Global Sugar-Free Chocolate Market Size

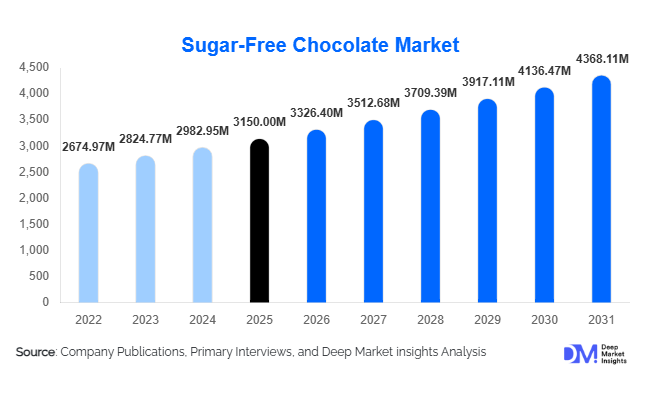

According to Deep Market Insights,the global sugar-free chocolate market size was valued at USD 3,150 million in 2025 and is projected to grow from USD 3,326.40 million in 2026 to reach USD 4,368.11 million by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing health-conscious consumer behavior, rising diabetic populations, and growing demand for guilt-free indulgence options that combine taste with reduced sugar intake.

Key Market Insights

- Health-driven consumer demand is accelerating, particularly among individuals seeking low-calorie, diabetic-friendly, and keto-compliant chocolate alternatives.

- Dark and specialty sugar-free chocolate flavors are gaining popularity, driven by antioxidant benefits and superior taste profiles compared to conventional sugar-free variants.

- North America dominates the market with high penetration of sugar-free products and robust retail infrastructure.

- Europe remains a leading growth region, supported by clean-label trends, regulatory compliance, and premium confectionery culture.

- Asia-Pacific is emerging as the fastest-growing market, led by rising middle-class incomes in China, India, and Southeast Asia.

- Technological adoption, including advanced sweetener formulations and e-commerce distribution, is enhancing product accessibility and consumer engagement.

What are the latest trends in the sugar-free chocolate market?

Functional and Health-Enhanced Chocolates

Manufacturers are increasingly launching sugar-free chocolates enriched with functional ingredients such as proteins, probiotics, and plant-based nutrients. These products cater to consumers seeking metabolic health benefits, weight management support, or keto-friendly indulgences. Innovations in sweetener technology and flavor masking have minimized aftertaste, enabling sugar-free products to closely mimic traditional chocolates. Functional chocolates are also being positioned as premium products, supporting higher price points and brand differentiation in competitive markets.

Expansion of Digital and Direct-to-Consumer Channels

E-commerce platforms and direct-to-consumer models are reshaping market access for sugar-free chocolates. Online channels provide convenience, access to niche flavors, and personalized offerings. Subscription models and limited-edition flavor launches are helping brands engage health-conscious consumers effectively. Data-driven insights from digital platforms also allow companies to optimize product positioning, anticipate demand trends, and tailor marketing campaigns to specific demographics, particularly millennials and Gen Z consumers.

What are the key drivers in the sugar-free chocolate market?

Rising Health Awareness and Lifestyle Changes

Global consumers are increasingly conscious of sugar’s negative health impacts, including obesity, diabetes, and dental issues. Sugar-free chocolates offer an alternative that allows indulgence without excessive sugar intake. This trend spans age groups, particularly in developed markets with higher disposable income and wellness orientation.

Growing Diabetic and Diet-Conscious Population

The rising prevalence of diabetes worldwide is driving demand for sugar-free chocolate products that provide safe indulgence options. Dietary recommendations increasingly encourage sugar-free alternatives, creating a substantial market among diabetic and pre-diabetic consumers.

Sweetener and Flavor Innovations

Advances in natural sweeteners like stevia, erythritol, and monk fruit, along with flavor optimization technologies, have improved taste, texture, and consumer acceptance. This innovation has helped overcome traditional taste barriers, boosting repeat purchases and wider market adoption.

What are the restraints for the global market?

Higher Production Costs

Premium sweeteners and complex formulations increase production costs compared to sugar-based chocolates. These higher costs are often reflected in retail pricing, which can limit adoption in price-sensitive markets and emerging economies.

