Sugar Confectionery Market Size

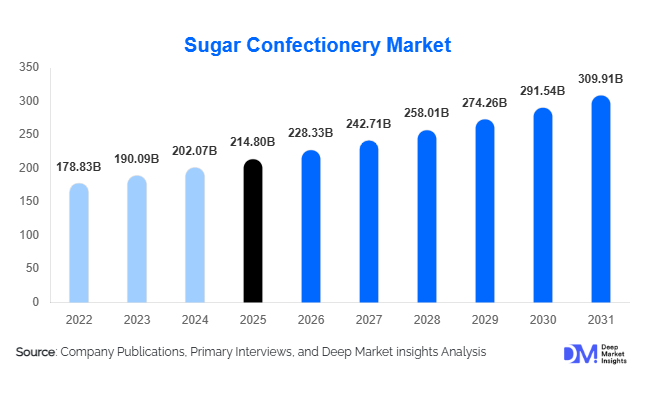

According to Deep Market Insights, the global sugar confectionery market size was valued at USD 214.8 billion in 2025 and is projected to grow from USD 228.33 billion in 2026 to reach USD 309.91 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The sugar confectionery market growth is primarily driven by increasing consumer demand for impulse snacking, premium candy innovations, expanding retail penetration, and rising popularity of functional and sugar-free confectionery products across both developed and emerging economies.

Key Market Insights

- Gummies and jellies dominate the product landscape, supported by rising popularity among younger consumers and increasing demand for functional confectionery products.

- Sugar-free and clean-label confectionery is witnessing rapid adoption, particularly in North America and Europe due to rising health consciousness and sugar reduction initiatives.

- Asia-Pacific dominates the global market, led by China, India, Japan, and Southeast Asia due to population growth and rising disposable income.

- Online retail and quick-commerce channels are transforming confectionery distribution, enabling direct-to-consumer expansion and faster product accessibility.

- Premiumization trends are accelerating globally, with consumers increasingly preferring artisanal, gourmet, and imported confectionery products.

- Sustainable packaging and ingredient transparency are becoming central purchasing criteria for environmentally conscious consumers.

Sugar Confectionery Market Trends

Functional and Wellness Confectionery Expanding Rapidly

Functional confectionery products are emerging as one of the most transformative trends within the sugar confectionery market. Manufacturers are increasingly launching gummies and candies infused with vitamins, minerals, probiotics, collagen, immunity-support ingredients, and botanical extracts to appeal to health-conscious consumers. Functional gummies targeting sleep enhancement, digestive wellness, beauty nutrition, and energy support are witnessing strong demand across North America, Europe, and Asia-Pacific. The convergence between nutraceuticals and confectionery is creating new product categories with higher profit margins and stronger consumer retention. Manufacturers are also adopting natural sweeteners such as stevia and monk fruit to reduce sugar content while maintaining flavor quality and texture consistency.

Premium and Artisanal Candy Innovations

Premiumization is significantly reshaping the global sugar confectionery industry. Consumers are increasingly seeking gourmet confectionery products featuring exotic flavors, imported ingredients, luxury packaging, and limited-edition seasonal offerings. Premium fruit flavors, sour candy innovations, and handcrafted confectionery products are gaining popularity among millennial and Gen Z consumers. Artisanal confectionery brands are leveraging storytelling, sustainable sourcing, and clean-label positioning to differentiate themselves in competitive retail environments. Seasonal gifting trends, especially during holidays and festivals, are further driving premium confectionery sales globally. Manufacturers are also investing in sustainable packaging materials and visually appealing branding to strengthen premium product positioning across retail shelves and e-commerce channels.

Sugar Confectionery Market Drivers

Growing Demand for Convenience Snacking

The increasing global preference for convenient and portable snack products remains a major driver for the sugar confectionery market. Urban consumers with fast-paced lifestyles are increasingly opting for affordable impulse snacks that can be consumed instantly without preparation. Candies, gummies, mints, and chewing confectionery products continue to benefit from their portability, long shelf life, and broad flavor variety. Convenience stores, supermarkets, vending channels, and quick-commerce platforms are further strengthening accessibility and driving frequent purchases. Younger demographics and working professionals represent key consumer groups fueling daily confectionery consumption globally.

