Starch Market Size

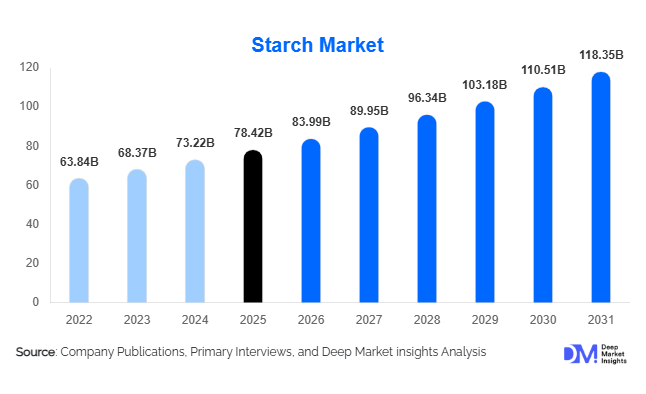

According to Deep Market Insights, the global starch market size was valued at USD 78.42 billion in 2025 and is projected to grow from USD 83.99 billion in 2026 to reach USD 118.35 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The global starch market growth is primarily driven by rising demand from processed food manufacturing, expanding industrial applications including paper and textiles, and increasing adoption of modified starches in pharmaceuticals and biodegradable materials. Growing consumer preference for clean-label and plant-based ingredients, along with the expansion of convenience food consumption in emerging economies, continues to strengthen long-term demand fundamentals across both food and industrial value chains.

Key Market Insights

- Food & beverage applications account for the largest share, supported by processed foods, bakery, dairy alternatives, and ready-to-eat meals.

- Modified starch demand is expanding rapidly due to superior functional properties such as thickening, stabilization, and moisture retention.

- Asia-Pacific dominates global consumption, driven by large-scale food processing industries in China and India.

- Industrial applications are diversifying, particularly in biodegradable packaging, adhesives, and paper coatings.

- Clean-label and non-GMO starch solutions are reshaping product innovation strategies among manufacturers.

- Technological advancements in enzymatic processing are improving yield efficiency and lowering production costs.

What are the latest trends in the global starch market?

Shift Toward Clean-Label and Functional Ingredients

The starch industry is undergoing a transformation driven by consumer demand for transparency and natural ingredients. Food manufacturers increasingly prefer native and minimally processed starches that align with clean-label standards. Non-GMO corn starch, tapioca starch, and potato starch are gaining adoption across bakery, dairy alternatives, and plant-based foods. Manufacturers are reformulating products to eliminate synthetic stabilizers, replacing them with functional starches capable of delivering comparable texture and shelf-life performance. This trend is particularly strong in North America and Europe, where regulatory scrutiny and consumer awareness influence purchasing behavior. As a result, ingredient suppliers are investing heavily in specialty starch portfolios that meet labeling and sustainability expectations.

Expansion of Industrial and Biopolymer Applications

Beyond food applications, starch is increasingly used as a renewable raw material in industrial sectors. Paper manufacturing, textile sizing, corrugated board adhesives, and biodegradable plastics rely on starch-based formulations. Rising environmental regulations aimed at reducing petroleum-based polymers are accelerating starch adoption in compostable packaging solutions. Bio-based plastics incorporating starch blends are witnessing rapid commercialization, particularly across Europe and Asia-Pacific. Advances in chemical and enzymatic modification technologies are enabling starch to achieve improved durability and thermal stability, expanding its industrial usability and opening new revenue streams for producers.

What are the key drivers in the global starch market?

Growth of Processed and Convenience Food Consumption

Urbanization, rising disposable incomes, and changing dietary habits have accelerated consumption of processed foods worldwide. Starch functions as a critical ingredient in sauces, soups, snacks, bakery items, confectionery, and dairy products due to its thickening, binding, and stabilizing properties. Emerging economies, particularly in Asia and Latin America, are witnessing rapid expansion of packaged food manufacturing, directly increasing starch demand volumes. Foodservice expansion and frozen meal consumption further amplify industrial usage.

Technological Advancements in Modified Starch Production

Recent innovations in enzymatic and physical modification processes have enhanced starch functionality, allowing manufacturers to tailor viscosity, gelatinization temperature, and stability characteristics. These improvements support specialized applications such as instant foods, pharmaceutical excipients, and high-performance adhesives. Enhanced processing efficiency has also reduced production costs, enabling broader adoption across price-sensitive markets.

