Sugar Alcohol Market Size

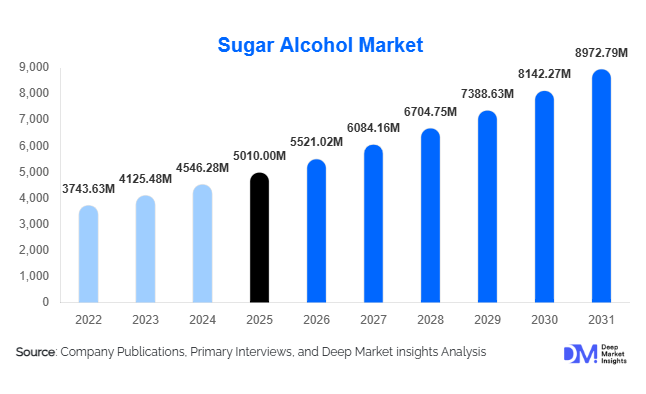

According to Deep Market Insights, the global sugar alcohol market size was valued at USD 5,010 million in 2025 and is projected to grow from USD 5,521.02 million in 2026 to reach USD 8,972.79 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). Market growth is primarily driven by increasing global demand for low-calorie sweeteners, rising prevalence of diabetes and obesity, and accelerating reformulation initiatives across food and beverage manufacturing. Sugar alcohols, also known as polyols, are gaining widespread adoption due to their reduced glycemic impact, tooth-friendly properties, and ability to provide bulk and texture similar to traditional sugar.

Key Market Insights

- Food and beverage manufacturers are accelerating sugar-reduction strategies, positioning sugar alcohols as essential formulation ingredients in low-calorie and functional products.

- Sorbitol remains the dominant product type, supported by cost efficiency and extensive use across confectionery, pharmaceuticals, and oral care applications.

- Asia-Pacific dominates global production and consumption, benefiting from strong starch-processing infrastructure and export-oriented manufacturing.

- Erythritol demand is rising rapidly, fueled by keto, diabetic-friendly, and clean-label product innovation.

- Direct B2B ingredient supply contracts lead distribution, reflecting strong partnerships between polyol producers and multinational food companies.

- Technological advancements in fermentation and hydrogenation processes are improving production efficiency and sustainability performance.

What are the latest trends in the sugar alcohol market?

Shift Toward Functional and Low-Glycemic Nutrition

Consumer dietary preferences are rapidly shifting toward functional foods that support metabolic health. Sugar alcohols are increasingly incorporated into sugar-free confectionery, protein snacks, dietary beverages, and diabetic-friendly foods. Food brands are reformulating legacy products to comply with sugar reduction targets without compromising taste or texture. The growing popularity of ketogenic and low-carb diets has significantly accelerated erythritol and xylitol adoption. Manufacturers are also developing blended sweetener systems combining polyols with natural sweeteners such as stevia to improve sweetness profiles while maintaining calorie reduction claims.

Sustainable and Bio-Based Manufacturing Expansion

Producers are investing in sustainable manufacturing processes to reduce carbon emissions and improve feedstock efficiency. Fermentation-based production using renewable biomass and alternative carbohydrate sources is becoming increasingly common. Sustainability certifications and ESG commitments are influencing procurement decisions by global food companies. Energy-efficient hydrogenation technologies and circular production systems are improving operational margins while aligning with environmental compliance standards. These developments are strengthening the long-term competitiveness of sugar alcohol manufacturers globally.

What are the key drivers in the sugar alcohol market?

Rising Global Health Awareness and Diabetes Prevalence

The increasing global incidence of diabetes and obesity is significantly driving demand for reduced-calorie sweeteners. Sugar alcohols provide sweetness with lower caloric value and slower glucose absorption, making them suitable for diabetic and weight-management diets. Governments and healthcare organizations promoting sugar reduction are indirectly accelerating polyol adoption across processed foods and beverages.