Expansion of Organized Retail and E-Commerce

The rapid growth of organized retail infrastructure and online grocery channels is significantly supporting sugar confectionery market expansion. Supermarkets and hypermarkets continue to dominate retail sales through product visibility, promotional campaigns, and bundled offerings. Meanwhile, e-commerce platforms and direct-to-consumer models are enabling confectionery brands to reach wider consumer bases without extensive offline investments. Social commerce, influencer marketing, and digital product launches are becoming increasingly important in driving engagement with younger consumers. Online channels are particularly beneficial for premium and niche confectionery brands seeking to scale internationally through targeted digital marketing strategies.

Sugar Confectionery Market Restraints

Increasing Regulatory Pressure on Sugar Consumption

One of the major restraints impacting the sugar confectionery market is rising global regulatory scrutiny regarding sugar intake and obesity-related health concerns. Governments across Europe, North America, and parts of Asia are introducing sugar taxes, stricter labeling standards, and marketing restrictions aimed at reducing excessive sugar consumption. These regulations are forcing manufacturers to invest heavily in reformulation strategies, low-sugar alternatives, and compliance initiatives. Advertising restrictions targeting children are also limiting promotional flexibility for traditional confectionery products.

Volatility in Raw Material Prices

Fluctuating prices of sugar, gelatin, dairy ingredients, flavoring agents, and packaging materials continue to create operational challenges for confectionery manufacturers. Supply chain disruptions, climate-related agricultural uncertainty, and geopolitical instability have contributed to raw material inflation over recent years. Rising logistics costs and energy prices are further pressuring manufacturer profit margins, especially in highly competitive and price-sensitive developing markets. Small and mid-sized confectionery companies are particularly vulnerable to sustained input cost volatility.

Sugar Confectionery Market Opportunities

Sugar-Free and Clean-Label Product Development

The growing demand for healthier indulgence products presents substantial opportunities for confectionery manufacturers globally. Consumers are increasingly seeking reduced-sugar, vegan, plant-based, and naturally flavored confectionery alternatives that align with evolving dietary preferences. Clean-label confectionery products made without artificial preservatives, synthetic colors, or high-fructose corn syrup are gaining strong traction in premium retail channels. Manufacturers investing in sugar substitutes, natural ingredient technologies, and transparent labeling practices are expected to gain competitive advantages in the coming years.

Expansion Across Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East offer major long-term growth opportunities for sugar confectionery manufacturers. Rising disposable income, urbanization, modern retail expansion, and increasing youth populations are driving higher confectionery consumption across countries such as India, Indonesia, Vietnam, Brazil, and Saudi Arabia. International brands are increasingly localizing manufacturing operations and adapting flavor profiles to regional tastes in order to strengthen market penetration. Growing demand for imported confectionery products and premium gifting assortments is also creating strong revenue opportunities within these high-growth markets.

Product Type Insights

Gummies and jellies dominate the global sugar confectionery market, accounting for approximately 28.4% of total market revenue in 2025. Their popularity is driven by texture innovation, broad flavor variety, and increasing adoption of functional ingredients such as vitamins and collagen. Hard-boiled candies continue to maintain strong demand due to affordability and high penetration in emerging markets, particularly across Asia-Pacific and Latin America. Toffees and caramels remain popular among traditional consumers, while premium and artisanal variants are expanding in Europe and North America. Sugar-free confectionery represents the fastest-growing segment as consumers increasingly seek healthier alternatives with reduced calorie intake. Seasonal and novelty confectionery products also contribute significantly to annual revenues, especially during holidays, festivals, and gifting seasons.

Ingredient Type Insights

Sugar-based confectionery remains the leading ingredient category with nearly 63% market share due to cost efficiency, taste familiarity, and large-scale production capabilities. However, natural sweetener-based confectionery is witnessing rapid expansion as manufacturers increasingly incorporate stevia, monk fruit, erythritol, and plant-derived sweeteners into product formulations. Functional ingredient integration is also accelerating, with manufacturers adding probiotics, vitamins, and immunity-support compounds into gummies and chewy candies. Organic and clean-label confectionery products are gaining traction among premium consumers seeking transparency and minimal ingredient processing.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the sugar confectionery market distribution landscape with approximately 39% market share due to extensive product visibility, promotional campaigns, and impulse purchasing behavior. Convenience stores continue to play a major role in driving daily confectionery consumption through strategic checkout placements and on-the-go accessibility. Online retail channels are experiencing the fastest growth, supported by rising smartphone penetration, digital grocery adoption, and direct-to-consumer business models. Specialty candy stores and gourmet confectionery boutiques are also benefiting from premiumization trends, particularly in urban markets where consumers increasingly seek imported and artisanal confectionery products.

