Stevia Extract Market Size

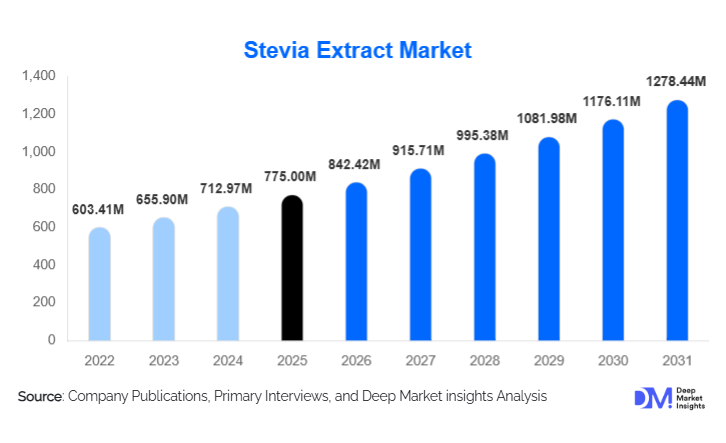

According to Deep Market Insights, the global stevia extract market size was valued at USD 775 million in 2025 and is projected to grow from USD 842.42 million in 2026 to reach USD 1,278.44 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The stevia extract market growth is primarily driven by rising consumer preference for natural, zero-calorie sweeteners, sugar reduction initiatives in the food and beverage industries, and technological advancements in high-purity stevia extraction and formulation.

Key Market Insights

- Health-conscious and clean-label consumption is fueling demand, as consumers prefer natural sweeteners over sugar and artificial alternatives.

- Food & beverage reformulation continues to dominate demand, with beverages, bakery, and dairy products adopting stevia extracts for sugar reduction.

- Asia-Pacific leads global production, particularly in China and India, due to favorable cultivation conditions and cost-efficient extraction.

- North America is a major growth market, driven by sugar reduction regulations, functional beverages, and clean-label initiatives.

- Technological advancements such as enzymatic conversion and precision purification are enhancing taste profiles, enabling adoption in broader applications.

- Emerging end-use applications include nutraceuticals, pharmaceuticals, and personal care products, further expanding market opportunities.

What are the latest trends in the stevia extract market?

Natural Sweeteners Gaining Momentum

Stevia extract is increasingly being recognized as a mainstream sugar alternative due to its zero-calorie profile and natural origin. Food and beverage manufacturers are reformulating products to meet consumer demand for low-sugar and clean-label items. Functional beverages, RTDs, dairy alternatives, and bakery products are increasingly adopting stevia, highlighting a broader shift toward healthier consumption patterns. Regulatory support for sugar reduction in North America, Europe, and Asia reinforces this trend, creating opportunities for both established players and new entrants.

Technological Advancements Enhancing Product Quality

Emerging extraction and purification technologies, such as enzymatic conversion to high-purity Reb M and Reb D, are improving taste and solubility while reducing bitterness. Precision fermentation, liquid concentrates, and powder optimization enhance usability across diverse applications. Manufacturers are also leveraging flavor blending and masking techniques, expanding the range of products that can incorporate stevia without compromising taste. These advancements allow stevia to compete more effectively with artificial sweeteners and appeal to a health-conscious consumer base.

What are the key drivers in the stevia extract market?

Rising Health Awareness and Sugar Reduction Initiatives

Consumers are increasingly prioritizing sugar reduction due to rising obesity, diabetes, and cardiovascular concerns. Stevia extract offers a natural, zero-calorie alternative to sugar, aligning with both regulatory mandates and consumer preferences. Clean-label trends further encourage the replacement of synthetic sweeteners with natural alternatives, solidifying stevia’s role in mainstream products.

Expansion in the Food & Beverage Industry

Beverages, bakery, and dairy products are leading the adoption of stevia extract. Beverage reformulation, including RTDs, carbonated drinks, and functional drinks, drives the majority of demand due to taste compatibility and regulatory pressures. Manufacturers increasingly prioritize stevia as it allows sugar reduction without altering flavor or texture significantly.

Geographical Supply Chain Advantage

Asia-Pacific dominates stevia cultivation and extraction, offering cost-efficient production that fuels global supply. China and India serve as hubs for both bulk supply and high-purity extracts, enabling manufacturers in North America and Europe to access competitive prices and reliable quality, supporting widespread adoption.

What are the restraints for the global market?

Taste Profile Challenges

Lower-purity stevia extracts can exhibit bitterness, limiting their application in sensitive formulations. Manufacturers must invest in blending, purification, and masking technologies to overcome taste issues, adding complexity and cost to production.

High Production Costs

Producing high-purity stevia extracts involves advanced processing and precision purification, which increases costs for smaller manufacturers. Capital-intensive technologies can limit market entry and may restrain growth in price-sensitive regions.

What are the key opportunities in the stevia extract market?

New End-Use Applications

Beyond food and beverages, stevia extract is increasingly adopted in nutraceuticals, dietary supplements, pharmaceuticals, and personal care products. For instance, diabetic-friendly syrups, chewable supplements, and cosmetics are integrating stevia due to its natural, functional properties. Expanding these applications allows players to diversify revenue streams and reduce dependence on traditional segments.

Technological Differentiation

Investment in enzymatic conversion and purification technologies allows the production of high-purity Reb M and Reb D with minimal bitterness. Companies can leverage these innovations to create premium product lines, differentiate offerings, and expand into high-margin applications.