Consumer Taste Perception

Despite improvements, some consumers still perceive sugar-free chocolates as less flavorful or with an aftertaste compared to conventional variants. Overcoming this challenge requires ongoing R&D, which can be resource-intensive for smaller manufacturers.

What are the key opportunities in the sugar-free chocolate market?

Functional and Specialty Product Innovation

Opportunities exist in creating sugar-free chocolates with added health benefits, such as protein enrichment, probiotics, and plant-based nutrients. Functional innovation allows brands to differentiate products, command premium pricing, and appeal to consumers seeking metabolic health, weight management, or lifestyle-specific solutions.

Emerging Market Expansion

Asia-Pacific, Latin America, and parts of the Middle East are high-growth regions due to rising disposable incomes, urbanization, and increasing health awareness. Localized flavor profiles, culturally relevant marketing, and partnerships with distributors can accelerate market penetration in these regions.

Integration of Digital and E-Commerce Channels

Digital commerce provides scalable access to niche consumer segments, personalized products, and subscription models. Social media marketing, data-driven campaigns, and direct-to-consumer sales enhance brand reach and consumer engagement, particularly among tech-savvy and health-conscious younger audiences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3150 Million |

| Market Size in 2026 | USD 3326.40 Million |

| Market Size in 2031 | USD 4368.11 Million |

| CAGR | 5.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global sugar-free chocolate market is primarily led by the 100% sugar-free chocolate segment, which accounts for approximately 58% of total market share in 2025. The dominance of this segment is driven by the rising prevalence of diabetes, growing adoption of ketogenic and low-carb diets, and increasing consumer preference for clean-label, zero-sugar formulations. Manufacturers are leveraging alternative sweeteners such as stevia, erythritol, and monk fruit to replicate the taste and texture of traditional chocolate without compromising on flavor, thereby strengthening consumer acceptance. The premium positioning of 100% sugar-free chocolate further enhances its appeal among health-conscious and affluent consumers seeking guilt-free indulgence. Meanwhile, no-added-sugar chocolate and sugar-free flavored ingredients complement overall market expansion by targeting flexitarian and calorie-conscious buyers. Sugar-free confectionery formats, including bars, filled chocolates, chips, and baking inclusions, are expanding across both retail and B2B applications, particularly within bakery, dairy, and dessert manufacturing industries, thereby reinforcing volume growth across multiple value chain layers.

Flavor Insights

Dark sugar-free chocolate remains the leading flavor segment, accounting for nearly 60% of the total flavor category in 2025. Its higher cocoa concentration, natural antioxidant properties, and compatibility with plant-based and alternative sweeteners make it highly attractive among health-focused consumers. The perceived functional benefits of dark chocolate, including heart-health support and lower sugar perception, further drive segment leadership. Additionally, dark variants align well with premium and artisanal positioning strategies adopted by manufacturers. Milk and white sugar-free chocolate flavors follow, supported by mainstream consumer preference for creamy textures and familiar taste profiles. Specialty flavors such as mint, coffee, caramel, sea salt, and nut-based variants are witnessing increasing traction as brands focus on flavor innovation, limited-edition launches, and seasonal offerings to enhance differentiation and consumer engagement.

Distribution Channel Insights

Store-based retail channels dominate the sugar-free chocolate market, contributing approximately 72% of total sales in 2025. Supermarkets, hypermarkets, specialty health stores, and pharmacy chains provide extensive shelf visibility, impulse purchase opportunities, and product variety that support sustained demand. The strong retail infrastructure in developed markets, combined with in-store promotional campaigns and private-label expansion, continues to reinforce this segment’s leadership. However, non-store distribution channels, particularly e-commerce and direct-to-consumer (DTC) platforms, are witnessing accelerated growth. Online platforms offer convenience, subscription models, broader product assortments, and access to niche and premium sugar-free brands. Younger demographics and digitally savvy consumers increasingly rely on online channels for functional and specialty chocolate purchases, making digital commerce a critical driver of long-term market scalability.

