5836.57 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural sweetener-based inclusions dominate the global market, accounting for approximately 38% of total revenue share in 2025, primarily driven by increasing consumer demand for clean-label, plant-derived, and low-calorie alternatives to conventional sugar-based ingredients. The shift toward healthier indulgence, rising obesity concerns, and regulatory pressure on sugar reduction are accelerating the adoption of natural sweeteners across food and beverage formulations. Powdered formats hold the largest share of nearly 45%, supported by their superior stability, longer shelf life, ease of transportation, and seamless integration into bakery, confectionery, beverage, dairy, and nutraceutical applications. Powdered inclusions also enable precise dosage control, consistent sweetness distribution, and cost-efficient bulk handling, making them highly preferred among manufacturers. Fiber-based inclusions such as inulin and polydextrose are witnessing rapid growth due to their dual functional benefits of sugar reduction and digestive health enhancement. These ingredients provide bulk, mouthfeel, and prebiotic functionality, enabling formulators to develop reduced-sugar and high-fiber products without compromising taste or texture. Continuous innovation in formulation technologies and blending solutions further strengthens product diversification across segments.

Application Insights

Confectionery remains the leading application segment, capturing approximately 32% of market share in 2025, supported by rising demand for sugar-free chocolates, gummies, candies, and functional sweets. The leading segment driver is the increasing consumer preference for guilt-free indulgence combined with improved taste-masking technologies that enhance product appeal. Beverage applications, including carbonated soft drinks, flavored water, energy drinks, and ready-to-drink functional beverages, are expanding steadily as manufacturers reformulate products to reduce sugar content while maintaining flavor intensity. Bakery applications also contribute significantly, particularly in reduced-calorie cakes, cookies, and snack bars. Functional foods and nutraceutical applications are among the fastest-growing categories, fueled by rising health awareness, preventive healthcare trends, and demand for fortified and digestive-health-supporting products. Product innovation, clean-label positioning, and advancements in flavor modulation technologies are collectively shaping the evolving application landscape.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 50% of the global distribution share, benefiting from extensive retail networks, strong consumer trust, wide product assortments, and promotional visibility. The dominance of organized retail is further supported by impulse purchases and expanding shelf space for healthier alternatives. Online retail is emerging as a high-growth channel, particularly across Asia-Pacific, driven by increasing digital penetration, convenience-oriented purchasing behavior, subscription-based health product models, and targeted marketing toward health-conscious consumers. E-commerce platforms enable direct-to-consumer strategies, broader geographic reach, and data-driven personalization. Specialty health stores and food service channels complement mainstream retail by catering to niche dietary needs, premium product positioning, and customized formulations for commercial food manufacturers.

End-Use Insights

Confectionery and beverage industries represent the fastest-growing end-use segments, supported by large-scale reformulation initiatives aimed at reducing sugar content while preserving sensory attributes. The leading growth driver across end-use industries is the global shift toward reduced-calorie, functional, and clean-label product portfolios. Nutraceuticals and dairy applications are increasingly incorporating sugar-free inclusions to enhance functional benefits, particularly in probiotic yogurts, flavored milk, protein supplements, and fortified beverages. Export-driven demand from developed regions such as North America and Europe to emerging Asia-Pacific and Latin American markets is further supporting global expansion. End-use industries are projected to grow at a compound annual growth rate of 5–7%, reflecting sustained innovation, regulatory compliance requirements, and growing consumer preference for health-oriented formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar-Free Inclusions Market Segmentations

By Type

- Natural Sweetener-Based Inclusions

- Artificial Sweetener-Based Inclusions

- Fiber-Based Inclusions

By Form

- Powder

- Granules

- Liquid

- Tablets/Compressed Form

By Application

- Confectionery

- Bakery & Snacks

- Dairy & Frozen Desserts

- Beverages

- Nutraceuticals & Dietary Supplements

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Food Service & Institutional

Regional Insights

North America

North America leads the global market with approximately 30% revenue share in 2025, driven primarily by the strong presence of health-conscious consumers, advanced food processing infrastructure, and proactive sugar-reduction policies. The United States and Canada are at the forefront of innovation in clean-label and functional formulations, supported by regulatory frameworks that encourage transparent labeling and nutritional reformulation. High prevalence of obesity and diabetes has accelerated the shift toward low-calorie and fiber-enriched alternatives. Robust demand from confectionery, bakery, and functional beverage manufacturers, combined with significant R&D investments and strong retail penetration, continues to reinforce regional dominance.

Europe

Europe accounts for approximately 28% of the global market, with Germany, the United Kingdom, and France serving as major contributors. Regional growth is primarily driven by stringent sugar taxation policies, government-led reformulation initiatives, and widespread consumer awareness regarding health and wellness. Clean-label preferences and the rapid expansion of functional and organic food categories are further supporting market expansion. The United Kingdom represents one of the fastest-growing European markets, registering around 7% CAGR, largely due to progressive public health campaigns and strong retailer commitment to sugar reduction. Innovation in plant-based and fiber-enriched formulations is also enhancing regional competitiveness.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at an estimated CAGR of approximately 8%, led by China, India, Japan, and Australia. Rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing awareness of lifestyle-related diseases are key growth drivers. The region is witnessing significant growth in mid-range and functional food applications, particularly in urban centers. Government initiatives promoting healthier diets, expanding modern retail infrastructure, and rapid growth in e-commerce platforms are accelerating product accessibility. Additionally, the growing domestic manufacturing base and rising demand for innovative, affordable sugar-reduced products are strengthening regional momentum.

Latin America

Latin America, led by Brazil, Argentina, and Mexico, is experiencing steady growth driven by increasing awareness of diabetes and metabolic health concerns. Government initiatives focused on nutritional labeling and sugar reduction policies are encouraging product reformulation across food and beverage categories. Confectionery and beverage segments dominate regional demand, supported by strong consumer preference for flavored drinks and sweets. Expanding retail modernization, rising urban populations, and increasing penetration of international food brands are further supporting market development across the region.

Middle East & Africa

The Middle East and Africa region represents an emerging growth opportunity, supported by rising disposable incomes, expanding urban populations, and increasing demand for premium and functional food products. The United Arab Emirates and Saudi Arabia lead the Middle Eastern market due to high-income expatriate populations and strong retail infrastructure. Africa is increasingly positioning itself as a production and sourcing hub for certain raw materials, facilitating regional supply chain integration. Intra-regional trade agreements, growing health awareness campaigns, and expanding modern retail networks are collectively driving gradual but steady market growth across the region.

Top 15 Global Players in Sugar-Free Inclusions Market

- Cargill, Inc.

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- ADM (Archer Daniels Midland Company)

- Glencore Nutrition

- Beneo GmbH

- Sweeteners Plus, Inc.

- Stevia Corp

- CP Kelco

- Frutarom Industries Ltd.

- Kerry Group PLC

- DSM Food Specialties

- Ajinomoto Co., Inc.

- Balchem Corporation