Food Industry Reformulation and Clean-Label Demand

Major food manufacturers are reformulating product portfolios to meet evolving consumer expectations around nutrition transparency and reduced sugar intake. Unlike high-intensity sweeteners, sugar alcohols provide bulk functionality, enabling manufacturers to maintain texture and mouthfeel in bakery and confectionery products. This functional advantage has made polyols indispensable in sugar-replacement strategies globally.

What are the restraints for the global market?

Digestive Tolerance Limitations

Excessive consumption of certain sugar alcohols may cause digestive discomfort, requiring regulatory labeling in several regions. These limitations restrict inclusion levels in some formulations and necessitate balanced product development strategies.

Raw Material and Energy Cost Volatility

Production costs are influenced by fluctuations in corn, wheat, and tapioca feedstock prices as well as energy-intensive hydrogenation processes. Variability in agricultural commodity markets can impact manufacturer profit margins and pricing stability, particularly for smaller producers.

What are the key opportunities in the sugar alcohol industry?

Expansion in Functional Foods and Nutraceutical Applications

The rapid growth of nutraceutical gummies, protein supplements, and dietary products presents significant opportunities for polyol manufacturers. Sugar alcohols enable sugar-free positioning while preserving product texture and stability. As global functional food markets expand, manufacturers capable of delivering high-purity grades are expected to capture premium margins.

Emerging Market Consumption Growth

Urbanization and rising disposable incomes in Asia, Latin America, and the Middle East are driving processed food consumption. Local production investments and regional supply chain development are creating opportunities for both global and regional manufacturers. Governments encouraging domestic food processing industries further strengthen long-term demand potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5010.00 Million |

| Market Size in 2026 | USD 5521.02 Million |

| Market Size in 2031 | USD 8972.79 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Sorbitol continues to dominate the global sugar alcohol market, accounting for nearly 32% of total demand, supported by its broad functionality, cost efficiency, and compatibility across multiple industrial applications. Its widespread use in confectionery, pharmaceuticals, oral care products, and processed foods positions it as the most commercially viable polyol for large-scale manufacturers. The leading driver for sorbitol’s dominance lies in its dual functionality as both a sweetener and humectant, allowing manufacturers to improve texture stability, moisture retention, and shelf life while simultaneously reducing sugar content. Additionally, sorbitol’s relatively low production cost compared to alternative polyols strengthens its adoption in emerging economies where price sensitivity remains high.Xylitol maintains strong positioning, particularly within oral care applications, where its scientifically validated anti-cariogenic properties actively inhibit bacterial growth responsible for tooth decay. Increasing global dental health awareness and the expansion of preventive oral care solutions continue to drive steady consumption across toothpaste, mouthwash, and chewing gum products. Meanwhile, erythritol represents the fastest-growing product segment, largely fueled by rising adoption of keto, diabetic-friendly, and calorie-conscious diets. Its near-zero glycemic impact and clean sweetness profile make it highly attractive for food reformulation initiatives targeting sugar reduction without compromising taste.Maltitol remains extensively utilized in chocolate and bakery applications because it closely replicates sucrose’s sweetness intensity and mouthfeel, enabling manufacturers to produce sugar-free indulgent products with minimal sensory compromise. Growing consumer demand for permissible indulgence and reduced-sugar desserts continues to sustain maltitol usage globally. In parallel, specialty polyols such as isomalt and lactitol are witnessing increasing demand in premium confectionery, nutraceutical formulations, and pharmaceutical excipients. These ingredients support advanced product differentiation strategies as manufacturers develop specialized formulations addressing digestive tolerance, controlled sweetness release, and functional nutrition benefits.