Rising Demand for Bio-Based Materials

Global sustainability initiatives and carbon reduction targets are driving substitution of petrochemical ingredients with renewable alternatives. Starch-based materials are increasingly utilized in biodegradable packaging, disposable tableware, and agricultural films. Government regulations promoting circular economy models further strengthen long-term demand for starch-derived polymers.

What are the restraints for the global market?

Volatility in Agricultural Raw Material Prices

Starch production heavily depends on crops such as corn, cassava, wheat, and potatoes. Climate variability, geopolitical trade disruptions, and fluctuating fertilizer costs can significantly influence raw material prices. These fluctuations affect production margins and pricing stability for starch manufacturers.

Competition from Alternative Hydrocolloids

Ingredients such as gums, pectins, and synthetic stabilizers compete with starch in certain applications. While starch remains cost-effective, specialty hydrocolloids sometimes offer superior performance under extreme processing conditions, creating competitive pressure in high-end formulations.

What are the key opportunities in the global starch market?

Biodegradable Packaging and Sustainable Materials

The transition toward sustainable packaging presents one of the strongest growth opportunities for starch producers. Governments worldwide are restricting single-use plastics, encouraging adoption of compostable alternatives. Starch-based polymers provide cost-effective and scalable solutions for packaging manufacturers. Companies investing in thermoplastic starch technologies are expected to gain competitive advantages as sustainability regulations tighten globally.

Expansion in Emerging Food Processing Economies

Rapid industrialization of food manufacturing across Southeast Asia, Africa, and Latin America creates substantial growth potential. Investments in cold chains, retail infrastructure, and modern supermarkets are increasing consumption of processed foods requiring starch ingredients. Local production facilities reduce import dependence, creating opportunities for both multinational and regional producers.

Specialty and Functional Starch Innovation

High-margin specialty starches designed for pharmaceutical, nutraceutical, and plant-based food applications represent a major opportunity area. Resistant starch for digestive health, encapsulation starches for flavors, and instant starches for convenience foods are gaining traction. Innovation-driven differentiation allows companies to command premium pricing and improve profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.42 Billion |

| Market Size in 2026 | USD 83.99 Billion |

| Market Size in 2031 | USD 118.35 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global starch market demonstrates a diversified product landscape shaped by evolving industrial processing requirements, functional food innovation, and cost-performance optimization across end-use sectors. While native starch continues to maintain substantial adoption due to its affordability and widespread availability, modified starch dominates globally, accounting for approximately 46% of the total market share in 2025. The leadership of modified starch is primarily driven by the increasing complexity of modern food manufacturing systems, which require ingredients capable of performing consistently under demanding processing conditions such as high heat, mechanical shear, freezing–thawing cycles, and acidic environments.Modified starches undergo physical, enzymatic, or chemical treatment processes that enhance stability, viscosity control, and resistance to retrogradation, making them indispensable in large-scale industrial production. Food manufacturers increasingly rely on these functional advantages to maintain uniform product texture, extend shelf life, and ensure stability throughout global supply chains that often involve long storage and transportation durations. The expansion of ready-to-eat meals, frozen foods, instant mixes, and convenience snacks has further strengthened demand for modified variants, as native starches alone often fail to meet performance expectations in these applications.In addition, the rise of clean-label innovation has encouraged the development of specialty modified starches derived through physical modification techniques rather than chemical treatments. These solutions allow manufacturers to balance consumer demand for recognizable ingredients with the technical functionality required in processed foods. As global food companies reformulate products to eliminate synthetic additives while maintaining product quality, modified starch continues to gain strategic importance as a multifunctional ingredient capable of replacing emulsifiers, stabilizers, and texturizers simultaneously.

Source Insights

The starch market is fundamentally influenced by agricultural raw material availability, regional cultivation economics, and processing efficiencies. Among all sources, corn-based starch leads globally, representing nearly 55% of total market share in 2025. Corn’s dominance stems from its high starch yield per hectare, well-established supply chains, and extensive cultivation infrastructure across major producing countries such as the United States, China, and Brazil. The scalability of corn wet milling technology enables manufacturers to produce multiple co-products—including sweeteners, ethanol, and animal feed—thereby improving operational economics and reinforcing corn’s competitive advantage.The leading segment driver for corn starch lies in its cost efficiency combined with versatile functionality across food, industrial, and bio-based applications. Food processors rely on corn starch for thickening, moisture retention, and texture enhancement, while industrial users employ it in paper coating, adhesives, and biodegradable materials. Additionally, the rapid growth of bioeconomy initiatives and renewable material development has increased the use of corn-derived starch in bioplastics and sustainable packaging solutions, further expanding its market leadership.Potato starch maintains a strong presence within specialized European applications where superior viscosity, clarity, and water-binding properties are essential. Its high amylopectin content provides unique functional advantages in premium food formulations, sauces, and processed meats. European manufacturers favor potato-based starch for clean-label positioning, as consumer preference for minimally processed ingredients continues to influence sourcing decisions.