Regional Growth Opportunities

Asia-Pacific offers significant growth potential due to rising consumption, local production capacity, and increasing middle-class demand for low-calorie foods. North America and Europe present opportunities for high-value products in beverages and health-focused formulations, driven by regulatory sugar-reduction mandates and functional beverage trends.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 775 Million |

| Market Size in 2026 | USD 842.42 Million |

| Market Size in 2031 | USD 1278.44 Million |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Reb A continues to dominate the global stevia extract market, accounting for approximately 40% of total market share in 2024. Its leadership is driven by a combination of cost efficiency, favorable taste profile, and wide compatibility with beverages, bakery, and dairy formulations. Manufacturers prefer Reb A for mainstream applications due to its balance of sweetness intensity and minimal aftertaste, making it ideal for large-scale food and beverage production. Meanwhile, high-purity glycosides such as Reb M and Reb D are gaining traction, supported by advanced purification technologies and enzymatic conversion processes that reduce bitterness and improve solubility. The increasing demand for clean-label and sugar-reduced products is further encouraging manufacturers to invest in these premium glycosides, positioning them as emerging growth drivers in niche and high-value applications.

Application Insights

The food and beverage segment leads consumption, representing 60% of the 2024 market. Within this, beverages are the fastest-growing category, driven by rising consumer preference for low-calorie, sugar-reduced soft drinks, RTDs, and functional beverages. Bakery, dairy alternatives, sauces, and dressings are also significant contributors, reflecting broader reformulation trends. Emerging applications in nutraceuticals, dietary supplements, pharmaceuticals, and personal care are accelerating growth, as stevia serves as a functional ingredient providing sweetness, clean-label compliance, and potential health benefits. Functional beverages and diabetic-friendly nutraceuticals are particularly driving uptake in developed markets, while personal care products are integrating stevia for natural formulation claims.

Distribution Channel Insights

Direct bulk industrial contracts account for nearly 50% of market revenue, reflecting the reliance of large food and beverage manufacturers on stable, high-volume supply. Complementary channels include distributors, online ingredient marketplaces, and retail-packaged stevia products, which provide access to small and medium-sized enterprises. Growing digital adoption allows manufacturers to sell directly to niche markets and end-users, supporting targeted marketing and rapid scalability. This distribution diversity ensures both global reach and localized supply, enabling companies to serve traditional F&B sectors and emerging high-value applications effectively.

Explore more data points, trends and opportunities Download Free Sample Report

Stevia Extract Market Segmentations

By Product Type

- Reb A

- Reb M

- Reb D

- Other Steviol Glycosides

- Standard Leaf Extract / Crude Extracts

- Purified Stevia Extract Powder

- Liquid Stevia Extracts / Concentrates

By Application

- Food & Beverages

- Pharmaceuticals

- Dietary Supplements & Nutraceuticals

- Cosmetics & Personal Care

- Others (Pet Food, Feed Additives, Industrial Uses)

By Distribution Channel

- Direct Bulk Industrial Contracts

- Distributors & Ingredient Traders

- Online Ingredient Marketplaces

- Retail Packaged Products

Regional Insights

North America

North America accounts for 25–30% of the global stevia extract market in 2024. Growth is primarily driven by regulatory policies aimed at reducing sugar consumption, clean-label trends, and a surge in functional beverage reformulations. The U.S., as the largest consumer, benefits from extensive product innovation in low-calorie sodas, RTDs, and dietary supplements, while Canada exhibits increasing adoption across beverages and bakery products. Additional drivers include high health awareness among consumers, strong retail penetration, and government-backed sugar reduction initiatives, all of which create favorable conditions for stevia extract adoption.

Europe

Europe contributes 20% of the global market, with Germany, the U.K., and France as leading consumers. Key growth drivers include stringent sugar-reduction regulations, rising health consciousness, and clean-label product adoption. Beverage and bakery industries are reformulating products to meet EU labeling standards, while functional foods and dietary supplements are emerging as high-growth segments. Consumer demand for natural, low-calorie sweeteners and sustainability-focused formulations further strengthens stevia adoption. Additionally, well-established distribution networks and premium product pricing support market expansion across Western and Northern Europe.

Asia-Pacific

Asia-Pacific is both the largest producer (35% of the global market) and a rapidly expanding consumer region. China and India dominate cultivation and extraction due to favorable climatic conditions, cost efficiency, and government support for agricultural and food ingredient production. Growth is fueled by rising middle-class income, increasing awareness of sugar alternatives, and higher prevalence of diabetes and obesity, driving reformulation. Japan and Australia are notable consumption hubs, with premium beverage, bakery, and nutraceutical applications driving demand. Technological investment in extraction and high-purity glycosides enhances product quality, supporting both domestic adoption and exports to North America and Europe.

Latin America

Latin America, including Brazil, Argentina, and Mexico, is gradually increasing stevia adoption in beverages, bakery, and dairy products. Growth is driven by rising health consciousness among affluent consumers, increasing availability of imported high-purity extracts, and sugar reduction initiatives in processed foods. The expanding functional food and beverage sector, along with supportive trade agreements facilitating imports from Asia-Pacific and North America, also contributes to the gradual market expansion. Urbanization and growth in modern retail channels are additional enablers for regional adoption.

Middle East & Africa

Africa serves as a significant production hub for stevia leaves, supplying high-purity extracts for export markets in North America, Europe, and Asia-Pacific. Middle Eastern countries, including the UAE, Saudi Arabia, and Qatar, are emerging consumers due to high disposable income, growing health awareness, and increasing adoption of low-calorie and clean-label products. Drivers include government-backed sugar reduction campaigns, growing retail penetration of natural sweeteners, and strong demand from the hospitality and foodservice sectors. Export-oriented African production combined with local awareness campaigns in the Middle East is enabling robust regional market growth.