Application Insights

Food and beverage applications dominate the global sugar alcohol market, representing approximately 68% of total demand, primarily driven by the accelerating reformulation of packaged foods toward reduced-sugar and low-calorie alternatives. The leading driver for this segment is the global shift toward healthier dietary patterns combined with regulatory pressure to reduce added sugar consumption. Sugar-free confectionery, baked goods, dairy alternatives, beverages, and functional snacks remain key application categories, with manufacturers increasingly leveraging polyols to achieve sweetness balance while maintaining product texture and stability.Pharmaceutical applications are expanding steadily as sugar alcohols function as essential excipients in syrups, chewable tablets, lozenges, and pediatric formulations. Their non-cariogenic properties, stability, and compatibility with active pharmaceutical ingredients enhance formulation efficiency and patient compliance. Oral care applications continue to generate consistent demand, particularly for xylitol-based chewing gums and toothpaste, as preventive dental care gains importance across both developed and emerging markets.Personal care and cosmetic applications are also gaining traction, as polyols serve as effective humectants, stabilizers, and skin-conditioning agents in skincare and haircare formulations. Increasing demand for multifunctional cosmetic ingredients aligned with clean-label trends further supports this expansion. Industrial applications remain comparatively niche but stable, involving chemical intermediates, resins, and specialty formulations where polyols contribute to moisture regulation and chemical stability.

Distribution Channel Insights

Direct business-to-business (B2B) supply agreements account for nearly 70% of global distribution, reflecting the highly integrated nature of ingredient procurement within the food and pharmaceutical industries. Large multinational food manufacturers typically engage in long-term contracts with polyol producers to ensure price stability, consistent quality, and uninterrupted supply chains. The leading driver for this distribution structure is the need for scalable ingredient sourcing aligned with high-volume production cycles and strict formulation consistency requirements.Ingredient distributors play a critical intermediary role by serving mid-sized food processors, nutraceutical companies, and regional manufacturers that lack direct procurement capabilities. These distributors provide technical support, formulation guidance, and flexible purchasing volumes, enabling broader market penetration of specialty polyols. In recent years, digital ingredient marketplaces have emerged as a rapidly evolving distribution channel. These platforms improve supply transparency, enhance logistics efficiency, and allow smaller manufacturers to access specialized ingredients previously limited to large-scale buyers. The digitalization of ingredient sourcing is expected to gradually reshape procurement dynamics, particularly among small and medium enterprises.

End-Use Industry Insights

The food processing industry represents approximately 64% of total sugar alcohol consumption, supported by continuous innovation in reduced-calorie packaged foods and reformulated consumer staples. The leading driver for this segment is the growing demand for healthier alternatives that maintain taste and texture while complying with sugar reduction targets established by both governments and health organizations. Manufacturers increasingly rely on polyols to develop sugar-free chocolates, bakery products, dairy alternatives, and ready-to-eat snacks that meet evolving consumer expectations.The pharmaceutical industry is experiencing steady expansion as polyols enhance formulation stability and palatability in chewable tablets, syrups, and pediatric medicines. Their low glycemic response and non-cariogenic nature make them particularly suitable for diabetic-friendly medications and long-term therapeutic products. Oral care applications remain highly stable, supported by increasing preventive dental healthcare awareness, expanding middle-class populations, and rising expenditure on personal hygiene products worldwide.Nutraceutical manufacturing is emerging as the fastest-growing end-use segment, driven by strong global demand for sugar-free supplements, protein powders, gummies, and functional nutrition products. Consumers seeking wellness-oriented lifestyles are increasingly prioritizing low-sugar formulations, encouraging manufacturers to incorporate polyols into fortified and performance-based nutrition products. Additionally, export-oriented food manufacturing hubs across Asia are accelerating industrial demand for sugar alcohol ingredients as global brands expand outsourcing and contract manufacturing operations.