End-Use Insights

The primary end users of sugar-free chocolate include health-conscious consumers, diabetic individuals, lifestyle diet followers, and mainstream indulgence buyers seeking reduced-sugar alternatives. The fastest-growing demand originates from health-focused and diet-conscious segments, driven by increased awareness of sugar-related health risks, obesity management efforts, and preventive healthcare trends. Additionally, the foodservice and bakery industries are progressively incorporating sugar-free chocolate into cakes, pastries, desserts, beverages, and confectionery items to cater to evolving consumer preferences for low-sugar menu options. Export-driven demand is also strengthening, particularly toward regions with high diabetes prevalence and strong wellness-oriented consumption patterns, supporting cross-border trade and global brand expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar-Free Chocolate Market Segmentations

By Product Type

- 100% Sugar-Free Chocolate

- No-Added-Sugar Chocolate

- Sugar-Free Filled Chocolates

- Sugar-Free Chocolate Chips & Baking Ingredients

By Flavor

- Dark Sugar-Free Chocolate

- Milk Sugar-Free Chocolate

- White Sugar-Free Chocolate

- Specialty Flavors (Mint, Coffee, Nuts)

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty & Health Stores

- Online Retail / E-commerce

- Direct-to-Consumer / Brand Websites

By End-Use

- Retail Consumers / Health-Conscious Individuals

- Foodservice & Bakeries

- Export & International Trade

Regional Insights

North America

North America represents the largest regional market, accounting for approximately 38–40% of global share in 2025. The United States leads regional demand due to high health awareness, widespread prevalence of diabetes and obesity, and strong adoption of low-carb and keto diets. Well-established retail infrastructure, advanced product innovation capabilities, and strong brand presence further support market maturity. The expansion of functional foods, premium chocolate brands, and private-label offerings also contributes to sustained growth. In Canada, similar health-driven consumption patterns, premium product acceptance, and regulatory support for sugar reduction initiatives strengthen regional demand. The rapid growth of e-commerce, subscription snack services, and specialty health channels continues to enhance accessibility and product penetration across both countries.

Europe

Europe holds approximately 35–38% market share in 2025, driven by strong chocolate consumption culture and high acceptance of clean-label and reduced-sugar products. Germany, the United Kingdom, and France lead regional demand due to established premium chocolate industries and rising consumer focus on health and sustainability. Regulatory emphasis on sugar reduction and nutritional transparency further accelerates sugar-free product adoption. Additionally, European consumers demonstrate strong preference for high-cocoa dark chocolate, which aligns well with sugar-free formulations. Growth is also supported by innovation in organic, vegan, and ethically sourced chocolate products, positioning Europe as a key innovation hub within the global market.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, supported by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing awareness of lifestyle-related diseases. Countries such as China, India, Japan, and Southeast Asian nations are witnessing a steady shift toward healthier snacking options. The growing prevalence of diabetes in the region serves as a significant driver for sugar-free product adoption. Digital commerce platforms, social media marketing, influencer engagement, and cross-border e-commerce channels significantly enhance product visibility and accessibility. Furthermore, Western dietary influence and premiumization trends are encouraging greater experimentation with sugar-free and functional chocolate products across urban centers.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, represents an emerging growth market characterized by gradual but steady adoption of sugar-free chocolate. Rising health awareness, urbanization, and increasing exposure to global dietary trends through travel and digital platforms contribute to market expansion. The growing middle-class population and premium product interest among affluent consumers are supporting demand for specialty and imported sugar-free offerings. Additionally, improvements in modern retail infrastructure and supermarket penetration across major cities are enhancing product availability and brand visibility.

Middle East & Africa

The Middle East demonstrates promising growth potential, particularly in the UAE, Saudi Arabia, and Qatar, where high-income populations, luxury consumption patterns, and rising diabetes prevalence drive demand for premium sugar-free chocolate products. The region’s strong gifting culture and preference for high-end confectionery further support premium segment expansion. In Africa, while still at a nascent consumption stage, urbanization, improving retail infrastructure, and rising health awareness are gradually fostering intra-regional demand. Moreover, Africa’s position as a major cocoa-producing region supports upstream integration opportunities and specialty chocolate manufacturing growth within select urban markets.

Top Players in the Global Sugar-Free Chocolate Market

- The Hershey Company

- Lindt & Sprüngli AG

- Ferrero Group

- Mondelez International

- Mars, Incorporated

- Barry Callebaut AG

- Ghirardelli Chocolate Company

- Nestlé S.A.

- Russell Stover Chocolates

- Valrhona

- Hu Master Holdings

- Theo Chocolate

- Lotte Group

- Meiji Co., Ltd.

- Breyers / Unilever