Application Insights

Applications of starch span a wide spectrum of industries, though the food & beverage segment holds approximately 60% share of the global starch market, making it the dominant application category. The leading segment driver is the accelerating global demand for processed and convenience foods, fueled by urbanization, dual-income households, and changing dietary patterns that prioritize convenience without compromising sensory quality.Within food and beverages, starch functions as a thickener, stabilizer, moisture controller, and fat replacer across bakery products, dairy formulations, soups, sauces, snacks, confectionery, and ready meals. Bakery applications rely heavily on starch to improve crumb structure and shelf stability, while dairy producers utilize starch to enhance creaminess and prevent phase separation in yogurt and flavored milk beverages. The rapid expansion of plant-based alternatives has further strengthened starch demand, as manufacturers depend on starch matrices to replicate the texture and mouthfeel of animal-derived products.Emerging applications continue to broaden market scope. Functional nutrition products, sports supplements, and medical nutrition solutions incorporate resistant starch and modified carbohydrate systems to support digestive health and controlled energy release. These innovations highlight starch’s evolution from a traditional commodity ingredient into a technologically advanced functional component.

Function Insights

From a functional perspective, thickening and stabilizing properties represent the most significant use case, contributing nearly 38% of total starch consumption in 2025. The leading segment driver is the global food industry’s requirement for texture optimization and product consistency across large-scale manufacturing environments. Starch molecules interact with water during heating to form viscous gels, enabling manufacturers to achieve desired product viscosity while maintaining cost efficiency compared to alternative hydrocolloids.Stabilization functionality is particularly critical in emulsified products such as sauces, dressings, and dairy beverages, where starch prevents ingredient separation during storage. This capability enhances visual appeal and extends shelf life, both essential factors in modern retail distribution systems. Frozen foods rely on specially modified starches that maintain structural integrity during repeated freeze–thaw cycles, preventing syneresis and texture degradation.Advancements in starch chemistry have enabled the development of resistant starch varieties that function as dietary fiber, supporting gut health and glycemic control. As health-conscious consumers seek functional ingredients offering nutritional benefits alongside technical performance, starch functionality continues expanding into wellness-oriented product categories.

End-Use Industry Insights

The processed food industry represents the fastest-growing end-use sector for starch, expanding alongside global packaged food markets valued above USD 3 trillion. The leading segment driver is the ongoing transformation of global dietary habits toward convenience-oriented consumption patterns. Rapid urbanization, rising disposable incomes, and increased participation of working populations in emerging economies have intensified reliance on packaged meals and ready-to-cook products, all of which depend heavily on starch-based functional systems.Food manufacturers increasingly integrate starch to improve product yield, maintain sensory consistency, and reduce formulation costs. In plant-based meat analogues, starch plays a structural role by mimicking muscle fiber texture and improving water retention, enabling producers to deliver realistic meat substitutes. Functional nutrition and fortified foods also incorporate specialized starches to deliver controlled energy release and enhance digestive health benefits.Pharmaceutical applications are growing steadily as starch serves as a critical excipient in tablet manufacturing. Its binding, disintegration, and stabilization properties support drug delivery efficiency, particularly in controlled-release formulations. The expanding global pharmaceutical industry and increasing demand for generic medicines contribute to consistent growth within this segment.Emerging applications in biodegradable plastics and sustainable materials represent a long-term growth frontier. Governments and corporations pursuing carbon reduction targets are investing in bio-based polymers derived from starch feedstocks, creating new opportunities for market expansion beyond traditional food and industrial uses.