Explore more data points, trends and opportunities Download Free Sample Report

Sugar Alcohol Market Segmentations

By Product Type

- Sorbitol

- Xylitol

- Erythritol

- Maltitol

- Isomalt

- Lactitol

- Mannitol

- Others

By Application

- Food Beverages

- Pharmaceuticals

- Oral Care Products

- Personal Care Cosmetics

- Nutraceuticals Dietary Supplements

- Industrial Applications

By Distribution Channel

- Direct B2B Supply Agreements

- Ingredient Distributors Traders

- Online Ingredient Marketplaces

By End-Use Industry

- Food Processing Industry

- Pharmaceutical Manufacturing

- Oral Care Industry

- Nutraceutical Industry

- Personal Care Cosmetic Industry

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 41% of the global sugar alcohol market share and remains the primary production and consumption hub, led by China, India, Japan, and South Korea. China dominates global supply due to its extensive starch processing infrastructure, integrated raw material availability, and strong export-oriented manufacturing ecosystem. The region’s growth is primarily driven by expanding processed food industries, rising urban populations, and increasing adoption of reduced-sugar diets. India is emerging as a high-growth market supported by rapid expansion of packaged food manufacturing, improving healthcare awareness, and increasing diabetic population levels that encourage demand for sugar alternatives. Japan and South Korea contribute significantly through advanced functional food innovation and strong oral care product penetration. Regional growth is further supported by cost-competitive manufacturing, favorable government initiatives promoting food processing industries, and rising investments in nutraceutical production capacity.

North America

North America accounts for nearly 26% of global demand, driven predominantly by the United States, where consumer awareness regarding sugar consumption and metabolic health remains high. Regional growth is strongly supported by widespread adoption of keto-friendly, diabetic, and low-carbohydrate diets, which significantly accelerate erythritol consumption across beverages, snacks, and bakery products. Advanced food reformulation capabilities among major manufacturers enable rapid integration of polyols into mainstream consumer products. Additionally, strong regulatory frameworks encouraging transparent labeling and sugar reduction initiatives motivate companies to adopt alternative sweeteners. High spending on functional nutrition, dietary supplements, and premium oral care products further strengthens sustained market expansion across the region.

Europe

Europe represents approximately 22% of the global market, with Germany, France, and the United Kingdom leading consumption. Regional growth is largely driven by stringent sugar reduction policies, public health campaigns targeting obesity prevention, and regulatory pressure encouraging reformulation of high-sugar food products. European consumers demonstrate strong preference for clean-label and health-oriented ingredients, accelerating adoption of polyols in bakery, confectionery, and dairy alternatives. The region also benefits from advanced pharmaceutical manufacturing capabilities that utilize sugar alcohols as excipients. Innovation in premium confectionery and sugar-free chocolate products continues to create sustained demand, while sustainability-focused production practices encourage manufacturers to adopt efficient polyol processing technologies.

Latin America

Latin America contributes roughly 6% of global market share, led by Brazil and Mexico. Regional growth is supported by expanding processed food manufacturing, increasing urbanization, and rising awareness of lifestyle-related health conditions such as diabetes and obesity. Government-led nutritional labeling initiatives and gradual shifts toward healthier packaged foods are encouraging manufacturers to incorporate reduced-sugar formulations. Growing middle-class populations and increasing penetration of modern retail channels are further enabling wider availability of sugar-free confectionery and beverages, strengthening demand for sugar alcohol ingredients across regional food industries.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global market and represents the fastest-growing regional segment. Growth is driven by rapid urbanization, expanding modern retail infrastructure, and increasing imports of sugar-free and functional consumer products. Countries such as Saudi Arabia and the United Arab Emirates serve as key demand centers due to rising disposable incomes and growing health consciousness among consumers. Increasing prevalence of diabetes across the region is accelerating demand for low-calorie sweeteners in food and beverage applications. Furthermore, expanding hospitality sectors, premium food retail development, and diversification of regional economies toward food processing industries are expected to sustain long-term market growth.

Key Players in the Sugar Alcohol Market

- Cargill Incorporated

- Archer Daniels Midland Company

- Roquette Frères

- Ingredion Incorporated

- Mitsubishi Corporation Life Sciences

- Tereos Group

- Gulshan Polyols Ltd.

- SPI Pharma

- Shandong Futaste Co., Ltd.

- Zhucheng Dongxiao Biotechnology Co., Ltd.

- Baolingbao Biology Co., Ltd.

- Foodchem International Corporation

- Qingdao Bright Moon Seaweed Group

- Sukhjit Starch & Chemicals Ltd.

- B Food Science Co., Ltd.