Consumer Group Insights

Children remain the largest consumer segment within the sugar confectionery market, accounting for nearly 34% of global demand in 2025. Character-themed packaging, novelty candy formats, and fruit-flavored products continue to drive strong consumption among younger demographics. Teenagers and young adults are major consumers of sour candies, gummies, and social-media-driven confectionery trends. Adult consumers increasingly prefer premium, sugar-free, and functional confectionery products aligned with wellness and indulgence preferences. Geriatric consumers are gradually contributing to demand for softer confectionery formats and reduced-sugar variants designed for easier consumption and healthier lifestyles.

Packaging Type Insights

Flexible pouches lead the packaging segment with approximately 31% market share due to cost efficiency, portability, lightweight logistics, and strong shelf appeal. Multipack packaging formats are gaining popularity among families and value-oriented consumers seeking bulk purchases. Sustainable and recyclable packaging solutions are increasingly becoming strategic priorities for confectionery manufacturers responding to retailer sustainability mandates and environmental regulations. Premium packaging innovations featuring resealable designs, transparent windows, and luxury gift-oriented presentation are also supporting higher-value confectionery sales globally.

| By Product Type | By Ingredient Type | By Flavor Type | By Packaging Type |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for nearly 24.8% of the global sugar confectionery market, led primarily by the United States, which contributes more than three-fourths of regional demand. Premium gummies, sugar-free candies, and functional confectionery products are witnessing substantial growth across the region. Consumers increasingly prefer clean-label and reduced-sugar formulations, encouraging innovation among manufacturers. Canada is also experiencing growing demand for vegan and organic confectionery products supported by strong health-conscious consumer trends and premium retail expansion.

Europe

Europe represents approximately 22.7% of global market revenue, supported by mature confectionery consumption patterns and strong gifting traditions. Germany, the United Kingdom, France, Italy, and the Netherlands remain key markets due to high retail penetration and advanced confectionery manufacturing capabilities. Germany continues to dominate regional exports, while the United Kingdom leads demand for premium and novelty confectionery products. Regulatory pressure regarding sugar consumption is accelerating demand for low-sugar and naturally sweetened alternatives across European markets.

Asia-Pacific

Asia-Pacific dominates the global sugar confectionery market with around 38.6% share in 2025 and remains the fastest-growing regional market. China and India are the largest contributors due to their massive consumer bases, rapid urbanization, and rising disposable incomes. Japan and South Korea continue to lead innovation in premium, seasonal, and functional confectionery products. Southeast Asian countries including Indonesia, Thailand, and Vietnam are also witnessing strong confectionery consumption growth driven by expanding modern retail infrastructure and increasing youth demographics.

Latin America

Latin America is experiencing stable growth in sugar confectionery demand, particularly across Brazil, Mexico, and Argentina. Affordable candies and impulse confectionery products maintain strong penetration among younger consumers. Economic recovery, retail modernization, and increasing urbanization are supporting market expansion throughout the region. International confectionery brands are also increasing investments in localized production and flavor customization strategies to strengthen competitiveness within Latin American markets.

Middle East & Africa

The Middle East & Africa region is emerging as a promising growth market for sugar confectionery products due to rising youth populations, expanding supermarket infrastructure, and growing demand for imported premium confectionery. Saudi Arabia and the United Arab Emirates represent major regional consumption hubs supported by high disposable incomes and gifting-oriented consumer culture. South Africa remains a leading confectionery manufacturing and distribution center within Africa. Festival-driven demand and rising tourism are further contributing to confectionery sales growth across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Sugar Confectionery Market

- Mars Incorporated

- Mondelez International

- Perfetti Van Melle

- Haribo

- Ferrero Group

- Nestlé

- The Hershey Company

- Meiji Holdings

- Lotte Corporation

- Orkla ASA

- Yıldız Holding

- Cloetta

- August Storck KG

- Katjes International

- Roshen