Explore more data points, trends and opportunities Download Free Sample Report

Starch Market Segmentations

By Source

- Corn (Maize) Starch

- Wheat Starch

- Potato Starch

- Cassava/Tapioca Starch

- Rice Starch

- Other Botanical Sources

By Type

- Native Starch

- Modified Starch

- Starch Derivatives

By Functionality

- Thickening Agents

- Stabilizers

- Binders

- Gelling Agents

- Texturizers

- Film-Forming & Coating Agents

By Application

- Food & Beverages

- Animal Feed

- Paper & Pulp

- Textile Processing

- Pharmaceuticals

- Personal Care & Cosmetics

- Bioplastics & Bio-based Materials

- Adhesives & Industrial Applications

By Distribution Channel

- Direct Industrial Sales

- Ingredient Distributors

- Food Ingredient Suppliers

- Online B2B Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 41% of global market share in 2025, making it the largest regional market for starch production and consumption. China and India serve as the primary growth engines, supported by massive population bases, expanding middle-class consumption, and rapid industrialization. China dominates regional demand due to its extensive processed food manufacturing sector, large-scale paper production industry, and integrated agricultural supply chains. The country’s investments in food security and domestic processing capacity continue to strengthen starch consumption across multiple industries.Regional growth drivers include rising disposable incomes, expanding food processing infrastructure, strong export-oriented manufacturing, and increasing adoption of biodegradable materials. The region’s role as both a production hub and consumption center positions Asia-Pacific as the most dynamic market globally.

North America

North America holds nearly 24% market share, led by the United States, which benefits from advanced agricultural productivity and sophisticated food processing capabilities. The region’s growth is primarily driven by innovation rather than volume expansion. Clean-label reformulation trends encourage manufacturers to replace synthetic additives with functional starch ingredients capable of delivering natural texture and stability.Another major regional driver is bio-industrial innovation. Companies are investing heavily in starch-derived bioplastics, renewable chemicals, and sustainable packaging solutions to meet environmental targets and regulatory expectations. Strong research and development ecosystems support continuous product innovation, particularly in specialty modified starches tailored for premium applications.High consumer awareness regarding health and wellness also drives demand for resistant starch and fiber-enriched foods. Additionally, the mature pharmaceutical sector contributes stable demand for pharmaceutical-grade starch excipients.

Europe

Europe represents a mature yet innovation-driven starch market led by Germany, France, and the Netherlands. Growth in the region is strongly influenced by sustainability regulations and circular economy initiatives encouraging biodegradable packaging adoption. European Union policies promoting renewable raw materials have accelerated the use of starch in bio-based plastics and environmentally friendly adhesives.The leading regional growth driver is sustainability-led product innovation. Food manufacturers increasingly adopt specialty starches that enable clean-label claims while maintaining premium product quality. Potato starch remains particularly important due to regional agricultural strengths and consumer preference for locally sourced ingredients.Europe’s advanced food technology sector continues to develop functional starch solutions supporting plant-based foods, reduced-fat formulations, and sugar reduction initiatives. These innovation trends sustain steady market expansion despite overall market maturity.

Middle East & Africa

The Middle East and Africa region is emerging as a high-growth market supported by demographic expansion, urbanization, and rising dependence on processed food imports. Countries such as Saudi Arabia and South Africa serve as key consumption hubs due to growing retail infrastructure and expanding bakery and confectionery industries.Regional growth drivers include increasing population growth, rising tourism-related food demand, and investments in food security initiatives aimed at reducing supply chain vulnerabilities. As local food processing industries expand, demand for starch ingredients used in bakery products, sauces, and convenience foods continues to rise.Industrialization efforts and packaging sector development further contribute to starch consumption, particularly within paperboard and corrugated packaging applications supporting regional trade growth.

Latin America

Latin America, led by Brazil and Mexico, demonstrates steady expansion supported by strong agricultural resources and growing processed food industries. Abundant corn production provides a stable raw material base, enabling competitive starch manufacturing costs and regional self-sufficiency.Key regional growth drivers include expanding urban populations, increasing exports of processed foods, and rising investment in food manufacturing infrastructure. Brazil’s integrated agribusiness sector strengthens domestic starch availability, while Mexico’s proximity to North American supply chains encourages industrial collaboration and trade-driven demand.Additionally, growing awareness of sustainable materials and bio-based products is encouraging adoption of starch in biodegradable packaging and industrial applications, positioning Latin America as an increasingly important contributor to global market growth.

Key Players in the Global Starch Market

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- AGRANA Beteiligungs-AG

- Tereos Group

- Grain Processing Corporation

- BENEO GmbH

- Global Bio-Chem Technology Group

- SMS Corporation

- Südzucker AG

- Visco Starch

- Emsland Group

- Universal Starch Chem Allied Ltd.